TL;DR: Key Takeaways on the April 2026 Mutual Fund Rule Changes

If you are short on time and just want the highlights, here is what changed in the mutual fund world on April 1, 2026:

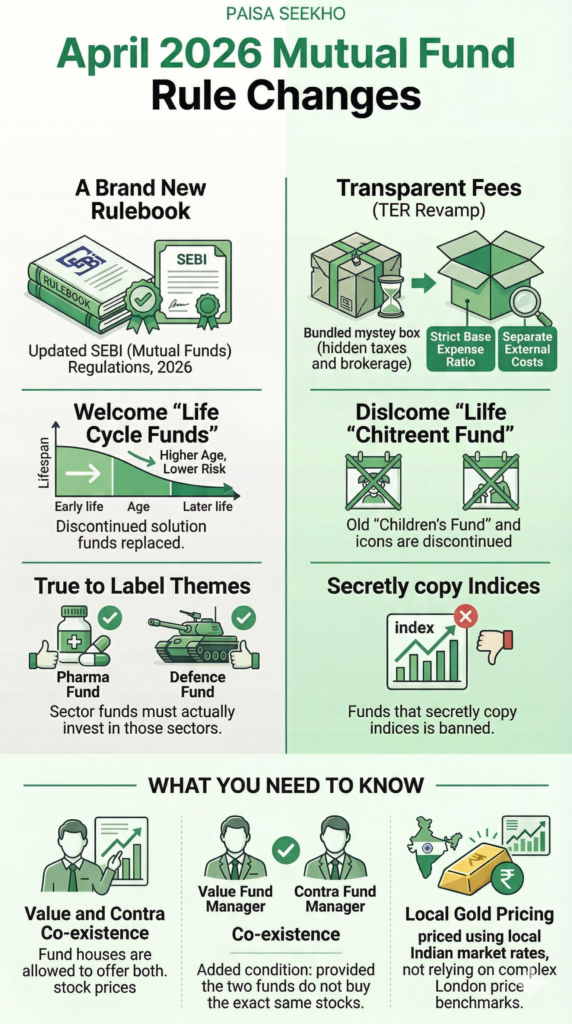

- A Brand New Rulebook: The entire mutual fund industry is now governed by the updated SEBI (Mutual Funds) Regulations, 2026.

- Transparent Fees (TER Revamp): Fund houses can no longer hide taxes and brokerage fees inside one big “Total Expense Ratio.” The fees are now split into a strict “Base Expense Ratio” and separate external costs, making it cheaper and highly transparent for you.

- Welcome “Life Cycle Funds”: Old “Solution-Oriented” funds (like specific Children’s or Retirement funds) are discontinued. They are replaced by highly advanced “Life Cycle Funds” that automatically reduce your risk as you get older.

- True to Label Themes: If a mutual fund claims to be a “Pharma Fund” or a “Defence Fund,” it must actually invest in those sectors. SEBI has banned these funds from secretly copying regular stock market index funds.

- Value and Contra Co-existence: Fund houses are now legally allowed to offer both a Value Fund and a Contra Fund at the same time, provided the two funds do not buy the exact same stocks.

- Local Gold Pricing: Gold and Silver ETFs will now be priced using local Indian market rates instead of relying on complex London price benchmarks.

Introduction

If you are an investor in India, April 1st is not just April Fools’ Day; it is the day the financial calendar resets. While most people were focused on the new income tax laws or credit card rule changes, the Securities and Exchange Board of India (SEBI) quietly rolled out the biggest update to the mutual fund industry in almost a decade.

For nearly thirty years, mutual funds in India operated under a very old set of rules. As the market grew and millions of new, young investors started Systematic Investment Plans (SIPs) from their smartphones, those old rules became confusing and outdated. To fix this, SEBI completely tore up the old rulebook and launched the brand new SEBI (Mutual Funds) Regulations, 2026.

If you have your hard-earned savings invested in mutual funds, you might be wondering if these new rules will hurt your returns or change how your money is managed.

Do not panic. These changes were designed entirely to protect you, the investor. SEBI’s goal is to make mutual funds cheaper, more transparent, and much easier to understand. In this deep-dive guide, we are going to break down every single major mutual fund change that became law on April 1, 2026, using simple, everyday language so you know exactly what is happening to your money.

1. Understanding the New Total Expense Ratio (TER)

When you invest in a mutual fund, the experts managing your money do not work for free. They charge a small annual fee called the Total Expense Ratio (TER). It is usually a small percentage, like 1% or 1.5% of your total investment.

For a very long time, the TER was basically a “mystery box.” Mutual fund companies (Asset Management Companies, or AMCs) would take that 1.5% and use it to pay for everything: the fund manager’s salary, marketing advertisements, the commission given to the agent who sold you the fund, and government taxes.

Because everything was bundled together in one number, you as an investor had no idea how much of your money was actually paying for investment expertise versus how much was just paying for flashy marketing.

The 2026 TER Revolution

Starting April 1, 2026, SEBI smashed the mystery box. They ruled that the Total Expense Ratio can no longer be one bundled, confusing number. It must be broken down clearly into distinct parts.

Here is how your mutual fund fees are now structured:

- The Base Expense Ratio (BER): This is the core fee. This money is strictly for the mutual fund company to pay its expert fund managers, cover their operational costs, and pay distribution commissions. SEBI has set very strict mathematical limits on exactly how high this BER can go, depending on how large the mutual fund is.

- External Costs Kept Separate: Things that the mutual fund company cannot control—like government GST, the Securities Transaction Tax (STT), stamp duty, and the brokerage costs of actually buying the stocks on the exchange—are now kept completely outside the Base Expense Ratio. They are charged exactly as they cost, on “actuals.”

Why is this good for you?

This is a massive win for the retail investor. First, it brings absolute transparency. When you look at your mutual fund statement, you will know exactly what the AMC is charging for their brainpower versus what the government is taking in taxes.

Secondly, by tightening the Base Expense Ratio caps and removing old “bonus charges” (like the extra 5 basis points AMCs used to charge just for having an exit load), SEBI has effectively forced mutual funds to become slightly cheaper. For many index funds and equity schemes, your overall costs will drop, which means more of your money stays invested and compounds over time.

(Note: While this is great for investors, it is causing a lot of stress for Mutual Fund Distributors and agents, as the tighter fee structures mean the mutual fund companies might have to reduce the commissions they pay out to the people selling the funds!)

2. Hello “Life Cycle Funds”, Goodbye “Solution Funds”

Mutual funds are designed to help you reach your life goals, like paying for your child’s college education or building a massive retirement corpus. To help with this, fund houses used to offer a special category called “Solution-Oriented Schemes” (often named things like “Children’s Gift Fund” or “Retirement Savings Fund”).

The problem with these old funds was that they were very rigid. If you bought a retirement fund at age 30, it might invest 80% of your money in high-risk, high-reward stocks. But what happens when you turn 58 and are about to retire? You do not want 80% of your life savings in the risky stock market right before you need the cash! You had to manually sell the risky fund and buy a safe fund.

Enter the “Glide Path” Strategy

On April 1, 2026, SEBI officially discontinued the old Solution-Oriented category. Any existing funds in this category are being merged into standard funds.

In their place, SEBI has introduced a brilliant, globally proven concept called Life Cycle Funds.

A Life Cycle Fund is the ultimate “fill it, shut it, and forget it” investment. When you buy a Life Cycle Fund, you choose a specific “target maturity” year—for example, a 15-year fund, a 20-year fund, or a 30-year fund.

These funds use a strategy called a “Glide Path.” * When you are young (Far from the goal): The fund manager will automatically put almost all of your money into high-growth equity (the stock market) to grow your wealth aggressively.

- As you get older (Closer to the goal): As the years pass, the fund manager will slowly, automatically, and safely move your money out of the risky stock market and put it into highly secure government bonds and debt funds.

By the time your target year arrives (like your 60th birthday), your money is sitting in the safest possible assets, completely protected from any sudden stock market crashes. You never have to manually adjust your portfolio; the Life Cycle Fund does the risk management for you automatically based on your age!

3. Stricter Rules for Thematic and Sectoral Funds

One of the biggest problems in the Indian mutual fund market over the last few years was “copycat funds.”

Let’s say you wanted to invest specifically in the healthcare industry, so you bought a “Pharma Sector Fund.” You expect that fund manager to go out and find the absolute best pharmaceutical companies in India.

However, many lazy fund managers would launch a “Pharma Fund,” put 40% of the money into pharma stocks, and then secretly put the remaining 60% of the money into massive, safe companies like HDFC Bank, Reliance, and TCS just to make sure their fund’s returns looked stable.

As an investor, you were being tricked. You were paying high fees for a specialized “Pharma Fund,” but you were essentially just getting a regular, boring Nifty 50 index fund in disguise.

The “True to Label” Rule

SEBI hated this deceptive practice. Under the new 2026 rules, SEBI has cracked the whip to ensure funds are “True to Label.”

Starting today, if a mutual fund belongs to a specific sector (like IT, Defence, or Pharma) or a specific theme, it is absolutely banned from having more than a 50% overlap with any other broad equity scheme.

In simple terms, a Sectoral fund must genuinely reflect its sector. It cannot secretly copy the portfolio of a massive diversified fund just to play it safe. If it says it is a Defence fund, it must live and die by the performance of the Defence sector. Existing mutual funds that break this rule have been given a strict three-year deadline to sell off their overlapping stocks and fix their portfolios.

4. Value and Contra Funds Can Now Overlap

In the mutual fund world, there are two very interesting, highly specialized types of investment strategies: Value Funds and Contra Funds.

- A Value Fund: The fund manager looks for great companies whose stock prices have unfairly fallen. They buy these “undervalued” stocks at a massive discount, hoping the market eventually realizes their true worth and the price goes up.

- A Contra Fund: The fund manager deliberately bets against the current market trend. If everyone is panicking and selling IT stocks because of bad news, the Contra fund manager steps in and buys them, betting that the panic is a temporary overreaction.

Historically, SEBI forced mutual fund houses to make a choice: A fund house (like SBI Mutual Fund or HDFC Mutual Fund) was only legally allowed to offer either a Value Fund or a Contra Fund. They could not offer both, because SEBI thought the two strategies were too similar and would confuse retail investors.

The 2026 Co-Existence Rule

SEBI has finally relaxed this old rule. Starting April 1, 2026, a single mutual fund company is officially allowed to offer both a Value Fund and a Contra Fund to its investors at the same time.

However, SEBI added a very smart safety net: The 50% Overlap Condition.

To ensure that the fund house isn’t just launching two identical funds with different names to collect more fees, SEBI mandated that the portfolio of the Value Fund and the portfolio of the Contra Fund cannot overlap by more than 50%. The fund managers must prove that they are actually executing two distinct, different strategies.

5. Pricing Gold and Silver Based on Indian Markets

Many Indians love investing in precious metals, but they hate dealing with the physical storage and making charges of jewelry. Because of this, Gold ETFs (Exchange Traded Funds) and Silver ETFs have become incredibly popular. When you buy a Gold ETF, the mutual fund company takes your money and buys real, physical gold bars to store in a vault on your behalf.

But how does the mutual fund calculate the exact daily value (the NAV) of your digital gold?

For decades, Indian mutual funds relied on the London Bullion Market Association (LBMA). Every morning, bankers in London would agree on a global benchmark price for gold. Indian mutual funds would take that London price, apply a complex mathematical formula to adjust for the Rupee-Dollar currency exchange rate, add customs duties, and add transportation costs to finally figure out the Indian price.

It was a messy, complicated process that sometimes resulted in inaccurate prices.

The Shift to Domestic Spot Prices

The Indian stock market is now large enough to stand on its own two feet. Under the new 2026 regulations, SEBI has ordered all mutual fund houses to stop looking at London.

Starting immediately, Gold and Silver ETFs must be valued using the domestic spot prices published directly by recognized Indian stock exchanges. This means the daily value of your Gold ETF will exactly mirror the real, live price of physical gold trading right here in India, completely removing the confusing international math and providing you with a much more accurate return on your investment.

Conclusion: A Safer, Smarter Market for Everyone

The mutual fund industry is built entirely on trust. You are handing over your life savings to strangers, trusting that they will grow your wealth over the next ten or twenty years.

The new SEBI (Mutual Funds) Regulations, 2026, are a massive leap forward in building that trust. By forcing fund houses to split open their fee structures, demanding that specialized funds stay true to their names, and introducing brilliant automated products like Life Cycle Funds, SEBI has made the Indian mutual fund market one of the safest and most transparent in the entire world.

You do not need to take any immediate action on your existing SIPs or portfolios today. The fund houses are legally required to make these backend changes automatically. However, as an investor, understanding these new rules gives you a powerful advantage. It ensures you know exactly what you are paying for, and it empowers you to make smarter, more profitable decisions for your financial future.

Frequently Asked Questions (FAQs): Mutual Fund Changes 2026

Q1: Will the new SEBI rules affect the SIPs I am currently running?

No, you do not need to stop or restart your current Systematic Investment Plans (SIPs). The changes initiated on April 1, 2026, mostly affect the backend fee structures and regulatory compliance of the fund houses. Your existing SIPs will continue to run normally, and you might actually see a slight drop in the fees you are being charged!

Q2: What is the difference between the Base Expense Ratio and the old TER?

The old Total Expense Ratio (TER) was a single bundled number that included the fund manager’s fees, broker commissions, and government taxes (like GST). The new Base Expense Ratio (BER) only includes the actual management and distribution fees. All external taxes and brokerage costs are now listed separately, giving you total transparency.

Q3: I have money in a Retirement Solution Fund. Is it gone?

Your money is 100% safe! While SEBI has discontinued the “Solution-Oriented” category name, the actual mutual funds are not being shut down. Your specific retirement fund will simply be officially merged or re-categorized into a standard fund or a new Life Cycle Fund that matches its risk profile. The AMC will send you an email explaining the exact name change.

Q4: Should I invest in a Life Cycle Fund instead of normal Mutual Funds?

If you want to actively manage your money and pick your own mix of high-risk and low-risk funds, standard mutual funds are still the best. However, if you have absolutely no knowledge of the stock market and just want a simple fund that automatically reduces your risk as you get older, a Life Cycle Fund is the perfect, stress-free choice.

Q5: What does “True to Label” mean for Sectoral funds?

“True to Label” means no more false advertising. If a mutual fund is called an “IT Sector Fund,” SEBI’s new rule mandates that the vast majority of its money must actually be invested in Information Technology companies. It cannot legally mimic a broader Nifty 50 fund just to play it safe.

Q6: What is a Portfolio Overlap?

Portfolio overlap happens when two different mutual funds buy the exact same stocks. For example, if both Fund A and Fund B put 80% of their money into Reliance, HDFC, and TCS, they have a massive portfolio overlap. SEBI’s new rules restrict this overlap for certain specialized funds so that investors aren’t accidentally paying two different fees for the exact same portfolio.

Q7: Can I now invest in both a Value Fund and a Contra Fund from the same AMC?

Yes! Previously, a mutual fund house (like SBI or ICICI) could only offer one or the other. Starting April 1, 2026, they can offer both, and you can invest in both. SEBI just requires the fund house to ensure the two funds have very distinct, different portfolios.

Q8: Why did SEBI change the way Gold ETFs are priced?

Previously, Indian funds used the London Bullion Market Association (LBMA) price and tried to mathematically convert it into Indian Rupees, which involved adding estimated customs duties and shipping costs. It was messy. By forcing funds to use the live domestic spot price published by Indian exchanges, your Gold ETF value will be much more accurate and transparent.

Q9: Do these changes make mutual funds totally risk-free?

Absolutely not. These changes make mutual funds fairer and more transparent, but they do not eliminate market risk. If you invest in an equity mutual fund, your money is still tied to the performance of the stock market, which can go up and down. You can still lose money in a market crash.

Q10: Where can I check the new Expense Ratio of my mutual fund?

Every mutual fund company was required to issue an official “addendum” (an update document) on April 1, 2026, detailing their revised fee structures. You can check the exact new Base Expense Ratio (BER) by visiting the official website of your specific mutual fund house (AMC) or by checking the updated Scheme Information Document (SID) on your broker app.

⚠️ Disclaimer

At Paisaseekho, our mission is to make you financially literate. The information provided in this article is for educational and informational purposes only and should not be construed as professional financial, investment, or tax advice.