TL;DR: Key Takeaways on the New Credit Guarantee Scheme

If you are short on time, here is a quick summary of the proposed financial relief package:

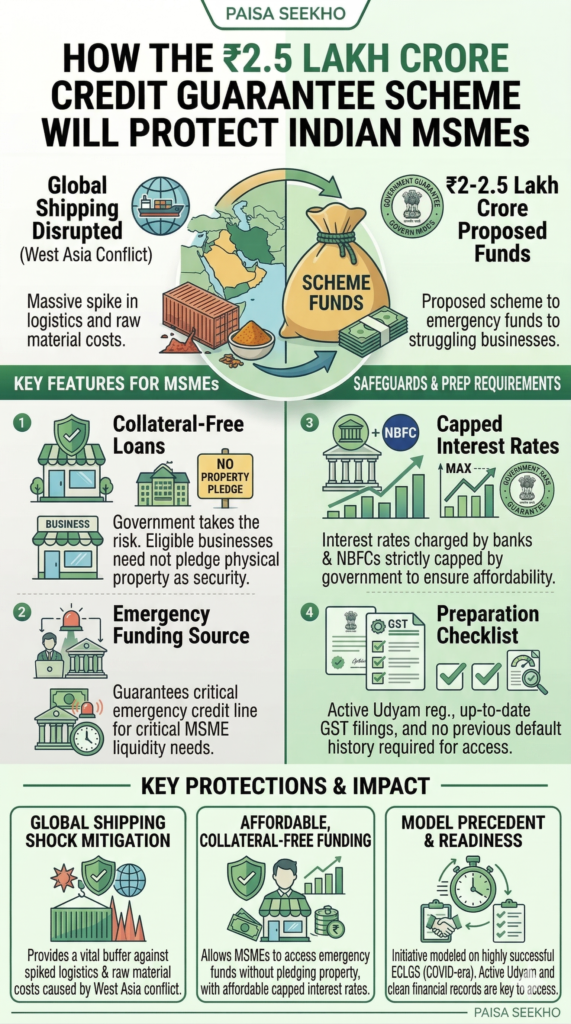

- The Crisis: The worsening West Asia conflict has disrupted global shipping routes, causing a massive spike in logistics and raw material costs for Indian businesses.

- The Solution: The government is proposing a ₹2-2.5 lakh crore credit guarantee scheme to provide emergency funding to struggling MSMEs.

- Collateral-Free: Under this scheme, eligible businesses can get emergency loans from banks without having to pledge any physical property or assets as security. The government takes the risk.

- The Precedent: This new initiative is heavily modeled on the highly successful Emergency Credit Line Guarantee Scheme (ECLGS) launched during the COVID-19 pandemic in 2020.

- Interest Rate Caps: To ensure the loans are actually affordable, the interest rates charged by banks and Non-Banking Financial Companies (NBFCs) will be strictly capped by the government.

- Preparation is Key: To access these funds, MSMEs must ensure their Udyam registration is active, their GST filings are up to date, and they do not have a history of defaulting on previous loans.

Introduction

Running a small business in India is already a challenging endeavor. You have to manage cash flows, handle delayed payments from clients, and navigate a highly competitive market. But what happens when a geopolitical crisis thousands of miles away suddenly threatens to shut down your operations?

In April 2026, the escalating conflict in West Asia sent shockwaves through the global economy. For Indian Micro, Small, and Medium Enterprises (MSMEs), this external shock translated into a severe liquidity crunch. Freight costs skyrocketed, supply chains were disrupted, and the price of raw materials surged overnight.

Recognizing that millions of jobs and the backbone of the Indian economy were at risk, the government stepped in with a massive financial shield: the proposed ₹2.5 Lakh Crore Credit Guarantee Scheme.

If you own a small business, work in the manufacturing sector, or simply want to understand how the government protects the economy during a global crisis, this comprehensive guide will break down everything you need to know. We will explain exactly how this scheme works, who is eligible, and how it mirrors the historic financial rescue packages of the past.

1. The Impact of West Asia Conflict and Supply Chain Chaos

To understand why the government is unlocking ₹2.5 lakh crore, you first have to understand the magnitude of the problem facing Indian businesses today.

The Indian economy does not operate in a vacuum. We are deeply connected to the global supply chain. A massive percentage of India’s exports and imports travel through the shipping lanes of the Middle East and the Red Sea. With the severe escalation of the West Asia conflict in early 2026, these vital trade routes have become incredibly dangerous and unpredictable.

Here is how a war in another continent directly hurts an MSME in India:

- Skyrocketing Freight Costs: Because the primary shipping lanes are disrupted, commercial cargo ships are forced to take much longer, alternative routes around the globe. This requires more fuel and more time, causing the cost of shipping a single container to double or triple.

- Delayed Payments: If an Indian manufacturer ships a container of goods to Europe, it now takes weeks longer to arrive. Because the buyer does not pay until the goods are received, the Indian business owner is left waiting for their cash, completely destroying their monthly working capital cycle.

- Rising Input Costs: India imports massive amounts of raw materials, including crude oil, specialty chemicals, and electronic components. The war has caused global commodity prices to spike, meaning Indian factories have to pay significantly more just to manufacture their products.

When a small business has to pay more for raw materials but is receiving its payments weeks late, it runs out of cash. It cannot pay its employees, it cannot pay its electricity bills, and it eventually shuts down. The government had to act fast to prevent this scenario.

2. What Exactly is a Credit Guarantee Scheme?

When the news announces a “₹2.5 Lakh Crore Scheme,” many people misunderstand how the money actually works. The government is not simply printing ₹2.5 lakh crore and handing it out as free cash to business owners.

Instead, the government is providing a Guarantee.

Normally, if a small business owner walks into a bank and asks for a ₹50 Lakh emergency loan, the bank manager will ask for “collateral.” They will ask the business owner to pledge their house, their factory machinery, or their land as security. If the business goes bankrupt and cannot repay the loan, the bank seizes the property so they do not lose money.

During a massive global crisis, business owners do not have any extra property to pledge. They are already financially stretched. Furthermore, banks become very scared to lend money during a war because they know the risk of businesses failing is very high.

This is where the Credit Guarantee Scheme steps in.

The government tells the banks: “Lend emergency working capital to these struggling MSMEs without asking them for any collateral. If the MSME goes bankrupt and cannot repay you, the Government of India guarantees that we will pay you back 100% of the lost money.”

This is the ultimate financial safety net. It instantly removes the fear from the banking system. Because the bank knows the government is backing the loan, they gladly open their checkbooks and provide immediate, life-saving cash to the businesses that desperately need it.

3. Impact of ECLGS on the Credit Guarantee Scheme 2026

If this strategy sounds familiar, it is because we have seen it work perfectly before. The new 2026 scheme is being heavily modeled on the historic Emergency Credit Line Guarantee Scheme (ECLGS), which was launched in May 2020 during the peak of the COVID-19 pandemic lockdowns.

During Covid-19, the entire country was shut down. Factories were closed, and zero revenue was coming in, but business owners still had to pay rent and salaries.

The government launched the ECLGS to pump emergency liquidity into the market. The results of that 2020 scheme were absolutely phenomenal and provide a clear blueprint for how the 2026 West Asia conflict scheme will operate:

- The 2020 scheme successfully issued guarantees amounting to over ₹3.62 lakh crore.

- It benefited over 11.9 million borrowers, allowing them to survive the lockdowns.

- According to a massive research report by the State Bank of India (SBI), the ECLGS directly saved MSME loan accounts worth ₹1.8 trillion from slipping into Non-Performing Assets (NPAs).

- Most importantly, the scheme ensured that over 1.35 million individual MSME units survived, saving millions of jobs that would have otherwise vanished permanently.

By dusting off the ECLGS playbook, the Finance Ministry and the RBI are using a battle-tested financial weapon. The infrastructure to deliver these loans through public and private banks is already in place, meaning the money can reach the business owners in a matter of days, not months.

4. Who Will Actually Benefit From The 2.5 Lakh Crore Credit Guarantee Scheme?

The ₹2.5 Lakh Crore Credit Guarantee Scheme is not meant for massive, multi-billion-dollar corporations. Companies like Reliance or Tata have massive cash reserves and their own ability to weather geopolitical storms. This scheme is strictly targeted at the vulnerable middle layer of the economy.

Export-Oriented Units

The businesses taking the heaviest hits from the West Asia conflict are the ones that export goods. Whether it is a textile factory in Tiruppur shipping garments to the UK, or an auto-parts manufacturer in Pune exporting to Germany, these companies are bearing the full brunt of the Red Sea shipping crisis. The scheme will heavily prioritize these export-oriented units to ensure India does not lose its footprint in global trade.

The Manufacturing Sector

Factories that rely on imported raw materials are facing severe stress. If a plastic manufacturer cannot afford the suddenly expensive petroleum by-products needed to make their goods, the entire factory comes to a halt. Emergency credit lines will allow these manufacturers to absorb the higher input costs without shutting down their assembly lines.

Retail and Wholesale Traders

During the Covid-era schemes, the government eventually expanded the definition of MSMEs to include retail and wholesale traders. Because traders also face massive inventory delays and working capital blockages during supply chain disruptions, they are widely expected to be eligible for emergency top-up loans under the 2026 framework.

5. How the Collateral-Free Loans Will Work

While the final, official notification of the 2026 scheme is currently being drafted by the Finance Ministry, industry bodies like the Confederation of Indian Industry (CII) and banking executives have indicated that the mechanics will closely mirror past emergency schemes. Here is what MSME owners can expect:

Automatic Pre-Approved Limits

The government wants to eliminate red tape. If an MSME already has an existing loan with a bank, they will not have to fill out massive stacks of new paperwork. The banks will automatically offer a “top-up” loan. For example, the scheme might dictate that an MSME can instantly borrow an additional 20% of their outstanding total debt as an emergency working capital term loan.

Strict Interest Rate Caps

If a bank gives you an emergency loan but charges you a 20% interest rate, it isn’t a rescue package; it is a debt trap. To prevent banks from exploiting desperate business owners, the government enforces strict interest rate caps on these guaranteed loans. During the previous ECLGS, interest rates were strictly capped at 9.25% per annum for banks and 14% per annum for NBFCs. You can expect similar, highly affordable rate caps in the new 2026 rollout.

The Moratorium Period

When a business is fighting to survive a war-induced supply shock, they cannot afford to start paying back a new loan immediately. These emergency credit lines typically come with a “Moratorium.” A moratorium is a grace period. For example, the government might grant a 1-year moratorium on principal repayment. This means for the first 12 months, the business owner only has to pay the small monthly interest, giving them a full year to stabilize their business before they have to start paying back the main loan amount.

Zero Guarantee Fees

Usually, when a government trust (like the Credit Guarantee Fund Trust for Micro and Small Enterprises – CGTMSE) guarantees a loan, they charge the business owner a small annual “guarantee fee” (around 0.50% to 1%). However, under specialized emergency schemes, the government typically waives this fee entirely to ensure the business owner faces absolutely zero extra financial burden.

6. How The MSME Scheme Will Help With Saving Jobs and the Indian Economy

You might wonder why the government is willing to risk ₹2.5 lakh crore of taxpayer liability to save private businesses. It is because allowing the MSME sector to collapse would trigger an economic catastrophe.

MSMEs are the absolute beating heart of the Indian economy. They contribute roughly 30% to India’s total Gross Domestic Product (GDP) and account for over 45% of the country’s total exports. More importantly, the MSME sector is the second-largest employer in the country after agriculture, providing jobs to over 11 crore (110 million) workers.

If the government does not intervene:

- Struggling factories shut down.

- Millions of lower-middle-class and daily wage workers lose their jobs.

- Without an income, these workers stop buying consumer goods, causing the broader retail economy to crash.

- The businesses default on their massive bank loans, turning them into Non-Performing Assets (NPAs).

- The banks lose billions of rupees, causing a full-blown banking crisis that hurts regular citizens’ savings.

By injecting a highly targeted ₹2.5 lakh crore credit guarantee, the government breaks this deadly chain reaction at the very first step. It is a brilliant, highly leveraged macroeconomic strategy. A temporary emergency loan keeps the factory open, keeps the worker employed, and keeps the banking sector completely insulated from the geopolitical chaos happening in West Asia.

7. Step-by-Step: How MSME Owners Can Prepare to Apply

When the government officially opens the window for the ₹2.5 Lakh Crore Credit Guarantee Scheme in the coming weeks, millions of businesses will rush to their banks. The banking servers will be flooded with requests. If you want to ensure your business receives its emergency funds quickly, you need to have your financial house in perfect order today.

Here is a checklist to prepare for the application process:

1. Update Your Udyam Registration

To qualify for any government MSME benefit, your business must be officially registered on the government’s Udyam portal. If you have not registered, do it immediately. It is completely free and completely digital. If you are already registered, log in and ensure your classification (Micro, Small, or Medium) is accurate based on your latest investment and turnover figures.

2. File Your Pending GST Returns

Banks will use your GST data to verify your revenue and calculate your eligible loan amount. If you have delayed filing your monthly or quarterly GST returns, clear the backlog immediately. A clean, up-to-date GST dashboard proves to the bank that your business is legitimate and operational.

3. Do Not Default on Existing EMIs

This is the most critical rule. Emergency credit guarantee schemes are designed to help healthy businesses survive a temporary external shock. They are not designed to bail out businesses that were already failing. If your account is classified as an NPA (Non-Performing Asset) or SMA-2 (Special Mention Account – severely delayed payments) before the scheme is announced, you will likely be completely disqualified. Do whatever it takes to keep your current EMIs paid on time so your CIBIL and commercial credit scores remain clean.

4. Prepare a Working Capital Projection

Don’t just ask the bank for a random amount of money. Sit down with your accountant and calculate exactly how much the West Asia shipping delays are costing you. Calculate your blocked inventory, your increased freight costs, and your monthly fixed expenses (rent and payroll). Having a clear, mathematical projection of your working capital gap will make the bank manager’s job much easier and speed up your loan approval.

8. The Role of the RBI and Industry Bodies

The creation of this ₹2.5 Lakh Crore scheme is a massive collaborative effort between the government, the Reserve Bank of India (RBI), and powerful industry bodies like the Confederation of Indian Industry (CII).

In the days leading up to the announcement, the CII actively lobbied the Finance Ministry, presenting a 20-point agenda highlighting the desperate need for targeted liquidity support, a temporary moratorium on restructuring, and a special forex swap facility to shield oil marketing companies from supply shocks.

Simultaneously, the RBI plays the role of the ultimate regulator. While the government provides the guarantee, the RBI must ensure there is enough actual cash liquidity in the banking system so that banks can actually disburse the ₹2.5 lakh crore. The RBI achieves this through open market operations and tweaking priority sector lending norms, ensuring the financial pipes remain fully open and functional.

Conclusion: A Shield for India Inc.

The world is becoming increasingly volatile, and the shocks of geopolitical conflicts now reach every corner of the globe in a matter of days. For a young, ambitious Indian entrepreneur, navigating these external crises can feel like an impossible task.

The ₹2.5 Lakh Crore Credit Guarantee Scheme proves that the Indian financial system has matured. Instead of reacting with panic, the government is proactively deploying a proven, data-driven financial shield. By providing 100% collateral-free, low-interest emergency capital, they are ensuring that a war in West Asia does not destroy the dreams and livelihoods of millions of Indian MSME owners.

If you run a business, keep a close eye on the official notifications from your bank in the coming weeks. Prepare your documents, calculate your needs, and use this emergency credit line exactly as it was intended: as a bridge to carry your business safely over the turbulent waters of the current global crisis.

Frequently Asked Questions (FAQs): MSME Credit Guarantee Scheme 2026

Q1: Is the ₹2.5 Lakh Crore Credit Guarantee Scheme a free grant from the government?

No, it is not free money. It is a loan provided by your bank that you must repay with interest. The government’s role is simply to provide a “guarantee” to the bank, meaning the bank will not ask you for collateral (like your house or machinery) to approve the loan.

Q2: Who is eligible to apply for this emergency scheme?

While the exact guidelines are being finalized, the scheme is targeted at officially registered Micro, Small, and Medium Enterprises (MSMEs). Priority will be given to export-oriented units, manufacturing businesses, and traders who are directly facing a liquidity crunch due to the supply chain disruptions caused by the West Asia conflict.

Q3: Do I have to pledge any property to get this loan?

No. The defining feature of this emergency scheme is that the loans are 100% collateral-free. The Government of India acts as your guarantor, taking on the risk so you do not have to put your personal or business assets on the line.

Q4: What is the maximum interest rate the bank can charge me under this scheme?

To protect MSMEs from high costs, the government enforces strict interest rate caps. Based on previous emergency schemes (like the ECLGS), interest rates are expected to be capped at a maximum of 9.25% per annum for standard banks and around 14% per annum for Non-Banking Financial Companies (NBFCs).

Q5: Can I use this loan to buy a new house or a personal car?

Absolutely not. This is strictly an emergency working capital loan. The funds must be used exclusively to meet the operational liabilities of your business—such as paying employee salaries, clearing vendor dues, paying factory rent, or covering increased shipping and raw material costs.

Q6: What happens if my business was already failing before the West Asia conflict started?

If your business loan account was already classified as a Non-Performing Asset (NPA) or you had a severe history of defaulting on your EMIs before the crisis hit, you will likely not be eligible for this scheme. The government guarantee is designed to support fundamentally healthy businesses that are facing a temporary external shock.

Q7: Is it mandatory to have an Udyam Registration to get this loan?

Yes. To be officially recognized as an MSME by the banking system and the government, you must have an active Udyam Registration Certificate. If you do not have one, you should register your business immediately on the official government Udyam portal.

Q8: What is a “Moratorium” and will this loan have one?

A moratorium is a legally approved “grace period” where you do not have to make full EMI payments. Emergency credit schemes typically include a moratorium of 6 to 12 months on the principal amount. During this time, you only pay the monthly interest, which gives your business time to stabilize before you start paying back the main loan amount.

Q9: Do I need to apply for a brand new loan, or can my current bank just give me the money?

The fastest and easiest way to get this money is through your existing bank where you already have a business loan or a current account. The scheme is designed as a “top-up” facility, meaning your existing bank will pre-approve you for an additional percentage (e.g., 20%) of your current outstanding credit limit.

Q10: Are retail and wholesale shop owners eligible for this scheme?

Yes. In 2021, the government officially revised the guidelines to include retail and wholesale traders under the MSME category for the purpose of Priority Sector Lending. Because traders are also heavily impacted by delayed inventory and shipping costs, they will be eligible to seek relief under this new credit guarantee framework.