TL;DR: The Quick Facts on the ₹29 Lakh Crore UPI Record

If you are in a rush and just need the headline numbers, here is the quick summary:

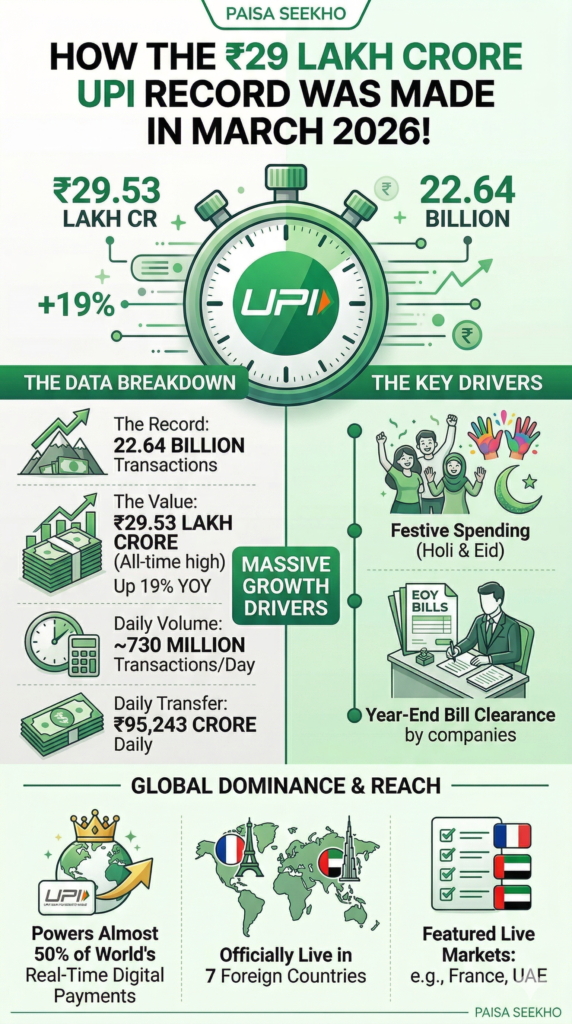

- The Record: In March 2026, UPI processed 22.64 billion individual transactions.

- The Value: The total value of these transactions hit an all-time high of ₹29.53 Lakh Crore (up 19% from the same month last year).

- The Daily Math: Indians made roughly 730 million transactions every single day, transferring about ₹95,243 crore daily.

- The Drivers: This massive surge was driven by festive spending (Holi and Eid) combined with companies aggressively clearing their bills for the financial year-end.

- Global Dominance: UPI now powers almost 50% of the entire world’s real-time digital payments and is officially live in 7 foreign countries, including France and the UAE.

Introduction

Have you bought a cup of tea today? Or maybe paid your local vegetable vendor? Chances are, you didn’t reach for your physical wallet to pull out a crumpled ten-rupee note. Instead, you automatically pulled out your smartphone, scanned a small QR code, heard a satisfying ding, and walked away.

This simple, everyday action has become the heartbeat of the Indian economy. We use it so often that we don’t even think about it anymore. But while we were busy scanning QR codes for our morning coffee and our monthly rent, the entire country came together to achieve something absolutely mind-boggling.

In March 2026, the Unified Payments Interface (UPI) officially broke all previous records, processing a staggering ₹29.53 Lakh Crore in a single month!

To put that into perspective, that is not millions, and it is not billions. That is nearly thirty trillion rupees moving seamlessly through the air in just 31 days.

If you want to understand how India went from a country that hoarded cash under mattresses to becoming the undisputed digital payment champion of the entire world, you are in the right place. This simple, easy-to-understand guide will break down this historic 2026 record, explain the unbelievable math behind it, and show you exactly how your daily ₹20 payments are reshaping global finance.

1. Understanding the Massive ₹29.53 Lakh Crore Milestone

When the National Payments Corporation of India (NPCI) released their official data on April 1, 2026, the financial world had to double-take. The numbers were staggering.

In March 2026, the UPI network processed exactly 22.64 billion transactions. That is 22,640,000,000 times that an Indian citizen scanned a code or sent money to a phone number.

The total monetary value of those transactions hit ₹29.53 Lakh Crore.

Human brains are not naturally designed to understand numbers that large. Let’s try to put it into a simple perspective. If you took ₹29.53 Lakh Crore and divided it by the population of India (roughly 1.4 billion people), it means that every single man, woman, and child in the country theoretically moved over ₹21,000 through UPI in a single month!

This represents a massive 19% growth in value and a 24% growth in volume compared to the exact same month last year. It proves that UPI is not just a passing trend; it is a continuously growing tsunami that has permanently changed how money works in India.

2. The Perfect Storm: Why Did It Spike in March 2026?

You might be wondering, why March? Why did this specific month shatter all the previous records? The answer is a perfect combination of culture and accounting. March 2026 created the ultimate financial storm.

The Festival Factor

India is a land of festivals, and festivals mean shopping. In March 2026, the country celebrated two major, vibrant festivals: Holi and Eid.

- People went out in massive numbers to buy sweets, colors, and new clothes.

- Families traveled to visit their relatives, booking train tickets and flights.

- Eidi (the traditional gift of money given to children and younger relatives during Eid) is increasingly being sent via UPI instead of physical cash envelopes.

All of this joyful spending resulted in millions of extra QR code scans at local markets and sweet shops across the country.

The Financial Year-End Rush

March 31st is the most stressful day of the year for any Indian business owner or accountant. It is the end of the Financial Year.

- Businesses are frantically clearing their pending invoices and paying their suppliers before the books close.

- Individuals are rushing to buy last-minute tax-saving investments (like ELSS mutual funds or health insurance) before the deadline.

- Companies are paying out annual bonuses to their employees.

Because UPI is instant, businesses and individuals relied heavily on it to make sure their high-value payments went through exactly on time, causing the total monetary value to shoot up past the ₹29 Lakh Crore mark.

3. The Daily Math: 730 Million Scans a Day!

Let’s break that massive monthly number down into a daily scale to really understand the magic of India’s technology.

According to the NPCI data, the UPI system handled an average of 730 million transactions every single day in March.

Think about what that means. Every single day, 730 million times, a bank server had to securely verify a person’s identity, check their bank balance, move the money to another bank, and send a success message to both phones. And it does all of this in less than three seconds!

Financially, this means about ₹95,243 crore was moving through the air daily.

This daily movement is a beautiful mix of the rich and the poor, the urban and the rural. One transaction might be a wealthy businessman buying a ₹2 Lakh television in a luxury mall in Mumbai. The very next transaction happening on the same server might be a college student in a small village in Bihar paying ₹10 to a street vendor for a plate of pani puri.

UPI does not discriminate. It treats the ₹10 transaction with the exact same speed and security as the ₹1 Lakh transaction. That is the true beauty of this digital infrastructure.

4. India’s Global Superpower: Ruling the World of Payments

We often look to Western countries for technological innovation. We use American search engines, American social media apps, and American smartphones. But when it comes to digital money, the entire world is looking at India with absolute jealousy.

The numbers are undeniable. Today, UPI accounts for a staggering 85% of all digital transactions within India. We have essentially stopped using debit cards and credit cards for our daily expenses.

But the most mind-blowing statistic is on the global stage. India’s UPI system now powers nearly 50% of the entire world’s real-time digital payments. Let that sink in. Half of all the instant digital money moving around the globe on any given day is happening right here in India.

Taking UPI Across Borders

The Indian government and the NPCI are not keeping this technology to themselves. They are actively exporting it.

As of early 2026, UPI is officially live and working in seven foreign countries:

- The United Arab Emirates (UAE)

- Singapore

- Bhutan

- Nepal

- Sri Lanka

- Mauritius

- France

The entry into France was a massive, historic milestone. It was UPI’s first step into Europe. Today, an Indian tourist visiting Paris can literally stand under the Eiffel Tower, buy a ticket or a souvenir, and pay for it by scanning a QR code with their Indian phone, with the money instantly converting from Rupees to Euros. No more dealing with expensive foreign exchange shops or confusing travel cards!

5. The Journey: From Cash-Hoarders to Digital Natives

To truly appreciate this ₹29 Lakh Crore milestone, we have to look back at how far we have come.

If you rewind the clock to ten years ago, India was a heavily cash-dependent economy. We kept cash hidden under mattresses, we stood in long lines at the ATM, and dealing with exact change was a daily nightmare. When the government launched the “Digital India” initiative, there were many loud critics.

People laughed and said, “India is too poor for digital payments! Do you really expect a farmer or a roadside tea seller to use a smartphone to take payments?”

The joke is on the critics. Today, the roadside tea seller is exactly the person who benefits from it the most.

Bridging the Gap

Before UPI, if a street vendor wanted to accept digital payments, they had to rent a bulky, expensive PoS (Point of Sale) card-swiping machine from a bank, pay a monthly internet fee, and pay the bank a 2% commission on every single sale. It was financially impossible for poor merchants.

UPI destroyed those barriers. It gave the street vendor a simple, printed QR code on a piece of paper. It costs absolutely nothing to print, requires no electricity, and takes zero commission from the merchant. This simple piece of paper bridged the gap between the formal banking system and the informal street economy, bringing millions of unbanked Indians into the digital financial fold.

6. The Key Players: Who Makes This Magic Happen?

It is important to understand that UPI is not an app; it is a “network.” It is the invisible highway that connects all the banks together.

- The NPCI: The National Payments Corporation of India is the genius organization that built and maintains this highway. They are an initiative created by the Reserve Bank of India (RBI) and the Indian Banks’ Association.

- The Banks: Behind every UPI app is your actual, traditional bank (like SBI, HDFC, or ICICI). They hold the actual money and do the heavy lifting of keeping it safe.

- The Apps (Third-Party Providers): These are the cars driving on the highway. Apps like PhonePe, Google Pay, and Paytm provide the beautiful, easy-to-use interfaces on your smartphone.

Currently, the market is heavily dominated by a few major players. As of the early 2026 data, PhonePe continues to hold the number one spot, processing nearly 45% of all the transaction volume. Google Pay sits securely in the second position with roughly a 33% market share, followed by Paytm and other banking apps.

7. What is Next? The Future After 29 Lakh Crore

Now that UPI has conquered the 29 Lakh Crore mountain, what is the next frontier? The NPCI is not relaxing; they are rolling out aggressive new features that will define the rest of the 2020s.

1. Credit on UPI

Until recently, UPI was strictly a “debit” system, meaning you could only spend the money you already had in your savings account. That has changed. You can now securely link your RuPay Credit Cards directly to your UPI apps. This means you can scan a normal QR code at a grocery store and pay using credit, allowing you to earn reward points without needing to carry a physical plastic card.

2. UPI Lite for Offline and Small Payments

To stop bank servers from crashing due to millions of tiny ₹10 and ₹20 transactions, the NPCI heavily promotes “UPI Lite.” This is essentially an “on-device wallet.” You load a small amount of money (up to ₹2,000) into the wallet, and you can make instant, PIN-less payments even if your internet connection is weak or the bank servers are temporarily down.

3. Voice-Based Payments

India is a highly diverse country with dozens of languages and millions of people who are not comfortable reading text on a screen. To solve this, conversational payments are being rolled out. In the near future, users will be able to simply speak into their phones and say, “Send 500 rupees to Rahul,” and the AI will process the UPI payment instantly using voice recognition in regional languages.

Conclusion: A Proudly Indian Achievement

The story of the ₹29.53 Lakh Crore record is not just a story about banking or finance; it is a story about Indian ingenuity.

For decades, developing nations have been told that they need to wait for wealthy Western countries to build the technology, and then buy it from them. UPI proved that narrative completely wrong. India built a piece of digital public infrastructure so powerful, so scalable, and so incredibly fast that the wealthiest countries in the world are now studying it, trying to figure out how we did it.

The next time you pull out your phone to scan a QR code for a simple cup of chai, take a second to appreciate the magic happening behind the screen. You are participating in the largest, most successful financial technology network in human history. Here is to the next milestone—the ₹50 Lakh Crore mark!

Frequently Asked Questions (FAQs): The UPI Miracle

Q1: What exactly does UPI stand for?

UPI stands for Unified Payments Interface. It is an instant real-time payment system developed by the National Payments Corporation of India (NPCI) that facilitates inter-bank peer-to-peer (P2P) and person-to-merchant (P2M) transactions securely using a smartphone.

Q2: Did people really send almost 30 Lakh Crore in just one month?

Yes! In March 2026, the exact total value was ₹29.53 Lakh Crore. This massive number is a combination of millions of small daily purchases (like groceries and tea) combined with high-value business transfers and tax payments made at the end of the financial year.

Q3: Who owns the UPI system? Is it a private company like Google or PhonePe?

No. Neither Google nor PhonePe own UPI. UPI is a public infrastructure built and owned by the National Payments Corporation of India (NPCI), which is backed by the Reserve Bank of India (RBI) and a consortium of major Indian banks. Google Pay and PhonePe are simply third-party apps that connect to this government-backed network.

Q4: Is it safe to link my bank account to UPI?

Yes, UPI is considered extremely safe. It is built on a highly secure, encrypted network. The app itself never stores your bank account password. Furthermore, every single transaction requires a secure, private UPI PIN that only you know. As long as you never share your PIN with anyone, your money is completely safe.

Q5: Why did the transaction volumes jump so high in March 2026?

March is historically the busiest financial month in India. First, the festivals of Holi and Eid led to massive consumer shopping. Second, March 31st is the end of the financial year, meaning all businesses and individuals were rushing to clear invoices, pay their final taxes, and make last-minute tax-saving investments, heavily relying on UPI for instant transfers.

Q6: Does the government charge a tax when I pay my local shopkeeper using UPI?

No! For regular retail customers paying a merchant (like a grocery store or a vegetable vendor) by scanning a QR code, the transaction is absolutely 100% free. There are no extra charges or taxes applied to the consumer for using UPI.

Q7: Can I use my Indian UPI app when I travel to foreign countries?

Yes, in specific countries! The NPCI has officially launched UPI in seven countries as of early 2026: the UAE, Singapore, Bhutan, Nepal, Sri Lanka, Mauritius, and France. If you visit these countries and see an authorized UPI QR code at a tourist spot or shop, you can scan it and pay using your Indian bank account!

Q8: What is UPI Lite and why should I use it?

UPI Lite is an “on-device wallet” feature within your UPI app. You can load a small amount of money into it. It allows you to make tiny payments (like ₹10 or ₹50) instantly without having to enter your UPI PIN. It is faster, it works even if the bank server is slow, and it stops your bank passbook from getting cluttered with hundreds of tiny ₹10 transactions!

Q9: Can I use a credit card on UPI, or is it only for debit/bank accounts?

You can now use credit cards! The RBI has officially allowed users to link their “RuPay” network Credit Cards to their UPI apps. Once linked, you can scan a merchant QR code and choose to pay the bill using your credit card limit instead of your bank savings account balance.

Q10: What happens if I accidentally send money to the wrong phone number on UPI?

Because UPI is instant, sending money to the wrong person is difficult to reverse. Your first step should be to immediately contact your bank and file a “wrong transfer” complaint. You should also raise a dispute within the UPI app (like GPay or PhonePe) and log a complaint on the official NPCI dispute portal. The bank will try to contact the receiver’s bank to reverse the funds, but it requires the receiver’s cooperation. Always double-check the name before entering your PIN!