TL;DR: Key Takeaways on Women Borrowers in India

If you are short on time, here is the quick summary of how women are reshaping the Indian banking sector:

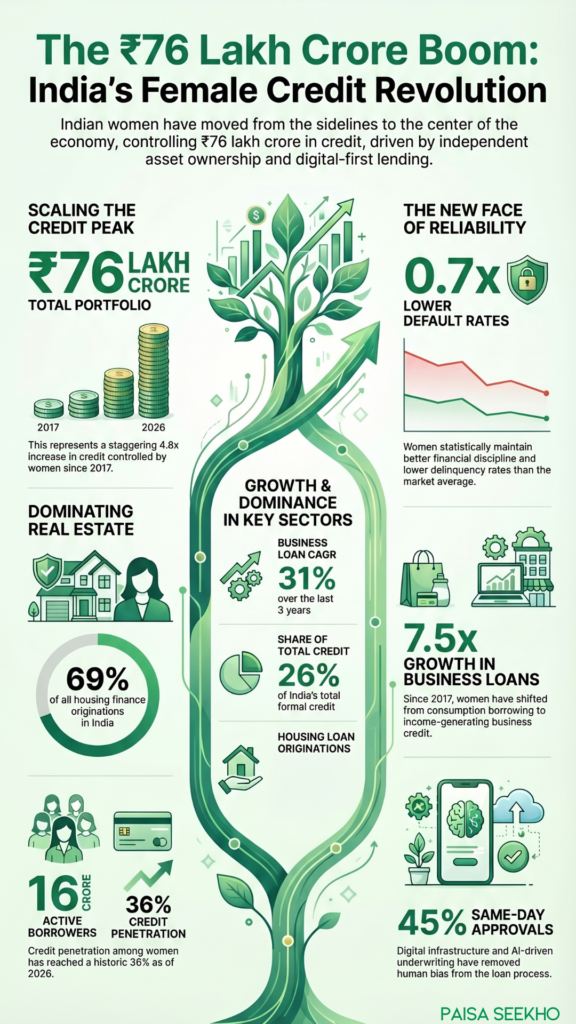

- Massive Growth: Women now control ₹76 lakh crore in credit, marking an incredible 4.8x increase since 2017.

- The Entrepreneurial Leap: Business-purpose loans for women have grown by 7.5x since 2017, proving a massive shift from consumption borrowing to income-generating business ownership.

- Dominating Real Estate: In a shocking twist, women now account for 69% of originations in housing finance, signaling a powerful push toward independent asset ownership.

- Better Financial Behavior: Banks love female borrowers because the data proves they are safer; women show a 0.7x lower default rate compared to the overall market average.

- Digital Acceleration: Faster, data-driven loan approvals (same-day approvals rose to 45% in 2025) have bypassed traditional biases, allowing 16 crore women to become actively credit-linked.

- The Untapped Market: Despite this massive success, nearly two-thirds of credit-eligible Indian women are still outside the formal system, leaving a massive runway for future growth.

Introduction

For decades, the image of an Indian borrower was almost exclusively male. Whether it was a father applying for a home loan, a husband buying a car, or a businessman securing working capital, women were often sidelined in the formal financial system—relegated either to joint-applicant status or informal microfinance groups.

But as we navigate through 2026, that outdated narrative has been completely shattered.

According to a groundbreaking new joint report released in April 2026 by TransUnion CIBIL, NITI Aayog, and MicroSave Consulting (MSC), women are no longer just participating in the Indian credit market; they are actively driving it. The data reveals a massive, structural shift: Indian women now hold a staggering credit portfolio of ₹76 lakh crore, representing 26% of the country’s total formal credit.

This is not just a story about numbers; it is a story of economic empowerment. Women are stepping out of the shadows of small microfinance loans and aggressively demanding business loans, housing finance, and retail credit to build their own independent empires.

In this comprehensive guide, we will decode this eye-opening 2026 report. We will explore why banks are actively chasing female borrowers, how digital apps have removed historic biases, and what this massive shift means for the future of the Indian economy.

What Does the 2026 CIBIL and NITI Aayog Report Reveal About Female Borrowers?

The joint report by TransUnion CIBIL, NITI Aayog, and MSC serves as the ultimate report card for India’s financial inclusion efforts over the last decade.

The headline number is jaw-dropping: 16 crore women are now actively borrowing in the formal credit system, pushing female credit penetration to a historic 36%. Between 2017 and 2025, women’s participation in formal credit grew at a Compounded Annual Growth Rate (CAGR) of 9%, vastly outpacing several traditional, male-dominated borrowing segments.

But the most important insight from the report is not the volume of the loans; it is the quality and depth of the borrowing.

Historically, when a woman borrowed money in India, it was usually through a rural Self-Help Group (SHG) or a microfinance institution just to buy a sewing machine or cover emergency household expenses. The 2026 data shows that this phase is over. Women are aggressively graduating into high-value retail and commercial credit, borrowing to buy personal cars, homes, and to scale up legitimate commercial enterprises.

Why Are Business Loans for Women Entrepreneurs Growing at a 31% CAGR?

One of the most exciting trends highlighted in the report is the explosion of the female entrepreneur.

For years, women who wanted to start a business faced heavy bias. Traditional bank managers often asked for their husband’s or father’s signatures as co-guarantors before approving a commercial loan. This restrictive environment forced millions of brilliant female entrepreneurs to rely on their own small savings.

The landscape has dramatically shifted. According to the data, business-purpose loan portfolios for women have grown 7.5x since 2017. Over the past three years alone, the number of women actually availing these business loans has surged at a massive 31% CAGR.

Why the sudden boom?

- Government Push: Schemes like Mudra Yojana and Stand-Up India specifically mandated banks to provide collateral-free working capital to women entrepreneurs.

- Cash-Flow Based Lending: As we discussed in our previous article on Small Finance Banks, modern lenders no longer demand heavy property as collateral. They look at digital GST receipts and UPI transactions. Because women run highly profitable digital boutiques, cloud kitchens, and service agencies, their strong cash flows easily qualify them for massive unsecured business loans.

- The Shift in Mindset: The data clearly proves a psychological shift from “consumption-led borrowing” (borrowing to buy a TV or a phone) to “income-generating credit demand” (borrowing to buy machinery or inventory to make more money).

How Is Digital Credit Access Changing the Home Loan Market for Women?

If there is one statistic in the CIBIL report that should make real estate developers sit up and take notice, it is this: Women now account for 69% of originations in housing finance.

This is a monumental shift in Indian wealth creation. Real estate has traditionally been a heavily male-owned asset class. Today, women are taking the lead in long-term financial planning and asset ownership.

The Role of Digital Infrastructure

How did so many women suddenly get approved for home loans? The answer is digital infrastructure.

In the past, visiting a physical bank branch, facing intimidating loan officers, and dealing with massive paperwork was a significant barrier for women.

Today, data-driven underwriting has digitized the process. According to the report, same-day loan approvals in consumption lending rose from 34% in 2022 to 45% in 2025. Because banks now use AI to analyze CIBIL scores and bank statements digitally, the human bias is completely removed from the approval process. If a woman has a good salary and a strong credit score, the computer approves the loan instantly, whether it is for a ₹50,000 personal loan or a ₹50 Lakh home loan.

The Financial Incentives

It is also worth noting that the government and banks actively incentivize women to buy property:

- Many state governments offer a 1% to 2% discount on stamp duty if a property is registered in a woman’s name.

- Most major banks offer a lower home loan interest rate (usually a 0.05% concession) for female co-applicants.

These mathematical benefits are pushing families to rightfully position women as the primary asset owners.

Do Women Borrowers Default Less Than Men?

If you ask any modern bank manager who their favorite type of customer is, the answer is almost universally a female borrower. The 2026 CIBIL report proves why mathematically.

Despite millions of women entering the credit market for the very first time (New-To-Credit women now account for 38% of retail originations), they maintain vastly superior financial discipline compared to men.

The report states that delinquency (default) rates among women are significantly lower. Women borrowers show a 0.7x default rate compared to overall credit originations. This means women are statistically much more likely to pay their EMIs on time, every single month, without bouncing cheques. This responsible credit behavior makes women highly profitable, low-risk customers for banks, which is why financial institutions are now launching aggressive marketing campaigns specifically targeting female professionals.

What is the Untapped Potential for Financial Inclusion in India?

While celebrating a ₹76 lakh crore milestone is important, the NITI Aayog and MSC report ends with a crucial reality check.

Despite having 16 crore active female borrowers, nearly two-thirds of credit-eligible women in India are still outside the formal credit system. Millions of women, especially in rural and semi-urban areas, are invisible to the credit bureaus.

To bring these women into the formal economy, the report emphasizes the need for the next phase of financial inclusion. This requires:

- Deeper Digital Engagement: Expanding the Business Correspondent (BC) network so rural women can access digital banking safely in their own villages.

- Financial Literacy: Teaching first-time earners how to build a CIBIL score so they don’t fall into the trap of predatory, unregulated loan apps.

- Product Innovation: Banks need to design specific loan products that cater to the unique lifecycle needs of women, supporting them as they transition from small micro-loans to higher-value commercial credit.

Conclusion: A Shift in Financial Power

The 2026 report by CIBIL and NITI Aayog is not just a collection of banking statistics; it is proof of a quiet revolution.

When women control ₹76 lakh crore of the credit market, they control the direction of the economy. They are building businesses, buying homes, educating their children, and proving to the financial sector that they are the most reliable borrowers in the country.

If you are a female professional or entrepreneur reading this, the data is entirely in your favor. Your clean credit history is a powerful asset. Do not hesitate to leverage the formal banking system to negotiate better interest rates, secure business capital, and build your own independent wealth in 2026 and beyond.

Frequently Asked Questions (FAQs): Women Borrowers in India 2026

Q1: How much of the total Indian credit market is currently driven by women?

According to the April 2026 report by CIBIL and NITI Aayog, women now hold a credit portfolio of ₹76 lakh crore, accounting for exactly 26% of the total formal system credit in India.

Q2: Are women still mostly borrowing from microfinance groups?

No. A massive shift has occurred. While microfinance was the starting point, women have aggressively transitioned into high-value retail loans (like car and personal loans) and commercial business loans.

Q3: What percentage of home loans are originated by women in 2026?

In a massive indicator of rising asset ownership, the report revealed that women now account for a staggering 69% of all originations in the housing finance sector.

Q4: Why are banks actively trying to lend more money to women?

Banks love female borrowers because they are statistically much safer. The report highlights that women borrowers have a 0.7x lower default rate compared to the overall market average, meaning they pay their EMIs on time much more consistently.

Q5: How fast are business loans for women entrepreneurs growing?

Business-purpose loan portfolios for women have exploded, growing 7.5x since 2017. Furthermore, the total number of women applying for these business loans has surged at a 31% CAGR over the last three years.

Q6: Are there any special benefits for a woman taking a home loan?

Yes. To encourage female asset ownership, most major Indian banks offer slightly lower home loan interest rates (typically 0.05% lower) for female applicants. Additionally, many states offer a 1% to 2% reduction in property stamp duty if the house is registered in a woman’s name.

Q7: How did digital infrastructure help female borrowers?

Digital infrastructure removed the human bias from lending. Because loan apps and banks use AI, UPI data, and digital CIBIL checks, women no longer face intimidation at physical branches. Same-day digital loan approvals rose to 45% in 2025, vastly improving access.

Q8: What is the current credit penetration rate among Indian women?

Credit penetration among women has risen to 36%, meaning there are currently 16 crore credit-active women operating within the formal Indian banking system.

Q9: What does it mean that women are shifting to “income-generating credit”?

It means women are borrowing money to make more money. Instead of taking a personal loan to buy a TV (consumption), they are taking business loans to buy inventory, sewing machines, or commercial ovens to build their businesses (income-generating).

Q10: Have all credit-eligible women in India received access to loans?

No. Despite the massive growth, the report warns that nearly two-thirds of credit-eligible Indian women remain outside the formal banking system, highlighting a massive opportunity for future financial inclusion and education.