TL;DR: Key Takeaways on Credit Card Fraud Prevention

If you are short on time and need to secure your card right now, here is your quick summary:

- The New Threat: Fraud has evolved from physical theft to AI-driven impersonation, sophisticated phishing links, and account takeovers.

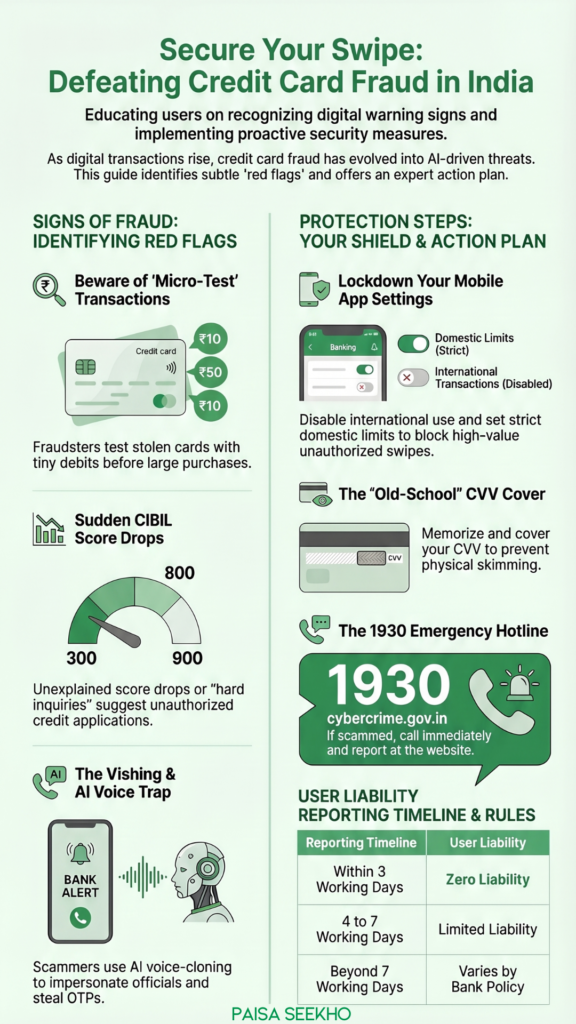

- The Silent Killer: Fraudsters often test stolen cards with tiny transactions (like ₹10 or ₹50) before making massive purchases. Never ignore a small, unknown debit.

- The Defense: Never share your OTP, CVV, or card number. Set strict transaction limits on your mobile banking app.

- Monitor Your Credit: Review your CIBIL score every 3 to 6 months to spot unauthorized credit checks or ghost accounts opened in your name.

- Immediate Action: If scammed, block the card via your app instantly, call the national cybercrime helpline at 1930, and report it on the official cybercrime.gov.in portal.

Introduction

You just finished a long day at work. You are relaxing on the couch, scrolling through your phone, when a sudden SMS pops up: “Transaction of ₹45,000 completed at a foreign merchant.”

Your heart sinks. Your credit card is sitting safely in your wallet. You haven’t bought anything. But in a matter of seconds, your hard-earned money has vanished.

As digital transactions in India continue to break global records, we are enjoying unparalleled convenience. But this hyper-connected ecosystem has also created a playground for highly sophisticated cybercriminals. Therefore, credit card fraud is no longer just about someone stealing your physical plastic card on a bus; it has evolved into a silent, invisible, AI-driven digital threat.

According to cybersecurity experts, credit card fraud is rising sharply in 2026. The most terrifying part? The victims generally only realize the extent of the damage when their credit score crashes or the collection agents start calling.

If you own a credit card, hoping for the best is not a security strategy. In this comprehensive, easy-to-understand guide, we are going to break down exactly how modern fraudsters steal your details. We will explore the silent warning signs you are probably ignoring, and provide you with an expert-backed action plan to shield your finances today.

What Are the Most Common Types of Credit Card Fraud Today?

Having a clear understanding of the enemy’s tactics is the first step to early detection. The days of a thief stealing your card and running to a jewelry store are largely over. Today’s threats are entirely digital.

1. Phishing and “Vishing” (The Impersonators)

This is the most common scam. You receive a highly professional-looking email, SMS, or phone call (Vishing). The caller pretends to be from your bank or a government agency. They create a sense of extreme panic (e.g., “Your card will be blocked in 10 minutes if you don’t verify this OTP”). In their panic, victims hand over their OTPs or CVV codes, giving the scammer instant access to their funds.

Experts warn that scammers are now using AI voice-cloning technology to sound exactly like bank officials or even family members!

2. Card-Not-Present (CNP) Fraud

Fraudsters buy stolen credit card databases on the dark web. They do not need your physical card; they just need the 16-digit number, expiration date, and CVV. They use these details to make massive purchases on international e-commerce websites where OTP verification is often not required.

3. Skimming

This happens in the physical world. Fraudsters install tiny, invisible card-reading devices (skimmers) inside ATM card slots or at merchant payment terminals (like a shady petrol pump). When you swipe your card, the skimmer copies the magnetic strip data, and a hidden camera records your PIN. They use this data to clone a duplicate card.

4. Account Takeover

This is a highly sophisticated attack. The fraudster gathers your personal information (from social media or data breaches) and contacts your bank, pretending to be you. They convince the bank to change your registered mobile number and address. Once they control the account, they request a new credit card to be mailed to their address, locking you out of your own finances entirely.

What Are the Silent Warning Signs Your Card is Compromised?

Most people wait for a massive ₹50,000 transaction before they realize they have been scammed. By then, the money is gone. You need to train yourself to look for the silent red flags.

1. The “Micro-Test” Transaction

Fraudsters are smart. When they steal your card details, they do not immediately buy an expensive laptop. First, they test the card to see if it is active. You might see a strange, unknown debit of just ₹10, ₹50, or a small foreign currency charge (like $1.00) on your statement. If you ignore this “micro-test,” the massive transaction will happen a few days later.

2. A Sudden Drop in Your CIBIL Score

If a scammer uses your identity to apply for multiple new credit cards or massive loans, it will leave a footprint on your credit report. If you check your CIBIL score and see a sudden, unexplained drop, or notice “hard inquiries” from banks you never applied to, your identity has been compromised.

3. Missing Mail or Bills

If you suddenly stop receiving your physical credit card statements or official bank communications, a fraudster might have initiated an “Account Takeover” and redirected your mail to a new address to hide their spending tracks.

5 Expert Tips to Shield Your Credit Card from Digital Thieves

The strongest defense against fraud is vigilance and proactive technology management. Here are five expert-backed ways to lock down your credit card:

1. The Power of Transaction Limits

This is the easiest and most effective hack. Open your mobile banking app right now. Find the “Card Settings” or “Manage Limits” tab.

- Disable “International Transactions” completely unless you are traveling abroad.

- Set a strict daily limit for online domestic transactions (e.g., ₹10,000).

If a scammer tries to swipe your card for ₹50,000, the bank’s system will automatically decline it because it breaches your custom limit.

2. Never Use Public Wi-Fi for Banking

Free Wi-Fi at airports, cafes, and hotels is notoriously insecure. Cybercriminals can easily set up fake networks or intercept data on public connections. Never make an online purchase, check your bank balance, or enter your credit card details unless you are on a secure, private home Wi-Fi network or using your cellular mobile data.

3. Embrace Virtual Credit Cards

Many modern banks now offer “Virtual Credit Cards” or single-use card numbers within their apps. If you are shopping on a new, unfamiliar website, generate a virtual card. It gives you a temporary 16-digit number tied to your actual account. Even if the website is hacked and the card number is stolen, it is completely useless to the fraudster because it expires after one use!

4. Cover Your CVV

This is an old-school trick that still works perfectly. Memorize the 3-digit CVV on the back of your physical card, and then scratch it off or cover it with a dark, opaque sticker. If a waiter or shopkeeper tries to quickly memorize your card details while processing a payment, they won’t have the CVV required to make online purchases later.

5. Read Your Statement Line-by-Line

Do not just look at the “Total Amount Due” and pay the bill. Treat your monthly statement like a forensic report. Look at every single line item. If you see a merchant name you do not recognize, dispute the charge immediately with your bank.

What Should You Do Immediately If You Become a Victim?

Panic is your worst enemy during a fraud event. If you notice an unauthorized transaction, you must act with military precision within the first few minutes.

- Block the Card Instantly: Do not waste time calling customer care if you can avoid it. Open your mobile banking app and use the “Temporarily Block” or “Hotlist” feature to instantly freeze the card.

- Call the National Helpline: Dial 1930 immediately. This is the official emergency helpline for the National Cyber Crime Reporting Portal.

- Register an Official Complaint: Go to the official government website at cybercrime.gov.in and register a formal complaint with all the transaction details. You can also log a complaint at the RBI’s Sachet portal (sachet.rbi.org.in).

- Dispute the Charge with Your Bank: Call your bank’s fraud department, give them the cybercrime complaint number, and officially “Dispute” the transaction. Under RBI rules, if you report the fraud within 3 working days, and the fraud was not due to your own negligence (like sharing an OTP), your financial liability is generally zero.

Conclusion: Convenience Requires Caution

In 2026, a credit card is one of the most powerful financial tools you can own. It builds your credit score, offers incredible rewards, and acts as an emergency safety net.

But with great power comes the responsibility of digital hygiene. Fraudsters are relying on your laziness. They are hoping you ignore the small ₹50 charges, that you leave your international limits open, and that you blindly trust a panic-inducing SMS.

By taking five minutes today to customize the security settings on your mobile app, and by treating your OTPs like the keys to your house, you can enjoy the unparalleled convenience of digital payments without ever losing a rupee to a scammer.

Frequently Asked Questions

Q1: What is a Card-Not-Present (CNP) fraud?

CNP fraud occurs when a scammer makes an online purchase using your stolen credit card details (card number, expiry, and CVV). They do not need to steal the actual physical plastic card to execute this scam.

Q2: Should I keep my international transactions enabled on my credit card?

Absolutely not. You should keep international transactions strictly disabled in your mobile banking app at all times. Only toggle them “ON” when you are actually traveling abroad or actively making a purchase on a foreign website, and turn them back off immediately after.

Q3: How do skimmers steal my credit card data?

Skimmers are tiny, illegal card readers secretly attached to ATMs or physical merchant payment machines. When you swipe your card, the device copies the magnetic strip data, allowing the fraudster to create a cloned duplicate of your card.

Q4: Will I get my money back if I am a victim of credit card fraud in India?

According to the RBI, if you report the unauthorized transaction to your bank within 3 working days, and you did not compromise your own security (e.g., you did not voluntarily share your OTP or PIN with the scammer), your liability is zero, and the bank must reverse the charge.

Q5: Why did the scammer only charge ₹10 on my credit card?

Fraudsters do “micro-tests.” They run a tiny transaction (like ₹10 or $1) to verify that the stolen card details are valid and active before they attempt a massive, high-value purchase a few days later. Never ignore these small charges.

Q6: What is “Vishing”?

Vishing (Voice Phishing) is when a scammer calls you on the phone, pretending to be a bank official or a police officer. They use psychological manipulation and panic tactics to trick you into verbally sharing your OTP, PIN, or CVV.

Q7: How can checking my CIBIL score help prevent fraud?

By checking your CIBIL credit report every 3 to 6 months, you can spot “Account Takeovers.” If a fraudster steals your identity to apply for new credit cards or loans in your name, it will show up as a “hard inquiry” or a new active account on your CIBIL report.

Q8: What is the official government website to report credit card fraud in India?

You should immediately report any digital financial fraud to the National Cyber Crime Reporting Portal at cybercrime.gov.in or call the national emergency helpline at 1930.

Q9: Are public Wi-Fi networks safe for online shopping?

No. Public Wi-Fi networks in cafes, airports, and hotels are highly insecure. Hackers can easily intercept the data transmitted over these networks. Always use a secure private Wi-Fi connection or your mobile data when entering credit card details online.

Q10: What is an Account Takeover (ATO) fraud?

ATO fraud happens when a scammer successfully convinces your bank that they are you. They change your registered mobile number and address in the bank’s system, effectively locking you out of your own account, and then request replacement credit cards sent to their location.