TL;DR: Key Takeaways on the RBI Inward Remittance Rules 2026

If you are expecting a foreign wire transfer soon, here is exactly how the new RBI rules will speed up your payment:

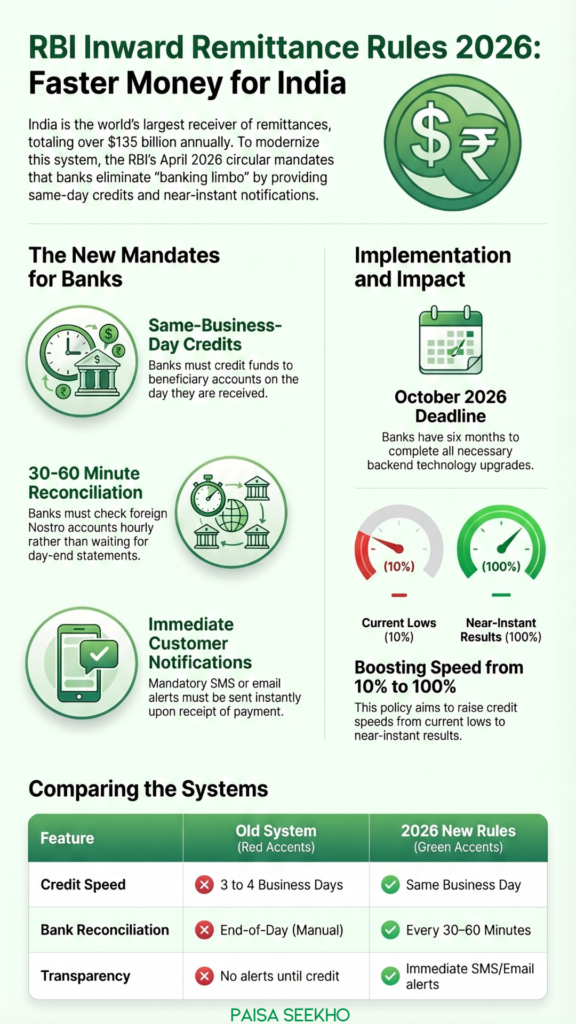

- The Core Mandate: Banks must credit inward foreign remittances to the beneficiary’s account on the same business day they are received (if received during forex market hours).

- Instant Notifications: Banks are now legally required to send you an SMS/email alert immediately upon receiving a cross-border payment message, ending the guessing game.

- The Nostro Fix: Banks can no longer wait until the “end of the day” to reconcile their foreign accounts. They must do it in near real-time (at intervals not exceeding 30 to 60 minutes).

- The Implementation Timeline: While notification rules apply immediately, the RBI has given Indian banks a 6-month deadline to upgrade their technology to guarantee same-day credit.

- The Macro Impact: At over $135 billion a year, India is the world’s largest receiver of remittances. This move will inject liquidity into the domestic economy much faster.

Introduction

If you are a freelance software developer working for US clients, an exporter shipping goods to Europe, or a parent waiting for your child working in Dubai to send money home, you know the anxiety of cross-border payments.

The client sends the money on Monday, and they send you a confirmation receipt. But when you check your Indian bank account on Tuesday, the money isn’t there. You call the bank on Wednesday, and they tell you it is “stuck in transit” or waiting for backend reconciliation. Finally, on Thursday or Friday, the funds magically appear.

For the country that receives more foreign money than any other nation on Earth, our inward remittance system has been unacceptably slow.

The Reserve Bank of India (RBI) has finally decided to fix this permanently. In a massive regulatory overhaul announced in April 2026, the RBI issued a final circular mandating banks to drastically accelerate cross-border inward remittances. The headline rule? Banks must now credit foreign payments to your account on the exact same business day.

In this comprehensive guide, we will break down the RBI’s new directives, explain the backend “Nostro account” problem that caused these delays, and explore how this will make life significantly easier for millions of Indians who rely on foreign income.

1. Why Did the RBI Intervene in Cross-Border Payments?

To understand the magnitude of this change, we have to look at the numbers.

India is the undisputed global champion of inward remittances. According to recent data, India receives over $135 billion annually from the diaspora (heavily concentrated in the US, UK, Canada, Australia, and the GCC countries). These funds are not just pocket money; they are critical for managing the country’s macroeconomic external sector risks and driving local consumption demand. In fact, remittances into India consistently top actual Foreign Direct Investment (FDI).

However, the speed of this massive money engine was embarrassingly slow.

The RBI noted a glaring discrepancy: Currently, less than 8% to 10% of inward remittances in India are credited to beneficiary accounts within an hour. For comparison, in advanced economies like the United States, roughly 75% of similar cross-border payments are credited within an hour.

The RBI realized that in the era of instant domestic UPI transfers, keeping billions of dollars floating in “banking limbo” for days was highly inefficient and unfair to the consumer.

2. The New Rule: “Same Business Day” Credit

The centerpiece of the RBI’s April 2026 circular is the strict new timeline imposed on commercial banks.

The Rule: If your Indian bank receives a cross-border inward payment message during official foreign exchange (forex) market hours, they are now legally mandated to credit those funds into your local savings or current account on that exact same business day.

If the payment message arrives late at night (after forex market hours), the bank must process and credit the money first thing on the very next working day.

What This Means for You:

- Freelancers & MSMEs: You no longer have to build a 3-to-4 day “buffer” into your cash flow expectations. If your American client pays your invoice on Monday morning (US time), the funds should hit your Indian account by Tuesday (IST time), completely bypassing the old mid-week delays.

- Better Exchange Rates: Because the bank must process the transaction on the same day, you are less exposed to the risk of the Rupee fluctuating wildly over a three-day waiting period.

3. Fixing the Backend: The “Nostro Account” Problem

If you ever wondered why it took three days for a wire transfer to reach you, the answer lies in something called a Nostro Account.

A Nostro account is essentially an account that an Indian bank holds in a foreign country, denominated in that foreign currency (e.g., SBI holding an account in New York in US Dollars). When your relative in the US sends you money, the US bank deposits those Dollars into SBI’s Nostro account in New York. SBI then credits the equivalent Rupees to your local account in India.

The Old Problem:

The RBI observed that many Indian banks were incredibly lazy with this process. They relied on “end-of-day statements.” This meant SBI India would only check their New York Nostro account once a day (at the end of the day) to see what money had arrived. This manual, delayed checking caused massive bottlenecks.

The New RBI Solution:

The RBI has strictly advised banks that end-of-day reconciliation is no longer acceptable. Banks must now carry out reconciliation and confirmation of credits in their Nostro accounts on a near real-time basis, or at periodic intervals that absolutely do not exceed 30 to 60 minutes.

By forcing banks to check their foreign accounts every hour, the money is identified instantly, allowing it to be pushed down to the retail customer on the same day.

4. Immediate Customer Notifications (Ending the Guessing Game)

One of the most frustrating parts of receiving foreign money is the lack of communication. You know the sender initiated the transfer, but your Indian bank acts completely silent until the money suddenly drops into your account days later.

The RBI is putting an end to this information blackout.

Under the new directives, banks are required to notify customers immediately upon the receipt of a cross-border inward payment message via the SWIFT network (or equivalent systems).

- If the message hits the Indian bank at 2:00 PM, you should get an SMS or email by 2:05 PM saying, “We have received an inward remittance instruction for $1,000. It is currently being processed.”

- If the message arrives at 11:00 PM (after business hours), the bank must send you that notification at the very start of the next working day.

This simple SMS adds a massive layer of transparency. If the bank requires you to submit a Purpose Code declaration or a Foreign Inward Remittance Certificate (FIRC) request, you now know exactly when to log into your net banking portal to provide it, rather than waiting in the dark.

5. Implementation Timeline: When Does This Start?

As with any massive technological shift in the banking sector, it cannot happen overnight. Banks need time to upgrade their backend APIs, automate their Nostro reconciliation software, and deploy straight-through processing (STP) systems.

The RBI has laid out a dual timeline:

- The 6-Month Deadline: Banks have been given exactly six months from the date of the circular (meaning roughly October 2026) to fully implement the core technology required to guarantee the “same business day credit” rule.

- Immediate Effect: All other provisions—such as sending immediate SMS notifications to customers and improving transparency—come into effect immediately.

Conclusion: A Massive Win for the Indian Consumer

The Reserve Bank of India’s push to accelerate cross-border payments is a monumental upgrade to the country’s financial plumbing. As India’s global footprint expands—with more remote workers, massive IT service exports, and a thriving diaspora—the speed of money directly dictates the speed of economic growth.

By forcing banks to abandon their sluggish end-of-day checks and mandating same-day credits, the RBI is ensuring that the $135 billion flowing into the country actually reaches the pockets of the people without unnecessary corporate friction. For the millions of Indians who rely on these funds to pay medical bills, buy groceries, or scale their local businesses, the days of waiting anxiously for a foreign wire transfer are finally coming to an end.

Frequently Asked Questions (FAQs): RBI Inward Remittance Rules 2026

Q1: What is the new RBI rule for inward foreign remittances?

The RBI has mandated that Indian banks must credit cross-border inward payments to the beneficiary’s account on the exact same business day the payment is received, provided it arrives during foreign exchange market hours.

Q2: When will the “same-day credit” rule actually start working?

While the RBI issued the circular in April 2026, they have given commercial banks a six-month grace period to upgrade their backend technology. You can expect the strict same-day credit system to be fully operational by October 2026.

Q3: What happens if my foreign payment arrives after banking hours?

If the payment message hits your Indian bank after official forex market hours or on a public holiday, the bank is mandated to process and credit the funds to your account on the very next working day.

Q4: Why was my foreign money taking 3 to 4 days to arrive previously?

A major reason for the delay was that Indian banks relied on “end-of-day” statements to check their foreign Nostro accounts. They only reconciled the incoming foreign currency once a day, which created massive administrative bottlenecks before releasing the funds in Rupees to you.

Q5: How has the RBI fixed the Nostro account delay?

The RBI has directed banks to stop end-of-day checking. Banks must now reconcile their Nostro accounts in near real-time, or at intervals not exceeding 30 to 60 minutes, ensuring the money is identified and processed continuously throughout the day.

Q6: Will the bank inform me when the foreign money is on its way?

Yes. A major new rule requires banks to notify customers via SMS or email immediately the moment they receive the cross-border payment message from the foreign sending bank, ending the uncertainty of waiting.

Q7: Does this rule apply to freelance payments from clients abroad?

Yes, absolutely. Whether it is a business payment, freelance service income, or a family maintenance transfer from a relative abroad, all standard cross-border inward remittances fall under these new speed mandates.

Q8: Do I still need to provide a “Purpose Code” for same-day credit?

Yes. The speed of the transaction does not bypass FEMA regulations. You must still ensure that your inward remittance is tagged with the correct RBI Purpose Code (e.g., P0802 for software services) so the bank can process it without regulatory holds.

Q9: How much money does India receive in foreign remittances every year?

India is the largest receiver of remittances globally. According to 2025-2026 data, the country receives over $135 billion annually, largely driven by the diaspora in the US, UK, Canada, Australia, and the Middle East.

Q10: Are outward remittances (sending money from India to abroad) also getting faster?

While this specific April 2026 circular focuses heavily on inward remittances, it is part of the RBI’s broader Payments Vision 2025, which aims to make all cross-border transactions (both inward and outward) faster, cheaper, and more transparent over the coming years.