If you are reading this, chances are you’ve just landed your first job, started a new business, or finally looked closely at your salary slip and wondered, “Where did a chunk of my hard-earned money go?” First things first: take a deep breath. Taxes can feel like a foreign language designed to confuse you, but at Paisaseekho, we believe that understanding your money shouldn’t require a finance degree. Whether you are working remotely from your hometown or have moved to a new city to chase your career, understanding income tax basics is your first step toward true financial independence.

In this comprehensive 2026 guide, we are going to break down everything you need to know about income tax in India. We will cover the new versus old tax regimes, how the latest Union Budget 2026 impacts your wallet, and how you can smartly, and legally, keep more of your own money. Let’s dive in.

1. What Exactly is Income Tax? (And Why Do We Pay It?)

At its core, Income Tax is a portion of your earnings that you pay to the Government of India. Think of it as a subscription fee for living in the country. The money collected from our taxes is used by the government to build national infrastructure (like highways and railways), fund public healthcare, maintain defense and security, and run welfare schemes.

Who Needs to Pay Income Tax?

If you are an Indian citizen, a Non-Resident Indian (NRI), or a business entity earning an income within India, you fall under the tax radar. However, not everyone has to pay tax. The government sets a “basic exemption limit.” If your annual income is below this limit, your tax liability is zero.

What Counts as “Income”?

Your income isn’t just the salary your employer deposits into your bank account. The Income Tax Department categorizes your earnings into five distinct “Heads of Income”:

- Income from Salary: Your monthly paycheck, bonuses, and allowances.

- Income from House Property: Rent received from a property you own.

- Profits and Gains from Business or Profession: Earnings if you run a startup, a shop, or work as a freelancer/consultant.

- Income from Capital Gains: Profits made from selling assets like mutual funds, stocks, real estate, or gold.

- Income from Other Sources: The “everything else” category, like interest earned on your savings account, fixed deposits (FDs), or even winning a lottery.

2. The Big Question: New Tax Regime vs. Old Tax Regime

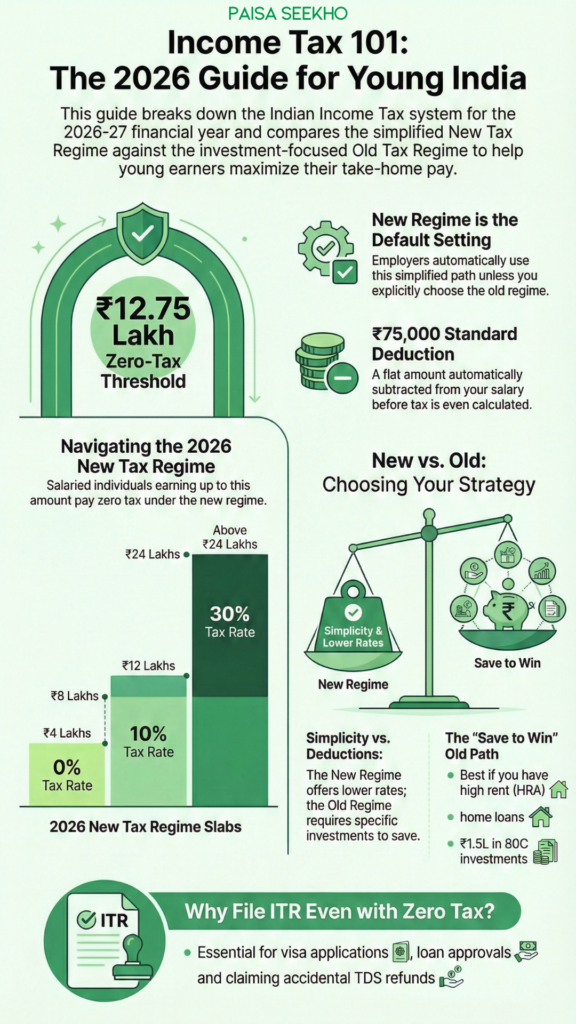

If there is one thing that confuses young earners the most, it’s this: “Should I pick the old regime or the new regime?” In recent years, the Indian government introduced a completely new way to calculate taxes. Following the Union Budget 2026, the New Tax Regime is the default option. If you don’t explicitly tell your employer otherwise, they will calculate your taxes based on the new regime.

Here is the simple difference between the two:

The Old Tax Regime: The “Save to Win” Path

The old regime encourages you to invest your money in specific government-approved schemes (like PPF, ELSS mutual funds, or life insurance). By investing, you can claim “deductions” and reduce the amount of your income that is eligible to be taxed.

- Best for: People who actively invest a large chunk of their salary, pay house rent (HRA), or have home loans.

- The catch: The tax rates (slabs) are higher, and you have to lock your money into specific investments to get the benefits.

The New Tax Regime: The “Keep It Simple” Path

The new regime was designed to make your life easier. It offers significantly lower tax rates, but in exchange, it strips away almost all the deductions and exemptions (you can’t claim your rent or your mutual fund investments to lower your tax).

- Best for: Young earners who are just starting out, want higher in-hand salary, and don’t want the pressure of forced investments.

- The magic number in 2026: Under the new regime, if your income is up to Rs. 12.75 Lakhs (after factoring in the Rs. 75,000 standard deduction), you effectively pay ZERO income tax due to government rebates.

3. 2026 Income Tax Slabs: Let’s Look at the Numbers

A “tax slab” simply means that your entire income isn’t taxed at one single rate. As your income increases, the extra money you earn falls into a higher bracket and gets taxed at a higher percentage.

Here is the breakdown of the New Tax Regime Slabs for the Financial Year 2026-27:

| Income Range | Tax Rate (New Regime) |

| Up to Rs. 4 Lakhs | 0% (Nil) |

| Rs. 4 Lakhs to Rs. 8 Lakhs | 5% |

| Rs. 8 Lakhs to Rs. 12 Lakhs | 10% |

| Rs. 12 Lakhs to Rs. 16 Lakhs | 15% |

| Rs. 16 Lakhs to Rs. 20 Lakhs | 20% |

| Rs. 20 Lakhs to Rs. 24 Lakhs | 25% |

| Above Rs. 24 Lakhs | 30% |

The “Zero Tax” Reality Check:

Looking at the table, you might think, “Wait, if I earn Rs. 10 Lakhs, do I have to pay 10%?” No! The government offers a special rebate under Section 87A for the new regime. Because of this rebate, if your total taxable income is up to Rs. 12 Lakhs, your tax becomes zero. Add the Rs. 75,000 standard deduction for salaried employees, and a salaried person earning up to Rs. 12,75,000 pays absolutely nothing in income tax.

4. The Tax Jargon Buster (Terms You Absolutely Must Know)

Before you sit down to plan your finances, you need to speak the language. Here are the most common terms simplified:

- Financial Year (FY) vs. Assessment Year (AY): * FY: The year you earn the money. It runs from April 1 to March 31. (e.g., FY 2026-27 is April 1, 2026, to March 31, 2027).

- AY: The year you file your returns and the government assesses your tax for the previous year. The AY is always the year immediately following the FY. (For FY 2026-27, the AY is 2027-28).

- Standard Deduction: A flat, blind deduction allowed to all salaried employees and pensioners. For 2026, this is Rs. 75,000 under the new regime. You don’t need to show any bills to claim this; it’s automatically subtracted from your salary before tax is calculated.

- TDS (Tax Deducted at Source): The government doesn’t want to wait until the end of the year to collect taxes. So, they ask your employer (or the bank) to deduct a small portion of tax before handing you your salary or interest. It’s like a pay-as-you-go tax system.

- Form 16: A certificate your employer gives you at the end of the financial year. It contains all the details of the salary paid to you and the TDS deducted. It is your holy grail for filing taxes.

- ITR (Income Tax Return): A formal form you submit to the Income Tax Department declaring your total income, deductions, and tax paid.

5. Old Regime Magic: How to Legally Save Tax

If you decide that the Old Tax Regime is better for you (usually if your salary is higher and you invest heavily), you need to know how to claim deductions. Deductions are legal ways to tell the government, “Hey, I spent my money on these good things, so please don’t tax me on this amount.”

Here are the heavy hitters:

Section 80C: The 1.5 Lakh Lifesaver

This is the most famous tax-saving section in India. You can claim up to Rs. 1.5 Lakhs as a deduction if you invest in:

- EPF (Employee Provident Fund): The portion of your salary that automatically goes into your PF.

- PPF (Public Provident Fund): A safe, long-term government savings scheme.

- ELSS (Equity Linked Savings Scheme): Mutual funds that invest in the stock market but have a 3-year lock-in period.

- Life Insurance Premiums.

- Principal repayment of your Home Loan.

Section 80D: Health is Wealth (and Tax-Free)

You can claim deductions on the premiums you pay for health insurance.

- Up to Rs. 25,000 for yourself, your spouse, and dependent children.

- An additional Rs. 25,000 to Rs. 50,000 if you buy health insurance for your parents (depending on their age).

HRA (House Rent Allowance)

If you live in a rented house and receive HRA as part of your salary components, you can claim a partial or full exemption on it. You will need to provide your landlord’s PAN card and rent receipts to your employer.

6. Which Regime Should You Choose in 2026? A Practical Guide

Choosing between the two regimes comes down to simple math.

Scenario A: The First Job (CTC: Rs. 4 Lakhs to Rs. 12 Lakhs)

If you are starting your career in a tier-2 or tier-3 city and earning anything up to Rs. 12.75 Lakhs, the New Tax Regime is a no-brainer. You will pay zero tax, you won’t have to lock up your limited disposable income in 15-year PPF accounts just to save tax, and you can focus on building an emergency fund and spending on your needs.

Scenario B: The Growing Career (CTC: Rs. 15 Lakhs+)

As your salary crosses the 13-15 lakh threshold, the math gets interesting. If you are paying a heavy rent (claiming high HRA), actively investing Rs. 1.5 Lakhs in Section 80C, paying health insurance premiums, and maybe paying off an education loan, the Old Regime might actually result in a lower tax outgo.

Paisaseekho Pro Tip: Always use an online income tax calculator. Enter your salary and your investments into both columns (Old vs. New) and see which one leaves you with more money. Choose that one!

7. Filing Your ITR: Why You Should Do It Even If You Owe Nothing

One of the biggest myths among young earners is: “My salary is below the taxable limit, so I don’t need to file an ITR.” Filing your Income Tax Return is crucial, and here is why:

- Claiming Refunds: Sometimes, your bank might deduct TDS on your fixed deposit interest, or an employer might deduct tax by mistake. The only way to get that money back from the government is by filing an ITR.

- Getting Loans and Credit Cards: When you apply for a car loan, home loan, or even a premium credit card, banks will ask for your last 2-3 years of ITR receipts as proof of stable income.

- Visa Applications: Planning to travel abroad? Embassies of countries like the US, UK, and the Schengen area often ask for your ITR history to process your visa.

- Carrying Forward Losses: If you dabbled in the stock market and made a loss, filing an ITR allows you to carry that loss forward to future years to offset future profits.

8. Common Income Tax Mistakes Young Earners Make

- Waiting until March to plan taxes: Tax planning should start in April. Scrambling in March usually leads to buying bad insurance policies just to save tax.

- Hiding freelance income: In today’s digital age, all your PAN card transactions are linked to the Annual Information Statement (AIS). The government knows about your side hustle. Declare it.

- Ignoring the AIS and TIS: Before filing your return, always download your Annual Information Statement from the income tax portal. It lists every major financial transaction you made that year. Ensure it matches your ITR.

- Not verifying the ITR: Your job isn’t done when you hit “Submit.” You must e-verify your return (usually via an OTP sent to your Aadhaar-linked mobile number) within 30 days, otherwise, your ITR is considered invalid.

Conclusion: Take Charge of Your Taxes

Let’s be honest: your first encounter with income tax can feel like you are being penalized for finally making your own money. But once you look past the confusing government jargon, taxes are just another part of adulting that you absolutely have the power to master.

Remember, tax planning isn’t just for the ultra-rich or seasoned finance bros. Whether you are earning Rs. 4 Lakhs at your first job in Indore or Rs. 15 Lakhs after a big promotion in Pune, understanding the basics ensures you never pay a single rupee more than you legally have to.

For 2026, the New Tax Regime is your default setting and often the best friend of young earners, giving you maximum in-hand salary without the pressure of forced investments. But don’t blindly accept it, always run the numbers. File your ITR on time, keep your Form 16 safe, and view tax planning as a tool to build your wealth, not deplete it. You’ve worked hard for your money; now it’s time to be smart about it.

Frequently Asked Questions

1. Do I need to file an ITR if my salary is below the taxable limit?

Yes, it is highly recommended! Even if your income is less than Rs. 3 Lakhs (the basic exemption limit under the new regime) or effectively tax-free up to Rs. 12.75 Lakhs, filing a “Nil Return” is a smart move. It serves as an official proof of income, which you will need when applying for a credit card, a home loan, or a visa to travel abroad.

2. What is the difference between Financial Year (FY) and Assessment Year (AY)?

Think of the Financial Year (FY) as the “Earning Year”, it runs from April 1 to March 31. The Assessment Year (AY) is the “Review Year” that immediately follows it. For example, the money you earn between April 1, 2025, and March 31, 2026, falls in FY 2025-26. You will evaluate and file taxes for this income in the following year, which makes the AY 2026-27.

3. Which ITR form should I fill out as a salaried employee?

If your primary source of income is your salary, you only own one house property, and your total income is below Rs. 50 Lakhs, you simply need to file ITR-1 (Sahaj). It is the most straightforward form. If you also earn from capital gains (like selling mutual funds or stocks), you will need to upgrade to ITR-2.

4. What is Form 16, and how do I get it?

Form 16 is essentially a report card of your salary and taxes, issued by your employer. It breaks down exactly how much you were paid and how much TDS (Tax Deducted at Source) your employer already submitted to the government on your behalf.

You don’t have to generate it; your HR or finance department must legally provide it to you, usually by mid-June every year.

5. Can I claim HRA or 80C deductions under the New Tax Regime in 2026?

No. The New Tax Regime was built to be simple. In exchange for much lower tax slab rates, the government removes almost all major deductions. You cannot claim HRA (House Rent Allowance), Section 80C (PPF, ELSS, Life Insurance), or Section 80D (Health Insurance) if you stick with the new regime.

6. Are there any deductions allowed in the New Tax Regime?

Yes, but very few! The most important one is the Standard Deduction of Rs. 75,000 for salaried employees. You don’t need to show any bills for this; it is a flat deduction applied automatically. You can also claim employer contributions to your NPS (National Pension System) account.

7. How do I get my income tax refund?

If your employer or bank deducted more TDS than your actual tax liability, the government owes you money! To get it back, you simply have to file your ITR online and declare all your income and investments. The Income Tax Department will calculate the excess amount and directly credit the refund into your pre-validated bank account.

8. What happens if I file my ITR after the deadline?

The usual deadline to file your ITR is July 31st. If you miss it, you can still file a “Belated Return” until December 31st, but it comes with a penalty. If your income is below Rs. 5 Lakhs, the late fee is Rs. 1,000. If your income is above Rs. 5 Lakhs, the penalty jumps to Rs. 5,000. Plus, you will have to pay extra interest on any tax you owe.

9. Is my side hustle or freelance income taxable?

Absolutely. Whether you are freelancing as a graphic designer, running a small Instagram thrift store, or consulting on the weekends, all of it is considered “Profits and Gains from Business or Profession.” It gets added to your total income and taxed according to your slab. Do not hide it, the government tracks your PAN card transactions!

10. How are my cryptocurrency and stock market profits taxed?

They are taxed differently.

- Stocks/Mutual Funds: Taxed as Capital Gains. If you hold equity for more than a year, it’s a Long-Term Capital Gain (LTCG) and taxed at 12.5% on profits over Rs. 1.25 Lakhs. If held for less than a year, it’s a Short-Term Capital Gain (STCG) taxed at 20%.

- Crypto: The government is strict here. Any profit you make from selling crypto or NFTs is taxed at a flat 30%, plus a 1% TDS on every transaction, regardless of which tax regime you choose.