When it comes to securing the future of our daughters, financial planning plays a crucial role. The Sukanya Samriddhi Yojana (SSY) is a savings scheme introduced by the Government of India to help parents build a financial safety net for their daughters. Designed to encourage saving for a girl child’s education and marriage, this scheme offers attractive interest rates and significant tax benefits, making it an excellent choice for parents looking to invest in their daughter’s future.

The SSY scheme is not just about saving money; it symbolizes empowerment and the importance of investing in the future of girls. By ensuring that your daughter has the funds she needs for her education or marriage, you are paving the way for her to lead an independent and successful life. In this guide, we will explore what the Sukanya Samriddhi Yojana is, how it works, and why it could be the perfect investment option for your family.

What is Sukanya Samriddhi Yojana (SSY) Scheme?

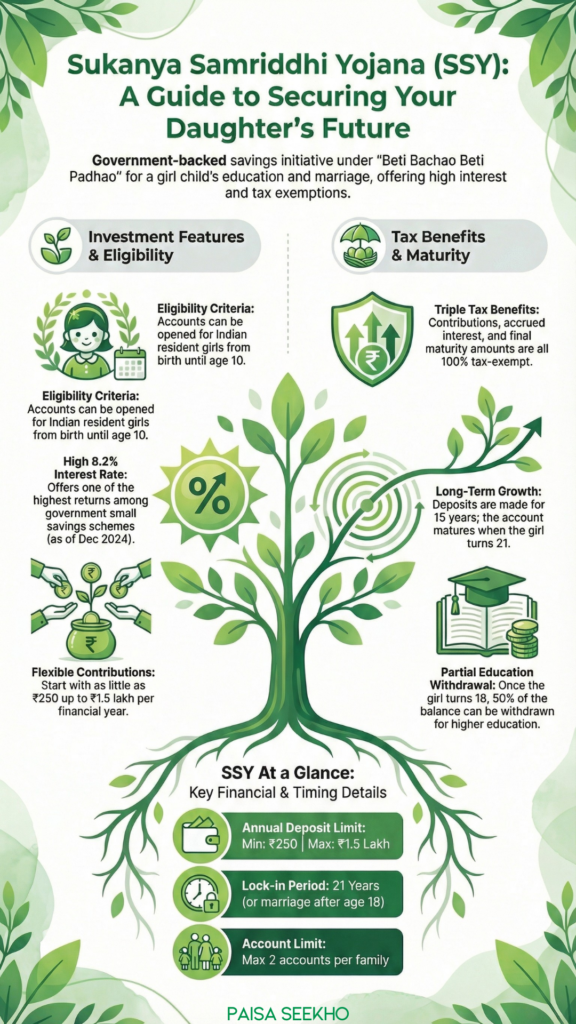

The Sukanya Samriddhi Yojana (SSY) is a small savings scheme launched by the Government of India as part of the Beti Bachao Beti Padhao initiative. It is designed to promote savings for the education and marriage expenses of a girl child. The scheme allows parents or legal guardians to open an SSY account in the name of their daughter, ensuring that a substantial corpus is available when she reaches adulthood.

The interest rate offered by the SSY scheme is usually higher than other small savings schemes, making it an attractive choice for parents. Currently, the interest rate stands at 8.2% (as of December 2024). Additionally, the scheme provides tax benefits under Section 80C of the Income Tax Act, allowing parents to save on their tax liabilities while building a secure future for their daughter. Withdrawals from the SSY account are allowed under specific conditions, such as funding higher education expenses once the girl turns 18, making it a flexible and practical investment option for families.

Key Features of Sukanya Samriddhi Yojana

- High Interest Rate: The SSY scheme offers a higher interest rate compared to other small savings schemes, making it a lucrative savings option.

- Tax Benefits: Contributions to the SSY account are eligible for tax deductions under Section 80C of the Income Tax Act, up to a maximum limit of ₹1.5 lakh per year.

- Long-Term Savings: Contributions can be made for up to 15 years from the date of opening the account, and the account matures when the girl turns 21 years old.

- Partial Withdrawals: Partial withdrawals are allowed after the girl turns 18, which can be used to fund her higher education.

- Minimum and Maximum Contributions: The minimum contribution is ₹250 per year, while the maximum contribution is ₹1.5 lakh per year.

- Account Ownership: The account is opened in the name of the girl child, and only parents or legal guardians can operate the account until she turns 18.

- Maturity and Closure: The account matures when the girl turns 21 or gets married, whichever is earlier. Upon maturity, the accumulated amount, including interest, is paid to the account holder.

Eligibility Criteria for Sukanya Samriddhi Yojana

- Age Limit: The SSY account can be opened for a girl child from birth until she reaches the age of 10.

- Number of Accounts: Only one account can be opened per girl child, and a maximum of two accounts can be opened per family (one for each girl child). In the case of twins or triplets, exceptions are allowed.

- Residency: The girl child must be an Indian resident at the time of account opening and throughout the tenure of the scheme.

Benefits of Sukanya Samriddhi Yojana Scheme

- Financial Security for the Girl Child: The SSY scheme helps parents build a substantial corpus for their daughter’s education and marriage, ensuring financial security.

- Attractive Interest Rates: The interest rate offered by the SSY scheme is typically higher than other government-backed savings schemes, allowing for better growth of savings.

- Tax Savings: Contributions made towards the SSY account are eligible for tax deductions under Section 80C of the Income Tax Act, reducing the overall tax liability of the parents.

- Flexibility in Withdrawals: Partial withdrawals are allowed for the purpose of funding higher education once the girl turns 18, providing flexibility in utilizing the funds when needed.

- Government Backed: The SSY scheme is backed by the Government of India, ensuring safety and reliability of the investment.

- Low Minimum Contribution: The minimum contribution of ₹250 per year makes the scheme accessible to families from all economic backgrounds.

How to Invest in Sukanya Samriddhi Yojana (SSY)?

Investing in Sukanya Samriddhi Yojana is simple and can be done by following these steps:

- Choose the Financial Institution: You can open an SSY account at any authorized bank or post office. Most major public and private sector banks are authorized to offer SSY accounts.

- Fill Out the Application Form: Obtain the SSY application form from the bank or post office and fill in the required details, including information about the girl child and the parent or guardian.

- Provide Required Documents: Submit the necessary documents, including:

- Birth Certificate of the girl child.

- Identity Proof (Aadhaar card, PAN card, etc.) of the parent or guardian.

- Address Proof (Aadhaar card, utility bill, etc.) of the parent or guardian.

- Make the Initial Deposit: Make an initial deposit of at least ₹250 to open the account. You can deposit any amount between ₹250 and ₹1.5 lakh per financial year.

- Receive the Passbook: Once the account is opened, you will receive a passbook that contains details about the account, such as the account number, the date of opening, and the amount deposited.

How to Apply for Sukanya Samriddhi Yojana?

Applying for Sukanya Samriddhi Yojana can be done both offline and online:

- Offline Application:

- Visit an authorized bank branch or post office.

- Fill out the SSY application form and provide the necessary documents (birth certificate, identity proof, and address proof).

- Make the initial deposit to activate the account.

- The bank or post office will provide you with a passbook for the account.

- Online Application:

- Some banks offer the facility to open an SSY account online through their internet banking portal.

- Log in to your internet banking account and navigate to the section for small savings schemes.

- Select the Sukanya Samriddhi Yojana option, fill in the required details, and upload the necessary documents.

- Make the initial contribution through net banking to activate the account.

- Once the process is complete, you will receive an e-passbook with the account details.

How to Open SSY Account Offline?

To open an SSY account offline, follow these steps:

- Visit the Bank or Post Office: Go to any authorized bank branch or post office that offers Sukanya Samriddhi Yojana accounts.

- Collect and Fill the Application Form: Request the SSY application form and fill it out with the required details, including information about the girl child and the parent or guardian.

- Submit Required Documents: Provide the necessary documents, such as the birth certificate of the girl child, identity proof, and address proof of the parent or guardian.

- Make the Initial Deposit: Deposit a minimum amount of ₹250 to open the account. The maximum deposit allowed per year is ₹1.5 lakh.

- Receive Passbook: After the account is opened, you will receive a passbook that includes details like the account number, date of opening, and transaction history.

How to Open SSY Account Online?

To open an SSY account online, follow these steps:

- Log In to Internet Banking: Log in to your internet banking account with an authorized bank that provides the facility to open Sukanya Samriddhi Yojana accounts.

- Navigate to Small Savings Schemes: Go to the section for small savings schemes and select the Sukanya Samriddhi Yojana option.

- Fill Out the Application Form: Fill in the required details, including information about the girl child and the parent or guardian, and upload the necessary documents (birth certificate, identity proof, address proof).

- Make the Initial Contribution: Make the initial deposit using net banking to activate the account. The minimum deposit is ₹250.

- Receive E-Passbook: Once the account is successfully opened, you will receive an e-passbook with the account details, which can be downloaded from the internet banking portal.

Sukanya Samriddhi Yojana Interest Rates

The government sets the interest rate for the Sukanya Samriddhi Yojana, which is revised every three months. The interest rate for the Sukanya Samriddhi Yojana is 8.2% per annum for the current quarter of 2024.

| SSY Interest Rate | 8.2% p.a. |

| Investment Amount | Minimum – Rs. 250; Maximum Rs. 1.5 lakh p.a. |

| Maturity Amount | It depends on the amount invested |

| Maturity Period | 21 years |

Sukanya Samriddhi Yojana (SSY) Interest Rates: Previous Rates

Here is a list of the previous Sukanya Samriddhi interest rates-

| Time Period | SSY Interest Rate (% annually) |

| Oct to Dec 2023 (Q3 FY 2023-24) | 8.0 |

| Apr to Jun 2023 (Q1 FY 2023-24) | 8.0 |

| Jan to Mar 2023 (Q4 FY 2022-23) | 7.6 |

| Oct to Dec 2022 (Q3 FY 2022-23) | 7.6 |

| Jul to Sep 2022 (Q2 FY 2022-23) | 7.6 |

| Apr to Jun 2022 (Q1 FY 2022-23) | 7.6 |

| Jan to Mar 2022 (Q4 FY 2021-22) | 7.6 |

| Oct to Dec 2021 (Q3 FY 2021-22) | 7.6 |

| Jul to Sep 2021 (Q2 FY 2021-22) | 7.6 |

| Apr to Jun 2021 (Q1 FY 2021-22) | 7.6 |

| Jan to March 2021 (Q4 FY 2020-21) | 7.6 |

| Oct to Dec 2020 (Q3 FY 2020-21) | 7.6 |

| Jul to Sep 2020 (Q2 FY 2020-21) | 7.6 |

| Apr to Jun 2020 (Q1 FY 2020-21) | 7.6 |

| Jan to March (Q4 FY 2019-20) | 8.4 |

| Oct to Dec 2019 (Q3 FY 2019-20) | 8.4 |

| Jul to Sep 2019 (Q2 FY 2019-20) | 8.4 |

| Apr to Jun 2019 (Q1 FY 2019-20) | 8.5 |

| Jan to March 2019 (Q4 FY 2018-19) | 8.5 |

| Oct to Dec 2018 (Q3 FY 2018-19) | 8.5 |

| Jul to Sep 2018 (Q2 FY 2018-19) | 8.1 |

| Apr to Jun 2018 (Q1 FY 2018-19) | 8.1 |

| Jan to March 2018 (Q4 FY 2017-18) | 8.1 |

| Oct to Dec 2017 (Q3 FY 2017-18) | 8.3 |

| Jul to Sep 2017 (Q2 FY 2017-18) | 8.3 |

| Apr to Jun 2017 (Q1 FY 2017-18) | 8.4 |

Tax Benefits of Sukanya Samriddhi Yojana (SSY)

Tax exemptions apply to the principle amount deposited, interest accrued throughout the course of the tenure, and maturity advantages. Up to Rs 1.5 lakh of the principal is deductible under Section 80C.

Sukanya Samriddhi Yojana Withdrawal Rules

Withdrawals from the Sukanya Samriddhi Yojana account are subject to certain rules:

- Partial Withdrawals for Education: Once the girl child reaches the age of 18, partial withdrawals are allowed to cover her higher education expenses. Up to 50% of the balance at the end of the previous financial year can be withdrawn for this purpose.

- Maturity Withdrawal: The SSY account matures when the girl turns 21. Upon maturity, the entire balance, including the accumulated interest, can be withdrawn by the account holder.

- Account Closure on Marriage: If the girl gets married before the age of 21, the account can be closed, and the entire corpus can be withdrawn, provided she is at least 18 years old.

Rules for Premature Withdrawal from SSY Account

Premature withdrawal from the SSY account is permitted under specific circumstances:

- Medical Treatment of the Girl Child: Premature withdrawal is allowed in case of medical emergencies such as treatment for life-threatening diseases. Proper documentation and medical certificates need to be submitted.

- Death of the Account Holder: In the unfortunate event of the death of the girl child, the account can be closed prematurely, and the balance along with interest will be paid to the parent or legal guardian.

- Five-Year Lock-In Period: Premature closure is allowed only after the account has completed a five-year lock-in period, except in the case of the account holder’s death or extreme medical emergencies.

Key Points to Keep in Mind about SSY

- Lock-In Period: The SSY account has a lock-in period until the girl child turns 21. Contributions can be made for up to 15 years from the date of account opening.

- Tax Benefits: Contributions are eligible for tax deductions under Section 80C of the Income Tax Act, allowing for significant tax savings.

- Partial Withdrawal for Education: After the girl child turns 18, partial withdrawals of up to 50% of the account balance are allowed to meet education expenses.

- Interest Rate: The interest rate offered by SSY is subject to change and is reviewed quarterly by the government. It is generally higher than other small savings schemes.

- Maximum Contribution Limit: The maximum annual contribution allowed is ₹1.5 lakh. Exceeding this limit will not earn additional interest.

- Account Operation: The account can be operated by the parent or legal guardian until the girl child turns 18, after which she can operate the account herself.

Conclusion

The Sukanya Samriddhi Yojana (SSY) is a well-thought-out savings scheme that provides parents with an opportunity to secure their daughter’s financial future. With attractive interest rates, tax benefits, and government backing, it is one of the best options available for long-term savings aimed at covering future education and marriage expenses. By investing in SSY, parents can ensure that their daughters have the necessary funds to pursue their dreams and lead a financially secure life. Start early, stay consistent, and watch your savings grow, ultimately benefiting your daughter as she steps into adulthood.

FAQs

Who can open an SSY account?

The SSY account can be opened by parents or legal guardians for a girl child below the age of 10 years.

What is the minimum and maximum contribution for SSY?

The minimum contribution is ₹250 per year, and the maximum contribution is ₹1.5 lakh per year.

Can I withdraw money from the SSY account before maturity?

Yes, partial withdrawals are allowed for higher education purposes once the girl turns 18. Up to 50% of the balance at the end of the previous financial year can be withdrawn for this purpose.

What happens if I fail to make the minimum annual contribution?

If the minimum annual contribution of ₹250 is not made, the account will be classified as default. It can be revived by paying a penalty of ₹50 per year of default along with the minimum contribution for the year.

Is the interest earned on SSY taxable?

No, the interest earned on the Sukanya Samriddhi Yojana account is tax-free. The entire maturity amount, including interest, is exempt from tax.

Can NRIs invest in Sukanya Samriddhi Yojana?

No, Non-Resident Indians (NRIs) are not eligible to open an SSY account. The girl child must be an Indian resident throughout the tenure of the account.

Can I transfer the SSY account?

Yes, the SSY account can be transferred from one bank or post office to another across India, free of charge. This is useful if you relocate to a different city or state.

How many SSY accounts can be opened in a family?

A maximum of two SSY accounts can be opened per family, one for each girl child. In the case of twins or triplets, an exception is made to allow more accounts.

What happens to the SSY account if the girl child gets married before maturity?

If the girl child gets married before the age of 21, the account can be closed, provided she is at least 18 years old at the time of marriage.

How is the maturity amount paid out?

Upon maturity, the entire balance, including the interest earned, is paid directly to the account holder (the girl child). The maturity amount can be used for any purpose, such as higher education or marriage.