TL;DR: Key Takeaways on the Business Correspondent Model

If you are short on time, here is the quick summary of how the RBI’s BC model impacts your daily life:

- The Concept: Business Correspondents (also called Bank Mitras or CSPs) are local retail agents. Banks authorise them to provide basic banking services right in your neighborhood.

- No Branch Needed: You can deposit cash, withdraw money, check your balance, and open a savings account at your local shop without ever visiting a formal bank branch.

- Powered by Aadhaar: The system primarily uses the Aadhaar Enabled Payment System (AePS). You just need your fingerprint and Aadhaar number to access your bank account.

- Zero Travel Costs: It brings “doorstep banking” to rural and unbanked areas, saving millions of citizens time and travel money.

- A Business Opportunity: If you own a small shop with a computer and internet, you can apply to become a BC agent, earning a commission on every financial transaction you process for your community.

- The 2026 RBI Overhaul: Starting July 2026, the RBI is officially restructuring agents into two distinct categories: fixed “Banking Outlets” (BC-BO) and flexible “Touchpoints” (BC-BT).

- Guaranteed Base Pay: For the first time, fixed BC-BO agents will receive a combination of a fixed base salary plus variable commission, ending the era of unpredictable monthly income.

Introduction

Imagine you live in a small village or a bustling semi-urban neighborhood. You need to deposit cash into your savings account, or perhaps you urgently need to withdraw the government subsidy that just arrived. In the past, this meant taking a day off from work, paying for a bus ticket, traveling 15 kilometers to the nearest city, and standing in a massive, sweaty line at a bank branch for three hours.

For millions of Indians, traditional banking was a luxury that cost them an entire day’s wages just in travel time.

The Reserve Bank of India (RBI) realized that India could never become a true economic superpower if half of its population was locked out of the banking system. Building massive, air-conditioned bank branches in every single village was financially impossible for the banks. So, the RBI came up with a brilliant, decentralized solution: The Business Correspondent (BC) Model. Instead of bringing the people to the bank, the RBI decided to bring the bank to the people, right to the local kirana store, the medical shop, or the mobile recharge booth.

Whether you are a customer tired of long bank queues, or a smart local entrepreneur looking to start a new, profitable business, the BC model is a financial superpower. In this comprehensive, easy-to-understand guide, we are going to break down exactly what the RBI Business Correspondent model is, how it keeps your money safe, the daily services you can use, and how you can actually partner with a bank to make money.

What Exactly is the RBI Business Correspondent Model in India?

To put it simply, a Business Correspondent (BC) is a “mini-bank” run by a regular person.

The RBI allows massive commercial banks (like SBI, HDFC, or Bank of Baroda) to hire third-party agents to act on their behalf. These agents are formally known as Business Correspondents. But in daily life, you might hear them called Bank Mitras or operators of a Customer Service Point (CSP).

Here is how the relationship works:

- The Bank: Holds the actual money, manages the heavy regulatory compliance, and provides the backend technology.

- The Corporate BC: Large companies (like CSC e-Governance or private fintech firms) that act as middlemen to manage thousands of agents.

- The Local Agent (CSP): The friendly shopkeeper in your village who has a biometric fingerprint scanner, a laptop or smartphone, and official authorization to handle your cash.

When you hand ₹1,000 in cash to the local BC agent to deposit into your account, they process it through their secure portal. The bank instantly updates your balance. The agent keeps the physical cash in their shop’s cash drawer (which they later settle with the bank). The RBI carefully monitors this entire chain to ensure the public’s money is handled safely.

What Daily Doorstep Banking Services Can a Customer Service Point (CSP) Offer?

You might assume that a small shopkeeper can only do basic tasks, but the modern CSP is surprisingly powerful. Thanks to aggressive digital upgrades, a Business Correspondent can handle almost 90% of the daily banking needs of an average Indian household.

If you visit your local Bank Mitra, you can securely access the following services:

1. Cash Withdrawals and Deposits

This is the most popular service. You do not need to find an ATM. You can walk up to the BC agent, verify your identity, and withdraw cash directly from your bank account.

2. Opening New Bank Accounts

BC agents were the absolute driving force behind the massive success of the Pradhan Mantri Jan Dhan Yojana (PMJDY). An agent can open a basic, zero-balance savings account for you in a matter of minutes. They use e-KYC (electronic Know Your Customer) simply by scanning your Aadhaar fingerprint.

3. Direct Benefit Transfers (DBT) Access

Millions of Indians receive government subsidies, like PM-Kisan installments, LPG subsidies, or old-age pensions, directly into their bank accounts. The BC model allows farmers and senior citizens to withdraw this government money instantly in their own village. No more spending ₹100 on a bus to withdraw a ₹500 pension.

4. Money Transfers (Remittances)

If a migrant worker from Bihar is working in a factory in Delhi, they can go to a local BC agent in Delhi. They can hand over physical cash, and instantly transfer that money to their family’s bank account back in their home village.

5. Micro-Insurance and Social Security

Bank Mitras are authorized to enroll you in incredibly affordable, government-backed social security schemes. For instance, the Pradhan Mantri Suraksha Bima Yojana (accidental insurance) and the Atal Pension Yojana (retirement pension). This helps secure your family’s future for just a few rupees a month.

Here is the new section detailing the massive April 2026 RBI overhaul of the Business Correspondent framework. You can insert this right before the “Conclusion” in your existing article!

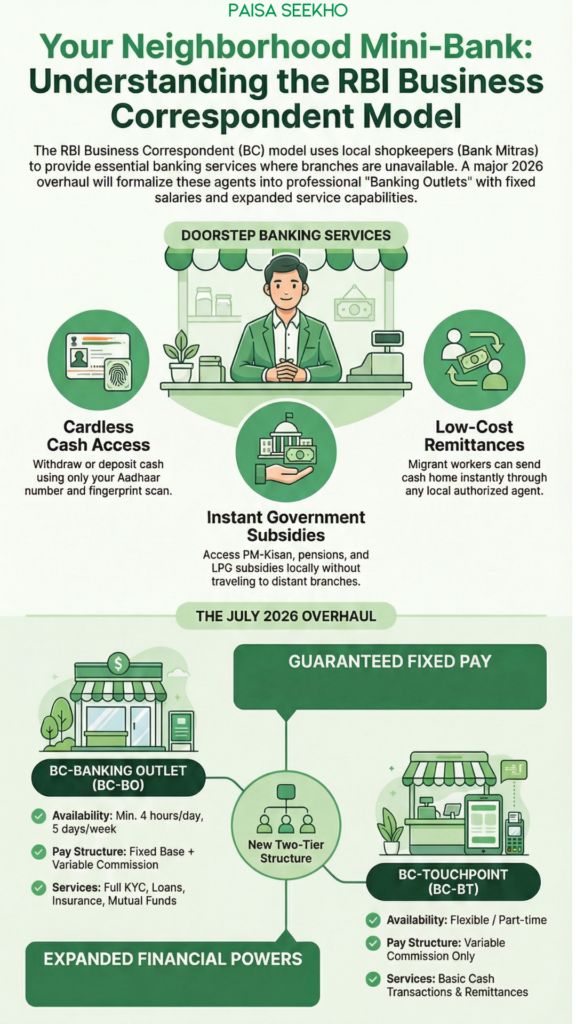

What Are the New April 2026 RBI Proposals for the Business Correspondent Model?

On April 6, 2026, the Reserve Bank of India proposed a massive, game-changing overhaul of the entire Business Correspondent framework. The BC model successfully brought millions of rural Indians into the banking system. So, RBI recognized that it was time to upgrade these local agents from simple cash-handlers to full-fledged mini-bankers.

Slated to come into effect on July 1, 2026, this new draft completely formalizes how local CSPs operate. This expands their power and protects their income. If you are an existing Bank Mitra or planning to become one, here are the massive structural changes coming your way:

1. The New Two-Tier Structure (BC-BO vs. BC-BT)

The RBI is dividing all Business Correspondents into two strict categories to standardize the customer experience:

- BC-Banking Outlets (BC-BO): These are fixed-location shops that commit to operating for at least four hours a day, five days a week. Because of their reliability, the RBI will officially classify these BC-BOs as actual “Banking Outlets” in their national data. This puts them on par with traditional bank branches for financial inclusion tracking.

- BC-Banking Touchpoints (BC-BT): These are flexible, smaller service points (like a mobile recharge vendor who only does part-time banking). They will be restricted to basic, small-value interoperable cash transactions and remittances.

2. Guaranteed “Fixed Pay” for Agents

For years, BC agents complained that their income was too unpredictable. This was because they only earned variable commissions based on how many people walked into the shop. The RBI has solved this! Under the new proposals, BC-Banking Outlets (BC-BOs) will now receive a combination of Fixed and Variable remuneration. The fixed base pay will be benchmarked by the Indian Banks’ Association. This guarantees a stable monthly income for dedicated agents. And variable pay will now also reward agents for high “customer satisfaction,” not just transaction volume.

3. The End of “Business Facilitators”

Previously, banks used “Business Facilitators” (BFs), people who just collected loan applications and handed them to the bank. But they couldn’t actually process transactions. The RBI is officially deleting the BF category. By September 30, 2026, all existing Business Facilitators must officially upgrade and migrate into the new BC-BO or BC-BT models.

4. Expanding the Power of the Agent

The RBI is allowing fixed BC-BO agents to handle much more complex financial products. Under the new rules, local agents will be permitted to:

- Handle full KYC updations and grievance redressals.

- Generate leads and actively sell Micro-Insurance, Mutual Funds, and Pension products.

- Disburse small-value credit (micro-loans) directly to customers.

- Conduct post-sanction monitoring and follow up on loan recoveries for the bank.

5. Stricter Rules and Reduced Prefunding

To balance these massive new powers, the RBI is enforcing tighter monitoring. Banks must review their BC operations every six months. BCs who process zero transactions for 60 continuous days will automatically have their IDs classified as “inactive.” However, as a massive relief to the agents, the RBI has proposed a progressive reduction in the “prefunding” requirements (the upfront cash deposit an agent must lock with the bank to start operating). This will link the reduction to the agent’s performance and service quality.

Is the Aadhaar Enabled Payment System (AePS) Safe with Local BC Agents?

A very common and valid fear among the public is security. “How can I trust my local grocery shop owner with my bank account details? Can they steal my money?”

The RBI anticipated this fear. This is why the Business Correspondent model is fundamentally powered by the Aadhaar Enabled Payment System (AePS). It is managed by the National Payments Corporation of India (NPCI).

Here is why the system is structurally safe:

- No Debit Cards or Passwords Needed: You do not give the agent your ATM card or your secret PIN. The agent never sees your bank password.

- Biometric Security: To make a transaction, you provide your Aadhaar number, the name of your bank, and your live fingerprint on a biometric scanner. The system matches your live fingerprint with the massive UIDAI database. If the print doesn’t match perfectly, the transaction is immediately blocked.

- Instant SMS Receipts: The moment a transaction is successful, your actual bank (not the agent) sends an official SMS to your registered mobile number confirming the exact amount deposited or withdrawn.

- System Limits: To prevent massive frauds, the RBI and NPCI have strict daily limits on how much cash can be withdrawn through AePS (usually capped around ₹10,000 per transaction), ensuring that life savings cannot be drained in a single swipe.

Cautionary Note: While the system is highly secure, “fingerprint cloning” scams have occasionally occurred. Always ensure you are dealing with an officially licensed, clearly branded BC agent, and never leave an agent’s shop if you receive an SMS for a withdrawal that you did not authorize.

How Does the Bank Mitra Network Solve the Rural Banking Crisis?

To understand the economic impact of the BC model, we must look at the macro picture. Before the BC model was aggressively expanded, the Indian economy faced a massive problem called “Cash Leakage.”

If a farmer in a remote village did not have a bank account, they kept their savings in a steel trunk under their bed. That money was economically “dead.” It was not earning interest for the farmer, and the banks could not use that cash to give out business loans to build the country.

By licensing thousands of Business Correspondents, the RBI created millions of new “micro-branches” overnight.

- Financial Inclusion: People who were previously terrified of grand, marble-floored bank branches felt completely comfortable walking into their neighbor’s shop to open a Jan Dhan account.

- Economic Velocity: Cash that was hidden under mattresses flooded into the formal banking system, strengthening the banks and integrating rural India into the digital economy.

- Empowering Women: Many BC agents and Bank Sakhis (female agents) are women. They actively encourage other rural women to open independent accounts, giving them financial privacy and control over household savings for the first time in their lives.

How to Become a Business Correspondent and Earn Money?

The BC model is not just a convenience for the consumer; it is a massive, highly profitable opportunity for local entrepreneurs.

If you own a small shop, like a cyber cafe, a mobile repair shop, or a local medical store, you already have foot traffic. By becoming an authorized Customer Service Point (CSP), you can add a massive new revenue stream to your existing business.

How Do You Make Money?

As a BC agent, you do not charge the customer a fee for basic services. Instead, the bank pays you a commission.

- You earn a commission for every new bank account you successfully open.

- You earn a percentage commission on every cash deposit, cash withdrawal, and money transfer you process.

- You earn fixed incentives for enrolling citizens in micro-insurance or pension schemes.

If your shop is located in a busy area or a village without a nearby ATM, processing 50 to 100 transactions a day can easily generate a handsome secondary monthly income. Furthermore, people who come to your shop to withdraw cash will likely buy groceries or mobile accessories from you before they leave, boosting your primary business!

The Basic Requirements to Start:

- Infrastructure: You need a permanent shop/retail space, a laptop or desktop computer, a reliable internet connection, a printer, and an RBI-approved biometric fingerprint scanner.

- Eligibility: You generally need to be at least 18 years old, have passed the 10th or 12th standard, have a clean police record, and possess basic computer literacy.

- The IIBF Certification: To ensure professionalism, the RBI strongly mandates that agents pass the basic “Business Correspondents/Facilitators” certification exam conducted by the Indian Institute of Banking & Finance (IIBF).

How to Apply

You usually do not apply directly to a massive bank like SBI. You apply through “Corporate BCs” or “National Business Correspondents” who hold master licenses. Companies like CSC (Common Service Centres), PayNearby, Fino Payments Bank, or specialized rural financial networks manage the onboarding. You submit your documents to them, they verify your shop, and then they link you to a sponsor bank to begin your operations.

Conclusion

When we talk about India’s financial revolution, we often focus on shiny smartphone apps, UPI records, and high-speed internet. But the true unsung heroes of Digital India are the Business Correspondents.

The RBI’s BC model is a masterclass in adapting to the unique geographical and cultural realities of a country. By trusting local shopkeepers and arming them with biometric technology, the RBI has successfully dismantled the walls of traditional banking.

If you are a consumer struggling with branch visits, look for the CSP or Bank Mitra board in your local market, it will save you hours of precious time. And if you are an ambitious shop owner looking to grow, consider joining this network. By becoming a Business Correspondent, you aren’t just starting a side business; you are becoming a vital pillar of financial empowerment for your entire community.

Frequently Asked Questions (FAQs): RBI Business Correspondent Model

Q1: What is a Business Correspondent (BC)?

A Business Correspondent is a retail agent or a local shopkeeper authorized by a bank to provide basic banking services (like cash withdrawals, deposits, and account openings) to citizens on behalf of the bank, usually in areas where setting up a full bank branch is not possible.

Q2: Is it safe to deposit my money with a local BC agent?

Yes, it is structurally safe. The agent uses secure, bank-authorized portals. The moment you hand over your cash and the agent processes it, the money reflects in your official bank account instantly, and you will receive an official confirmation SMS directly from your bank.

Q3: Do I need an ATM card to withdraw money at a CSP?

No, you do not need an ATM card. BC agents primarily use the Aadhaar Enabled Payment System (AePS). You only need your Aadhaar number (which must be linked to your bank account) and your live fingerprint on their scanner to withdraw cash.

Q4: Can a Business Correspondent charge me a fee for withdrawing my own money?

No. For basic AePS cash withdrawals and deposits, the agent is strictly prohibited from charging the customer any extra fee or “convenience charge.” The agent is paid a commission directly by the bank. If an agent demands a cut of your cash, you should report them to the sponsor bank.

Q5: Can I open a regular savings account at a Bank Mitra?

BC agents specialize in opening Basic Savings Bank Deposit Accounts (BSBDA) and Pradhan Mantri Jan Dhan Yojana (PMJDY) accounts. These are fully functional, zero-balance savings accounts designed for everyday use and receiving government subsidies.

Q6: What is the daily withdrawal limit at a Business Correspondent?

To prevent massive cash draining and fraud, the National Payments Corporation of India (NPCI) and individual banks set limits on AePS transactions. Currently, the limit is generally capped at ₹10,000 per transaction, and banks often restrict users to a maximum of 5 AePS transactions per day.

Q7: I want to become a BC agent. Do I need a college degree?

No, you do not need a college degree. Most Corporate BCs require you to have passed your 10th or 12th standard exams and possess basic computer and internet operating skills. You must also have a clean police verification record.

Q8: What is the IIBF BC/BF exam?

The Indian Institute of Banking & Finance (IIBF) conducts a mandatory certification exam for Business Correspondents and Business Facilitators. The exam tests your basic knowledge of banking rules, customer service, and financial products to ensure you are qualified to handle public money.

Q9: Can I offer loans as a Business Correspondent?

Generally, a standard BC agent does not have the authority to approve or disburse massive loans on the spot. However, you can act as a “Business Facilitator,” meaning you can help your local customers fill out loan applications, collect their documents, and forward the leads to the main bank branch, earning a commission if the loan is approved.

Q10: What equipment do I need to buy to start a CSP shop?

To start operations, you will need to invest in a desktop or laptop computer, a reliable internet connection (Wi-Fi or dongle), a standard printer for receipts, and an official STQC-certified biometric fingerprint scanner (like Mantra or Morpho) to authenticate Aadhaar transactions.