TL;DR: The Quick April 1, 2026 Checklist

If you are in a rush, here is a quick summary of the financial rules changing today:

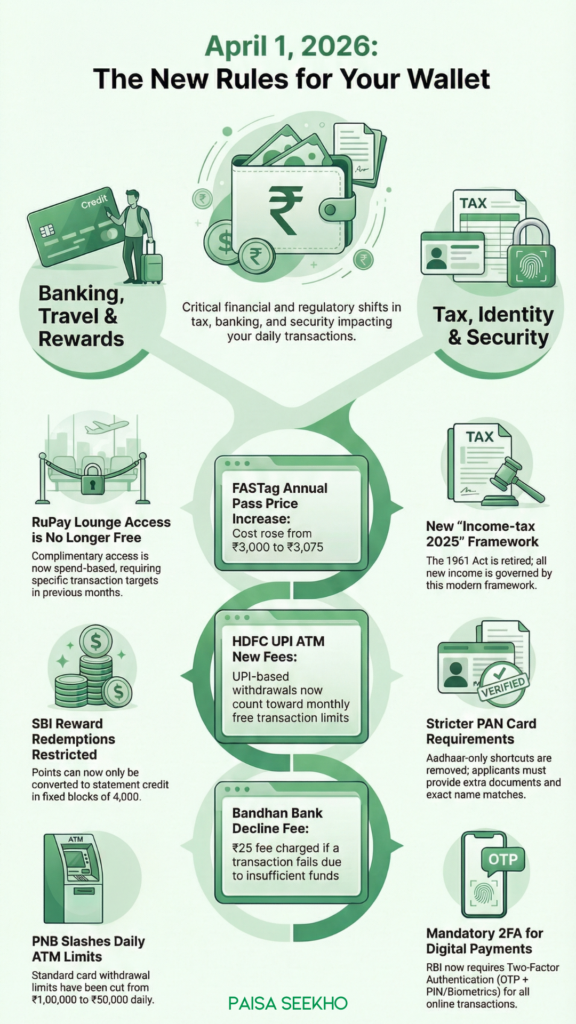

- A New Tax Law: The old Income-tax Act of 1961 is officially retired. The brand-new “Income-tax 2025” framework takes over today.

- Stricter PAN Card Rules: You can no longer get a PAN card instantly using only your Aadhaar card. You now need extra documents, and your name on both cards must match perfectly.

- SBI Credit Card Rewards: If you use an SBI Card, you can now only convert your reward points into statement credit in fixed blocks of 4,000 points.

- Costlier FASTag Passes: For frequent highway drivers, the NHAI has increased the price of the FASTag Annual Pass from ₹3,000 to ₹3,075.

- ATM Rules Revised: HDFC Bank is now charging for UPI-based cash withdrawals once you cross your free limit. Punjab National Bank (PNB) has slashed its daily cash withdrawal limits in half.

- No More Free Lounges for RuPay: The “cheat code” is over. RuPay Platinum debit cards no longer give you automatic, unconditional free access to airport and railway lounges.

- Double Security for Digital Payments: The RBI has mandated Two-Factor Authentication (2FA) for all digital payments to protect you from online scams.

Introduction

Happy New Financial Year! If you are reading this on or after April 1, 2026, we have officially entered Financial Year 2026-27 (FY27).

While New Year’s Day on January 1st is all about personal resolutions and gym memberships, April 1st is the day the government and banks make their own resolutions. Every year on this date, a massive wave of new financial rules, banking fees, and tax laws come into effect. It is the day the financial system resets.

This year is bringing some of the biggest structural changes we have seen in decades. From a completely new Income Tax Act replacing a 65-year-old law, to stricter rules for getting a PAN card, to new limits on how much cash you can pull out of an ATM, the rules of the game have changed.

If you do not pay attention, these changes can lead to unnecessary fees, rejected applications, or lost credit card rewards. This comprehensive, easy-to-understand checklist will break down every major rule change taking effect on April 1, 2026. Now you can protect your wallet and stay ahead of the curve.

1. The Biggest Overhaul: The New Income-Tax Law

Let’s start with the biggest news of the decade. For the last 65 years, every single taxpayer in India has been governed by the Income-tax Act of 1961. That era officially ends today.

What is changing?

Starting April 1, 2026, the government has implemented the brand-new Income-tax 2025 framework. The old 1961 Act stands fully repealed.

What this means for you:

The government’s goal with this new law is to simplify the complex web of taxes. They also want to remove outdated rules, and make the legal language much easier to understand.

Do not panic. If you have an ongoing tax dispute, an appeal in court, or a pending tax notice from the previous years, the government has created “transitional provisions.” This simply means older cases will be allowed to finish under the old rules so that the system doesn’t completely break down. However, all your fresh income earned from today onward will be taxed, assessed, and processed under this massive new legal framework.

2. PAN Card Applications Just Got Stricter

Your Permanent Account Number (PAN) is the most important financial document you own. For the past few years, the government made it incredibly easy to get a PAN card. You could just go online, type in your Aadhaar number, and get an OTP. An electronic PAN would be generated instantly.

What is changing?

That easy, Aadhaar-only shortcut officially expired on March 31, 2026. Starting today, April 1, the rules are much stricter.

What this means for you:

- Extra Documents: You can no longer rely just on Aadhaar e-KYC. You must submit additional supporting documents to prove your identity and address.

- The Name Match Rule: The income tax department is cracking down on mismatched data. From today, the name printed on your new PAN card application must match the name on your Aadhaar records exactly. Even a missing middle name or a different spelling will cause your application to be rejected.

- New Forms: The government has introduced specific new forms depending on who you are. Regular citizens must use Form 93. Companies use Form 94, foreign individuals use Form 95, and foreign companies use Form 96.

If you need a new PAN or need to update your old one, you must make sure your Aadhaar details are perfectly up-to-date first!

3. SBI Credit Card Reward Point Restrictions

Credit card companies love to give you reward points to encourage you to spend more. Many smart users save up these points and then convert them into “Statement Credit,. This basically means the bank uses your points to pay off a portion of your credit card bill.

What is changing?

SBI Card (which manages the incredibly popular Cashback SBI Card and other variants) has officially changed how you can use rewards.

What this means for you:

Starting April 1, 2026, you can only convert your reward points into statement credit in fixed blocks of 4,000 points.

Let’s look at an example to make this simple. Imagine you have saved up 6,500 reward points. In the past, you could convert all 6,500 points into cash to lower your bill. Under the new rule, you cannot do that. You can only redeem a block of 4,000 points. The remaining 2,500 points will just sit in your account. You will have to wait until you earn another 1,500 points (bringing your total to 8,000) before you can redeem the next block.

This forces customers to either spend more money to reach the 4,000-point milestones or leave their rewards unused.

4. Highway Driving Gets Pricier: FASTag Annual Pass Hike

If you drive on national highways, you already know about FASTag. It’s the sticker on your windshield that automatically pays toll so you do not have to stop at a booth.

Most people just recharge their FASTag with a few hundred rupees whenever they take a road trip. But for people who live near a toll plaza or commute across a toll every single day for work, paying the fee twice a day is too expensive. For these frequent travelers, the National Highways Authority of India (NHAI) offers a “FASTag Annual Pass,”. This gives them unlimited local travel for a flat yearly fee.

What is changing?

The NHAI has officially raised the price of this pass for the FY 2026-27 financial year.

What this means for you:

Starting today, the cost of the FASTag annual pass for non-commercial vehicles (like your personal family car, van, or jeep) has increased from ₹3,000 to ₹3,075. While a ₹75 increase might seem small, it affects millions of daily commuters who rely on the pass to get to work across the 1,150 fee plazas on National Highways and Expressways.

5. Major Changes to ATM Withdrawals and Fees

The way we use ATMs is changing. With the massive rise of UPI (scanning QR codes with our phones), people are using physical cash much less. Because of this, banks are restructuring their ATM networks, lowering withdrawal limits to prevent fraud, and introducing new fees.

Three major banks have rolled out new ATM rules effective April 1, 2026:

HDFC Bank: UPI ATM Withdrawals Now Cost Money

Did you know you can withdraw physical cash from an ATM without a debit card? You can just scan a QR code on the ATM screen using your UPI app. It is a brilliant feature.

- The New Rule: HDFC Bank has announced that these “UPI-based cash withdrawals” are no longer a free bonus. Starting today, every time you use UPI to withdraw cash from an HDFC ATM, it will be counted toward your standard monthly limit of free ATM transactions.

- The Penalty: If you use up all your free monthly ATM visits, HDFC will charge you a heavy fee of ₹23 plus taxes for every extra UPI withdrawal you make.

Punjab National Bank (PNB): Slashing Daily Limits

If you are a PNB customer, your debit card just lost a lot of its cash-pulling power. To protect customers from massive financial losses if their card is stolen or cloned, PNB has drastically reduced the amount of cash you can withdraw in a single day.

- For standard cards (like the RuPay Platinum, Women Power, and Palaash debit cards), the daily ATM withdrawal limit has been chopped in half, dropping from ₹1,00,000 down to just ₹50,000.

- For premium cards (like the RuPay Select, VISA Signature, and MasterCard Business), the limit has been reduced from ₹1,50,000 down to ₹75,000.

Bandhan Bank: Revised Free Transaction Limits

Bandhan Bank has completely rewritten its rulebook for how often you can use an ATM for free.

- Using a Bandhan Bank ATM: You are allowed 5 free financial transactions (withdrawing cash) per month. You get unlimited free “non-financial transactions” (like checking your balance or changing your PIN).

- Using Other Banks’ ATMs: If you live in a Metro city (Mumbai, Delhi, Bengaluru, Chennai, Hyderabad, Kolkata), you only get 3 free transactions a month (financial and non-financial combined). In non-metro cities, you get 5.

- The Penalty: Once you cross these limits, Bandhan Bank will hit you with a ₹23 fee for every cash withdrawal, and a ₹10 fee just for checking your balance! Even worse, if you try to withdraw money but your account is empty, they will charge you a ₹25 “decline fee.”

6. The End of an Era: RuPay Debit Card Lounge Access

For the last few years, the RuPay Platinum Debit Card was the ultimate travel cheat code for the Indian middle class. If you had this basic bank card in your wallet, you could walk into a luxury airport lounge, eat a massive buffet meal, drink unlimited coffee, and relax in a comfortable chair while waiting for your flight, all completely for free.

Because it was so easy to get, airport lounges across India became severely overcrowded. People were waiting in line for an hour just to get into the lounge!

What is changing?

The National Payments Corporation of India (NPCI), which manages the RuPay network, has officially pulled the plug.

What this means for you:

Starting April 1, 2026, RuPay Platinum debit cardholders will no longer have unconditional, complimentary access to domestic airport lounges, international airport lounges, or premium railway lounges.

You cannot just flash the card at the front desk anymore. Moving forward, lounge access will be strictly “spend-based.” This means the bank will look at your account history. If you spent a certain amount of money (like ₹10,000 or ₹50,000) using that debit card in the previous three months, only then will a free lounge visit be unlocked on your card. If you do not meet the spending target, you will have to pay the full entry fee at the airport.

7. RBI Mandates Double Security for Digital Payments

We live in a world where almost everything is paid for using our phones. Whether you are paying a massive electricity bill online or transferring money to a friend, digital payments are the backbone of the economy. Unfortunately, as digital payments have grown, so have the number of cybercriminals and scammers trying to steal your money.

What is changing?

The Reserve Bank of India (RBI) issued strict new guidelines mandatory from April 1, 2026.

What this means for you:

Every single digital payment transaction in India must now meet the norm of Two-Factor Authentication (2FA).

Authentication simply means proving to the bank that you are actually the person making the payment. It proves you’re not a hacker sitting in another country. The RBI now requires two separate proofs.

- Factor One: This is usually something only you know, like your secret UPI PIN, your banking password, or your fingerprint/Face ID.

- Factor Two: The RBI requires an additional, dynamic layer of security. For almost all banks, this will be an SMS-based One Time Password (OTP) sent directly to your registered mobile number.

If a hacker somehow steals your banking password, they still cannot steal your money because they do not have physical possession of your mobile phone to receive the final OTP. While this might add an extra ten seconds to your online shopping checkout process, it is a massive and necessary upgrade to keep your bank account safe from organized cybercrime.

Conclusion: Adapt and Protect Your Wallet

The rules of personal finance change every single year, and adapting to them is the only way to protect your money.

The April 1, 2026 changes are designed to modernize our economy, increase security, and close loopholes that were causing problems for banks and infrastructure. While it might be frustrating to lose free airport lounge access or deal with stricter ATM limits, these rules are the new reality.

Take a few minutes today to check your wallet. Update your Aadhaar details so you do not run into problems with your PAN card, check your bank’s website to memorize your new ATM limits, and plan your credit card spending so you can hit those 4,000-point reward blocks. By staying informed, you ensure that the new financial year brings you growth and stability, rather than surprise fees and penalties!

Frequently Asked Questions (FAQs)

Q1: Why did the government replace the old Income-tax Act of 1961?

The 1961 Act was 65 years old. Over the decades, the government had added thousands of confusing amendments, rules, and exceptions to it, making it incredibly difficult for regular citizens to understand. The new “Income-tax 2025” framework (effective April 1, 2026) is designed to be modern, streamlined, and easier to navigate for today’s digital economy.

Q2: Can I still get an instant e-PAN using just my Aadhaar OTP?

No. That facility ended on March 31, 2026. Starting April 1, you must fill out a specific form (like Form 93 for individuals) and provide additional supporting documents beyond just your Aadhaar card to apply for a PAN.

Q3: What happens if the name on my Aadhaar and PAN card do not match?

Under the new rules effective April 1, 2026, the income tax department requires an exact name match. If the spelling is different, or a middle name is missing on one card, your new PAN application or update request will be rejected. You must correct your Aadhaar details first.

Q4: I have 2,000 reward points on my SBI Cashback Card. Can I use them to pay my bill?

No, not immediately. Under the new rules, SBI Card only allows you to convert reward points into statement credit in blocks of 4,000. You will have to continue using your card until you earn another 2,000 points to hit that minimum 4,000-point threshold before you can redeem them.

Q5: Will my FASTag stop working if I don’t pay the new ₹3,075 fee?

No! The ₹3,075 fee is specifically for the “FASTag Annual Pass,” which is an optional, unlimited local travel pass used by frequent daily commuters. If you are a normal driver who just recharges your FASTag with a balance (like ₹500) for occasional road trips, this fee increase does not affect you at all. Your regular FASTag will work normally.

Q6: Does HDFC Bank charge ₹23 every time I use an ATM now?

No. HDFC Bank gives you a certain number of free ATM transactions every month (usually 3 to 5 depending on your account and city). The new rule simply means that using UPI to withdraw cash without a card now counts toward that free limit. You only pay the ₹23 fee after you have used up all your free visits for the month.

Q7: Why did PNB reduce the ATM cash withdrawal limit to ₹50,000?

Banks reduce daily cash limits to protect their customers from massive financial losses. If your debit card is stolen and the thief somehow gets your PIN, a lower daily limit prevents them from draining your entire bank account in a single day before you have the chance to call the bank and block the card.

Q8: Can I still get free food at the airport lounge with my RuPay card?

If you have a RuPay Platinum debit card, you no longer get automatic, unconditional free entry. Starting April 1, 2026, you will only be allowed into the lounge for free if you have met specific spending targets on that debit card in the previous months. Check with your specific bank to see what your spending target is.

Q9: What is Two-Factor Authentication (2FA) for digital payments?

Two-Factor Authentication is a double-lock system required by the RBI. When you make a digital payment, you cannot just use a password. You must provide a second proof of identity, which is almost always a One Time Password (OTP) sent via SMS to your registered mobile phone.

Q10: What happens if I try to use an ATM and my account has no money?

If you use a Bandhan Bank ATM (and several other banks have similar rules) and you try to withdraw cash, but the transaction fails because your account balance is too low, the bank will charge you a “decline fee” (currently ₹25 at Bandhan Bank). Always check your balance on your mobile app before requesting cash!

⚠️ Disclaimer:

At Paisaseekho, our mission is to make you financially literate. The information provided in this article is for educational and informational purposes only and should not be construed as professional tax, investment, or legal advice.