TL;DR: Best Gold Investment Options for Beginners

- The Traditional Trap: Buying physical 22K jewelry or 24K coins is the absolute worst way to invest for a beginner. Making charges (which can go up to 25%) and a mandatory 3% GST instantly put your investment at a massive loss on day one.

- The SIP Winner (Gold ETFs & Mutual Funds): If you want to invest a small amount like Rs. 1,000 every month, Gold ETFs or Gold Mutual Funds are your best option. They offer instant liquidity, zero making charges, and unlock a 12.5% Long-Term Capital Gains (LTCG) tax rate after just 12 months.

- The Lump-Sum Winner (Sovereign Gold Bonds): If you have Rs. 50,000 sitting in the bank and do not need to touch it for 8 years, SGBs are the undisputed king. You get the benefit of gold price appreciation plus an extra 2.5% fixed interest paid directly to your bank account every year.

- The Micro-Investing Tool (Digital Gold): Buying gold on UPI apps is great if you only have Rs. 100 to spare, but beware of the hidden 3% buying spread that eats into your profits.

Note: Always align your gold investment with your specific time horizon. Financial experts recommend keeping your total gold allocation to 10%-15% of your overall investment portfolio.

1. Overcoming “Gold Confusion”

You finally got your first real paycheck. After treating yourself and paying your bills, you decide it is time to be a responsible adult and start investing. You want to play it safe, so you decide to invest in gold.

But the moment you try to actually buy some, you are completely paralyzed by choice.

Your mom is telling you to go down to the family jeweler and buy a 24-karat gold coin to keep in the bank locker. Your finance-bro friend is telling you to open a demat account and buy a “Gold ETF.” Meanwhile, your phone keeps buzzing with notifications from UPI apps telling you to buy “Digital Gold” for just Rs. 10.

If you are a beginner in 2026, the sheer number of ways to buy gold is overwhelming. And here is the harsh truth: not all gold investments are created equal.

If you choose the wrong method, you could end up paying thousands of rupees in hidden taxes, making charges, and storage fees, effectively destroying your returns before you even start. This guide is going to cut through the noise, strip away the financial jargon, and give you the definitive answer on exactly where you should put your money based on your actual budget.

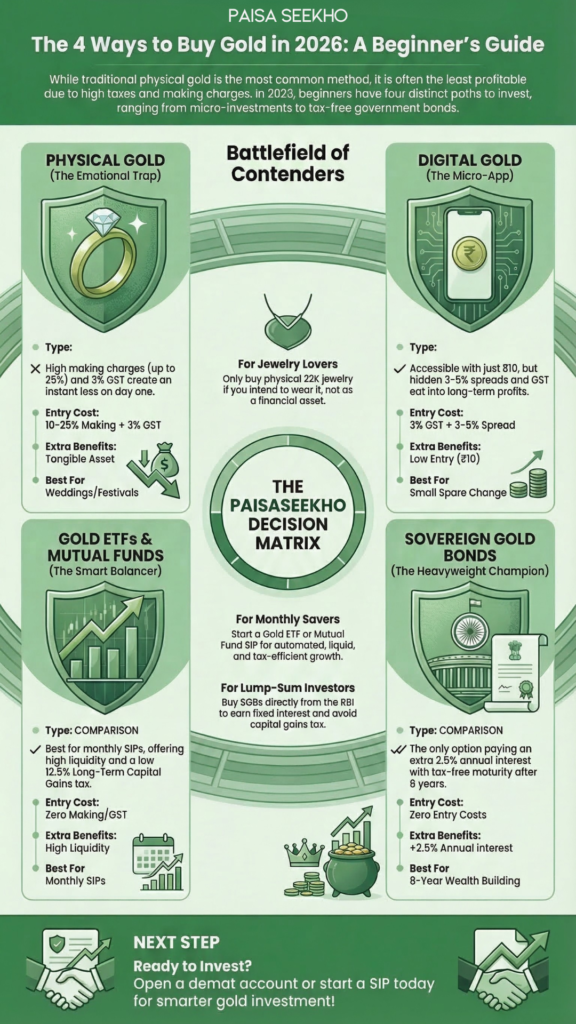

2. The 4 Ways to Buy Gold in 2026 (The Battlefield)

To figure out the best option, you first need to know what you are dealing with. In 2026, the Indian gold market is divided into four distinct contenders:

- Physical Gold: The traditional jewelry, coins, and biscuits.

- Digital Gold: The micro-investing feature found on popular UPI and payment apps.

- Paper Gold: Gold ETFs and Gold Mutual Funds traded on the stock market.

- Government Gold: Sovereign Gold Bonds (SGBs) issued directly by the Reserve Bank of India.

Let’s break them down one by one, expose their hidden flaws, and declare the ultimate winner for beginners.

3. Contender 1: Physical Gold (The Emotional Trap)

This is the method our parents and grandparents relied on. You walk into a brightly lit showroom, pick out a beautiful 22K gold chain or a shiny 24K gold coin, hand over your cash, and walk out with the metal in your pocket.

It feels safe because you can actually touch it. But mathematically, it is a beginner’s worst nightmare.

The Pros:

- High Emotional Value: It feels incredibly satisfying to hold your wealth in your hands.

- No Technology Needed: You do not need a smartphone, a demat account, or an internet connection to buy it.

The Cons (The Paisaseekho Math):

- The Sunk Costs: The second the jeweler prints your bill, you are charged a mandatory 3% GST. On top of that, you have to pay “making charges” for the labor, which usually range from 10% to 25% of the total gold value.

- Instant Loss: If you buy a Rs. 50,000 gold coin and try to sell it back to the exact same jeweler five minutes later, they will only pay you for the raw weight of the gold. The GST and making charges are gone forever. You instantly lose around 15% of your money’s value on day one.

- The Storage Tax: You cannot leave physical gold sitting on your kitchen counter. You have to rent a bank locker to prevent theft, which costs thousands of rupees every single year, eating directly into whatever tiny profit you might have made.

The Verdict: Never use physical gold as a pure financial investment. Only buy physical jewelry if you actually plan to wear it for weddings or festivals. If your goal is to grow your wealth, keep reading.

4. Contender 2: Digital Gold (The Micro-App)

If you have ever used a UPI app like PhonePe, Google Pay, or Paytm, you have definitely seen the shiny banner urging you to “Buy 24K Gold for just Rs. 10!”

Digital Gold allows you to buy microscopic fractions of real, physical 24K gold. When you hit buy, a partner company (like MMTC-PAMP or SafeGold) purchases the equivalent amount of physical gold and locks it in a highly secure, insured vault under your name.

The Pros:

- The Ultimate Micro-Investment: You do not need to save up Rs. 70,000 for a 10-gram coin. You can literally invest the Rs. 50 cashback you just won. It is the most accessible entry point for absolute beginners.

- Zero Storage Hassle: You don’t have to worry about bank lockers or theft. The vaulting companies handle all the security.

The Cons (The Hidden Spread):

- The 3% GST Hit: Every time you buy Digital Gold, a mandatory 3% GST is instantly slapped onto your purchase price.

- The Buy-Sell Spread: This is the silent killer. If you open your app right now, you will notice that the “Buy Price” of gold is always significantly higher than the “Sell Price” (usually a difference of 3% to 5%). This spread covers the platform’s fees, insurance, and vault storage.

- Instant Loss: Because of the GST and the spread, your investment is automatically down by almost 6% to 8% the exact second you buy it. The price of gold has to rise significantly just for you to break even.

The Verdict: Digital Gold is a fun novelty. It is a great place to park your spare pocket change instead of spending it on junk food, but the hidden spreads make it a terrible vehicle for serious, long-term wealth building.

5. Contender 3: Gold ETFs & Mutual Funds (The Smart Balancer)

Now we are entering the territory of real financial planning.

Paper Gold includes Gold ETFs (Exchange Traded Funds) and Gold Mutual Funds. Instead of buying a physical piece of metal, you buy “units” of a fund on the stock market. The fund manager takes your money, buys pure 24K physical gold bullion, and stores it in an audited vault. Your units represent your exact share of that massive gold bar.

The Pros:

- Zero Toxic Costs: There are no making charges, no hidden spreads, and absolutely zero 3% physical GST to pay when you buy.

- Ultimate Liquidity: If you have an emergency and need cash instantly, you can sell your Gold ETF units on your brokerage app (like Zerodha or Groww) in exactly two seconds during market hours. The cash hits your account almost immediately.

- The 2026 Tax Advantage: Following recent budget updates, Gold ETFs are incredibly tax-efficient. You only need to hold them for 12 months to unlock the lowest 12.5% Long-Term Capital Gains (LTCG) tax rate.

The Cons:

- Demat Account Required: You cannot buy a Gold ETF without opening a proper stockbroking demat account. (Though you can buy a Gold Mutual Fund without one, which acts almost identically but with slightly higher management fees).

- No Passive Income: Like physical gold, it doesn’t pay you interest. Your only profit comes from the price going up.

The Verdict: This is the absolute best option for beginners who want to set up a monthly SIP (Systematic Investment Plan). If you want to automatically invest Rs. 1,000 every month, buy a Gold Mutual Fund or Gold ETF. It is cheap, highly liquid, and incredibly tax-efficient.

6. Contender 4: Sovereign Gold Bonds (The Heavyweight Champion)

If Gold ETFs are the smart balancer, Sovereign Gold Bonds (SGBs) are the heavyweight champion of the gold world.

Issued directly by the Reserve Bank of India (RBI) on behalf of the government, SGBs are essentially a loan you give to the government. In return, they give you a digital certificate denominated in grams of gold.

The Pros:

- The Double Profit: This is the only gold investment on the planet that actually pays you to hold it. You get the full profit of the gold price rising over time, PLUS the government pays you an extra 2.5% fixed interest directly into your bank account every single year.

- Tax-Free Maturity: If you buy the bond directly from the RBI during a fresh issue window (as an original subscriber) and hold it for the full 8-year term, your capital gains tax is exactly zero.

- Zero Costs: No GST, no making charges, no storage fees, and no expense ratios.

The Cons:

- The 8-Year Lock-In: Your money is locked away for 8 years. While you can technically sell them on the stock market earlier (after 5 years), the trading volume is very low, meaning you might have to sell at a massive discount if you are desperate for cash. Plus, selling early ruins the tax-free maturity benefit.

The Verdict: SGBs are the undisputed king if you have a lump sum of cash (like a Diwali bonus or a fixed deposit maturing) that you absolutely do not need to touch for the next decade.

7. Conclusion: The Ultimate Beginner’s Decision Matrix

If you have made it this far, you now know that buying gold is not just about walking into a store and handing over cash. It is about matching the type of gold to your specific financial goals.

To make this completely foolproof, do not guess. Just follow this strict Paisaseekho “If This, Then That” rulebook:

- If you have Rs. 1,000 a month to invest -> Start a Gold ETF or Mutual Fund SIP. It is cheap, highly liquid, completely automated, and unlocks the 12.5% LTCG tax rate after just 12 months.

- If you have a Rs. 1 Lakh bonus and won’t touch it for 8 years -> Buy an SGB directly from the RBI. You get the price appreciation, zero capital gains tax on maturity, plus an extra Rs. 2,500 in interest every single year just for holding it.

- If you are saving for a wedding in 2 years -> Buy a Gold Mutual Fund. You need high liquidity so you can cash out the exact week you need to pay the jewelers, without worrying about the 8-year SGB lock-in.

- If you literally want to wear it on Diwali -> Buy physical 22K jewelry. Just remember, you are buying a beautiful accessory, not a high-growth financial asset. Accept the making charges and enjoy it!

Your Next Step: If your goal is wealth creation, skip the jewelry store this weekend. Open your demat account (like Zerodha, Groww, or Upstox) or your mutual fund app, and set up your very first Rs. 500 SIP into a Gold ETF or Gold Mutual Fund. The best time to start hedging your portfolio against inflation is today!

Top 10 Frequently Asked Questions

1. Which is the best way to invest in gold for beginners?

For a beginner looking to invest small amounts regularly, Gold ETFs or Gold Mutual Funds are the best options. They offer high liquidity, zero making charges, and you can start with as little as Rs. 500 per month through a SIP.

2. Is Digital Gold on UPI apps a safe investment?

Yes, it is safe because your purchase is backed by real 24K gold stored in insured vaults by companies like MMTC-PAMP. However, it is not a good long-term investment because of the hidden 3% buy-sell spread and mandatory 3% GST that instantly eats into your profits.

3. What is the difference between a Gold ETF and a Gold Mutual Fund?

A Gold ETF requires a demat account and is traded on the stock exchange in real-time like a stock. A Gold Mutual Fund is a fund that invests in Gold ETFs; it does not require a demat account, making it easier for absolute beginners, but it charges a slightly higher annual expense ratio.

4. Are Sovereign Gold Bonds (SGBs) better than physical gold?

Financially, yes! SGBs track the same 24K gold price but completely eliminate making charges, GST, and locker fees. Most importantly, the government pays you an extra 2.5% fixed interest every year, and your profits are tax-free if you hold the bond for 8 years.

5. Why shouldn’t I buy physical 24K gold coins for investment?

When you buy physical coins, you instantly lose money to a 3% GST and jeweler making charges (which can be up to 10%). When you sell the coin back, the jeweler only pays for the metal weight, meaning you start your investment at a massive loss.

6. Can I sell my Sovereign Gold Bond before 8 years?

Yes, but it is difficult. While SGBs are listed on the stock exchange and can be traded, the trading volume (liquidity) is very low. You might have to sell it at a heavy discount if you need emergency cash. If you need liquidity, stick to Gold ETFs.

7. What taxes do I pay on Gold Mutual Funds in 2026?

If you hold your Gold Mutual Fund (or physical gold) for more than 24 months, your profits are taxed at 12.5% as Long-Term Capital Gains (LTCG). If you sell before 24 months, the profits are added to your income slab. (Note: Gold ETFs only require a 12-month holding period for LTCG!).

8. Is Rs. 1,000 a month enough to invest in gold?

Absolutely! Rs. 1,000 a month invested via a SIP into a Gold ETF or Mutual Fund is the perfect way to build a financial safety net over time without straining your monthly budget.

9. What percentage of my portfolio should be in gold?

Most financial experts recommend keeping your total gold allocation to 10% to 15% of your net worth. Gold is a defensive asset designed to protect your wealth against inflation, while your equity mutual funds and stocks are meant to aggressively grow it.

10. Do I get physical gold when my SGB matures?

No. Sovereign Gold Bonds are cash-settled. When the 8-year term ends, the RBI looks at the current market price of 24K physical gold and deposits the equivalent cash value directly into your registered bank account.