TL;DR: Key Takeaways on the New Credit Reporting Cycle

If you are short on time, here is exactly how the RBI’s new rules will impact your wallet:

- Lightning-Fast Updates: Banks must now report borrower data to credit bureaus at weekly intervals (four times a month).

- Instant Rewards: When you clear a loan or pay down a credit card, your CIBIL score will improve in a matter of days, not weeks.

- Instant Punishment: If you miss an EMI or default, it will reflect on your credit report almost immediately, instantly dropping your score.

- The Death of “Loan Stacking”: The dangerous practice of applying for multiple loans from different apps within a 30-day window (before the system updates) is now officially impossible.

- Better Approvals for Good Borrowers: With near-real-time data, banks can confidently and instantly approve loans for healthy borrowers because they know exactly how much debt you hold today.

Introduction

If you have ever paid off a massive credit card bill or finally closed a heavy personal loan, you probably know the feeling of waiting for your CIBIL score to jump. You check it the next day, and… nothing. You check it a week later, and it still shows the old, high debt.

For decades, the Indian credit system operated on a massive time delay. Banks were slow to report your good behavior, which meant you had to wait weeks to get approved for a new, cheaper loan. On the flip side, this delay also allowed reckless borrowers to cheat the system.

The Reserve Bank of India (RBI) has decided that in the era of 10-minute grocery deliveries and instant UPI payments, waiting a month for a credit report update is unacceptable.

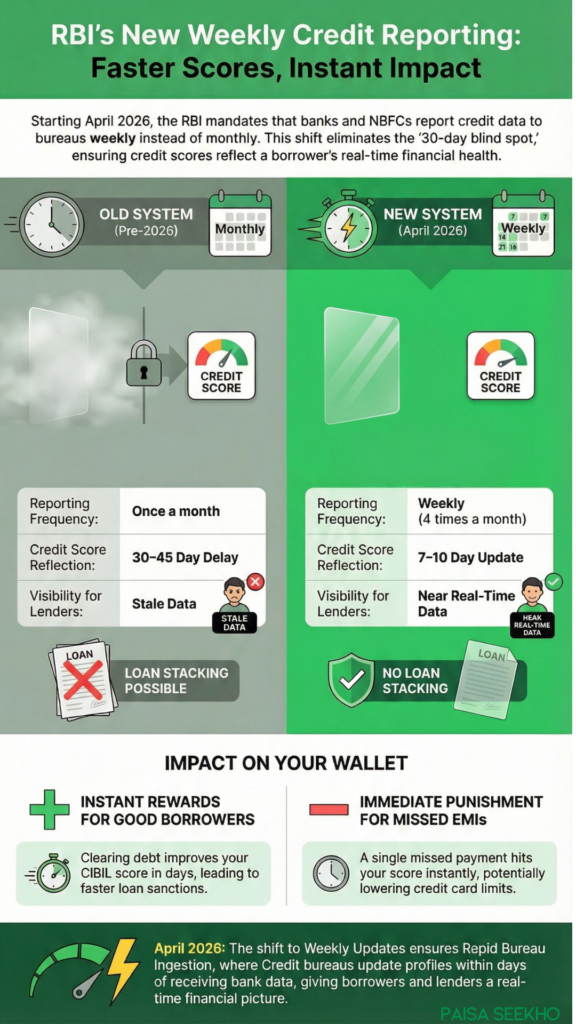

Starting in April 2026, the RBI has officially mandated a massive shift in how banks, NBFCs, and loan apps communicate with Credit Information Companies (CICs like CIBIL, Experian, and Equifax). The system is moving from a sluggish monthly or fortnightly cycle to an aggressive weekly reporting cycle.

This might sound like a boring backend banking update, but it is going to completely rewire how your EMIs are tracked, how fast your loans are approved, and how quickly you are punished for missing a payment. Let us break down exactly what this new reporting cycle means for your financial life.

What Was the Old CIBIL Score Update Time, and Why Was it Flawed?

To understand why this 2026 update is a game-changer, we have to look at the incredibly flawed system we used to rely on.

Historically, banks and NBFCs reported your credit data to bureaus like CIBIL only once a month.

Imagine you had a ₹5 Lakh personal loan, and you paid off the final installment on the 2nd of the month. Your bank wouldn’t officially tell CIBIL about this until the 30th of the month. CIBIL would then take a few more days to ingest and update their database.

This meant there was a massive 30 to 45-day blind spot in your financial record.

If you tried to apply for a home loan on the 15th of the month, the new bank would pull your CIBIL report, see that you still owed ₹5 Lakhs (because it hadn’t updated yet), and reject your home loan application for having too much debt. It was incredibly frustrating for honest taxpayers.

While the RBI tried to fix this in 2025 by shifting to a 14-day (fortnightly) reporting cycle, it still wasn’t fast enough for the modern, app-based digital lending economy.

What is the RBI Weekly Credit Reporting Rule for 2026?

The RBI realized that credit reports are the absolute backbone of the financial sector. If the data is stale, the whole system is at risk.

Under the new directives rolling out in April 2026, the RBI has instructed all regulated lending institutions (Banks, NBFCs, and Housing Finance Companies) to upgrade their technology. They are now required to submit “incremental” credit information records to CICs at weekly intervals (specifically on the 7th, 14th, 21st, 28th, or the last day of the month, depending on the specific regulatory bracket).

This “incremental” data includes:

- Any brand-new loan accounts you opened.

- Any loan accounts you officially closed.

- Changes in your outstanding balances (like paying a heavy credit card bill).

- And most importantly, any accounts where an interest or principal installment is overdue.

Furthermore, the credit bureaus (like CIBIL) are mandated to ingest this data into your profile within just a few calendar days of receiving it. The 45-day blind spot has been permanently erased.

How Will the New Cycle Stop “Loan Stacking” in CIBIL?

While the new system helps honest borrowers, it was primarily designed as a weapon to destroy a dangerous fraud known as “Loan Stacking.”

During the boom of instant digital lending apps, a toxic trend emerged. Let’s say a borrower was desperate and needed ₹5 Lakhs, but their salary only qualified them for a ₹1 Lakh loan.

The borrower would download five different loan apps and apply for a ₹1 Lakh loan on all of them on the exact same day.

Because of the old 30-day reporting delay, App #2 had no idea that App #1 had just given the borrower a loan. App #3 had no idea about Apps #1 and #2. The borrower would successfully “stack” five different loans, walk away with ₹5 Lakhs, and inevitably default because they could not afford the massive combined EMIs.

With the new 2026 weekly reporting cycle, loan stacking is dead.

If you take a loan on Monday, it will hit your credit report in a few days. If you try to apply for a second loan on Friday, the new lender’s system will instantly see Monday’s debt and flag you as a high-risk, desperate borrower, immediately rejecting the application. This protects both the banks from bad loans and the borrower from falling into a deadly debt trap.

Will Fast Loan Approvals in India Become Easier for Good Borrowers?

Yes, absolutely! In the banking world, uncertainty is expensive. When a bank is not 100% sure about your current financial health, they either reject your application, ask for a mountain of physical paperwork to prove your income, or charge you a very high interest rate to cover their risk.

Near-real-time credit reporting removes the uncertainty.

When you apply for an auto loan or a home loan now, the bank pulls a credit report that is less than a week old. They can clearly see that you paid your credit card bill just three days ago. Because they have absolute confidence in your current, real-time data, they can run your profile through their AI underwriting models and issue an instant, pre-approved sanction letter.

If you have a clean financial record, the friction of getting a loan has essentially been reduced to zero.

How Often Do Banks Report Missed EMIs Under the New System?

This is the harsh reality check of the new system. The era of “forgiveness delays” is over.

In the past, if your EMI was due on the 5th, but you forgot and paid it on the 15th, you might have gotten lucky. If the bank only reported data on the 30th, they would just report the account as “current” and “paid,” and your CIBIL score would remain perfectly untouched.

Under the new weekly reporting cycle, your mistakes are broadcasted instantly.

If you miss your EMI and cross the weekly reporting threshold, that “Overdue” or “Days Past Due (DPD)” flag is instantly sent to CIBIL.

This has severe, cascading consequences. Modern banks continuously monitor your credit score in the background. If you miss a personal loan EMI on a Tuesday, by next week, your other banks might see that drop in your CIBIL score and proactively slash the credit limit on your existing credit cards to reduce their own risk.

How Should You Prepare Your Finances for Real-Time Credit Scores?

The rules of the game have changed. You can no longer play fast and loose with payment deadlines. To thrive in this new, hyper-fast credit environment, you need to update your financial habits:

1. Automate Everything (The 3-Day Rule)

Do not rely on your memory to pay EMIs. Set up auto-debit mandates (e-NACH) for every single loan and credit card. More importantly, ensure the money is sitting in your bank account at least 3 days before the due date. A simple server glitch or a weekend delay could now result in an instant negative mark on your real-time credit report.

2. Time Your Major Loan Applications

If you are planning to apply for a massive home loan, pay off all your smaller debts (like your credit card balances or BNPL accounts) and wait about 10 days. Because the system updates weekly, your CIBIL score will quickly reflect a clean, zero-debt profile, allowing you to negotiate the lowest possible home loan interest rate.

3. Space Out Your Credit Card Inquiries

Every time you apply for a credit card, the bank does a “Hard Inquiry” on your CIBIL report, which drops your score by a few points. Because updates are so fast now, applying for three different credit cards in a single week will instantly trigger alarm bells across the banking system, leading to automatic rejections. Space out your applications by at least three to six months.

Conclusion: A System Built for Trust

The transition to a weekly credit reporting cycle in 2026 is a massive leap forward for the Indian financial ecosystem. While the instant punishment for a missed EMI might seem harsh, the overall macroeconomic benefits are undeniable.

By eliminating the dangerous blind spots that allowed fraudsters to stack loans and cheat the system, the RBI is making the entire banking sector safer and more stable. And when banks feel safe, they lend more freely and at cheaper interest rates.

For the disciplined, everyday middle-class Indian, this new system is a massive reward. Your good financial habits are no longer ignored for a month. Every time you clear a debt or pay a bill on time, the system recognizes it almost instantly, paving a faster, smoother road to achieving your financial goals.

Frequently Asked Questions (FAQs): RBI Credit Reporting Cycle

Q1: How long does it take for CIBIL to update after closing a loan in 2026?

Thanks to the new RBI mandate, once you officially close a loan and receive the No Objection Certificate (NOC), the bank will report the closure during their next weekly reporting cycle. Your CIBIL score should reflect the closed account within 7 to 10 days.

Q2: What is the new RBI rule for credit reporting frequency?

Starting in April 2026, the RBI requires all commercial banks, NBFCs, and housing finance companies to report incremental borrower data (like new loans, closed loans, and missed payments) to Credit Information Companies at weekly intervals (four times a month).

Q3: Will checking my own CIBIL score frequently lower it?

No. When you check your own score on apps like GPay or the official CIBIL website, it is called a “Soft Inquiry.” Soft inquiries do not impact your score at all. Only “Hard Inquiries” (when a bank checks your score because you applied for a loan) will drop your score slightly.

Q4: What is “loan stacking” and why is it banned?

Loan stacking is a dangerous practice where a borrower applies for multiple loans from different apps simultaneously to get more money than they can afford to repay. The new weekly reporting cycle kills this practice because lenders can now instantly see if you recently took a loan from a competitor just days ago.

Q5: If I miss my EMI by just 2 days, will it hit my CIBIL instantly?

Banks typically report an account as overdue once it crosses the billing cycle deadline. While a 2-day delay might incur late fees from the bank, it depends on whether those 2 days cross the exact date the bank sends its weekly file to CIBIL. It is highly risky, so always pay on time.

Q6: Do these new fast reporting rules apply to BNPL (Buy Now, Pay Later) apps?

Yes. BNPL apps are essentially micro-loans partnered with registered NBFCs. Those NBFCs are strictly regulated by the RBI and must adhere to the exact same weekly reporting cycles. Missing a small BNPL payment will quickly damage your overall credit score.

Q7: Will my credit card limit decrease if I miss a personal loan EMI?

It is very possible. Many banks use “continuous monitoring” algorithms. If you miss a loan EMI at Bank A, it updates on your CIBIL quickly. Bank B sees the drop in your score and might proactively reduce your credit card limit to protect themselves from your perceived financial stress.

Q8: Which Credit Information Companies (CICs) does this apply to?

The RBI directive applies to all four major Credit Information Companies operating in India: TransUnion CIBIL, Experian, Equifax, and CRIF High Mark.

Q9: Will loan approvals actually be faster now?

Yes. Because banks have access to near-real-time data regarding your current outstanding debt, they do not have to assume extra risk. This allows their automated underwriting software to approve personal and auto loans instantly for healthy borrowers.

Q10: What should I do if my bank reports incorrect data under the new fast cycle?

If a bank mistakenly reports an EMI as missed, it will damage your score quickly. You should immediately raise a formal “Dispute” on the official CIBIL website. The bureau is legally required to contact the bank, and the bank must verify and correct the error within a strict timeframe set by the RBI.