Getting your first few real paychecks is an incredible feeling, until you look closely at your salary slip, spot that mysterious “TDS” deduction, and experience a mini-heartbreak. Suddenly, the salary you were promised isn’t the salary hitting your bank account.

If you are feeling frustrated, you are not alone. Taxes can feel like a heavy penalty for finally starting your career or growing your business. But here is the good news: you don’t have to part with all that money. Through income tax deductions, the government provides legal, structured ways for you to reduce your taxable income. Simply put, a deduction is a specific expense or investment that you subtract from your total gross income. The lower your taxable income, the less tax you have to pay.

Why Does the Government Let You Save Tax?

It might seem counterintuitive that the government would hand you a cheat code to pay them less. But income tax deductions are actually designed to nudge you toward good financial habits. The government wants you to save for retirement, buy health insurance so public hospitals aren’t overburdened, and invest in the country’s infrastructure through specific funds. When you do these things, they reward you by lowering your tax bill.

By the end of this guide, you will know exactly which of these rewards apply to your life, whether you are paying off a student loan, sending rent money to a landlord in Bangalore, or buying medical insurance for your parents back home.

Which is Better for Tax Saving in 2026: The Old Tax Regime or the New Tax Regime?

Before we dive into the giant list of tax-saving sections, we need to address the elephant in the room. Following the Union Budget 2026, the biggest source of confusion for young earners is figuring out which tax system to choose.

Here is the golden rule you must remember while reading this guide: almost all of the tax-saving investments and deductions we are about to discuss only apply if you choose the Old Tax Regime.

Why is the New Tax Regime the “Default” Now?

The government designed the New Tax Regime to make filing taxes incredibly simple and straightforward, and as of 2026, it remains the default setting. If you do not explicitly tell your HR department that you want the old regime, they will calculate your taxes using the new one.

The New Tax Regime offers significantly lower tax rates (slabs), and a flat Standard Deduction of Rs. 75,000 for salaried employees. Because of a special rebate, if your total salary is up to Rs. 12.75 Lakhs, you effectively pay zero income tax.

However, this simplicity comes at a cost. Under the new regime, you must surrender almost all other tax-saving tools. You cannot claim your rent (HRA), your life insurance premiums, or your mutual fund investments to lower your taxes.

Who Should Actually Choose the Old Tax Regime for Deductions?

If the new regime is so simple, why does the old one still exist? Because for many growing professionals, the old regime actually saves them more money.

You should strongly consider sticking to the Old Tax Regime and using the deductions in this guide if:

- Your annual CTC has crossed the Rs. 13 Lakh to Rs. 15 Lakh threshold.

- You pay a significant amount of house rent and receive House Rent Allowance (HRA) from your employer.

- You are aggressively investing your money in Provident Funds, ELSS mutual funds, or life insurance.

- You are paying off a heavy education loan or the EMIs for a home loan.

If your financial life involves these heavy expenses, the Old Tax Regime is your golden ticket to keeping more of your hard-earned wealth.

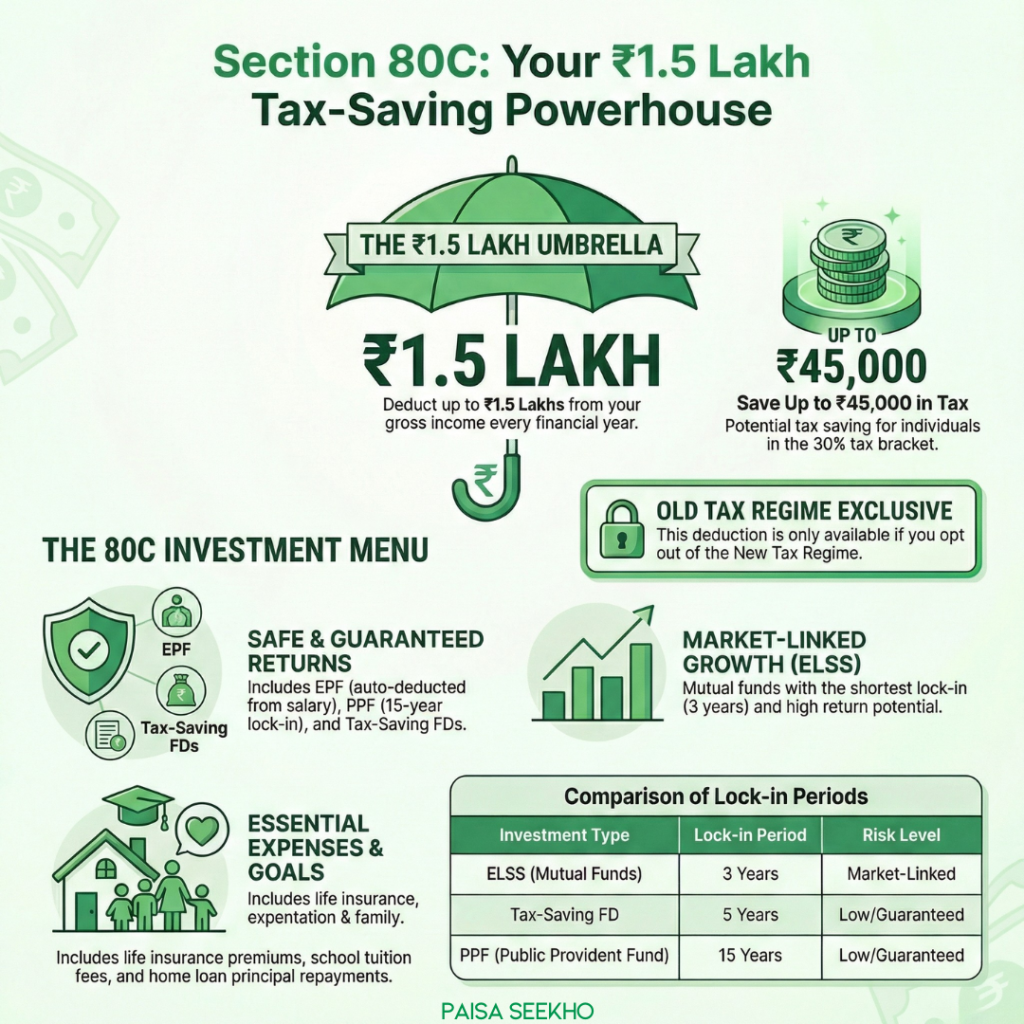

What is Section 80C and How Can It Save You Up to Rs. 1.5 Lakhs?

If the Income Tax Act were a movie, Section 80C would be the undeniable superstar. It is the most popular, most widely used tax-saving basket in India. Under the Old Tax Regime, Section 80C allows you to claim a maximum deduction of Rs. 1.5 Lakhs from your gross total income every single financial year.

To put that into perspective: if your income places you in the 30% tax bracket, fully utilizing this single section can save you over Rs. 45,000 in taxes alone!

Where Can You Invest for Section 80C Income Tax Deductions?

The beauty of Section 80C is its variety. You do not have to put all your money into one place. Here is how you can break down your options based on your risk appetite and your current life stage:

- The Safe Bets (Fixed Returns):

- EPF (Employee Provident Fund): The 12% of your basic salary that your employer deducts every month? That automatically counts toward your 1.5 Lakh limit!

- PPF (Public Provident Fund): A government-backed scheme with a 15-year lock-in period. It is entirely tax-free and perfect for long-term, risk-free wealth building.

- Tax-Saving FDs & NSC: 5-year Fixed Deposits and National Savings Certificates offer guaranteed returns, though the interest you earn is taxable.

- The Growth Play (Market-Linked):

- ELSS (Equity Linked Savings Scheme): These are mutual funds that invest directly in the stock market. They have the shortest lock-in period (just 3 years) of all 80C options and offer the highest potential returns to help you beat inflation.

- Life Essentials:

- Life Insurance Premiums: The premiums you pay for your term life insurance (or traditional endowment plans) for yourself, your spouse, or your children are fully deductible.

- Children’s Tuition Fees: Have kids? The tuition fees paid to any school, college, or university in India for up to two children qualify under this section.

- Home Goals:

- Home Loan Principal Repayment: If you are paying off a home loan, the portion of your EMI that goes toward the principal amount (not the interest) falls under this magical section.

Are There Any Section 80C Tax Saving Rules I Should Know?

Paisaseekho Pro-Tip: Do not panic-buy a random insurance policy in March just to save tax. First, look at your salary slip to calculate your annual EPF contribution. Subtract that from Rs. 1.5 Lakhs, and then consciously invest the remaining amount in instruments that actually align with your financial goals, like an ELSS fund to build wealth or a term plan to protect your family.

How Does Section 80D Protect Your Health and Wealth?

Medical emergencies do not just take a physical toll; they can wipe out years of hard-earned savings in a matter of days. With medical inflation in India consistently rising, having health insurance is no longer a luxury, it is a strict necessity.

To encourage you to protect yourself and your family, the government offers Section 80D. This section allows you to claim deductions on the premiums you pay for medical insurance, and it sits totally independent of your Rs. 1.5 Lakh 80C limit.

What Are the Section 80D Deduction Limits for Medical Insurance in 2026?

The amount you can claim depends entirely on who the policy covers and how old they are. Let’s break down the math for the Old Tax Regime:

- For Yourself & Your Nuclear Family: You can claim up to Rs. 25,000 for the premiums paid for yourself, your spouse, and dependent children.

- For Your Parents (Below 60 Years): You can claim an additional deduction of up to Rs. 25,000 if you pay the health insurance premiums for your parents.

- For Your Senior Citizen Parents (60+ Years): If your parents are senior citizens, this additional limit doubles to Rs. 50,000.

The Ultimate Scenario: If you (below 60) pay for your own family’s insurance and also pay the premiums for your senior citizen parents, your total allowable deduction under Section 80D jumps to a massive Rs. 75,000!

How Can You Claim the Hidden Rs. 5,000 Preventive Health Check-Up Deduction?

Here is a lesser-known benefit tucked inside Section 80D: the government allows a deduction of up to Rs. 5,000 for preventive health check-ups for you or your family.

Why is this a hidden gem? Because unlike insurance premiums, which must be paid digitally or via cheque to claim the tax benefit, you can claim this Rs. 5,000 deduction even if you paid for the lab tests in cash.

Important Note: This Rs. 5,000 is not extra money on top of your limits. It is included within your overall Rs. 25,000 or Rs. 50,000 limits. So, if your insurance premium for the year was Rs. 20,000, you can use the remaining Rs. 5,000 limit by getting a full-body preventive check-up and max out the bracket!

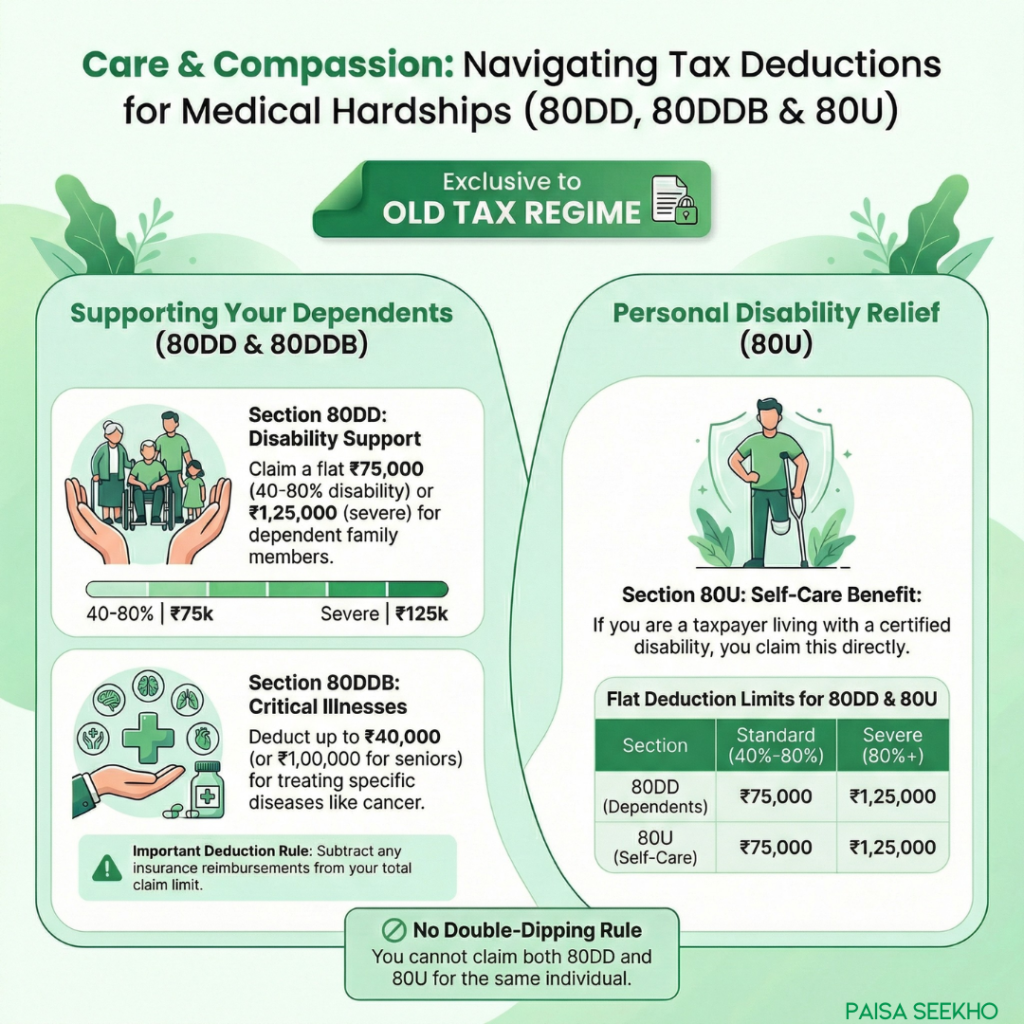

What Are the “Care & Compassion” Tax Deductions? (Sections 80DD, 80DDB & 80U)

At Paisaseekho, we know that life isn’t always a smooth ride. When a family member is diagnosed with a severe illness or lives with a disability, the emotional toll is heavy enough, you shouldn’t have to carry a crushing financial burden, too.

The government recognizes this. If you are financially supporting yourself or your dependents through medical hardships, there are three specific “care and compassion” sections under the Old Tax Regime that can provide significant tax relief.

How Does Section 80DD Help Families with Disabled Dependents?

If you are taking care of a dependent family member (spouse, child, parent, or sibling) who is differently-abled, you can claim a deduction under Section 80DD. This covers expenses for their medical treatment, training, rehabilitation, or even specific insurance premiums paid for their maintenance.

- The Benefit: You don’t need to submit every single pharmacy bill. The government offers a flat deduction based on the severity of the disability (which must be certified by a recognized medical authority).

- For 40% to 80% Disability: You can claim a flat deduction of Rs. 75,000 per year.

- For Severe Disability (80% or more): The deduction jumps to a flat Rs. 1,25,000 per year.

What is Section 80DDB and Which Specified Diseases Does It Cover?

While Section 80D covers your regular health insurance premiums, Section 80DDB is meant for the actual out-of-pocket medical expenses incurred for treating specific critical illnesses. This includes major battles like cancer, chronic renal failure, AIDS, and severe neurological diseases (like dementia or Parkinson’s).

- For Patients Below 60 Years: You can claim up to Rs. 40,000.

- For Senior Citizens (60+ Years): The limit is raised to Rs. 1,00,000.

- Important Note: If your health insurance already reimbursed a portion of the hospital bill, you must subtract that payout from your claim limit. You only get tax relief on the money that actually left your pocket.

Can You Claim Section 80U if You Live with a Disability?

Yes. While Section 80DD is for your dependents, Section 80U is designed for the taxpayer themselves. If you are a working professional living with a certified physical or mental disability, you can claim this deduction directly on your own Income Tax Return.

- The limits are identical to 80DD: a flat Rs. 75,000 for a standard disability and Rs. 1,25,000 for a severe disability.

- Rule to remember: You cannot claim both 80DD (from a family member claiming you as a dependent) and 80U (on your own tax return) at the same time.

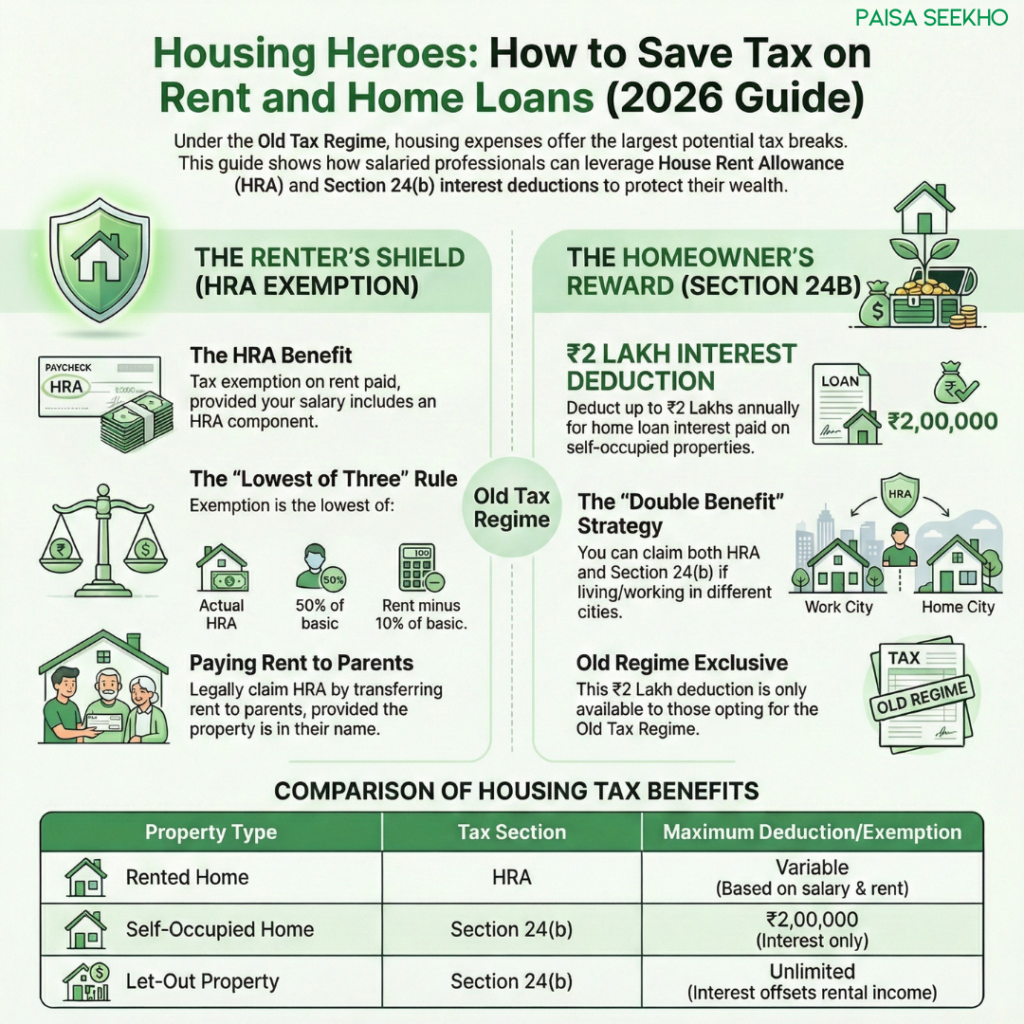

How Can “Housing Heroes” Save Tax on Rent and EMIs? (HRA & Section 24b)

Whether you have just moved to a booming tech hub for your first job or you are finally buying that dream apartment back in your hometown, housing takes up the biggest slice of your salary pie. Thankfully, under the Old Tax Regime, housing expenses also offer some of the largest tax breaks.

How Do You Claim HRA (House Rent Allowance) Exemption?

If you live in a rented house and your salary slip includes a component called “HRA,” you can claim a massive tax exemption on the rent you pay.

To claim this, you need to provide your employer with your rental agreement and monthly rent receipts. If your annual rent exceeds Rs. 1 Lakh, you will also legally need to submit your landlord’s PAN card.

- The Math: The actual exemption you get is calculated as the lowest of three figures:

- The actual HRA received from your employer.

- 50% of your basic salary (if living in a Metro city) or 40% (if in a Non-Metro city).

- The actual rent paid minus 10% of your basic salary.

- Paisaseekho Pro-Tip: Even if you pay rent to your parents (provided the house is registered in their name and you actually transfer the money to their bank account), you can legally claim HRA! Just make sure they declare that rent as income on their own ITR.

How Does Section 24(b) Reduce Tax for Home Buyers?

If you have taken a home loan to buy or construct a property, you get to claim tax benefits on two fronts. We already learned that the principal repayment falls under Section 80C.

But what about the massive interest you pay the bank every month? That is where Section 24(b) comes in.

- For a Self-Occupied Property: If you live in the house you bought, you can claim a deduction of up to Rs. 2 Lakhs on the home loan interest paid during the financial year.

- For a Let-Out Property: If you bought a house and rented it out to someone else, you can still use the interest paid to offset your rental income.

2026 Reality Check: Remember, under the New Tax Regime, the government no longer allows you to claim the Rs. 2 Lakh interest deduction for a self-occupied property. This is the number one reason why many young home buyers with heavy EMIs stick to the Old Tax Regime!

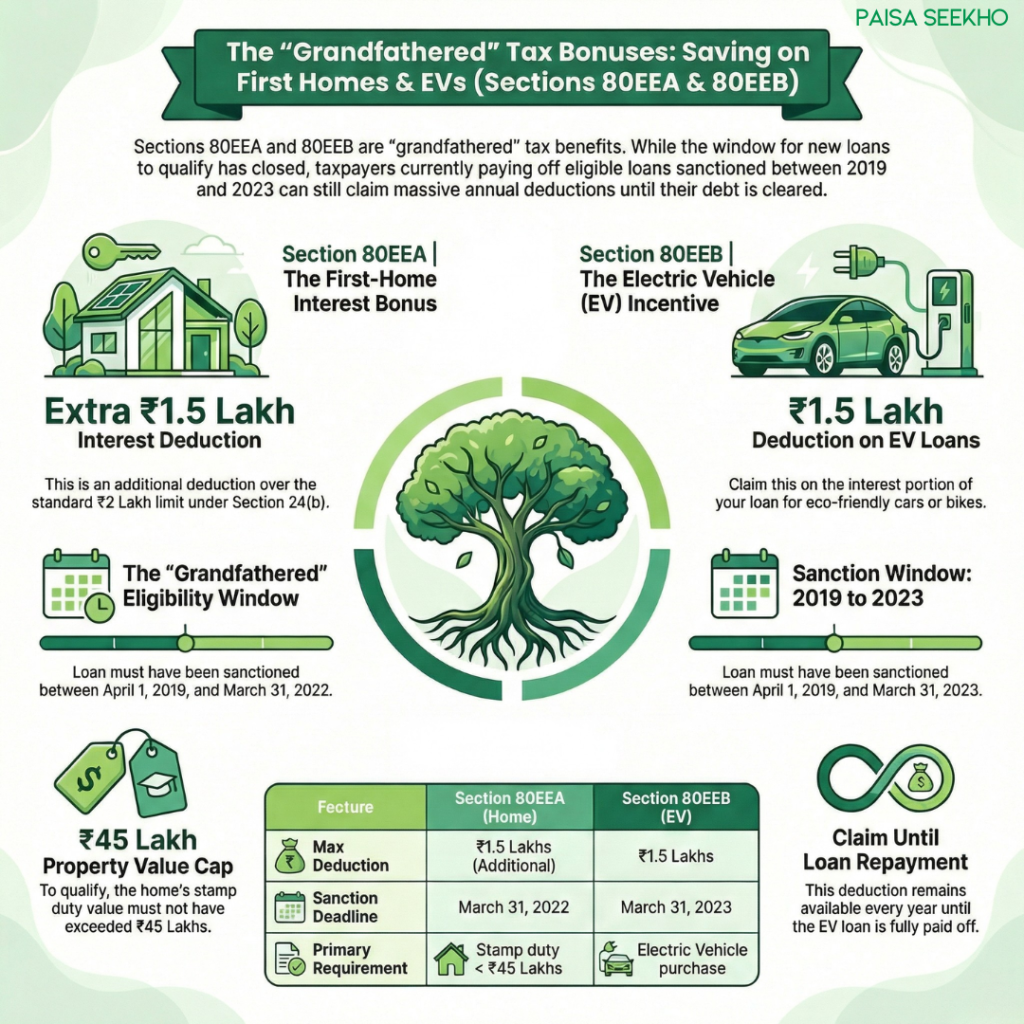

What Are the EV and First-Home Bonus Tax Deductions? (Sections 80EEA & 80EEB)

If you bought your first affordable home or joined the green revolution by buying an Electric Vehicle (EV) a few years ago, you might be sitting on a goldmine of tax deductions under the Old Tax Regime.

However, there is a massive catch you need to know for 2026: These sections are “grandfathered.” This means the government has closed the window for new loans to qualify. But if you already took the loan during the specified dates and are still paying the EMIs today, you can absolutely continue claiming these massive deductions until the loan is cleared!

How Does Section 80EEA Give Extra Tax Relief for Home Buyers?

We already know Section 24(b) gives you a Rs. 2 Lakh deduction on your home loan interest. But what if your interest payout is even higher? Enter Section 80EEA. This section was created to boost affordable housing and offers an additional deduction of up to Rs. 1.5 Lakhs on home loan interest.

- The Catch for 2026: To claim this today, your home loan must have been sanctioned between April 1, 2019, and March 31, 2022, and the stamp duty value of the house must not have exceeded Rs. 45 Lakhs.

- If you meet these criteria, you can combine Section 24(b) and 80EEA to claim a massive Rs. 3.5 Lakhs in total interest deductions!

Can I Still Claim Section 80EEB for My Electric Vehicle Loan?

Yes, if you meet the timeline! To encourage young Indians to buy eco-friendly cars and bikes, the government introduced Section 80EEB. It allows a deduction of up to Rs. 1.5 Lakhs on the interest paid on a loan taken to buy an Electric Vehicle.

- The Catch for 2026: Your EV loan must have been sanctioned between April 1, 2019, and March 31, 2023.

- If you bought your EV within this window, keep asking your bank for that annual interest certificate, because you can keep claiming this Rs. 1.5 Lakh deduction every year until your EV loan is fully paid off.

How Can Education and Retirement Tax Deductions Build Your Future? (Sections 80E & 80CCD)

Paying off a student loan while trying to save for the future can make you feel like your salary is disappearing before you even get to enjoy it. Thankfully, the Income Tax Act provides specific lifelines to help you manage education debts and build a retirement corpus.

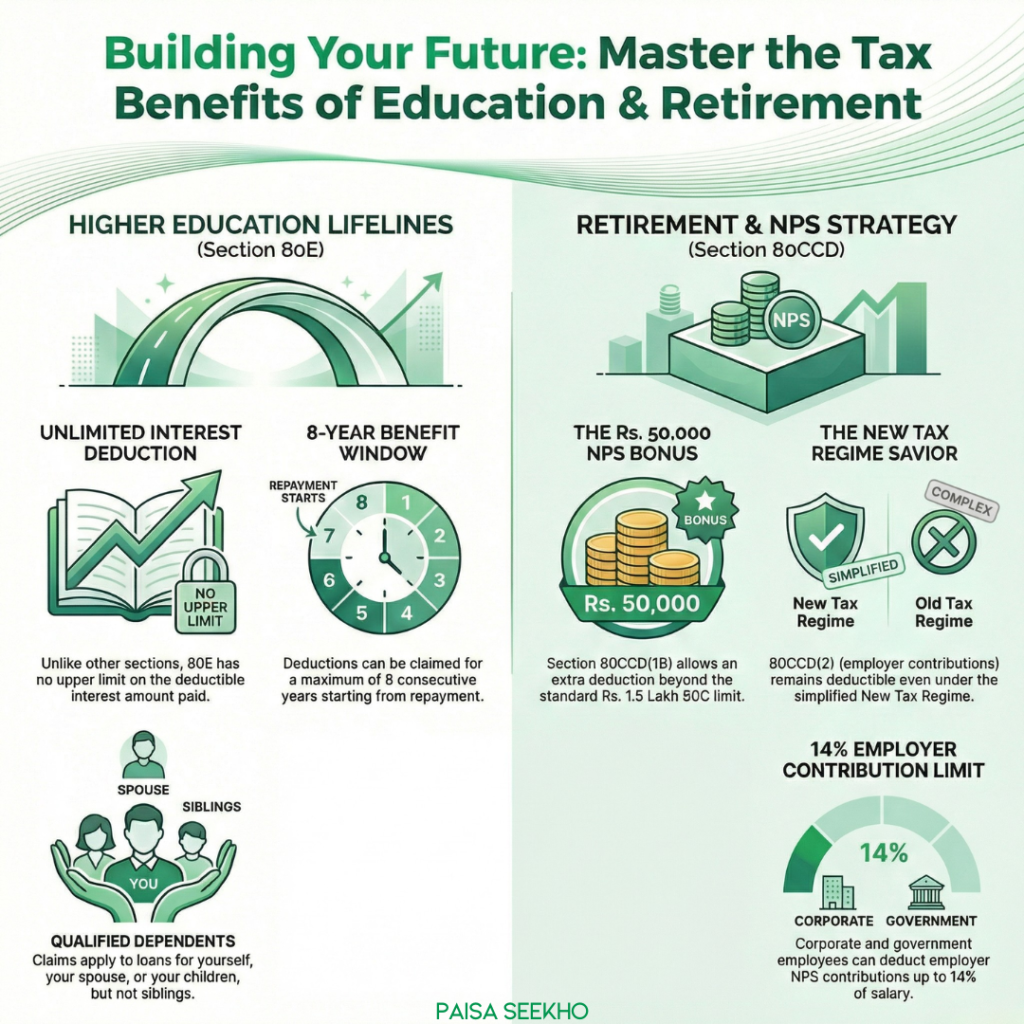

What is the Section 80E Income Tax Deduction Limit for Education Loans?

Here is a mind-blowing fact about Section 80E: it is one of the only sections in the entire Income Tax Act that has no upper limit.

If you have taken an education loan from a recognized bank for your own higher studies, or for your spouse or children, you can claim a deduction on the entire interest amount you pay during the financial year.

- The Rule: You can only claim the interest portion of your EMI, not the principal.

- The Timeline: You can claim this deduction for a maximum of 8 consecutive years, starting from the year you begin paying the interest.

- Remember: This unlimited deduction is only available if you opt for the Old Tax Regime!

How Does Section 80CCD Give You Extra NPS Tax Benefits?

The National Pension System (NPS) is a government-backed retirement scheme, and it comes with some of the best tax-saving cheat codes in the book. It is split into different parts, and understanding them is crucial:

1. Section 80CCD(1B): The Rs. 50,000 Bonus (Old Regime Only)

If you have already maxed out your Rs. 1.5 Lakh limit under Section 80C, you are not out of options. You can voluntarily invest an additional amount into an NPS Tier-1 account and claim an extra deduction of up to Rs. 50,000 under Section 80CCD(1B). This pushes your total investment-based tax-saving limit to Rs. 2 Lakhs!

2. Section 80CCD(2): The New Tax Regime Savior

This is perhaps the most important update for young earners in 2026. Section 80CCD(2) deals with the contribution your employer makes to your NPS account.

Following recent Budget updates, whether you are a government employee or work in the private corporate sector, employer contributions to your NPS are entirely tax-deductible up to 14% of your salary (Basic + DA).

Why is this a big deal?

Because unlike almost every other deduction we have discussed, Section 80CCD(2) is allowed under the New Tax Regime! If you want to stick to the lower tax slabs of the new regime but still want to save some tax, asking your HR to restructure your salary to include an employer NPS contribution is your smartest move.

How Do “Everyday Deductions” Like Sections 80TTA, 80G & 80GGC Save You Tax?

Not all tax deductions require you to lock your money away for 15 years or buy a house. Some of the easiest deductions under the Old Tax Regime come from your everyday banking and your willingness to give back to society.

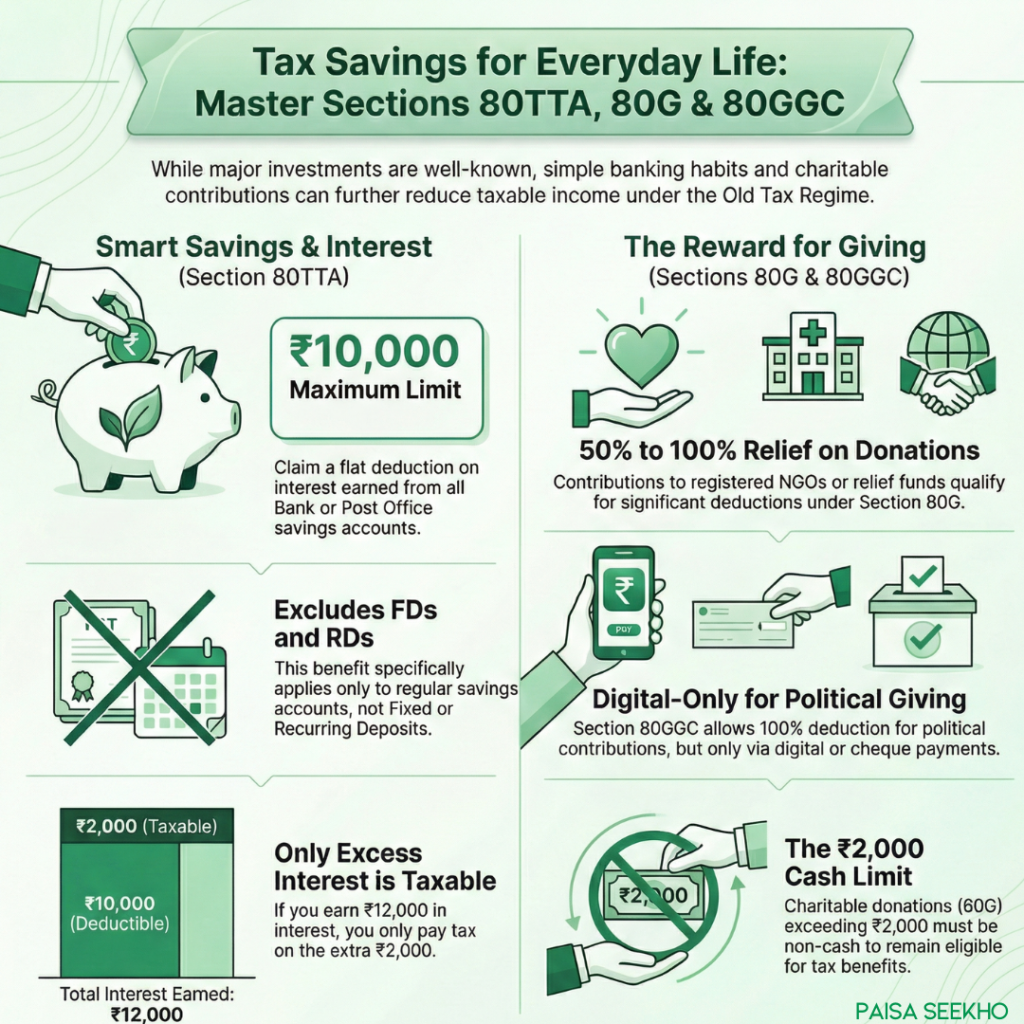

What is the Section 80TTA Limit for Savings Account Interest?

Every quarter, your bank credits a small amount of interest to your regular savings account. While this feels like free money, the Income Tax Department considers it “Income from Other Sources.”

Thankfully, Section 80TTA protects the little guy. It offers a flat deduction of up to Rs. 10,000 per year on the interest earned across all your savings accounts (Bank or Post Office). If you earn Rs. 8,000 in interest, it is completely tax-free. If you earn Rs. 12,000, you only pay tax on the extra Rs. 2,000. (Note: This does not apply to Fixed Deposits or Recurring Deposits).

How Can Section 80G Save Tax on Charitable Donations?

If you believe in giving back, the government rewards your philanthropy. Under Section 80G, donations made to specified relief funds (like the Prime Minister’s National Relief Fund) or registered charitable NGOs are eligible for tax deductions.

- Depending on the organization, you can claim either a 50% or 100% deduction on the donated amount.

- The Golden Rule: You cannot claim this deduction simply by transferring money. You must get a valid 80G receipt from the NGO, which includes their name, PAN, and registration number. Also, cash donations above Rs. 2,000 are not eligible for tax deductions.

What is Section 80GGC for Political Contributions?

If you want to financially support the democratic process, Section 80GGC allows you to claim a 100% deduction on contributions made to registered political parties or electoral trusts.

- The only catch? Absolutely no cash donations are allowed. You must use a cheque, demand draft, UPI, or net banking to claim this benefit.

Which Income Tax Deductions Actually Survive in the New Tax Regime in 2026?

We have covered a massive list of tax-saving cheat codes. But if you remember the golden rule from the beginning of this guide, almost all of them vanish if you choose the simplified New Tax Regime.

However, the New Regime is not completely stripped of benefits. If you opt for the default New Tax Regime in 2026, here are the strictly limited deductions you are still legally allowed to claim:

- The Standard Deduction (Rs. 75,000): This is a flat deduction automatically given to all salaried employees and pensioners. You do not need to show a single bill or receipt to claim it.

- Section 80CCD(2) (Employer’s NPS Contribution): As discussed earlier, if your employer contributes to your Tier-1 NPS account, you can claim a deduction of up to 14% of your salary (Basic + DA). This is the biggest tax-saving weapon available in the new regime.

- Family Pension Deduction: If you receive a family pension, you can claim a standard deduction of Rs. 25,000 or one-third of the pension amount, whichever is lower.

That’s it. No HRA, no 80C, no health insurance premiums.

How Do You Actually Claim These Tax Deductions? (The Paperwork Reality)

Reading about sections is one thing, but how do you actually get the government to acknowledge them so your HR doesn’t deduct massive TDS from your monthly paycheck?

Here is the real-world timeline every young professional needs to know:

- Step 1: The April Declaration (The Plan): At the start of the financial year (usually April), your employer will ask you for an “Investment Declaration.” This is just you promising the company that you intend to invest Rs. 1.5 Lakhs in 80C or pay Rs. 20,000 in health insurance. Your HR will use this promise to lower your monthly TDS deductions.

- Step 2: The January Proof Submission (The Reality Check): Around January or February, the HR department will come knocking for proof. This is when you must upload your actual PPF receipts, ELSS statements, rent agreements, and landlord’s PAN card to your company’s payroll portal. If you promised to invest but didn’t, your HR will deduct heavy taxes in February and March to make up the difference.

- Step 3: The July ITR Filing (The Backup Plan): What if you missed the HR deadline in January and they deducted excess tax? Do not panic. When you file your Income Tax Return (ITR) in July directly on the government portal, you can manually enter your deductions there and claim a tax refund!

Conclusion: Stop Panicking and Start Planning

Tax planning can feel like trying to solve a puzzle where the pieces keep changing. But by taking the time to understand these basic income tax deductions, you are taking active control of your financial future.

Whether you are happily accepting the zero-tax life of the New Tax Regime for a salary under Rs. 12.75 Lakhs, or you are meticulously calculating your HRA and 80C investments under the Old Tax Regime to protect your Rs. 15 Lakh package, the power is now in your hands. Do not wait until the last week of March to make panicked financial decisions. Invest in things that grow your wealth first, and let the tax savings be a happy byproduct.

FAQs

1. Which deductions are actually allowed under the New Tax Regime in 2026?

The New Tax Regime is designed to be deduction-free for simplicity, but there are a few exceptions. If you are a salaried employee, you get a flat Standard Deduction of Rs. 75,000 automatically. You can also claim your employer’s contribution to your NPS account under Section 80CCD(2) (up to 14% of your basic salary). Everything else, like 80C, HRA, and health insurance, is gone.

2. Can I pay rent to my parents and still claim HRA?

Yes, absolutely! This is a completely legal and smart way to save tax under the Old Regime. As long as the property is registered in your parents’ name and you actually transfer the rent money to their bank account every month, you can claim HRA. Just remember: your parents must declare this rent as their income when they file their own taxes.

3. Can I claim both HRA and a Home Loan deduction (Section 24b) at the same time?

Yes! It is very common for young professionals to buy a house in their hometown (paying an EMI) while living on rent in a different city for work (paying rent). Under the Old Tax Regime, the government allows you to claim both the HRA exemption for your rent and the Rs. 2 Lakh interest deduction for your home loan simultaneously.

4. What happens if I forget to submit my tax-saving proofs to HR on time?

First of all, don’t panic! If you miss the January/February deadline to submit your rent receipts or mutual fund statements to your HR, they will deduct higher TDS from your March salary. However, your money isn’t lost. You can claim all those missed deductions directly on the income tax portal when you file your ITR in July, and the government will send the excess tax back to you as a refund.

5. Are all mutual funds tax-free under Section 80C?

No! This is a very common mistake. Only a specific type of mutual fund called an ELSS (Equity Linked Savings Scheme) qualifies for the Rs. 1.5 Lakh deduction under Section 80C. Regular mutual funds or SIPs do not give you any tax breaks. Remember, ELSS funds also come with a mandatory 3-year lock-in period.

6. Do I need to attach my investment proofs (like LIC receipts) while filing my ITR?

No. The Income Tax Return (ITR) process is completely paperless. The online form never asks you to upload your premium receipts, rent agreements, or medical bills. You just have to declare the amounts. However, you must keep all these documents safely in a digital folder. If the tax department selects your profile for a random check later, you will need to produce them.

7. Can I claim an Education Loan deduction (Section 80E) for my sibling’s studies?

Unfortunately, no. While Section 80E offers an unlimited deduction on the interest paid for an education loan, it only applies if the loan was taken for yourself, your spouse, or your children. Loans taken for brothers, sisters, or other relatives do not qualify.

8. Can I switch between the Old and New Tax Regimes every year?

If you are a salaried employee with no business or freelance income, yes! You have the freedom to calculate your taxes under both regimes every single year and pick the one that saves you more money. However, if you have any income from a business or profession (even a side hustle), the rules are stricter, you only get to switch back to the old regime once in your lifetime.

9. What is the maximum tax I can save using Sections 80C, 80CCD(1B), and 80D together?

If you opt for the Old Tax Regime and strategically max out your investments, the savings are massive. You can combine Rs. 1.5 Lakhs (80C) + Rs. 50,000 (NPS under 80CCD1B) + Rs. 75,000 (Max 80D for yourself and senior citizen parents). That is a whopping Rs. 2.75 Lakhs wiped clean off your taxable income!

10. Does the Rs. 75,000 Standard Deduction require any proof or bills?

Nope! Whether you use the Old Regime (Rs. 50,000 standard deduction) or the New Regime (Rs. 75,000 standard deduction in 2026), this is a flat, blind deduction given to every salaried employee and pensioner. You don’t need to show a single petrol bill or medical receipt. Your employer automatically subtracts it from your gross salary.