TL;DR: Key Takeaways on the Iran War Impact on Loans

If you are short on time, here is the quick summary of how the West Asia conflict is hitting the Indian financial system:

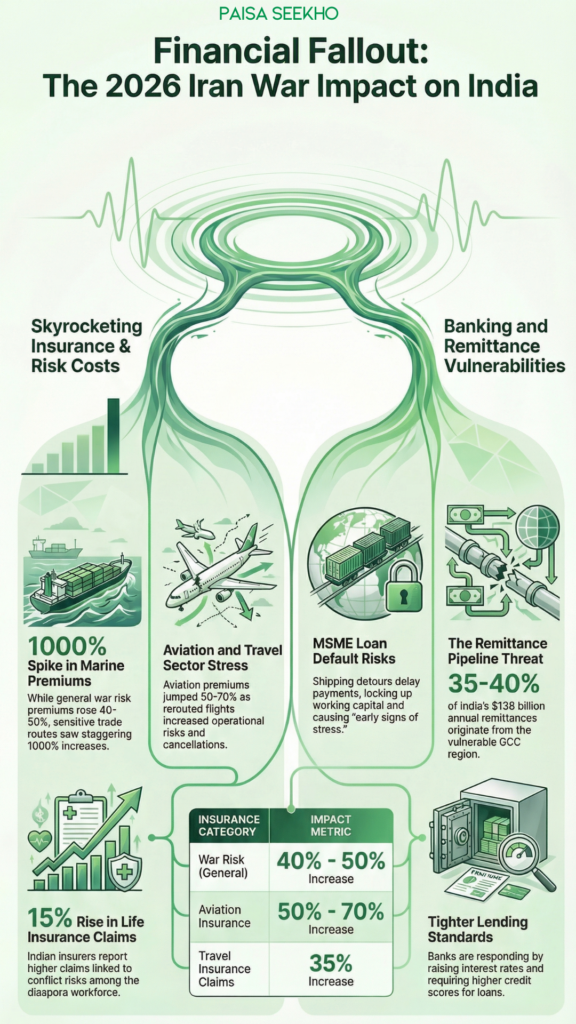

- The Cost of Risk: War risk premiums have jumped by 40% to 50% generally, with marine insurance premiums surging by over 1000% on key trade routes.

- Bank Margins Under Pressure: High crude prices and supply chain delays are causing companies (especially MSMEs) to delay their loan repayments, putting pressure on bank margins.

- The Remittance Threat: 35% to 40% of India’s inward remittances come from GCC (Gulf) countries. A prolonged war could hurt employment in the Middle East, dropping the money sent back to Indian families.

- Travel Insurance Hikes: Aviation insurance costs have shot up by 50–70%, and travel insurance claims have increased by 35% due to flight cancellations and airspace restrictions.

- Slower Trade: Trade finance is choked. Supply chain delays mean businesses have their working capital locked up for much longer, increasing the risk of defaults.

Introduction

When a geopolitical conflict breaks out thousands of miles away, most people worry about the price of petrol. But behind the scenes, a much deeper and more dangerous financial chain reaction is taking place.

The escalating conflict in West Asia (involving Iran) has severely disrupted global shipping routes and triggered massive volatility in crude oil prices. But according to a startling new April 2026 report by global consulting firm EY India, the real victim of this war is not just the oil market, it is the entire Indian Banking, Financial Services, and Insurance (BFSI) sector.

The report highlights that the war is pushing up “War Risk Premiums” by a staggering 40% to 50%, completely reshaping cost structures for banks, insurers, and ultimately, everyday consumers.

If you run a small business (MSME), send money to family abroad, or are planning to renew your business or travel insurance, you are about to feel the heat of this global crisis. In this deep-dive guide, we will break down the EY India report, explaining exactly how the war is stressing out Indian banks, why your insurance premiums are about to skyrocket, and how it could threaten the remittance economy.

1. What is a “War Risk Premium”?

When cargo ships travel from Europe or the Middle East to India, they carry millions of dollars worth of goods (like oil, electronics, and chemicals). To protect these goods from sinking or piracy, companies buy “Marine Insurance.”

However, standard insurance does not cover damages caused by a literal war. If a ship has to travel through a highly dangerous, active conflict zone (like the Red Sea or the Strait of Hormuz right now), the insurance company demands an extra fee called a “War Risk Premium.”

According to EY India, the current conflict has caused the standard war risk premiums to jump by 40% to 50%. But it gets worse. For specific, highly sensitive marine routes, these premiums have surged by an unbelievable 1000%.

When a shipping company pays 1000% more for insurance, they do not absorb that loss. They pass that cost down to the Indian manufacturer, who passes it down to the Indian consumer. This massive spike in insurance costs is a direct, hidden driver of the imported inflation we discussed in our previous articles.

2. Why Indian Banks Are Getting Nervous (The MSME Threat)

You might wonder why a bank in Mumbai cares about a ship in the Red Sea. It is because of Trade Finance and Working Capital.

Let’s say an Indian MSME (Micro, Small, and Medium Enterprise) manufactures auto parts and exports them to Germany. The MSME takes a “Working Capital Loan” from SBI to buy raw materials. Usually, the goods reach Germany in 20 days, the German client pays the MSME, and the MSME pays the loan back to SBI.

But because of the war, ships have to take a massive detour around the continent of Africa. That 20-day journey now takes 45 days.

- The MSME does not get paid for 45 days.

- Their money is “locked up” in the delayed cargo.

- Because they have no cash flow, they struggle to pay their EMI back to the Indian bank on time.

EY India explicitly warns that Indian banks are already seeing “early signs of stress.” MSMEs are showing irregular cash flows, elongated receivable cycles, and a higher dependence on short-term emergency liquidity just to survive. If this war drags on for another quarter, these delayed payments could quickly turn into Non-Performing Assets (NPAs), causing severe damage to the asset quality of Indian banks.

3. The Remittance Risk: The Middle East Money Pipeline

India relies heavily on its diaspora. We are the highest receiver of inward remittances in the world, pulling in roughly $138 billion annually.

A massive chunk of this money, about 35% to 40%, originates from hardworking Indians living in the Gulf Cooperation Council (GCC) countries (like the UAE, Saudi Arabia, and Qatar). According to the EY report, the UAE–India corridor alone contributes nearly $22 billion every year.

If the West Asia conflict remains contained, remittances might actually see a short-term spike as expats panic and rush to send all their savings back to the safety of Indian bank accounts.

However, if the war spreads and becomes a prolonged regional conflict, the economic fallout would be devastating. A massive war would halt construction projects, shut down businesses, and lead to widespread job losses for Indian expats in the Middle East. If they lose their jobs, the $138 billion remittance pipeline will shrink, severely hurting millions of families back in Kerala, Punjab, and Uttar Pradesh who rely on that monthly foreign cash to survive.

4. The Insurance Nightmare: Aviation, Travel, and Life Claims

The insurance sector is arguably taking the sharpest, most immediate hit from the West Asia conflict. EY India highlights that the chaos is spreading across multiple specific insurance segments:

Aviation and Travel Insurance

Because commercial airlines are being forced to completely reroute their flights to avoid flying over hostile airspace, their operational costs and risks have skyrocketed. In response, aviation insurance premiums have increased by 50% to 70%.

For the everyday consumer, the impact is visible in travel insurance. Flight cancellations, missed connections, and stranded passengers have caused travel insurance claims to jump by an estimated 35%. If you are planning an international trip to Europe or the Middle East this summer, expect your travel insurance policy to be significantly more expensive than it was last year, with much stricter terms regarding “acts of war.”

Life Insurance Claims

Tragically, the war is also impacting human lives connected to the Indian diaspora and cross-border workforce. The EY report notes that Indian life insurers are already seeing a 10% to 15% increase in claims linked directly to conflict-related risks. To make matters worse, settling these claims is becoming a bureaucratic nightmare due to the complexities of getting official death certificates and documentation out of active war zones.

Reinsurers Are Pulling Back

When an Indian insurance company takes on too much risk, they buy “reinsurance” from massive global companies to protect themselves. Because the global risk is so high right now, these global reinsurers are raising their costs and refusing to cover high-risk geographies. This forces the primary Indian insurers to take on all the risk themselves, severely crushing their profitability.

5. What Does This Mean for the Everyday Consumer?

The EY India report proves that the BFSI sector is bracing for impact. As these massive financial institutions start shifting into “proactive risk management,” the effects will trickle down to the regular consumer in three distinct ways:

1. Tighter Lending Standards:

Because banks are worried about MSMEs defaulting, they will become much stricter with approving new business loans or personal loans. If you are applying for an unsecured loan, you will need a flawless CIBIL score, and you can expect slightly higher interest rates as the banks “price in” the geopolitical risk.

2. Expensive Insurance Renewals:

If you run a business that relies on importing or exporting, prepare for a massive shock when you renew your trade credit or marine insurance this quarter. Even for regular retail consumers, expect slight premium hikes across general travel and health insurance as companies try to protect their shrinking profit margins.

3. Mixed Impact on Payments:

As fuel and freight costs go up due to expensive oil, the overall cost of buying goods will rise (inflation). Initially, digital payment companies might see a boost in transaction values (because everything costs more). However, as inflation eats into people’s salaries, “discretionary consumption” will drop. People will stop buying luxury items, swiping their credit cards less often, which will ultimately hurt the fee income of massive payment networks.

Conclusion

The 2026 EY India report on the BFSI sector is a sobering reminder that war is terrible for business. While the stock market might react to daily headlines, the actual structural damage is happening deep within the plumbing of the financial system.

When war risk premiums jump by 1000%, and working capital gets locked up in delayed ships, the Indian banking system is forced to absorb the shock.

For the everyday citizen and business owner, this is not a time to panic, but it is a time to be incredibly financially defensive. Ensure your business has enough cash reserves to survive delayed client payments, avoid taking on unnecessary unsecured debt, and be prepared to pay a premium to protect your assets in an increasingly volatile world.

Frequently Asked Questions (FAQs): War Risk and BFSI Margins

Q1: What is a “War Risk Premium” in insurance?

Standard marine and aviation insurance policies do not cover damages caused by acts of war. If a ship or airplane has to travel through a dangerous conflict zone, the insurance company charges a massive extra fee, known as a War Risk Premium, to provide coverage.

Q2: How much have these premiums increased due to the West Asia conflict?

According to the EY India report, general war risk premiums have jumped by 40% to 50%. Aviation insurance has gone up by 50-70%, and marine insurance on specific sensitive trade routes has surged by over 1000%.

Q3: How does the war hurt the profit margins of Indian banks?

The war delays shipping, meaning Indian businesses (especially MSMEs) have their money locked up in transit for much longer. Because they have irregular cash flow, they struggle to pay their bank loan EMIs on time, increasing the risk of defaults (NPAs) and squeezing the bank’s profit margins.

Q4: Will the war affect the money NRIs send back to India?

India receives nearly 40% of its massive remittance inflows from Gulf (GCC) countries. If the war stays contained, remittances might briefly increase as expats send emergency savings home. However, a prolonged war could cause massive job losses in the Middle East, leading to a severe drop in the money sent back to Indian families.

Q5: Why are travel insurance claims increasing?

Due to the conflict, airlines are avoiding specific airspaces, leading to massive flight rerouting, cancellations, and delays. This chaos has caused travel insurance claims to jump by 35% as stranded passengers claim compensation for disrupted travel plans.

Q6: What are “second-order effects” in banking?

First-order effects are immediate (like the stock market crashing). Second-order effects happen with a delay of a few months. For example, a business paying higher freight costs today will eventually show irregular cash flow and GST volatility next quarter, which are the early warning signs before a loan default.

Q7: Will my personal loan or credit card interest rate go up?

It is highly likely. As banks face margin compression and see higher risks in the market, they will tighten their lending standards. They may increase interest rates on unsecured, small-ticket retail loans to compensate for the higher risk of defaults in the economy.

Q8: What is happening to the reinsurance market?

Reinsurers are massive global companies that provide insurance to insurance companies. Because the global geopolitical risk is so high, reinsurers are limiting their capacity and raising their prices. This forces primary Indian insurers to take on more risk themselves, hurting their profitability.

Q9: How are life insurance companies impacted by a war in West Asia?

Indian life insurers are seeing a 10% to 15% increase in claims connected directly to conflict-related risks, primarily from the Indian diaspora and cross-border workforce in the affected regions.

Q10: What should an MSME owner do to survive this crisis?

MSME owners must prioritize liquidity. Secure longer working capital credit limits from your bank before lending standards tighten further. Factor in the 40-50% higher insurance premiums and 20-day shipping delays into your pricing models, and avoid locking all your cash into non-essential inventory.