TL;DR: Key Takeaways on Gifting Property to a Spouse

If you are planning to transfer a house deed to your partner tomorrow, here are the absolute must-know facts:

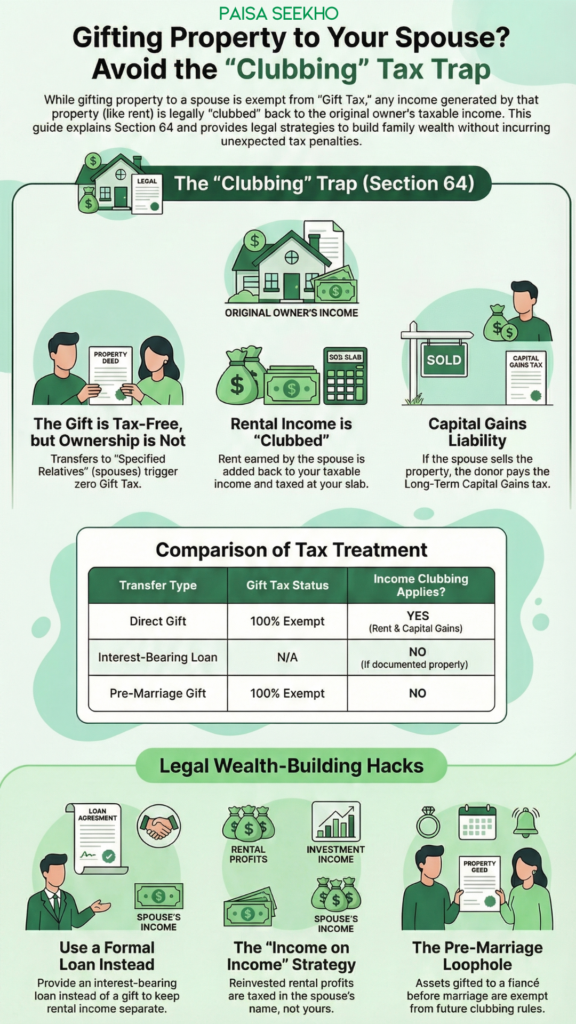

- The Gift is Tax-Free: Under Section 56, giving the property to your spouse does not trigger any “Gift Tax.” The transfer value is fully exempt.

- Stamp Duty Still Applies: While the income tax is zero, you still have to legally register a “Gift Deed” and pay state stamp duty (though many states offer massive discounts for spouses).

- The Clubbing Rule (Section 64): If your spouse earns rent from the gifted property, that rental income is “clubbed” (added back) to your taxable income. You pay the tax, not them.

- Selling the House (Capital Gains): If your spouse later sells the gifted property at a profit, the Long-Term Capital Gains (LTCG) tax is also clubbed and taxed in your hands.

- The “Income on Income” Hack: If your spouse takes the rental income and reinvests it (like putting it in an FD), the interest earned on that second investment is NOT clubbed. It is taxed as your spouse’s own income.

- Proper Reporting is Mandatory: The person who gifted the property must explicitly report the clubbed income in their Income Tax Return (ITR) to avoid severe penalties.

Introduction

Transferring a residential flat or a piece of land to your husband or wife is a beautiful gesture. Often, it is done out of pure love and a desire to provide financial security for the family. However, in many cases, it is also done as a secret strategy to save money.

If you are in the 30% tax bracket and your spouse is a homemaker with zero income, it seems mathematically brilliant to transfer a rental property into their name. You assume that the rental income will now be taxed at your spouse’s 0% tax slab, saving your family lakhs of rupees every year.

Unfortunately, the Income Tax Department is way ahead of you.

While the actual act of gifting the property is completely tax-free, the income generated by that property is a completely different story. Thanks to a strict set of rules known as the “Clubbing Provisions,” your brilliant tax-saving plan could quickly turn into an income tax nightmare if you don’t understand the law.

Under the newly streamlined Income Tax Act 2025, the rules around hiding wealth within your family remain as strict as ever. In this comprehensive guide, we are going to break down the complex web of income tax, property gifts to a spouse, clubbing provisions, and reporting. We will explain exactly who pays the tax, what happens if your spouse sells the house, and the legal tax hacks you can use to protect your wealth.

Why Gifting Property to Your Spouse is “Tax-Free” (But Not Really)

Let us start with the good news. The Indian tax code is very friendly when it comes to keeping wealth within the immediate family.

If a random friend gives you a gift worth more than ₹50,000, the entire amount is fully taxable as “Income from Other Sources.” However, the law provides a special exemption for “Specified Relatives.” Your spouse is at the top of this list.

If you transfer a ₹2 Crore apartment to your wife or husband without asking them for a single rupee in return, there is zero income tax on the transaction itself. ### The Stamp Duty Catch

However, just because the Income Tax Department doesn’t want a cut doesn’t mean the state government will let you walk away for free. To legally change ownership, you must draft and register a Gift Deed at the local sub-registrar’s office.

This requires paying stamp duty and registration charges. The good news is that many Indian states (like Maharashtra and Haryana) offer massive concessions on gift deed stamp duty for blood relatives and spouses. Instead of paying the standard 5% to 7%, you might only have to pay a flat fee or a microscopic 1% duty to execute the legal transfer.

2. What Is the Section 64 Clubbing of Income Rules?

Here is where the government closes the tax-evasion loophole.

The Income Tax Department knows that high-earning individuals will try to divert their income-generating assets to their non-working spouses to exploit the basic tax exemption limits (₹3 Lakhs to ₹4 Lakhs). To stop this, they enforce the Clubbing of Income rules under Section 64.

The rule is brutally simple: If you transfer an asset to your spouse without “adequate consideration” (meaning it was a free gift, not a market-rate sale), any income arising from that asset belongs to you for tax purposes.

The Rental Income Example

Let’s say Rahul is an IT engineer earning ₹25 Lakhs a year (placing him in the 30% tax bracket). He buys a commercial shop and gifts it to his wife, Priya, who is a homemaker with zero income.

Priya rents out the shop for ₹40,000 a month (₹4,80,000 a year).

- The Expectation: Rahul thinks Priya will file her own ITR, and because her income is ₹4.8 Lakhs (which is below the tax-free rebate limit), the family will pay zero tax on the rent.

- The Reality: Under Section 64, the Income Tax Department intercepts this. They take Priya’s ₹4.8 Lakh rental income and “club” it directly into Rahul’s ITR. Rahul’s taxable income becomes ₹29.8 Lakhs, and he is forced to pay a heavy 30% tax on the rental income.

Even though Priya is the legal owner of the shop and the rent goes into her bank account, Rahul carries the entire tax burden.

3. Does Capital Gains Tax on Gifted Property Also Get Clubbed?

Rent is a recurring income, but what happens if the spouse decides to sell the gifted property entirely?

Many people mistakenly believe that the clubbing provisions only apply to monthly cash flow like rent or FD interest. This is a very dangerous assumption. The clubbing rule applies to all income arising from the asset, including the profit made from selling it.

The Capital Gains Trap

Imagine you gifted a plot of land to your spouse in 2020. In 2026, your spouse sells the land and makes a massive Long-Term Capital Gain (LTCG) profit of ₹50 Lakhs.

Legally, your spouse signed the sale deed. The ₹50 Lakhs went into your spouse’s bank account. However, because the original asset was a gift from you, the entire ₹50 Lakh LTCG is clubbed into your income tax return. You, the original donor, will be legally responsible for paying the 12.5% LTCG tax on that ₹50 Lakh profit. If you fail to report this massive gain in your ITR, the tax department will hit you with severe concealment penalties.

4. How to Avoid Clubbing of Income: Legal Hacks and Exceptions

The clubbing rules seem terrifying, but they are not absolute. The tax code is built on logic, and there are completely legal, verified strategies to ensure the clubbing provisions do not trigger.

If you want to structure your family finances smartly, here are the best legal loopholes to avoid clubbing:

Hack 1: The “Income on Income” Principle (Accretion)

This is the most powerful wealth-building loophole in the Indian tax system.

The law states that the income from the gifted asset is clubbed. However, if your spouse takes that income and reinvests it, the second layer of income is NOT clubbed!

- Example: You gift your wife ₹10 Lakhs. She puts it in a Fixed Deposit (FD) and earns ₹70,000 in interest. That ₹70,000 is clubbed into your income.

- The Hack: Your wife takes that ₹70,000 profit and buys a mutual fund. A year later, that mutual fund generates ₹10,000 in profit. That ₹10,000 is strictly taxable in your wife’s hands. It is not clubbed with you! By continuously reinvesting the profits, your spouse can slowly build an independent, non-clubbed wealth portfolio.

Hack 2: Give a Loan, Not a Gift

If you want to help your spouse buy a property to earn rent, do not gift them the money. Instead, draft a formal, legal document and give them an interest-bearing loan.

Charge a reasonable interest rate (like 6% or 7%), ensure your spouse actually pays you that interest every year, and document the transactions via bank transfers. Because it is a formal loan and not a “gift without adequate consideration,” the property belongs entirely to your spouse, and the rental income will be taxed strictly in your spouse’s hands at their lower tax slab!

Hack 3: Pre-Marriage Gifts

The clubbing provision only applies if the relationship of “husband and wife” exists both at the time of the gift and at the time the income is generated. If you gift a house to your fiancé a month before you officially get married, the clubbing rules will never apply to that property, even after you tie the knot!

Hack 4: Gifts Under an Agreement to Live Apart

In the unfortunate event of a divorce or a formal legal separation, any property transferred to a spouse as alimony or maintenance (an agreement to live apart) is completely exempt from the clubbing rules. The separated spouse will pay taxes on their own income.

5. Reporting Clubbed Income in ITR 2026: Who Pays the Tax?

Understanding the math is only half the battle; filling out the paperwork correctly is what keeps you out of trouble with the taxman.

Under the streamlined Income Tax Act 2025, transparency is mandatory. You cannot simply ignore the transaction just because no actual money changed hands between you and your spouse.

For the Giver (The Donor):

Since you are the one bearing the tax liability, you must declare the clubbed income in your own ITR.

- When you log into the tax portal, you will use specific schedules designed for clubbing (traditionally known as Schedule SPI – Specified Persons Income).

- You must clearly mention your spouse’s PAN, the nature of the income (e.g., Income from House Property for rent, or Capital Gains for a property sale), and the exact amount being clubbed.

- TDS Benefit: If a tenant deducted TDS (Tax Deducted at Source) on the rent and deposited it against your spouse’s PAN, you are legally allowed to claim that TDS credit in your own ITR! You simply map the clubbed income to the corresponding TDS in your filing.

For the Receiver (The Donee):

Even though the spouse receiving the gift does not pay tax on the clubbed income, they should ideally still file an ITR if they have other investments. To avoid questions from assessing officers later, the receiving spouse can declare the rental income under the “Exempt Income” schedule, adding a note that the income has been successfully clubbed and taxed in the spouse’s ITR under Section 64.

Conclusion: Plan Before You Transfer

Gifting a house or a massive fixed deposit to your spouse is an incredibly generous act, but it is a terrible way to blindly avoid taxes.

The Income Tax Act is brilliantly designed to look right through superficial family transfers. The clubbing provisions of Section 64 ensure that if you are the economic source of the wealth, you remain the economic target of the tax.

Before you execute a gift deed or transfer massive amounts of money, take a step back. Analyze your family’s overall tax brackets. If your goal is purely to shift tax liability, consider giving your spouse a formal loan instead of a gift. And if you have already gifted property, ensure your CA accurately reports the clubbed rental income in your upcoming ITR. Proper planning today guarantees that your family’s golden gift doesn’t turn into a penalty notice tomorrow.

Frequently Asked Questions (FAQs): Income Tax on Spouse Property Gifts

Q1: Do I have to pay Gift Tax if my husband transfers a flat to my name?

No. Under the Indian Income Tax Act, any gift received from a “specified relative” (which includes a spouse) is 100% exempt from income tax, regardless of the property’s value.

Q2: What is the meaning of “Clubbing of Income”?

Clubbing of income is an anti-tax evasion rule. It states that if you transfer an income-generating asset (like a house or an FD) to your spouse for free, the income earned from that asset will be added back to your total income and taxed at your applicable slab rate.

Q3: If I gift an empty plot of land to my wife and it earns no income, is there any tax?

If the asset does not generate any income (no rent, no interest, and it is not sold), there is absolutely no income tax or clubbing provision to worry about. The clubbing rule only activates when the asset generates actual money.

Q4: My wife sold the house I gifted her five years ago. Who pays the Capital Gains tax?

You do. Under Section 64, the Long-Term Capital Gains (LTCG) profit generated from selling an asset that was gifted without adequate consideration is clubbed into the original donor’s taxable income.

Q5: How can I legally avoid the clubbing of income with my spouse?

The safest legal hack is to give your spouse a formal, documented, interest-bearing loan instead of a free gift. If your spouse uses that loan to buy a property and pays you regular interest, the rental income they earn will be taxed in their own hands, not yours.

Q6: What is the “Income on Income” exception?

If your spouse earns ₹1 Lakh rent from a gifted property (which gets clubbed to you), and they reinvest that ₹1 Lakh into the stock market and earn ₹10,000 profit, that secondary ₹10,000 profit is NOT clubbed. It is treated entirely as your spouse’s independent income.

Q7: Will my spouse’s professional salary be clubbed with my income?

No. Any income your spouse earns through their own technical or professional qualifications, manual skills, or independent employment is never clubbed. It is entirely their own taxable income.

Q8: Does the clubbing rule apply if I gift property to my children?

If you gift property to a minor child (under 18), the income is heavily clubbed with the parent who earns a higher salary. However, if you gift property to a major child (over 18), the clubbing provisions completely vanish! The major child pays tax on their own income.

Q9: Who pays the stamp duty when transferring property to a spouse?

The family must pay the stamp duty to legally register the Gift Deed. However, state governments regulate stamp duty, and many states offer massive concessions (sometimes charging as little as ₹1,000 or 1%) when transferring immovable property between a husband and wife.

Q10: Where do I report my spouse’s clubbed rental income in my 2026 ITR?

You must report it in your own Income Tax Return. The clubbed rent should be added under the “Income from House Property” schedule, and you must declare the details of the transfer and your spouse’s PAN in the “Specified Persons Income” (SPI) schedule of the ITR form.