TL;DR: Key Takeaways on EPFO 3.0 PF Withdrawal Rules

If you are in a rush and just need the most critical updates on your PF account, here is a quick summary of the 2026 rules:

- The ATM and UPI Revolution: You no longer have to wait weeks for emergency cash. EPFO 3.0 introduces PF-linked ATM cards and a mobile app for UPI withdrawals.

- The 50% Emergency Cap: To ensure you do not accidentally drain your retirement savings, instant ATM and UPI withdrawals are strictly capped at 50% of your total EPF balance.

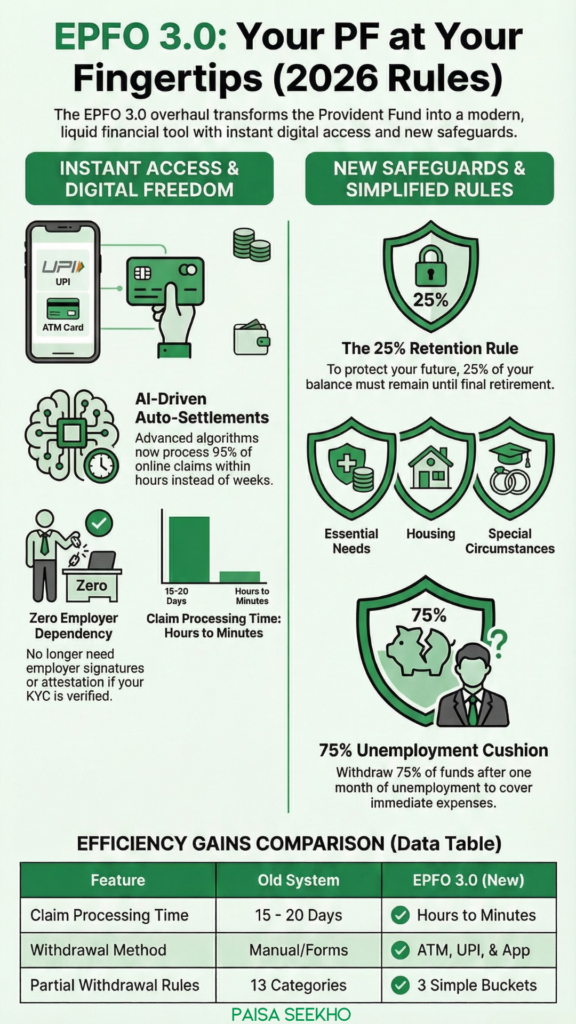

- Lightning-Fast Processing: The new AI-driven system automatically processes and settles 95% of online claims within hours or even minutes, eliminating the old 20-day waiting period.

- The “25% Retention” Rule: To protect your long-term future, the new rules mandate that 25% of your eligible balance must remain in the account at all times until absolute final retirement.

- No More Employer Attestation: You are now in complete control. If your Aadhaar, PAN, and bank details are verified, you do not need your employer’s approval to withdraw your money.

- Simplified Withdrawals: The confusing 13 categories for partial withdrawal have been merged into just 3 simple buckets. Plus, you can now withdraw for education up to 10 times, and for marriage up to 5 times.

Introduction

If you are a salaried employee in India, the Employees’ Provident Fund (EPF) is probably your biggest financial safety net. A portion of your hard-earned salary goes into this account every single month, slowly building a massive corpus for your retirement or emergencies.

But let’s be completely honest for a moment: actually taking your own money out of that account used to be an absolute nightmare.

Historically, withdrawing your PF felt like running a bureaucratic marathon. You had to fill out complicated forms, beg your past employers for physical signatures and attestations, upload blurry photos of your bank passbook, and then wait anywhere from 15 to 20 days praying that your claim would not get rejected over a minor spelling mistake. It was stressful, slow, and incredibly frustrating.

Thankfully, the government has heard these complaints. In 2026, the Employees’ Provident Fund Organisation (EPFO) has completely rewritten the rulebook and overhauled its digital infrastructure. Welcome to the era of EPFO 3.0.

Rolling out fully in mid-2026, EPFO 3.0 transforms your traditional, slow-moving retirement fund into a highly liquid, incredibly smart, and easily accessible financial tool. From allowing you to swipe an ATM card to access your PF, to withdrawing funds instantly via UPI, the system has fundamentally changed.

1. EPFO 3.0 PF Withdrawals via ATM and UPI

Let us start with the most futuristic and exciting feature of EPFO 3.0. For the first time in Indian history, your Provident Fund will behave a little bit like a regular bank savings account.

The PF ATM Card

Under the new system, eligible EPFO members will be issued physical ATM cards directly linked to their UAN (Universal Account Number) and PF balance.

Imagine you are facing a sudden medical emergency in the middle of the night. In the old days, your PF money was useless in that exact moment. Now, you can walk into an authorized bank ATM, insert your EPFO card, authenticate the transaction using a secure PIN or OTP, and withdraw physical cash directly from your retirement corpus.

The UPI Integration

If you do not want to carry a physical card, the EPFO has partnered with major banks and the National Payments Corporation of India (NPCI) to integrate PF accounts directly into the UPI ecosystem via a newly launched mobile application. You can check your PF balance live on the app and instantly transfer eligible funds to your bank account using the UPI network.

The Safety Net: The 50% Cap

While this sounds incredible, the EPFO is fully aware that making retirement money too easy to access is dangerous. Human nature might tempt people to withdraw their PF to buy a new smartphone or take a vacation.

To prevent you from destroying your financial future, the government has placed a strict speed limit on this feature. You can only withdraw a maximum of 50% of your total EPF balance using the instant ATM or UPI features. This brilliant compromise provides you with instant liquidity for genuine emergencies while securely locking away the other half of your money to ensure you still have a safety net when you retire.

2. Auto-Claim Settlement Rules Under EPFO 3.0

If you applied for a PF withdrawal in 2023 or 2024, you probably remember checking the portal every day, watching the status sit on “Pending” for weeks. The old system required human officers to manually open your file, check your documents, verify your service history, and approve the payment.

EPFO 3.0 changes the game entirely with advanced algorithms and automation.

Under the new 2026 framework, 95% of all withdrawal claims will be settled automatically by the system. When you submit a claim for an illness, a marriage advance, or an education withdrawal, the computer instantly cross-checks your digital KYC (Aadhaar, PAN, and Bank Account). If all the data matches perfectly and you meet the mathematical eligibility criteria, the system approves the claim without a human officer ever looking at it.

What used to take 15 to 20 business days is now reduced to a few hours, and in some cases, a few minutes. The money is transferred seamlessly into your verified bank account via NEFT or RTGS.

3. The “25% Retention” Rule For Guarding Your Future

With all this speed and accessibility, the government had to introduce a structural guardrail to ensure the fundamental purpose of the Provident Fund—funding your old age—was not defeated.

This brings us to the new Minimum Balance Requirement.

Under the updated EPFO 3.0 rules, members are required to maintain a baseline of 25% of their total eligible balance in the account at all times during their active working years.

Even if you face an emergency and max out your allowable withdrawals, the system will mathematically block you from draining the account down to zero. That final 25% is untouchable until you reach the official retirement age of 55, face permanent disability, or permanently emigrate from India.

The good news? That retained 25% doesn’t just sit there doing nothing. It continues to attract the massive annual compound interest rate (which currently hovers around 8.25%), ensuring that your wealth quietly multiplies in the background while you navigate your career.

4. Goodbye to 13 Rules: The 3 New Simplified Categories

The old EPF rulebook was famously frustrating. There were 13 different, highly specific clauses for partial withdrawals. You had different rules for buying a plot of land, different rules for renovating a house, and different rules for illness. Each required different minimum years of service.

EPFO 3.0 has thrown out the confusing paperwork and consolidated everything into three simple, unified categories. Furthermore, the mandatory service requirement for most partial withdrawals has been drastically reduced to just 12 months of service.

Category 1: Essential Needs (Education, Marriage, and Medical)

This is the most frequently used bucket. It covers the major milestones and emergencies of a standard middle-class life.

- Education: Previously, you could only withdraw money for education a limited number of times. The new rules generously allow you to withdraw funds for your children’s higher education up to 10 times during your entire career.

- Marriage: You can withdraw funds for your own marriage, or the marriage of your children, sister, or brother. The new rules have relaxed the limit, allowing you to use this provision up to 5 times.

- Medical Emergencies: For serious illnesses affecting yourself or your immediate family, you can instantly withdraw the lower of your total employee share (with interest) or 6 months of your basic wages plus Dearness Allowance (DA).

Category 2: Housing Requirements

Buying a home is the great Indian dream, and the EPF is often the only way middle-class families can afford the down payment.

Under this simplified category, you can withdraw up to 90% of your total EPF balance to purchase or construct a residential property in your name or jointly with your spouse. If you already own a home, you can withdraw an amount equal to 12 months of your basic wages to fund home renovations or expansions.

Category 3: Special Circumstances

This bucket covers absolute worst-case scenarios, such as your company shutting down permanently, or you not receiving your salary for more than two consecutive months due to employer bankruptcy. In these extreme situations, the system allows you to withdraw 100% of your own employee contribution to survive the crisis.

5. Job Loss and Unemployment Rules Under EPFO 3.0

Losing a job is terrifying. In the past, the EPFO allowed you to withdraw 100% of your money if you were unemployed for two months. However, they realized this encouraged young people to completely drain their retirement funds between jobs, ruining their long-term financial planning.

The 2026 rules have drastically altered the timeline for unemployed individuals.

The Immediate Safety Net (75%):

If you lose your job or resign, and remain unemployed for one full month, you are eligible to immediately withdraw up to 75% of your total PF balance. This provides you with a massive cushion of cash to pay your rent, buy groceries, and cover your EMIs while you search for a new job.

The Extended Waiting Period (25%):

What happens to the remaining 25%? Under the old rules, you could grab it after just two months. Under the new EPFO 3.0 rules, you cannot access that final 25% until you have been continuously unemployed for 12 months.

This rule is designed to force you to keep your PF account active. If you find a new job within a few months (which most people do), you simply transfer that remaining 25% to your new employer, keeping the chain of compound interest alive.

The Pension (EPS) Lock-in:

Every month, a small portion of your employer’s contribution goes into the Employees’ Pension Scheme (EPS). If you have worked for less than 9.5 years, you are allowed to withdraw this cash using Form 10C. However, EPFO 3.0 has extended the waiting period to withdraw this pension cash to 36 months post-unemployment. The government is heavily incentivizing workers to leave their pension money alone so they can eventually qualify for a monthly lifetime pension.

6. The End of Employer Dependency

Perhaps the most liberating update in EPFO 3.0 is that the employee is finally the undisputed owner of their account.

For decades, unethical employers used the PF system as a weapon. If you quit your job on bad terms, the HR department would refuse to digitally attest your withdrawal forms or delay updating your “Date of Exit” on the portal, essentially holding your own money hostage.

Under EPFO 3.0, employer attestation is dead.

You do not need your old boss’s permission to touch your money. As long as your digital profile is complete, you are in total control. The system relies entirely on independent digital verification.

Furthermore, you no longer have to beg HR to fix spelling mistakes in your name or date of birth. The new portal allows employees to make corrections to their own PF profiles directly using an Aadhaar-linked OTP verification process.

7. The Digital Ecosystem: DigiLocker, Face Auth, and No More Cheques

The EPFO has fully embraced the “Digital India” stack, stripping away the annoying paperwork that used to define the process.

1. No More Uploading Cancelled Cheques

In the past, you had to physically scan a cancelled cheque or a stamped bank passbook and upload the image so the EPFO could verify your bank account. It was a massive reason for claim rejections if the image was blurry.

Under the new streamlined rules, this requirement is completely eliminated. Because your bank account is already verified directly through the NPCI and your bank’s database using your IFSC code and Aadhaar linkage, the system trusts the digital handshake. No uploads required!

2. Face Authentication via UMANG

Forgetting passwords or struggling with mobile network OTPs is no longer a roadblock. You can now securely log into your account and verify your UAN (Universal Account Number) using advanced Face Authentication technology directly through the government’s UMANG mobile app.

3. DigiLocker Integration

Your essential EPFO documents—such as your UAN Card, your Pension Payment Order (PPO) for retirees, and your Scheme Certificates—are now automatically pushed to your DigiLocker app. You can access your official retirement documents securely from your smartphone, anytime, anywhere.

8. The Tax Implications of Your PF Withdrawal

While the technology has changed, the strict rules of the Income Tax Department remain exactly the same. Before you tap on that new UPI app to withdraw your PF, you need to understand the tax math.

The taxation of your Provident Fund depends entirely on one metric: Your continuous years of service. * The 5-Year Rule: If you have worked continuously for 5 years or more (this includes working at multiple different companies, as long as you properly transferred your UAN balance each time you switched jobs), your PF withdrawal is 100% Tax-Free. You do not pay a single rupee to the government.

- Less than 5 Years: If you withdraw your PF before completing 5 years of continuous service, the money loses its tax-exempt status. It is treated as regular income.

- The TDS Trap: If your service is less than 5 years and your withdrawal amount is greater than ₹50,000, the EPFO will deduct a 10% TDS (Tax Deducted at Source) before sending you the money. Crucial warning: If your PAN card is not properly linked to your UAN, that TDS rate skyrockets to a massive 30%! Always ensure your PAN is verified.

9. Security Risks: The Dark Side of the ATM Revolution

While the convenience of EPFO 3.0 is unparalleled, it is vital to acknowledge the new risks.

By issuing physical ATM cards and enabling UPI transactions, the EPFO has exposed retirement funds to the same vulnerabilities that plague regular bank accounts.

- ATM Skimming: Fraudsters can attach hidden skimming devices and tiny cameras to bank ATMs to steal your EPFO card details and PIN.

- UPI Scams: Phishing links, fake QR codes, and social engineering scams over the phone could trick vulnerable employees into accidentally transferring their retirement savings to cybercriminals.

Because of this, digital literacy is more important than ever. Treat your PF ATM card with the exact same caution as your primary debit card. Never share your OTP, never share your PIN, and ensure biometric authentication is enabled on your mobile phone before using the new EPFO UPI app.

Conclusion: Total Financial Freedom

The launch of EPFO 3.0 in 2026 is not just a software update; it is a fundamental shift in how the Indian working class interacts with their wealth.

For generations, the Provident Fund felt like money that belonged to the government or the employer, locked away in a distant vault that you could only access if you jumped through dozens of bureaucratic hoops.

Today, that money is finally back in your pocket. By empowering you with ATM cards, instant UPI withdrawals, AI-driven auto-settlements, and total freedom from employer attestations, the government has given you total financial independence. Keep your KYC updated, link your Aadhaar, and enjoy the peace of mind that comes with knowing your life savings are just a tap away whenever you truly need them.

Frequently Asked Questions (FAQs): EPFO 3.0 Rules

Q1: What exactly is EPFO 3.0?

EPFO 3.0 is a massive technological and policy upgrade by the Employees’ Provident Fund Organisation (expected to be fully active by mid-2026). It modernizes the entire retirement system, introducing features like AI-driven auto-claim settlements, ATM cards for PF withdrawal, UPI integration, and the removal of physical paperwork.

Q2: Can I withdraw 100% of my PF using the new ATM card?

No. To protect your retirement savings, the EPFO has placed a strict limit on instant access. You can only withdraw a maximum of 50% of your total EPF balance using the new ATM cards or the UPI mobile app.

Q3: How fast will I get my money if I apply online?

Incredibly fast. Under the old system, it took up to 20 days. Under EPFO 3.0, the system uses automation to settle 95% of standard online claims. If your KYC is perfect, the money can hit your bank account in a matter of hours, or even minutes.

Q4: Do I still need my old company’s HR to approve my withdrawal?

Absolutely not. This is one of the biggest benefits of the new system. As long as your UAN is activated and your Aadhaar, PAN, and Bank Account details are digitally verified in your profile, you do not require any approval or attestation from your current or former employer.

Q5: I just lost my job. How much PF can I withdraw immediately?

Under the 2026 rules, if you remain unemployed for one full month, you can immediately withdraw 75% of your total PF balance to cover your living expenses.

Q6: What happens to the remaining 25% after a job loss?

The new rules mandate that you must wait until you have been continuously unemployed for 12 months before you can withdraw the final 25% of your PF balance. This is designed to encourage you to keep the account active and transfer it to your next employer.

Q7: Is it true that I have to keep a minimum balance in my PF now?

Yes. To ensure members do not completely drain their retirement safety net during their working years, the new rules state that a baseline of 25% of your eligible contribution must be maintained in the account at all times (until retirement or severe disability).

Q8: How many times can I withdraw PF for my children’s education?

The rules have been significantly relaxed. Under the “Essential Needs” category of EPFO 3.0, an employee can make partial withdrawals for educational purposes up to 10 times during their entire service tenure.

Q9: Do I have to upload a cancelled cheque to verify my bank account online?

No. The new simpler online claim submission process has removed the need to scan and upload a cancelled cheque or a bank passbook. The system automatically verifies your bank details directly with the bank’s servers using your IFSC code and Aadhaar linkage.

Q10: Will I be taxed if I withdraw money using the new UPI app?

The method of withdrawal does not change the tax laws. If you have been contributing to the EPF for more than 5 continuous years, your withdrawal is 100% tax-free. If your service is less than 5 years and the amount is over ₹50,000, you will be subject to a 10% TDS (or 30% if your PAN is not linked).