TL;DR: Gold Drafts vs. Gold Loans at a Glance

If you are at the bank right now and need a quick answer, here is the summary:

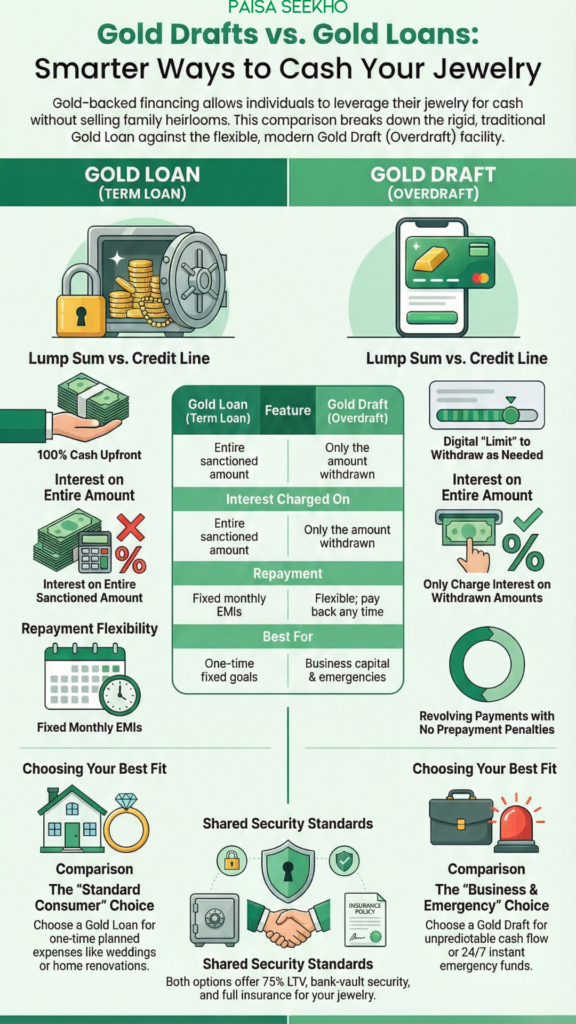

- The Gold Loan (Lump Sum): Best for planned, one-time expenses (like a wedding or a house renovation). You get all the money at once and start paying interest on the full amount from day one.

- The Gold Draft (Overdraft): Best for businesses or unpredictable emergencies. The bank gives you a “limit” on your mobile app. You only pay interest on the money you actually withdraw, not the whole limit.

- Interest Math: Gold loans usually have slightly lower interest rates, but Gold Drafts can be cheaper overall because you only pay for what you use.

- Repayment: Gold loans have fixed EMIs. Gold Drafts are like a “revolving door”—you can take money out and put it back in whenever you want, as long as you stay within your limit.

- The Security: In both cases, your gold is kept in a high-security bank vault, fully insured, and returned to you once the debt is cleared.

Introduction

In almost every Indian household, gold is more than just jewelry; it is a silent, golden insurance policy. Whether it is the heavy bangles passed down by a grandmother or the coins bought every Dhanteras, gold is our ultimate safety net. We buy it for beauty, but we keep it for “bad times.”

But when those “bad times” or even “big opportunities” arrive—like a medical emergency, a sudden business deal, or a child’s college admission—most families face a dilemma. Should you sell the gold? No, that feels like losing a piece of family history. This is where the world of gold-backed financing comes in.

For a long time, the only option was a simple Gold Loan. You give your gold to the bank, they give you a lump sum of cash, and you pay it back in EMIs. But recently, a newer, smarter sibling has entered the market: the Gold Draft (also known as a Gold Overdraft).

Choosing between these two can be the difference between saving thousands of rupees in interest or getting trapped in a rigid repayment schedule. In this comprehensive, deep-dive guide, we will break down the “Gold Draft vs. Gold Loan” debate. We will explain the math, the flexibility, and the hidden traps so you can decide which one is the perfect fit for your financial goals.

What exactly is a Gold Loan and how does it work for immediate cash?

The Gold Loan is the traditional method that most of us are familiar with. It is a “Term Loan.”

Imagine you need ₹5 Lakhs for your sister’s wedding. you take your gold to a bank or a company like Muthoot or Manappuram. They check the purity, weigh the gold, and tell you that based on the current market price, they can give you exactly ₹5 Lakhs.

Once you sign the papers, the bank transfers the full ₹5 Lakhs into your account. From that very second, the “interest clock” starts ticking on the entire ₹5 Lakhs. Even if you only spend ₹3 Lakhs on the wedding and keep the other ₹2 Lakhs in your cupboard, the bank will still charge you interest on the full ₹5 Lakhs.

The Structure of a Gold Loan:

- Disbursal: 100% of the loan amount is given to you upfront.

- Tenure: Usually short-term, ranging from 6 months to 3 years.

- Repayment: You usually pay monthly EMIs (Principal + Interest) or “Bullet Repayment” (where you pay the whole interest and principal at the very end).

- Purpose: Ideal for a specific, known expense where you know exactly how much money you need to spend today.

What is a Gold Draft (Overdraft) facility and why is it becoming popular?

The Gold Draft, or Gold Overdraft (OD), is a much more modern and flexible way of borrowing. Think of it like a “Credit Card” backed by your gold.

Instead of taking a lump sum of cash, you “pledge” your gold to the bank to open a credit line. Let’s use the same example: you give the bank gold worth a ₹5 Lakh limit. But instead of the bank giving you the cash, they simply “enable” a limit of ₹5 Lakhs on your bank account.

Your bank balance might show zero, but you have the power to withdraw up to ₹5 Lakhs whenever you want through your mobile app or a cheque book.

The Magic of Interest Calculation:

If you have a ₹5 Lakh Gold Draft limit, but you only withdraw ₹50,000 to pay a hospital bill, the bank will only charge you interest on that ₹50,000. The remaining ₹4.5 Lakhs of your limit is sitting there for free. If you pay back that ₹50,000 after ten days, the interest stops immediately.

The Structure of a Gold Draft:

- Disbursal: No money is given upfront. A “limit” is set. You withdraw what you need, when you need it.

- Tenure: Usually renewed every year.

- Repayment: There are no fixed EMIs. You are generally required to pay the interest every month, and you can pay back the principal whenever you have extra cash.

- Purpose: Perfect for small business owners who have frequent ups and downs in cash flow, or for people who want an “emergency fund” ready just in case.

Gold Loan vs Gold Draft: What are the key differences in interest calculation?

This is where the math gets very interesting. At first glance, a Gold Loan might look cheaper because the interest rate (the percentage) is often 0.5% to 1% lower than a Gold Draft. But don’t let that fool you.

Scenario A: The Gold Loan Math

You take a ₹1,00,000 Gold Loan at 10% interest for one year.

You will pay interest on ₹1,00,000 for 365 days.

Total Interest Cost: Roughly ₹10,000.

Scenario B: The Gold Draft Math

You open a ₹1,00,000 Gold Draft at a slightly higher 11% interest.

However, you only actually needed the money for two months to buy stock for your shop. After two months, you sold the stock and paid the money back.

You only pay 11% interest on ₹1,00,000 for 60 days.

Total Interest Cost: Roughly ₹1,800.

The Verdict on Interest:

Even though the “rate” was higher in the Gold Draft, the “out-of-pocket cost” was much lower because you weren’t paying for money you didn’t need. However, if you plan to take the full amount and keep it for the entire year without paying it back, the traditional Gold Loan will be cheaper because of its lower base rate.

Which option offers better repayment flexibility for small business owners?

If you run a business, you know that cash flow is never a straight line. Some months you have too much work and no cash to buy raw materials. Other months, you have plenty of cash but no work.

For a business owner, a Gold Loan is like a cage. You are forced to pay a fixed EMI every month. If you have a bad month in business, that EMI becomes a huge burden. If you have a great month and want to pay off the loan early, many banks will charge you a “Prepayment Penalty” (a fee for paying your own debt too fast!).

For a business owner, a Gold Draft is like a partner.

It gives you the freedom to manage your “Working Capital.”

- Monday: You see a great deal on raw materials. You withdraw ₹2 Lakhs from your Gold Draft.

- Friday: You deliver the finished goods and the client pays you. You deposit that ₹2 Lakhs back into the account.

- The Cost: You only paid interest for 5 days.

The Gold Draft allows you to “recycle” your capital. You can withdraw and deposit money 100 times a month if you want. There are no prepayment penalties because there is no fixed schedule. This flexibility is why almost every modern entrepreneur prefers a Gold Draft over a traditional loan.

How do the Loan-to-Value (LTV) ratios compare for gold-backed credit?

Whether you choose a loan or a draft, you need to understand LTV (Loan-to-Value). This is the percentage of your gold’s value that the bank is legally allowed to lend you.

The Reserve Bank of India (RBI) sets strict rules for this. Usually, the LTV is capped at 75%.

This means if you have gold worth ₹1,00,000, the bank can only give you a loan or a draft limit of ₹75,000. The other 25% acts as a “margin” or a cushion for the bank.

The Price Drop Risk:

What happens if the global price of gold suddenly crashes?

- In a Gold Loan: The bank might send you a “Margin Call” notice. They will ask you to either deposit some cash or give them more gold to bring the ratio back to 75%. If you don’t, they have the right to sell your jewelry.

- In a Gold Draft: The bank will simply “reduce” your limit. If your limit was ₹75,000 and gold prices drop, the app might show your new limit as ₹70,000. If you have already withdrawn ₹75,000, you will have to pay back the ₹5,000 difference immediately.

In general, the LTV rules are the same for both products, but because a Gold Draft is a live, digital account, the bank monitors the value of your gold much more closely every single day.

What are the processing fees and hidden costs in gold-based financing?

When you pledge your gold, the bank has to do work. They have to hire a “Gold Appraiser” to check the purity, they have to pay for insurance, and they have to maintain a high-security vault. You pay for these services through fees.

1. Processing Fees

- Gold Loan: Usually a flat fee (e.g., ₹500 to ₹2,000) or a small percentage (0.5%) of the loan amount. You pay this once when the loan starts.

- Gold Draft: Since this is a long-term credit line, you often pay an “Annual Maintenance Fee” or a “Renewal Fee.” It might be slightly higher than a one-time loan fee because the bank has to keep the facility open for you for years.

2. Valuation Charges

This is the fee paid to the person who rubs your gold on a touchstone to check its purity. This is usually a small, one-time fee of ₹200 to ₹500.

3. Documentation and Stamp Duty

Depending on which state in India you live in, you might have to pay a small “Stamp Duty” to create a legal charge on your gold.

4. Prepayment and Foreclosure Charges

This is the most important “hidden” cost.

If you have a 2-year Gold Loan and you try to close it in 6 months, the bank loses interest income. To compensate, they charge you 1% to 2% of the remaining balance. Gold Drafts almost never have these charges.

Is a Gold Draft better for emergency funds or planned expenses?

This is the golden question. The answer depends on your personality and your specific need.

Choose a Gold Loan IF:

- You have a fixed goal: You are buying a car, paying a specific college fee, or fixing your roof. You know the exact amount and you want a disciplined way to pay it back over 12 months.

- You are a “spender”: If you have a ₹5 Lakh limit on an app (Gold Draft), you might be tempted to withdraw money for a new iPhone or a vacation. A Gold Loan gives you the cash you need for your goal and then forces you into a strict repayment habit.

Choose a Gold Draft IF:

- You want an “Emergency Shield”: You don’t need money today, but you want to be ready. You can pledge your gold now, pay a small processing fee, and have a ₹10 Lakh limit ready on your phone. If a medical emergency hits at 2 AM on a Sunday, you can transfer money to the hospital instantly via UPI from your Gold Draft. You can’t do that with a Gold Loan.

- You are a Business Owner: As we discussed, the ability to take money for 3 days and pay it back is a financial superpower that only the Gold Draft provides.

How does the RBI’s stance on gold valuations affect your borrowing limit?

The Reserve Bank of India (RBI) is very protective of the Indian banking system. They know that Indians have an emotional connection to gold.

In early 2026, the RBI issued new guidelines regarding how banks value gold. Previously, some local lenders were “overvaluing” jewelry to give people more money. They would include the weight of the stones (diamonds, rubies) in the gold weight.

The New Rule:

Banks are now strictly ordered to only value the “Net Weight” of 18K, 22K, or 24K gold. If your necklace weighs 50 grams but has 10 grams of heavy decorative stones, the bank will only give you a loan based on 40 grams of gold. This applies to both Gold Loans and Gold Drafts. This rule ensures that if the bank has to sell the gold to recover a debt, they don’t lose money because of “stone weight.”

Furthermore, the RBI now requires banks to use the average price of gold from the last 30 days to calculate your loan amount, rather than just today’s price. This protects you from a sudden one-day dip in gold prices that could reduce your loan amount unfairly.

What happens to your jewelry if you default on a Gold Loan or Draft?

This is the part no one likes to talk about, but it is the most important. What happens if you cannot pay the money back?

In both a Gold Loan and a Gold Draft, your jewelry is the “Collateral.”

If you stop paying your interest or your EMIs for 3 to 6 months, the bank will follow a very strict legal process:

- Reminders: You will get multiple SMS, emails, and phone calls.

- Final Notice: The bank will send a registered legal notice giving you 15 to 30 days to clear the dues.

- The Auction: If you still don’t pay, the bank will publish a notice in a local newspaper and hold a public auction to sell your jewelry to the highest bidder.

- The Settlement: The bank will take the money you owed them (Principal + Interest + Auction Costs). If there is any “extra” money left over from the sale, they are legally required to return that extra cash to you.

However, you will lose the jewelry forever. Because gold often has sentimental value (like a wedding Mangalsutra), a default is a heavy emotional loss. This is why a Gold Draft is often safer—it allows you to pay back even small amounts of ₹1,000 whenever you have them, making it much harder to slip into a total default.

Verdict: Gold Draft or Gold Loan – which is the right choice for your financial goal?

After comparing every detail, the winner depends entirely on your cash flow.

The Gold Loan is the winner for the “Standard Consumer.”

If you are a salaried employee with a one-time big expense and a steady monthly paycheck, the Gold Loan is perfect. It is simple, the interest rate is the lowest, and the fixed EMI ensures you will get your gold back in exactly 12 or 24 months.

The Gold Draft is the winner for the “Smart Saver & Entrepreneur.”

If you want the ultimate flexibility, if you want an emergency fund that costs nothing unless you use it, or if you are running a business, the Gold Draft is vastly superior. The ability to pay interest only on what you use and the freedom from fixed EMIs makes it the most powerful borrowing tool in the Indian market today.

Gold is your family’s hard-earned wealth. Whether you choose a loan or a draft, ensure you read the fine print regarding “Late Payment Penalties” and “Processing Fees.” Use your gold as a bridge to reach your dreams, but always have a clear plan to bring that gold back home to your family vault.

Frequently Asked Questions (FAQs): Gold Loans vs. Gold Drafts

Q1: Which one has a lower interest rate, a Gold Loan or a Gold Draft?

Typically, a traditional Gold Loan has a slightly lower interest rate (often 0.5% to 1% lower) than a Gold Draft. This is because the bank gets the interest on the full amount upfront. However, a Gold Draft can be cheaper in total rupees because you only pay interest on the money you actually use.

Q2: Can I get my gold back partially in a Gold Draft?

Yes! This is a great feature of many Gold Drafts. If you pledged 10 gold coins for a ₹5 Lakh limit, and you decide you only need a ₹2 Lakh limit now, you can pay back a portion of your debt and ask the bank to return some of your gold coins while keeping the account open with the remaining coins.

Q3: Is my jewelry safe in the bank vault?

Yes. All RBI-regulated banks and NBFCs are required to store pledged gold in high-security, fireproof, and burglar-proof vaults. Furthermore, the bank is legally required to insure your gold for its full market value. If a bank robbery happens, the insurance company will pay for the gold.

Q4: Do I need a good CIBIL score to get a Gold Loan or a Gold Draft?

One of the best things about gold-backed credit is that banks are very relaxed about CIBIL scores. Since the bank is holding your physical gold, they are not worried about your credit history. Even if you have a low CIBIL score, you can easily get a Gold Loan or Draft, as long as your gold is real.

Q5: Can I use my gold for a Gold Draft if it is only 18-Karat?

Yes. Most banks accept gold jewelry ranging from 18-Karat to 24-Karat. However, they will not accept jewelry below 18-Karat. The loan amount you get will be lower for 18K gold compared to 22K gold because the actual gold content is lower.

Q6: What is a “Bullet Repayment” in a Gold Loan?

A Bullet Repayment is a special type of gold loan where you don’t pay any monthly EMIs. You take the money, use it for 6 or 12 months, and then pay the entire principal and the entire accumulated interest in one single “bullet” payment at the end of the year to get your gold back.

Q7: Is there a minimum amount I can withdraw from a Gold Draft?

Most banks allow you to withdraw as little as ₹1,000 or ₹5,000 from your Gold Draft limit. This makes it perfect for small, daily needs, unlike a Gold Loan which usually requires a minimum borrowing of ₹20,000 or more.

Q8: Can I pay my Gold Draft interest using UPI?

Absolutely. Most modern banks (like SBI, ICICI, or HDFC) and gold-loan companies have mobile apps. You can see your monthly interest due and pay it instantly using Google Pay, PhonePe, or any UPI app.

Q9: Will the bank accept gold coins and bars for a Gold Draft?

Banks in India are allowed to accept gold coins (up to 50 grams per customer) for loans. However, many banks are restricted from taking pure gold bars as collateral for individual loans. Jewelry is almost always accepted without any issues.

Q10: Can I renew my Gold Draft every year?

Yes. Gold Drafts are usually “revolving” facilities. At the end of 12 months, the bank will re-value your gold based on the current market price. If gold prices have gone up, they might even increase your limit! You simply pay a small renewal fee, and your credit line continues for another year.