TL;DR: Key Takeaways on the NPS Swasthya Scheme

If you need the quick facts about this revolutionary new retirement update, here is your summary:

- The Big Change: Under the new “NPS Swasthya” scheme, eligible NPS subscribers can legally use a portion of their retirement corpus to pay for both out-patient (OPD) and in-patient hospitalisation expenses.

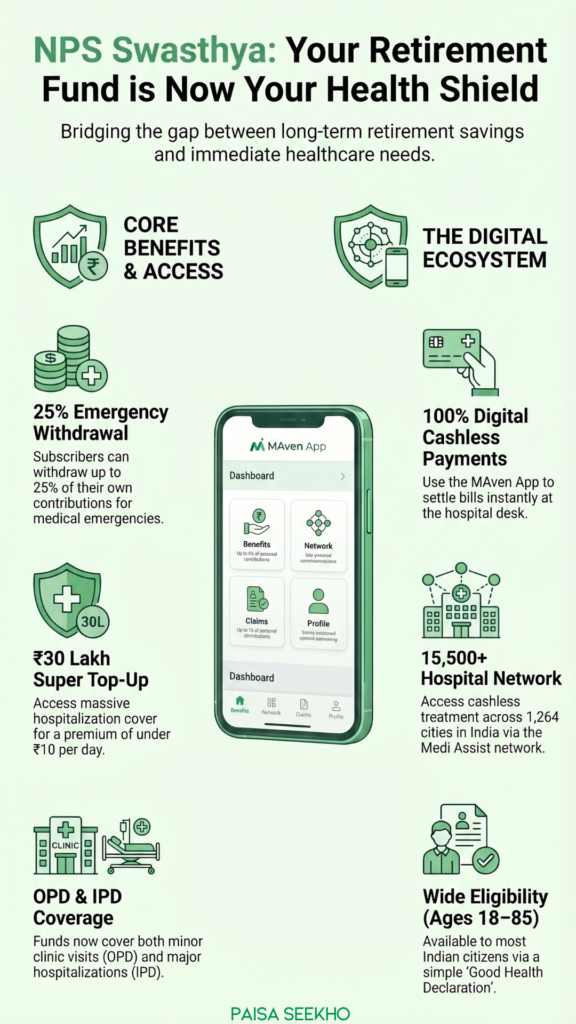

- The Withdrawal Limit: You are permitted to access a ‘Net Eligible Balance’ of up to 25% of your own contributions specifically for medical emergencies.

- The Insurance Bonus: The scheme includes a built-in ‘Group Health Super Top-Up’ insurance plan from Aditya Birla Health Insurance, offering up to ₹30 lakh coverage for under ₹10 a day!

- Cashless Convenience: The entire system is digitized via the MAven App (powered by Medi Assist), allowing you to make cashless payments at over 15,500 hospitals across India.

- Eligibility: The scheme is available to Indian citizens aged 18 to 85, subject to a standard ‘Good Health Declaration’ during onboarding.

Introduction

If there is one financial fear that haunts almost every Indian as they grow older, it is the devastating cost of healthcare. You can spend thirty years diligently saving for a peaceful retirement, only for a single, massive medical emergency to wipe out a significant portion of your life savings in a matter of days.

Historically, the National Pension System (NPS) was a strict, locked-in vault. You put your money in, and you could not easily touch it until you turned 60. While this forced discipline was great for building wealth, it created a tragic paradox: elderly citizens were sitting on massive retirement funds, yet they struggled to pay for immediate, life-saving hospital treatments because their money was inaccessible.

In April 2026, the Pension Fund Regulatory and Development Authority (PFRDA) completely changed the rules of the game with a historic new initiative: NPS Swasthya.

For the very first time, this multi-partner scheme explicitly bridges the gap between your retirement savings and your immediate healthcare needs. In this comprehensive, easy-to-read guide, we are going to break down exactly what NPS Swasthya is, how you can unlock your pension funds for hospital bills, and how this brilliant new initiative acts as a massive financial safety net for your family.

1. What is NPS Swasthya and Why Was it Created?

To put it simply, NPS Swasthya is the ultimate financial hybrid. It takes the wealth-building power of a mutual fund, the discipline of a pension, and the safety of health insurance, and rolls them into one single, powerful product.

Sivasubramanian Ramann, the Chairperson of PFRDA, summarized the philosophy behind the launch perfectly: “The idea of retiring with dignity cannot be alienated from a strong sense of medical security… several elderly remain outside the medical insurance net, making them extremely vulnerable.”

The reality of 2026 is that people are living longer, but healthcare inflation is rising at an alarming 14% every year.

The Old Rule: Under standard NPS rules, early partial withdrawals were heavily restricted and required painful manual paperwork.

The NPS Swasthya Rule: This new multi-partner initiative legally carves out a specific medical corridor. It allows subscribers to seamlessly unlock up to 25% of their contributions to fund immediate medical crises, all while the remaining 75% of the corpus continues to enjoy long-term, tax-free, market-linked compounding growth.

2. How the Ecosystem Works

The PFRDA didn’t just tweak a rule; they built an entire healthcare ecosystem. To make NPS Swasthya work, several massive financial and medical institutions had to join forces:

- The Regulator: PFRDA oversees the entire operation to ensure your retirement money is safe.

- The Technology Backbone: Medi Assist acts as the core aggregator. They developed the MAven App, which connects your NPS account directly to the hospital billing desk.

- The Record Keeper: CAMS KRA manages your onboarding, handles the KYC, and keeps track of your exact eligible balance.

- The Fund Managers: The actual money within the NPS Swasthya pool is actively managed and grown by Tata Pension Fund and Axis Pension Fund.

- The Insurance Shield: Aditya Birla Health Insurance steps in to provide a massive, integrated Super Top-Up insurance cover.

3. How Do You Access the Money? (The MAven App)

The biggest complaint about government schemes is the bureaucracy. If you are having a heart attack, you cannot wait 15 days for a babu to approve your withdrawal form.

NPS Swasthya completely digitizes the crisis response.

When you enroll in the scheme, your account is integrated into the MAven App. If you or a covered family member requires hospitalization, you do not need to liquidate your assets or beg relatives for a loan.

You simply open the app at the hospital. Because Medi Assist has a network of over 15,500 hospitals across 1,264 cities in India, the app facilitates a direct, cashless payment system. The app calculates your 25% eligible balance, instantly sells the equivalent number of your NPS mutual fund units, and transfers the cash directly to the hospital to settle your in-patient (IPD) or out-patient (OPD) bills.

(Note: Phase 1, launched earlier in January 2026, only covered out-patient services. This massive April update officially unlocks the funds for heavy in-patient hospitalization bills!)

4. The Hidden Gem: The Built-In ₹30 Lakh Super Top-Up

While unlocking 25% of your savings is fantastic, what happens if your medical bill is massive and your 25% balance is simply not enough to cover it?

This is where NPS Swasthya proves its brilliance.

When you enroll in this specific scheme, you are not just getting withdrawal rights; you are automatically given access to a ‘Group Health Super Top-Up’ insurance plan provided by Aditya Birla Health Insurance.

- As noted by Sumit Shukla, MD & CEO of Axis Pension Fund, this proposition is incredibly unique.

- It offers a massive hospitalization cover of up to ₹30 lakh.

- The cost? It is structured to be remarkably affordable, costing the subscriber under ₹10 per day.

By combining your own liquid NPS savings with this massive insurance top-up, you create an almost impenetrable financial shield against unexpected medical disasters.

5. Who is Eligible and How Do You Enroll?

The PFRDA wants to ensure this safety net reaches as many citizens as possible.

- Age Limit: The scheme is exceptionally broad, available to Indian citizens aged 18 to 85 years.

- The Health Check: Because the scheme includes a massive insurance component, you cannot enroll if you are already sitting in an ICU. Enrollment is subject to a standard ‘Good Health Declaration’. This means the onboarding process is fast and seamless for members who do not currently suffer from major, severe pre-existing conditions like advanced heart disease or chronic diabetes.

By shifting your retirement strategy to embrace NPS Swasthya, you are no longer just saving for an imaginary, distant future. You are actively building a dynamic fund that respects the reality of human aging, ensuring that if your health ever fails, your wealth will step in immediately to save you.

Frequently Asked Questions (FAQs): NPS Swasthya 2026

Q1: What exactly is the newly launched NPS Swasthya scheme?

NPS Swasthya is a multi-partner initiative launched by the PFRDA in April 2026. It allows National Pension System subscribers to legally withdraw a portion of their locked retirement funds to pay for out-patient and in-patient medical expenses, while also providing them with a massive, affordable health insurance top-up.

Q2: How much of my NPS money can I withdraw for medical emergencies?

Under the NPS Swasthya framework, eligible subscribers are permitted to access a “Net Eligible Balance” of up to 25% of their own contributions toward the pension fund specifically for medical needs.

Q3: Does it cover both minor clinics and major hospital surgeries?

Yes. Phase 1 (launched in Jan 2026) allowed withdrawals for out-patient (OPD) services like doctor consults and pharmacy bills. The new Phase 2 officially unlocks the funds to cover heavy in-patient (IPD) hospitalization bills.

Q4: How do I actually pay the hospital using my NPS funds?

You do not have to handle the cash yourself. The system is digitized through the MAven App, developed by Medi Assist. The app integrates directly with your NPS account (via CAMS CRA) and allows for instant, cashless payments at over 15,500 network hospitals across India.

Q5: What is the ₹30 Lakh Super Top-Up feature?

As a massive added benefit, NPS Swasthya enrollees get access to a ‘Group Health Super Top-Up’ insurance plan from Aditya Birla Health Insurance. For a very low premium (under ₹10 a day), it provides up to ₹30 lakh in extra coverage if your medical bills exceed your base savings.

Q6: Who manages the money in the NPS Swasthya fund?

The retirement funds allocated to this specific healthcare initiative are actively managed by Tata Pension Fund and Axis Pension Fund, ensuring your money continues to grow with market-linked returns when you are not using it.

Q7: Who is eligible to join the NPS Swasthya scheme?

The scheme is available to all Indian citizens between the ages of 18 and 85.

Q8: Do I need to undergo a massive medical test to join?

No, a physical medical test is generally not required for standard onboarding. However, enrollment is subject to a ‘Good Health Declaration,’ which acts as a simplified screening to ensure new members do not have severe, existing critical illnesses like advanced heart disease at the time of joining.

Q9: Does withdrawing 25% ruin my retirement pension?

No. The PFRDA designed this carefully. By capping the medical withdrawal at 25% of your own contributions, the system mathematically ensures that the vast majority (75% plus employer contributions and all compounded interest) remains strictly locked-in to provide you with a monthly pension when you retire.

Q10: Why is PFRDA prioritizing healthcare within a pension system?

The PFRDA recognizes that “retiring with dignity” is impossible if you are bankrupt due to medical bills. With many elderly Indians falling outside traditional, expensive senior-citizen health insurance nets, NPS Swasthya bridges the gap between retirement savings and healthcare accessibility.