TL;DR: Best Gold Loan Companies in India Takeaways

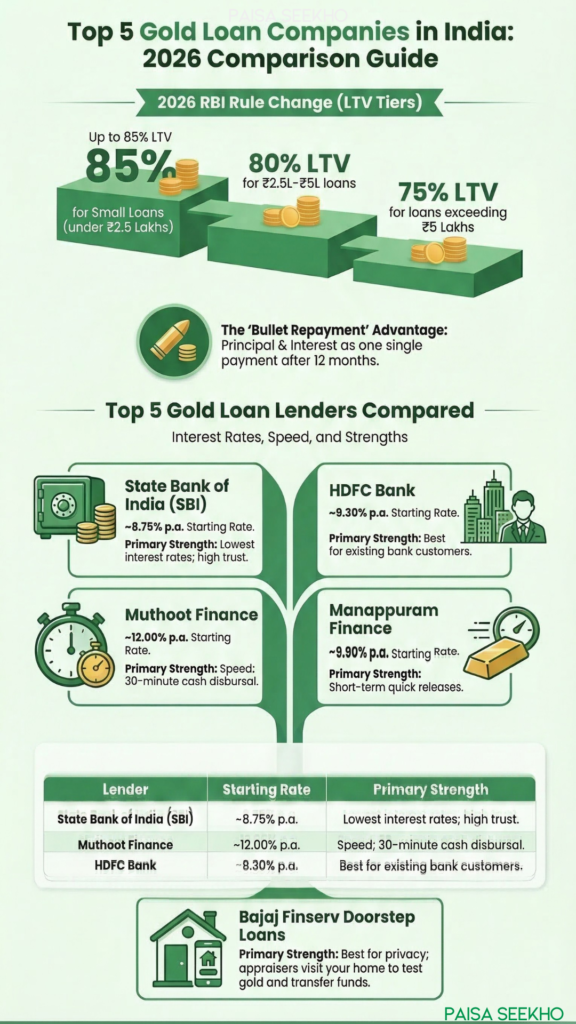

- The 2026 RBI Update: The rules have changed! Starting April 2026, the RBI has increased the Loan-to-Value (LTV) limit. You can now get up to 85% LTV for loans under Rs. 2.5 Lakhs, 80% LTV for loans between Rs. 2.5 to 5 Lakhs, and 75% LTV for loans above Rs. 5 Lakhs.

- Banks vs. NBFCs: Public sector banks (like SBI) offer the absolute lowest interest rates (starting around 8.75%), but the process takes a bit longer. NBFCs (like Muthoot or Manappuram) charge slightly higher rates but offer lightning-fast, 30-minute disbursals.

- The Smart Alternative: A gold loan is almost mathematically superior to a standard Personal Loan. It requires no CIBIL score check, has significantly lower interest rates, and offers flexible repayment options like “Bullet Repayment” (pay everything at the end of the year).

- The Top 5 Lenders: Based on interest rates, hidden fees, and customer experience, the top lenders in India right now are SBI, HDFC Bank, Muthoot Finance, Manappuram Finance, and Bajaj Finserv (for doorstep loans).

1. Escaping the Gold Loan Taboo

For generations, taking a gold loan in India carried a massive cultural stigma. It was seen as the absolute last resort of a desperate family, the dramatic movie scene where the mother tearfully hands over her wedding bangles to save the house.

If you are a young professional or a small business owner in 2026, you need to completely erase that taboo from your mind.

The Indian gold loan market has undergone a massive structural shift. Today, wealthy investors, smart entrepreneurs, and middle-class professionals are actively using their physical gold to unlock cheap, instant liquidity. Why? Because financially speaking, letting Rs. 5 Lakhs worth of gold sit idle in a dark bank locker while you take out a high-interest Personal Loan at 15% is a terrible financial decision.

A gold loan is one of the smartest, fastest, and cheapest ways to access cash in an emergency or fund a short-term business opportunity. This guide is going to break down exactly how gold loans work, expose the massive new 2026 RBI rule changes, and rank the absolute best gold loan companies in India so you don’t get trapped by hidden fees.

2. The 2026 RBI Rule Change (The LTV Cheat Code)

Before you walk into a bank, you need to know exactly how much money your gold can actually unlock. This is determined by the Loan-to-Value (LTV) ratio, which is strictly governed by the Reserve Bank of India (RBI).

For years, the RBI capped the LTV at 75%. If you pledged Rs. 1 Lakh worth of gold, the maximum loan you could get was Rs. 75,000.

However, in a massive win for borrowers, the RBI has introduced a new tiered LTV structure for 2026:

- Loans up to Rs. 2.5 Lakh: You now get up to 85% LTV.

- Loans between Rs. 2.5 Lakh to Rs. 5 Lakh: You get up to 80% LTV.

- Loans above Rs. 5 Lakh: The limit remains at the standard 75% LTV.

Paisaseekho Example: If you have Rs. 2 Lakhs worth of 22K gold jewelry, under the old rules, you could only borrow Rs. 1,50,000. Under the new 2026 rules, you can instantly unlock Rs. 1,70,000!

3. Gold Loan vs. Personal Loan: Which is Better?

If you need emergency cash, you are probably debating between an unsecured Personal Loan and a secured Gold Loan. Here is why the Gold Loan wins almost every single time:

- Interest Rates: Personal loans are risky for banks, so they charge anywhere from 12% to 20% interest. Because a gold loan is 100% secured by your physical asset, banks feel incredibly safe and offer interest rates as low as 8.75% to 10%.

- Zero CIBIL Score Drama: If you missed a credit card payment three years ago and your CIBIL score is ruined, getting a personal loan is nearly impossible. Gold loan companies do not care about your credit score. Your gold is your credit score.

- Flexible Repayment (The Bullet Option): Personal loans force you to pay a rigid monthly EMI. Many gold loans offer a “Bullet Repayment” scheme, where you don’t have to pay a single rupee for 6 or 12 months. You just pay the entire principal and interest together at the very end of the loan tenure!

4. Top 5 Gold Loan Companies in India (2026 Rankings)

The market is heavily divided into two camps: Public/Private Banks (cheap but strict) and NBFCs (slightly more expensive but incredibly fast). Here are the top 5 players dominating the space today:

1. State Bank of India (SBI): The Interest Rate Champion

- Best For: Borrowers who want the absolute lowest interest rate and have 1 or 2 days to wait for processing.

- Starting Interest Rate: ~8.75% p.a.

- The Verdict: SBI is the undisputed king of cheap gold loans. They offer incredible schemes, including 3-month, 6-month, and 12-month bullet repayment options. The processing fee is incredibly low (often around 0.25% to 0.50%), making it the best option for large, calculated loans where saving on interest is your top priority.

2. Muthoot Finance: The Trusted Giant

- Best For: People who need cash in 30 minutes and want a trusted branch near their house.

- Starting Interest Rate: ~12.00% p.a.

- The Verdict: Muthoot is India’s largest gold loan NBFC. What they lack in rock-bottom interest rates, they make up for in sheer convenience. With thousands of branches across India, minimal paperwork, and approval times measured in minutes, they are the go-to option for massive, sudden emergencies.

3. HDFC Bank: The Private Banking Sweet Spot

- Best For: Existing HDFC customers and urban professionals.

- Starting Interest Rate: ~9.30% p.a.

- The Verdict: HDFC bridges the gap perfectly between the low rates of public banks and the fast service of NBFCs. If you already have a salary account with HDFC, you can often get preferential rates, very high loan limits (up to Rs. 1 Crore), and lightning-fast digital disbursals right into your account.

4. Manappuram Finance: The Quick-Release Specialist

- Best For: Short-term, urgent loans (3 to 6 months).

- Starting Interest Rate: ~9.90% p.a.

- The Verdict: The biggest rival to Muthoot, Manappuram is famous for its heavily tech-driven process and short-tenure loan schemes. They are fantastic if you just need to bridge a cash-flow gap for a couple of months and want to release your gold quickly without getting hit by massive foreclosure penalties.

5. Bajaj Finserv (Doorstep Gold Loans): The Modern Disruptor

- Best For: Privacy-conscious borrowers who don’t want to carry gold through the streets.

- Starting Interest Rate: ~9.50% p.a.

- The Verdict: Transporting Rs. 10 Lakhs worth of gold to a bank branch is terrifying. Bajaj Finserv (and other fintechs like Rupeek) have popularized the “Doorstep Gold Loan.” A certified appraiser comes to your house, weighs and tests the gold in front of you, and transfers the money to your bank account before they leave with the gold. It is the ultimate modern convenience.

5. The Hidden Traps: What They Don’t Tell You

While gold loans are fantastic, lenders are not running charities. Before you sign the papers, watch out for these three massive traps:

- The Stone Deduction: When evaluating your 22K gold necklace, the bank will strictly deduct the weight of any diamonds, rubies, or enamel work. You only get a loan based on the pure gold weight. Do not expect a loan based on the jeweler’s original bill!

- Valuation Charges: Many banks will charge you a hidden fee (ranging from Rs. 250 to Rs. 1,000) just to have their internal goldsmith test the purity of your gold. Always ask if valuation charges are included in the processing fee.

- The Auction Risk: Because gold prices fluctuate, if the price of gold suddenly crashes by 20%, the bank might ask you to deposit extra cash to maintain the LTV margin. If you fail to do so, or if you default on your final bullet repayment, the bank has the legal right to auction your family jewelry to recover their money.

6. Conclusion: Which Lender Should You Choose?

Taking a gold loan in 2026 is a sign of smart financial maneuvering, not desperation.

Your Decision Matrix:

- If you have a planned expense (like business capital or home renovation) and want to save maximum money, go to SBI or HDFC Bank. The slightly longer paperwork process is worth the thousands you will save on the 8.75% interest rate.

- If you have a medical emergency at 2 PM and need cash by 3 PM, walk into a Muthoot or Manappuram branch. You will pay a slightly higher interest rate, but you will have the money instantly.

- If you value absolute privacy and safety, use a Doorstep Gold Loan service. Your Next Step: Gather your gold, make sure it is 18K to 22K purity, and use an online Gold Loan Calculator. Factor in the new 85% LTV rule to see exactly how much liquidity is hiding in your locker right now!

Top 10 Frequently Asked Questions

1. What is the new RBI rule for gold loans in 2026?

The RBI has updated the Loan-to-Value (LTV) limits to provide more liquidity. Borrowers can now get up to 85% LTV for loans under Rs. 2.5 Lakhs, 80% LTV for loans between Rs. 2.5 Lakhs and Rs. 5 Lakhs, and the standard 75% LTV for loans above Rs. 5 Lakhs.

2. Which bank offers the lowest gold loan interest rate in India?

Public sector banks typically offer the lowest rates. State Bank of India (SBI) is consistently the market leader, with gold loan interest rates starting as low as 8.75% to 9.00% p.a., depending on the repayment scheme you choose.

3. Do I need a good CIBIL score to get a gold loan?

No! This is the biggest advantage of a gold loan. Because the loan is 100% secured by your physical gold, lenders generally do not perform a hard credit check or require a high CIBIL score for approval. Your gold acts as your creditworthiness.

4. What is a “Bullet Repayment” gold loan scheme?

A Bullet Repayment scheme allows you to skip monthly EMIs entirely. You simply pledge your gold, take the cash, and pay back the entire principal amount plus the accumulated interest in one single “bullet” payment at the end of the loan tenure (usually 6 or 12 months).

5. NBFCs vs. Banks: Which is better for a gold loan?

It depends on your priority. Banks (like SBI or HDFC) are better if you want the absolute lowest interest rate and have a day or two to spare for processing. NBFCs (like Muthoot or Manappuram) are better if you are willing to pay a slightly higher interest rate in exchange for instant, 30-minute cash disbursal with minimal paperwork.

6. Are making charges and gemstones included in the gold valuation?

Absolutely not. Lenders will deduct the weight of any diamonds, rubies, enamel work, and the original making charges. The loan amount is calculated strictly on the weight and purity of the raw gold alone.

7. What happens if the price of gold crashes while I have a loan?

If gold prices drop significantly, the value of your collateral decreases. If it drops below the required LTV margin, the bank will issue a “margin call,” requiring you to either deposit cash or pledge more gold to make up the difference.

8. What happens if I fail to repay my gold loan?

If you default on your payments and ignore the final warning notices, the lender has the legal right to auction your pledged gold jewelry to recover their principal and interest.

9. Can I get a gold loan without income proof or salary slips?

Yes. Unlike personal loans or home loans, most gold loan companies do not ask for salary slips, ITR returns, or business income proof. All you need is your KYC documents (Aadhaar/PAN) and the physical gold.

10. Do lenders accept 18K gold for loans?

Yes, most major banks and NBFCs accept gold jewelry ranging from 18K to 24K purity. However, the loan amount you receive per gram will be significantly lower for 18K gold compared to 22K or 24K gold.