TL;DR: Key Takeaways on India’s Health Insurance Coverage Gap

If you are short on time and need the hard facts right now, here is what the latest financial data reveals:

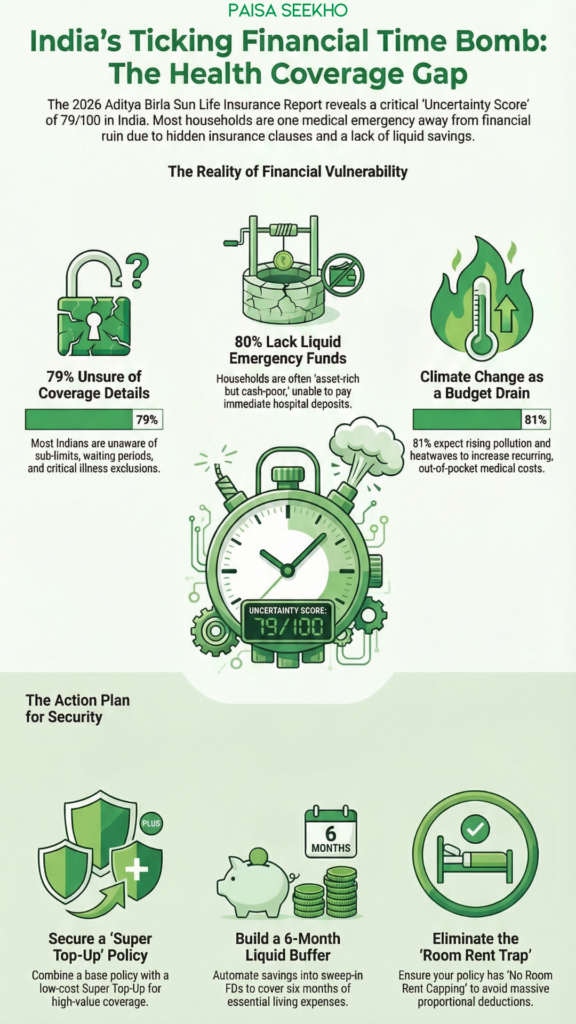

- The Ignorance Trap: 79% of Indians do not know the fine print of their health insurance. They are unaware of sub-limits, waiting periods, and critical illness exclusions.

- Living on the Edge: 80% of Indians lack a liquid emergency fund. Most households are one medical bill away from falling into severe debt.

- The Cost Anxiety: 82% of citizens are actively worried that the skyrocketing cost of private healthcare will permanently derail their financial stability.

- Climate as an Economic Threat: 81% expect pollution and climate-linked illnesses (like extreme heat stroke and vector-borne diseases) to worsen, translating into recurring, out-of-pocket medical expenses.

- The Mental Health Crisis: 81% report a rise in mental health issues, but 80% hesitate to seek help, leading to severe productivity loss and income disruption.

- The Solution: You must decouple your insurance from your employer, buy an independent Super Top-Up policy, and aggressively automate a 6-month liquid cash emergency fund.

Introduction

Imagine this scenario: It is 2:00 AM, and a medical emergency strikes your family. You rush to the nearest private hospital. As you stand at the admission desk, terrified and stressed, the receptionist asks for a massive upfront deposit. You hand over your corporate health insurance card, feeling a brief moment of relief, until the billing department informs you that your policy does not cover this specific illness, or that your room-rent limit has been breached, leaving you to pay lakhs of rupees out of your own pocket.

You quickly check your bank account, only to realize your savings are tied up in fixed deposits that carry a penalty to break, or mutual funds that will take three days to hit your account.

If this nightmare scenario sends a shiver down your spine, you are not alone. In fact, this is the fragile financial reality for the vast majority of the country.

According to a highly revealing report published in April 2026 by Aditya Birla Sun Life Insurance, India is currently sitting on a massive, ticking financial time bomb. The data shows that a staggering 79% of Indians are completely unsure if their health insurance actually covers serious illnesses, and exactly 80% of households are operating without a sufficient emergency fund.

We work incredibly hard to earn our salaries, but we are leaving our back doors completely wide open to financial ruin. In this comprehensive, deep-dive guide, we are going to break down the shocking findings of this 2026 report. We will explore why we are so unprepared, how climate change is secretly destroying our budgets, and give you a clear, step-by-step action plan to bulletproof your health cover and emergency savings today.

What Does the 2026 Aditya Birla Sun Life Insurance Report Reveal About Our Finances?

To fix a problem, we first have to admit that the problem exists. The April 2026 report by Aditya Birla Sun Life Insurance serves as a harsh reality check for the Indian middle class.

The researchers calculated an “Overall Uncertainty Score” for India, which currently stands at an uncomfortably high 79 out of 100. This means the average Indian is living with chronic financial anxiety.

While we often worry about job security or stock market crashes, the report highlights that our biggest vulnerabilities are actually biological and environmental. Despite aggressive government campaigns and the trauma of the recent pandemic years, preparedness remains dangerously low.

The report noted a fascinating geographic shift. This lack of financial resilience is no longer just a problem for the urban poor; it is a massive, glaring issue across Tier 2 and Tier 3 markets. As the cost of living and private medical care spreads into smaller cities, families who previously relied on cheap local clinics are suddenly facing metro-city hospital bills without metro-city salaries to back them up.

Why Are 79% of Indians Unsure About Their Health Insurance Coverage?

It is a bizarre paradox: India is seeing record numbers of health insurance policies being sold, yet 79% of people holding these policies have no idea what they actually bought. How did we get here?

1. The “Corporate Cover” Illusion

The number one reason for this ignorance is over-reliance on employers. Millions of salaried professionals assume they are perfectly safe because their company provides a ₹3 Lakh or ₹5 Lakh group health insurance plan.

Because they did not buy the policy themselves, they never read the document. They do not realize that corporate policies often have strict co-pay clauses (where you have to pay 10% or 20% of the bill), or that the moment they quit their job or get laid off, that insurance vanishes into thin air, leaving their family completely exposed.

2. The Danger of Jargon and Sub-Limits

Health insurance documents are notoriously written in complex legal jargon. People buy a “₹10 Lakh policy” and assume they can claim up to ₹10 Lakhs for anything. This is a fatal mistake.

Insurance policies are riddled with “Sub-Limits.”

- The Room Rent Trap: Your policy might have a 1% room rent limit. For a ₹5 Lakh policy, the insurance company will only pay ₹5,000 per day for your hospital room. If you choose a private room that costs ₹8,000 a day, you don’t just pay the ₹3,000 difference. Hospitals link all their surgical and doctor fees to the room category. Because you upgraded your room, the insurance company will proportionally deduct money from your entire surgery bill, leaving you to pay lakhs out of pocket!

3. Ignoring Waiting Periods

If you buy a policy today and suffer a heart attack next week, you are likely covered. But if you try to claim money for a cataract surgery or knee replacement, your claim will be rejected. Most standard policies have a strict 2-year to 4-year “Waiting Period” for pre-existing diseases and specific slow-growing ailments. Because 79% of people do not know these exclusions exist, they face brutal financial shocks at the hospital billing desk.

Why Do 80% of Indian Households Lack a Proper Emergency Fund?

If the insurance fails, your savings are supposed to catch you. But the report highlights that 80% of Indians are operating without a financial safety net.

Confusing “Investments” with “Emergencies”

Many Indians proudly point to their real estate plots, their locked-in Provident Fund (EPF), or their long-term equity mutual funds and say, “I have savings!” But an emergency fund is not about wealth; it is about liquidity.

If you need ₹2 Lakhs in cash at 3:00 AM on a Sunday to pay a hospital admission deposit, you cannot sell a piece of land in three hours. You cannot redeem a mutual fund on a weekend. Because Indians heavily prefer locking their money into physical assets or illiquid government schemes, they are effectively “asset-rich but cash-poor.”

The Vicious Cycle of Lifestyle Inflation

The Indian middle class is experiencing massive lifestyle inflation. Thanks to easy EMIs and “Buy Now, Pay Later” (BNPL) schemes, young professionals are dedicating a huge chunk of their monthly salary to paying off iPhones, cars, and vacations. When your entire paycheck is immediately swallowed by EMIs and rent, there is absolutely nothing left at the end of the month to sweep into a boring emergency savings account. They are living paycheck-to-paycheck on high salaries.

How Are Climate Change and Pollution Increasing Our Healthcare Costs?

One of the most unique and alarming insights from the 2026 Aditya Birla Sun Life Insurance report is the intersection of climate and finance.

For the first time, environmental and climate risks have emerged as the second-largest driver of financial anxiety in India. A massive 81% of respondents expect pollution levels to worsen, and they recognize that this is no longer just an environmental issue, it is an economic threat.

The Geographic Reality of Climate Illness

The report highlights that climate-linked illnesses are draining household budgets across specific geographies:

- Western Metros (Mumbai, Ahmedabad, Pune): Severe, prolonged heatwaves and toxic air pollution are leading to chronic respiratory illnesses, asthma in children, and heat-induced hospitalizations. This leads to continuous, recurring Out-Patient Department (OPD) expenses for inhalers, doctor visits, and medications, which are almost never covered by standard health insurance.

- Southern Regions (Chennai, Bengaluru, Kerala): Erratic monsoon patterns and sudden temperature spikes are causing massive outbreaks of vector-borne diseases like Dengue, Chikungunya, and Malaria. These diseases require sudden, emergency hospitalizations, placing immediate stress on families without liquid cash reserves.

As climate change accelerates, “seasonal illnesses” are becoming year-round chronic conditions. The 82% of Indians worried about rising healthcare costs are absolutely right to be terrified; you cannot escape the air you breathe.

What is the Hidden Financial Drain of the Mental Health Crisis in India?

While physical ailments are obvious, a silent epidemic is rapidly destroying the financial stability of the Indian workforce.

The 2026 report reveals a heartbreaking statistic: 81% of Indians report a significant rise in mental health issues (such as severe anxiety, clinical depression, and burnout). Yet, despite this massive surge, nearly 80% of individuals hesitate to seek professional support.

The Stigma Costs Money

Why is this a financial issue? Because untreated mental health conditions directly lead to productivity loss.

When an employee suffers from severe burnout or depression and refuses to seek therapy due to societal stigma, their performance drops. They take more unpaid sick leaves, miss out on promotions, or in severe cases, are forced to resign from their jobs entirely. This causes a sudden, violent disruption in their primary source of income.

The Insurance Gap for Therapy

Even if that 80% decided to seek help tomorrow, they would hit a financial wall. Psychiatric therapy and counseling in India are expensive. More importantly, while the government has legally mandated that health insurance must cover mental illness, this coverage usually only applies to in-patient hospitalization (being admitted to a psychiatric ward).

Regular, weekly therapy sessions with a psychologist fall under OPD (Out-Patient Department) expenses, which 95% of standard Indian health insurance policies simply do not cover. This forces families to pay for critical mental health support entirely out of their own pockets, rapidly draining whatever small savings they might have.

How Can You Fix Your Health Insurance Gap Today?

If you are part of the 79% who are unsure about their coverage, today is the day you take control. You cannot wait for an emergency to test your policy. Follow this strict action plan:

1. Delink from Your Employer

Your corporate health insurance is a fantastic bonus, but it is not a safety net. You must buy an independent, standalone comprehensive retail health insurance policy for your family. If you get laid off or decide to start your own business, this independent policy stays with you, ensuring your family is never left unprotected.

2. Buy a “Super Top-Up” (The Ultimate Hack)

A ₹20 Lakh base health insurance policy is very expensive and might stretch your monthly budget. The smartest financial hack is the “Super Top-Up.”

- Buy a standard base policy of ₹5 Lakhs.

- Then, buy a Super Top-Up policy of ₹15 Lakhs with a “deductible” of ₹5 Lakhs.

Because the Super Top-Up only triggers after your hospital bill crosses ₹5 Lakhs, the premium for this massive coverage is incredibly cheap (often just a few thousand rupees a year). This combination gives you ₹20 Lakhs of total coverage at a fraction of the cost!

3. Read the Dreaded Fine Print

Sit down this weekend with a cup of coffee and your policy document. Look for three specific things:

- Room Rent Capping: Ensure your policy says “No Room Rent Capping” or “Single Private AC Room.”

- Co-Payment: Ensure your co-pay is 0%. You want the insurance company to pay 100% of the approved bill.

- Disease Wise Sub-Limits: Check if your policy has secret limits for common surgeries like cataracts or knee replacements, and upgrade to a better policy if the limits are too low.

How Do You Build a Bulletproof Emergency Fund Fast?

If you are part of the 80% living without a cash buffer, you are walking on a financial tightrope. Building an emergency fund is not about getting rich; it is about buying peace of mind.

The 6-Month Rule

Calculate your absolute bare-minimum monthly survival number. This includes your rent, your EMIs, your groceries, your children’s school fees, and your utility bills. Do not include dining out or movie tickets.

Multiply that survival number by 6. That is your target emergency fund. If you lose your job tomorrow, this fund ensures your family survives for half a year without borrowing a single rupee.

Where Should You Park This Money?

Do not keep this money in your regular salary account; you will accidentally spend it on a Swiggy or Amazon order. You must separate it, but keep it highly liquid.

- Sweep-in Fixed Deposits: This is the best option. The money earns FD interest (around 6.5% to 7%), but if you swipe your debit card at a hospital, the FD automatically breaks instantly to fund the transaction without any paperwork.

- Liquid Mutual Funds: These are low-risk debt funds that give slightly better returns than a savings account. You can withdraw the money and have it hit your bank account within 24 working hours.

Automate the Savings

You will never build an emergency fund if you wait until the end of the month to save “whatever is left.” Treat your emergency fund like an EMI. Set up an automated bank transfer on the 1st of every month. The moment your salary hits your account, 10% or 20% should instantly vanish into your emergency liquid fund before you even have a chance to see it.

Conclusion

The 2026 Aditya Birla Sun Life Insurance report is a massive wake-up call for the Indian middle class. The data is clear: hoping for the best is no longer a viable financial strategy.

We live in a world where climate change is creating new, unpredictable diseases, healthcare inflation is rising at nearly 14% every year, and the mental health crisis is threatening our ability to earn a living. Relying on a basic corporate health policy and zero cash reserves is a guaranteed recipe for financial disaster.

The good news is that you have the power to fix this immediately. By educating yourself on the fine print of your insurance, upgrading your family’s coverage, and ruthlessly automating your emergency savings, you can step out of that 80% statistic. Protect your wealth, protect your health, and ensure that when life inevitably throws a curveball, your family’s financial foundation remains absolutely unbreakable.

Frequently Asked Questions (FAQs)

1: Why do 79% of Indians face a health insurance coverage gap?

A massive 79% of Indians are unsure of their coverage because they rely entirely on employer-provided corporate insurance, which they never read. They are unaware of critical limitations like co-payments, room-rent sub-limits, and waiting periods for pre-existing diseases, leaving them exposed to massive out-of-pocket bills during emergencies.

2: What happens if I rely solely on my corporate health insurance?

If you rely only on corporate cover, you are financially vulnerable. Corporate policies often have low limits (₹3 Lakhs to ₹5 Lakhs) which are insufficient for major surgeries. More importantly, if you are laid off, resign, or retire, that insurance coverage instantly terminates, leaving your family completely unprotected until you secure a new job.

3: How does a room rent sub-limit destroy your health insurance claim?

If your policy has a 1% room rent sub-limit, it will only pay ₹5,000 per day on a ₹5 Lakh policy. If you choose a room costing ₹10,000, you don’t just pay the extra ₹5,000. Hospitals link doctor fees and surgery costs to the room category. The insurance company will proportionally deduct coverage for the entire surgery, potentially costing you lakhs of rupees in deductions.

4: Why do 80% of Indians lack a liquid emergency fund?

Many Indians confuse “investments” with “emergency funds.” They lock all their savings into real estate, PPF, or equity mutual funds, which cannot be converted to cash instantly at 2:00 AM during a medical crisis. Combined with rising lifestyle inflation and heavy EMI burdens, 80% of households fail to keep easily accessible liquid cash.

5: What is the exact size an emergency fund should be in 2026?

Financial experts strictly recommend that your liquid emergency fund should cover exactly 6 months of your mandatory living expenses. This includes rent, active EMIs, groceries, insurance premiums, and school fees, ensuring your family can survive a sudden job loss or medical crisis without taking on predatory debt.

6: How is climate change impacting Indian healthcare costs?

The Aditya Birla report noted that 81% of Indians expect pollution to worsen. Extreme heat and toxic air in western metros are causing chronic respiratory issues, while erratic monsoons in the south are triggering vector-borne diseases. These climate-linked illnesses result in continuous, recurring OPD and hospitalization costs that drain household budgets.

7: Does Indian health insurance cover mental health issues like depression?

While the government mandates that health insurance must cover mental illness, the coverage usually only applies to “in-patient hospitalization” (being admitted to a psychiatric facility). The vast majority of standard Indian policies do not cover regular OPD expenses like weekly therapy or counseling sessions, forcing patients to pay out-of-pocket.

8: What is a Super Top-Up health insurance policy and why do I need one?

A Super Top-Up is an incredibly cheap, supplementary insurance policy that acts as a massive safety net. It only activates after your hospital bill crosses a specific “deductible” amount (e.g., ₹5 Lakhs). By combining a standard ₹5 Lakh base policy with a ₹15 Lakh Super Top-Up, you secure ₹20 Lakhs of total coverage at a fraction of the premium cost.

9: Where is the safest place to park my emergency funds?

Your emergency fund must be highly liquid and safe from stock market crashes. The best places to park this money are Sweep-in Fixed Deposits (which automatically break to fund your debit card transactions without penalty) or Liquid Debt Mutual Funds (which offer slightly better interest than a savings account and can be withdrawn within 24 hours).

10: How can I force myself to build an emergency fund if I live paycheck to paycheck?

The only proven way to build a fund is through aggressive automation. Set up a standing instruction or an automated SIP with your bank for the 1st of every month. The moment your salary hits your account, 10% to 20% should automatically transfer into your separate emergency fund before you even have a chance to spend it on lifestyle expenses.