TL;DR: Key Takeaways on the War’s Impact on Your Wallet

If you are in a rush and just want to know how the West Asia crisis affects you, here is the quick summary:

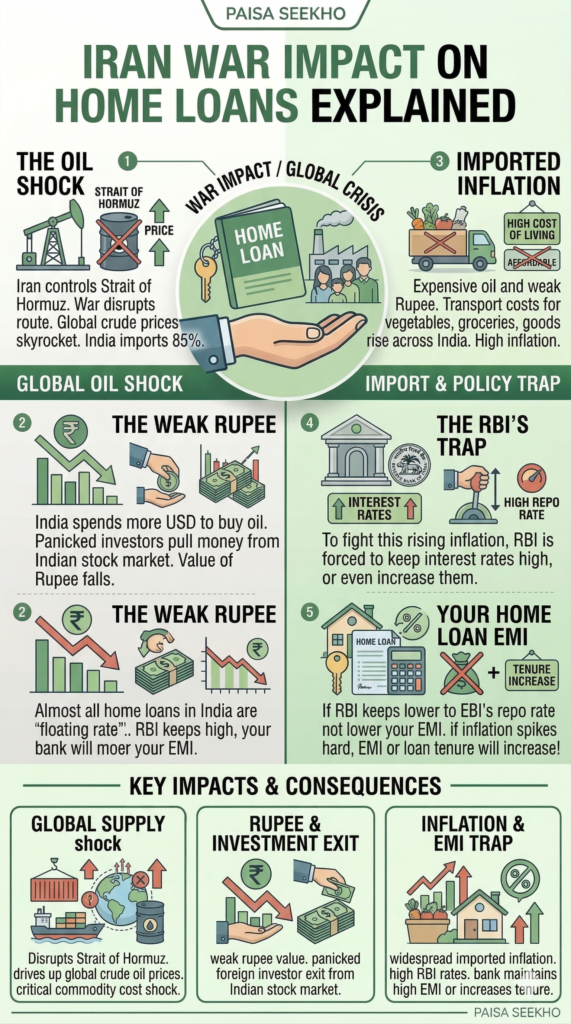

- The Oil Shock: Iran controls the Strait of Hormuz, a massive global oil shipping route. The war disrupts this route, causing global crude oil prices to skyrocket. India imports 85% of its oil, making this a massive problem.

- The Weak Rupee: Because oil is expensive, India has to spend more US Dollars to buy it. At the same time, panicked foreign investors are pulling their money out of the Indian stock market. This double-hit causes the value of the Rupee to fall.

- Imported Inflation: Expensive oil and a weak Rupee mean that the cost of transporting vegetables, groceries, and manufactured goods across India goes up. This causes high inflation (the rising cost of living).

- The RBI’s Trap: To fight this rising inflation, the Reserve Bank of India (RBI) is forced to keep interest rates high, or even increase them.

- Your Home Loan EMI: Almost all home loans in India are “floating rate” loans linked to the RBI’s repo rate. If the RBI keeps rates high to fight war-induced inflation, your bank will not lower your EMI. In fact, if inflation spikes hard, your EMI or loan tenure will increase!

Introduction

It is April 2026, and if you have turned on a news channel or opened a financial app recently, the headlines are painting a very stressful picture. The Indian stock market is seeing massive sell-offs, bathing investors’ portfolios in red. The Indian Rupee is dropping in value against the US Dollar. And the root cause of all this panic? A severe escalation of a geopolitical war in West Asia, specifically involving Iran.

For the average Indian citizen, a war thousands of miles away might seem like a tragedy, but not necessarily a personal financial crisis. You might be thinking: “I live in Pune, I work in IT, and I am just trying to pay off my 2BHK flat. Why should I care if there is a conflict in the Middle East?”

Here is the harsh reality of the modern global economy: everything is connected. A missile fired in West Asia creates a massive economic shockwave that travels across the ocean and directly hits your monthly household budget.

If you are paying an EMI for a home loan, an auto loan, or a personal loan, this global conflict is about to become your personal problem. In this comprehensive, easy-to-understand guide, we are going to strip away the complex financial jargon. We will explain exactly how a war causes oil prices to spike, why that makes the Rupee weak, and the exact mathematical chain reaction that could force your bank to increase your monthly Home Loan EMI.

1. The Butterfly Effect: How the Global Financial Market is Connected

There is a famous concept called the “Butterfly Effect,” which suggests that a butterfly flapping its wings in Brazil can cause a tornado in Texas. The global financial system works exactly the same way.

We no longer live in isolated bubbles. The phone in your pocket was designed in America, manufactured in China, powered by a battery made with minerals from Africa, and shipped to India using ships fueled by oil from the Middle East.

When a war breaks out in a highly sensitive region like West Asia, it disrupts this delicate web. The immediate reaction of the global stock markets is pure fear. Investors hate uncertainty. When they are scared, they pull their money out of risky investments (like Indian company stocks) and hide it in safe assets (like physical gold or US government bonds).

This is why your mutual fund portfolio is currently showing negative returns. But a dropping stock market is only the first domino to fall. The real danger to your wallet comes from the second domino: Crude Oil.

2. The Root Cause: Crude Oil and the Strait of Hormuz

To understand why the Iran conflict is so economically terrifying, you have to look at a map of the Middle East.

Right next to Iran is a narrow strip of water called the Strait of Hormuz. It is essentially the most important traffic choke-point on the planet. Roughly 20% to 25% of the entire world’s daily oil consumption passes through this tiny, narrow waterway on massive cargo ships.

When war erupts involving Iran, the global market instantly panics that this strait might be blocked, attacked, or shut down. If the ships cannot get through, the global supply of oil drops drastically. And as basic economics teaches us, when the supply of something drops but the world still needs it, the price skyrockets.

Why is this a nightmare for India?

India is a massive, growing economy, but we lack one crucial resource: we do not have our own oil. India imports roughly 85% of all the crude oil it consumes. We buy it from foreign countries, and we have to pay for it in US Dollars.

When the global price of a barrel of crude oil jumps from $75 to $95 or $100 because of the war, India’s national import bill explodes. The government and oil marketing companies suddenly have to spend billions of extra dollars just to keep the petrol pumps running in Delhi, Mumbai, and Bangalore.

3. The Impact of Rupee Falling

The next headline you probably saw is that the “Indian Rupee has hit a new low against the US Dollar.” Let’s break down exactly why this happens during a war, and why it makes the situation so much worse.

The value of the Rupee against the Dollar is basically a game of supply and demand.

- Factor 1: The Oil Bill: Because oil has become so expensive due to the war, Indian oil companies have to buy massive amounts of US Dollars to pay the Middle Eastern suppliers. Because they are aggressively buying Dollars and selling Rupees, the demand for the Dollar goes up, making it stronger, and the Rupee becomes weaker.

- Factor 2: Foreign Investors Fleeing: Foreign Institutional Investors (FIIs) have billions of dollars invested in the Indian stock market. When a war starts, they panic. They sell their Indian stocks (which crashes the market), convert their Rupees back into US Dollars, and take their money back to America where it feels safer. This massive selling of the Rupee drives its value down even further.

The Vicious Cycle

A weak Rupee is a terrible thing for a country that imports heavily. If the Rupee falls from ₹83 per dollar to ₹85 per dollar, it means that even if the global price of a laptop, a mobile phone part, or a barrel of oil stays exactly the same, it now costs an Indian importer significantly more Rupees to buy it.

We are getting hit twice: The price of oil went up because of the war, AND our currency became weaker, making that expensive oil cost even more!

4. Why Your Groceries Will Cost More

So, oil is incredibly expensive, and the Rupee is weak. How does this reach your kitchen? The answer is Imported Inflation.

Inflation is the rate at which the general cost of goods and services goes up. Think about how goods move in India. When a farmer grows tomatoes in Maharashtra, those tomatoes do not magically teleport to a supermarket in Delhi. They have to be loaded onto a heavy diesel truck.

If the price of crude oil skyrockets globally, the price of diesel at your local Indian petrol pump eventually goes up. When diesel goes up, the truck driver charges more money to transport the tomatoes. The supermarket has to pay the truck driver more, so they increase the price of the tomatoes on the shelf.

This happens to everything. The cost of manufacturing cement, running factory generators, flying airplanes, and delivering Amazon packages all rely heavily on fuel. When fuel gets expensive, the price of literally every single product in the country goes up. The cost of living rises rapidly, burning a hole in your monthly household budget.

5. The RBI Repo Rate Connection

This is where your Home Loan finally enters the picture.

The Reserve Bank of India (RBI) is the supreme boss of the Indian banking system. One of the RBI’s most important legal duties is to fight inflation. They have been given a strict target by the government: they must keep inflation around 4%.

If the Iran war causes oil prices to spike, and inflation in India suddenly shoots up to 6% or 7%, the RBI hits the panic button. They have to slow down the economy to stop prices from rising. Their primary weapon to fight inflation is something called the Repo Rate.

What is the Repo Rate?

The Repo Rate is the interest rate at which the RBI lends money to normal banks (like SBI, HDFC, or ICICI).

- If inflation is high, the RBI increases the Repo Rate.

- This makes it more expensive for your bank to borrow money from the RBI.

- Because borrowing is now expensive for the bank, the bank immediately passes that extra cost down to you. They increase the interest rates on personal loans, auto loans, and home loans.

- When loans become expensive, people stop borrowing money to buy new cars or houses. This slows down demand in the economy, which eventually forces prices to drop, bringing inflation back under control.

Before the West Asia conflict escalated, the Indian economy was actually doing quite well. Inflation was dropping, and financial experts were predicting that the RBI was finally going to cut the Repo Rate in 2026, which would have made everyone’s home loan EMIs cheaper.

The war has completely destroyed that hope. Because the war threatens to bring massive inflation back to India, the RBI is now forced to keep interest rates high, or worse, they might have to increase them again!

6. How Your Home Loan Takes the Hit

If you have a home loan in India, it is almost certainly a “Floating Rate” loan.

A floating rate loan means that your interest rate is not locked in forever. It is legally tied to an external benchmark, which is almost always the RBI’s Repo Rate.

The Direct Mathematical Hit

Let’s say the RBI is forced to hike the Repo Rate by 0.50% to fight the war-induced inflation. Your bank will send you an SMS the very next week stating that your Home Loan interest rate has also increased from, for example, 8.5% to 9.0%.

When your interest rate goes up, the bank usually does not increase your monthly EMI amount because they know people have fixed monthly salaries. Instead, they quietly increase the Tenure (the length) of your loan.

The Shocking Math: Imagine you took a ₹50 Lakh home loan for 20 years at an 8.5% interest rate. Your monthly EMI is roughly ₹43,391. If the war causes rates to jump to 9.0%, and you keep paying that exact same EMI amount, your loan tenure will instantly jump from 20 years to nearly 23 years! Because of a conflict thousands of miles away, you are suddenly trapped paying an extra three years of massive interest payments to the bank. Over the lifetime of the loan, that 0.50% hike could cost you an additional ₹8 Lakhs to ₹10 Lakhs in pure interest!

7. Action Plan: How to Protect Your Home Loan and Wallet

You cannot stop a geopolitical war, and you cannot control the global price of crude oil. However, you can absolutely control how you manage your own debt. Here are the smartest things you can do right now to protect your finances from this global shockwave:

1. Do Not Panic and Lock into a Fixed Rate Blindly

When people hear that interest rates are going up, they panic and ask their bank to convert their floating-rate loan into a “Fixed Rate” loan. This is usually a bad idea. Banks are smart. If they offer you a fixed rate during a crisis, they will charge you a massive premium (often 1.5% to 2% higher than the current floating rate). You will end up locking yourself into an incredibly expensive loan just for “peace of mind.” Stick to the floating rate; wars eventually end, and rates will eventually come back down.

2. Voluntarily Increase Your Monthly EMI

If your bank increases your interest rate, they will try to increase your loan tenure to keep your EMI the same. Do not let them do this! Call your bank and tell them, “Do not increase my tenure. I want you to increase my monthly EMI amount instead.” Paying an extra ₹1,500 or ₹2,000 a month hurts your monthly budget slightly, but it keeps your timeline perfectly intact and saves you lakhs of rupees in compound interest over the next 20 years.

3. Start Making Prepayments

This is the ultimate weapon against rising interest rates. If the stock market is crashing and giving you negative returns, redirect some of your extra savings toward your home loan. If you can manage to pay just one extra EMI every year (perhaps using your annual Diwali bonus or tax refund) and apply it directly to your principal loan amount, you can knock off nearly 4 to 5 years from your total loan tenure, completely destroying the negative impact of the RBI rate hikes!

4. Review Your Discretionary Spending

Because imported inflation is about to make groceries, fuel, and daily items more expensive, you need to tighten your belt. Review your monthly budget. Cut down on unnecessary subscriptions, delay buying that new luxury car, and ensure your emergency cash fund has at least 6 months of living expenses saved up in a safe, liquid bank account.

Conclusion

When the stock market flashes red and news channels broadcast images of conflict in West Asia, it is easy to feel overwhelmed. The realization that an international conflict directly dictates the price of your tomatoes and the length of your home loan is a sobering reminder of how globally integrated our lives have become.

However, the Indian economy has survived oil shocks, wars, and pandemics before, and it will survive this one too. The key to surviving this crisis as an individual is to not bury your head in the sand.

Understand that inflation might be high for the next few quarters, and your home loan interest rate is not going to drop anytime soon. By aggressively using prepayments to attack your principal loan amount, opting for higher EMIs instead of longer tenures, and being disciplined with your household budget, you can build a financial fortress that protects your family from the chaos of the outside world.

Frequently Asked Questions (FAQs): War, Inflation, and Home Loans

Q1: Why does a war in Iran affect the Indian stock market?

Foreign Institutional Investors (FIIs) hate risk and uncertainty. When a major war breaks out, they panic and pull their billions of dollars out of emerging markets like India to put it into safe assets like US bonds or gold. This massive, sudden selling causes the Indian stock market to crash.

Q2: Will the price of petrol and diesel go up immediately?

Not necessarily immediately, but eventually yes. In India, oil marketing companies (like IOCL and BPCL) absorb some of the shock for a short time. However, if the war drags on and global crude oil stays above $90 or $95 a barrel for weeks, the companies will be forced to pass that cost onto the consumer, leading to higher prices at the petrol pump.

Q3: How exactly does expensive oil cause my home loan EMI to increase?

It is a chain reaction: Expensive oil causes transport costs to rise -> This causes the price of all goods to rise (Inflation) -> To fight high inflation, the RBI increases the Repo Rate -> Because your home loan is linked to the Repo Rate, your bank increases your home loan interest rate -> This results in a higher EMI or a much longer loan tenure.

Q4: Should I convert my floating-rate home loan to a fixed rate right now?

Usually, no. Banks anticipate future rate hikes, so their fixed-rate offers are heavily marked up. If you switch to a fixed rate now, you are locking in at the absolute peak of the crisis. When the war ends and inflation cools down, floating rates will drop, but you will be stuck paying the expensive fixed rate.

Q5: My bank increased my loan tenure instead of my EMI. Is this bad?

Yes, it is terrible for your wealth. Increasing the tenure means you will be paying interest to the bank for an extra 3 to 5 years. Over the lifetime of a 20-year loan, this can easily cost you ₹10 Lakhs to ₹15 Lakhs in pure, extra interest. Always try to increase your monthly EMI amount instead to keep the tenure short.

Q6: What is “Imported Inflation”?

Imported inflation happens when the general price of goods in a country rises because the cost of importing raw materials has gone up. For India, because we import 85% of our oil and pay for it in US Dollars, a spike in global oil prices and a weak Rupee instantly creates imported inflation.

Q7: I am about to take a new home loan next month. Should I wait?

You should not try to “time” the interest rate market. If you have found the right house and your finances are stable, take the loan. Since it will be a floating rate loan, if interest rates are high now, you will automatically get the benefit when the RBI eventually cuts rates in the future after the crisis resolves.

Q8: If the Rupee is weak, does it benefit anyone in India?

Yes. A weak Rupee is actually fantastic for Indian companies that export goods and services. For example, massive Indian IT companies (like TCS or Infosys) who bill their American clients in US Dollars will earn more Rupees for every Dollar they bring back into the country, temporarily boosting their profit margins.

Q9: The stock market is crashing. Should I stop my mutual fund SIPs?

Absolutely not! Stopping your Systematic Investment Plans (SIPs) during a market crash is the worst financial mistake you can make. When the market is down, your SIP amount buys more units of the mutual fund at a massive discount. When the war ends and the market eventually recovers, those cheap units will generate massive wealth for you.

Q10: Can the government stop the RBI from increasing the Repo Rate?

No. The Reserve Bank of India (RBI) operates independently. While they work closely with the government to manage the economy, the RBI has a legal mandate to keep inflation strictly between 2% and 6%. If the war threatens to push inflation past 6%, the RBI’s Monetary Policy Committee will hike rates, regardless of political pressure.