Ever been to the vegetable market and wondered, “Why do prices fluctuate so much?” One week, tomatoes cost ₹60 per kilo; the next, they’re down to ₹30. Such price swings are generally linked to inflation—a measure of how prices of goods and services evolve over time. For many middle-class Indians, especially those in Tier-2 and Tier-3 cities, rising inflation can quickly strain monthly budgets. So, when news emerges about a drop in inflation, it feels like a small sigh of relief.

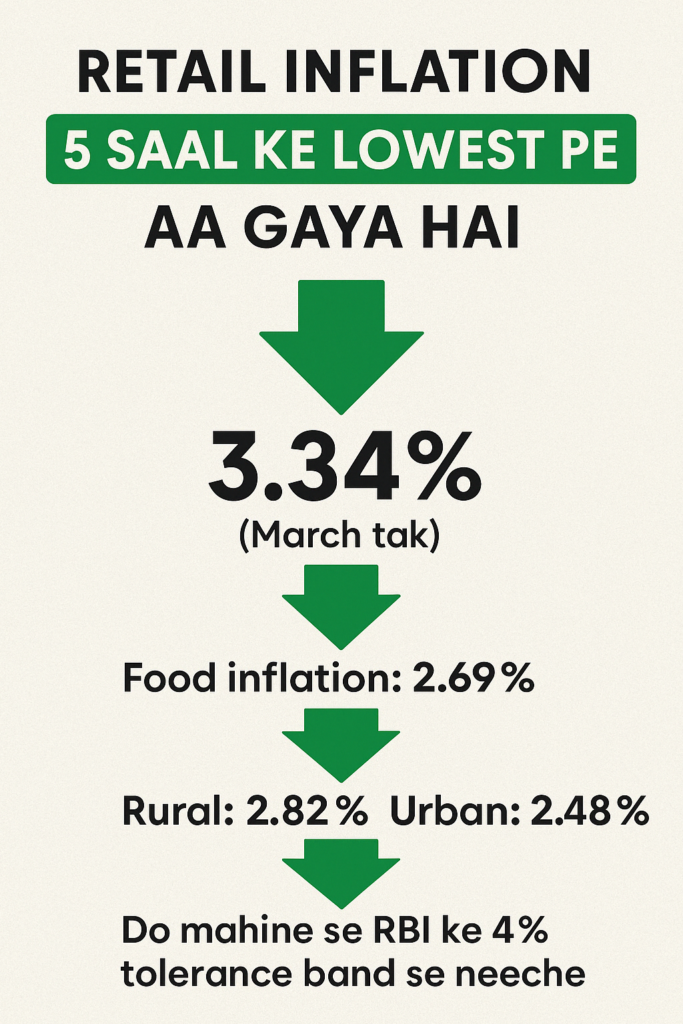

According to recent data released by the Union government, retail inflation in India (often tracked through the Consumer Price Index, or CPI) dipped to 3.34% in March—its lowest since August 2019. In February, it stood at 3.61%, indicating a continued trend downward. Even more noteworthy, food inflation saw a decline, falling to 2.69% in March from 3.75% in the previous month. This marks the second consecutive month where retail inflation remains below the Reserve Bank of India’s (RBI) tolerance level of 4%.

If you’ve been fretting over monthly expenses—from groceries to cooking gas and transport costs—this news could be a welcome break. But what exactly does low inflation imply for your day-to-day life, and how might it shape India’s economic climate? Read on to understand the nuances and the potential impacts, along with some practical tips on managing personal finances amid fluctuating inflation rates.

1. Understanding Inflation and Why It Matters

Inflation measures how much overall prices for goods and services increase over a specified time. When inflation rises, your purchasing power decreases—meaning you need more money to buy the same items as before. On the other hand, when inflation falls, it suggests a slower increase in prices or, in some scenarios, even a potential drop in specific commodity costs.

- Why You Should Care: For middle-class families with tight budgets, a 1% or 2% difference in inflation can substantially affect monthly grocery and utility bills. Over a year, this difference can free up money for savings, investments, or paying down debt.

- The RBI’s Tolerance Band: India’s central bank typically strives to maintain inflation around the 4% mark, with a 2% margin on either side (i.e., between 2% and 6%). Remaining below 4% for two months could influence the RBI’s approach to interest rates and overall monetary policy.

2. Snapshot of the Latest Data

- Overall Retail Inflation: Dropped from 3.61% in February to 3.34% in March—a 5-year low.

- Food Inflation: Declined to 2.69% from 3.75% previously, reflecting cheaper costs in staple items like vegetables and cereals.

- Rural vs. Urban: Rural inflation stands at 2.82%, while urban inflation is 2.48%. The difference underscores how price changes can impact daily essentials in distinct ways across India’s varied landscapes.

This downward trend suggests that, on average, you may be spending slightly less now on common household goods than you were a few months ago, or at least not seeing a significant surge in prices.

3. Factors Driving Lower Inflation

Stable Food Supplies

Food items often hold the biggest weight in India’s CPI. Recent improvements in agricultural yields—helped by favorable weather conditions—can boost the supply of essential crops (like cereals, vegetables, and pulses). When supply increases, prices tend to soften.

Global Commodity Markets

Inflation doesn’t exist in a bubble. If global fuel or commodity prices remain stable, India often feels the ripple effect. With moderate global demand in certain commodities, the cost of raw materials may not spike drastically, keeping local production costs (and therefore retail prices) in check.

Supportive Government Policies

Government interventions—like minimum support prices (MSP) for farmers or import/export adjustments—can shape food availability and costs. When well-calibrated, these policies help manage surpluses or shortages, mitigating extreme price hikes.

4. Impact on Your Pocket: Short-Term and Long-Term Views

Groceries and Daily Essentials

If you frequently buy vegetables, pulses, milk, or cereals, the data suggests you might find them marginally cheaper or at least stable in price. Even small changes—like ₹2 or ₹3 less per kilo—add up if you’re buying in bulk for a family of four or five.

Loan Rates and EMI Costs

Inflation influences monetary policy. When inflation goes below the RBI’s comfort zone, it sometimes prompts the central bank to consider lowering interest rates or adopting an accommodative stance. This decision can eventually ripple down to banks offering more competitive rates on personal loans, home loans, or car loans. For those with floating-rate EMIs, such a shift may translate into lower monthly outflows over time.

Saving and Investment Strategies

- Fixed-Income Instruments: When inflation is low, the “real return” (net of inflation) on a fixed deposit or recurring deposit can look more favorable.

- Equities: A stable or downward trending inflation can encourage markets if investors anticipate that companies will keep costs in check and preserve profit margins.

- Gold: Typically viewed as a hedge against inflation. If inflation remains subdued, gold prices might not spike significantly—though various factors also affect gold’s price, like global economic conditions and currency movements.

5. Potential Caution Flags

While low inflation is generally perceived as good news, it isn’t a free pass to ignore potential economic challenges:

- Risk of Deflation: If inflation dips too low for too long, it could indicate reduced consumer demand or a slowdown in economic activity.

- Uneven Benefits: Lower inflation doesn’t automatically mean every product in your local market gets cheaper. Some items might remain expensive if supply constraints persist in specific geographies or categories.

- Future Price Volatility: Commodity prices can be erratic; a single poor monsoon or a spike in global oil costs could reverse inflation trends quickly.

6. Practical Tips for Household Budgeting Amid Lower Inflation

Revisit Your Grocery Budget

Observe the changes in your monthly grocery expenses, especially for produce and staples. If you see a noticeable dip in outlay, consider redirecting that difference into a short-term savings plan or an emergency fund.

Evaluate Existing Debts

With inflation below the RBI’s 4% target for two consecutive months, you could anticipate the possibility (though not a guarantee) of interest rate adjustments. It might be a good time to consider if refinancing or switching to a floating rate loan could be beneficial.

Diversify Investments

While fixed deposits may look more appealing if deposit interest rates remain stable, it’s worth mixing them with other instruments—like debt mutual funds, equities, or balanced funds—depending on your risk appetite and goals. The drop in inflation alone shouldn’t fully dictate your portfolio choices, but it’s a useful factor to weigh in.

Prepare for the Unexpected

Lower inflation now doesn’t guarantee the same scenario six months down the line. Keep an eye on announcements from the RBI or significant changes in commodity markets. If you’re anticipating large future expenses (like a wedding or a property purchase), these rate changes might influence your planning strategy.

7. Urban vs. Rural: Bridging the Gap

The data highlights:

- Rural Inflation: 2.82%

- Urban Inflation: 2.48%

While both are under 3%, the rural figure is slightly higher. The difference might stem from limited access to wholesale markets or varied transportation costs. If you live in a rural area, you could still feel certain commodities are more expensive than your urban counterparts see on the same day. Understanding these nuances helps set realistic expectations and fosters empathy for price fluctuations across regions.

8. Looking Ahead: Could Inflation Rise Again?

Inflation rates aren’t fixed; they ebb and flow based on supply-demand shifts, government policies, monsoons, global markets, and more. Here are some watchpoints:

- Monsoon Quality: A poor monsoon season can hamper crop outputs and push up food prices.

- Crude Oil Volatility: As a key driver of transportation and production costs, any spike in global oil prices can trickle down to overall inflation.

- Global Economic Shifts: Factors like geopolitical tensions, trade policies, or currency valuation changes can indirectly affect domestic inflation.

Essentially, while we celebrate the relief from high inflation, remaining vigilant and prepared for potential reversals is wise.

Conclusion

For individuals and families juggling day-to-day expenses, retail inflation in India dropping to a 5-year low is an encouraging sign. If you’ve been struggling with surging vegetable prices or dreading your next utility bill, these recent numbers might hint at some financial breathing room. That said, it’s crucial to maintain perspective: inflation is just one piece of India’s dynamic economic puzzle.

Action Step: After reading about this new inflation data, why not reassess your monthly budget or recheck any outstanding loans? If you see meaningful changes in your expenses or anticipate new borrowing, consider speaking with a financial advisor or leveraging online calculators to see if any adjustments could help optimize your finances.

Ultimately, the hope is that lower inflation fosters more robust spending power among consumers—allowing you to spend confidently on essentials and maybe even indulge in that small luxury you’ve been putting off. Yet, remain watchful for policy changes and potential price swings in the months ahead. A well-informed approach ensures you’re financially ready, no matter which way inflation heads next.

FAQs (Frequently Asked Questions)

1. What exactly is “retail inflation,” and how is it measured in India?

Retail inflation reflects changes in the Consumer Price Index (CPI), which captures the average price of a basket of goods and services commonly bought by households. The CPI includes categories like food, clothing, housing, fuel, and more. Tracking these price movements provides insights into how the cost of living evolves for ordinary consumers.

2. Why does the RBI care about inflation being around 4%?

The Reserve Bank of India sets a target inflation range (currently 2%–6%, with a “comfort zone” at 4%) to maintain price stability and encourage predictable economic growth. If inflation rises too high, people’s real incomes shrink quickly; if it’s too low or negative, it could signal weaker consumer demand or a slowing economy.

3. Does lower inflation mean everything becomes cheaper?

Not necessarily. Lower overall inflation means prices, on average, rise more slowly (or some might even drop). However, certain items could still get more expensive if supply constraints exist. Always track your personal consumption basket to see which prices truly matter for your budget.

4. How can falling inflation affect interest rates?

If inflation remains below the central bank’s target for a prolonged period, the RBI might consider lowering policy rates to spur economic activity. This could translate into lower home loan or personal loan EMIs if banks pass on the rate cuts. However, many factors—like government borrowing requirements or global market conditions—also influence these decisions.

5. Will rural inflation always be higher than urban inflation?

No, it varies. Sometimes rural areas experience sharper price hikes for essentials (limited local supply, higher logistics costs), while in other periods, urban inflation may outpace rural inflation due to city-centric expenses like housing or transport. The differences reflect distinct supply chains and consumption patterns.

6. Should I change my investment strategy when inflation falls?

It depends on your goals. If the RBI shifts its monetary policy stance, interest rates on fixed deposits or debt instruments might change. Equities can react too, sometimes positively if lower inflation hints at stable corporate input costs. Still, focus on a long-term strategy, not just short-term inflation swings.

7. Are there drawbacks to inflation being too low?

Extremely low or negative inflation (deflation) can discourage consumer spending. People may delay purchases expecting prices to drop further, and businesses might see reduced profits, hampering economic growth. Thus, “moderate” inflation is generally considered healthy.

8. How does the government manage inflation levels?

Through a mix of monetary policy (the RBI adjusting repo rates, cash reserve ratios) and fiscal measures (government subsidies, controlling MSP or import duties, etc.). Also, supply-side interventions—improving logistics, storage facilities, or agricultural inputs—can manage food prices effectively.

9. Where can I track inflation changes monthly?

Official data is released by the Ministry of Statistics and Programme Implementation (MoSPI). Financial news portals, the RBI website, and reputable newspapers also publish monthly CPI figures. Keeping a casual eye on these sources can help you anticipate shifts that affect your cost of living.

By staying informed about retail inflation in India and adjusting your household budgeting or loan decisions accordingly, you can better navigate day-to-day costs and foster a healthier financial outlook—regardless of whether inflation edges lower or takes a turn in the coming months.