TL;DR: The Key Takeaways

- The New Regime (Default): For FY 2025-26 (AY 2026-27), the New Tax Regime is the default. It offers a streamlined 6-slab structure: 0% up to Rs. 4 Lakhs, scaling up progressively to a maximum of 30% for income above Rs. 24 Lakhs.

- The Zero-Tax Magic Number: Thanks to the Rs. 75,000 Standard Deduction and the massive Rs. 60,000 tax rebate under Section 87A, salaried individuals earning up to Rs. 12.75 Lakhs pay absolutely zero income tax under the New Regime.

- The Progressive Tax Rule: You do not pay your highest tax slab percentage on your entire income. India uses a progressive system, meaning you only pay the higher percentage on the specific amount that falls within that specific bracket.

Note: All slab rates and rebates are updated as per the official Union Budget announcements for FY 2025-26 (AY 2026-27).

1. The “How Much Do I Actually Owe?” Panic

Let’s picture a scenario: You just crushed your performance review. Your manager calls you into the office and tells you that your salary is being bumped up to Rs. 16 Lakhs a year.

You should be thrilled! But instead of celebrating, you immediately pull out your phone, frantically Google “income tax slabs,” and see that Rs. 16 Lakhs puts you in the 20% tax bracket. The panic sets in. You do the quick mental math: “Wait, 20% of 16 Lakhs is Rs. 3.2 Lakhs! Is the government really going to steal three lakhs from me?”

At Paisaseekho, we see this exact panic every single appraisal season. Young professionals often turn down small freelance gigs or fear getting a raise because they think jumping into a higher tax bracket means they will bring home less money than before.

This happens because most of us fundamentally misunderstand how tax slabs work. Tax slabs sound intimidating, but they are just stepping stones. We are going to demystify the math, break down the exact 2026 Budget numbers, and show you why a raise is always a good thing. By the end of this guide, you will be able to calculate your exact tax liability on a paper napkin in under two minutes!

2. The Biggest Tax Myth: How Tax Slabs Actually Work

Before we throw a bunch of percentages at you, we need to kill the biggest financial myth in India.

The Myth: “If I earn Rs. 25 Lakhs, I fall into the 30% slab, which means the government takes 30% of my total income.”

The Reality: That is absolutely false. India uses a Progressive Taxation System. This means the government does not look at your income as one giant block; they look at it as a series of buckets.

Think of tax slabs as buckets placed in a row:

- The First Bucket (0%): You pour your first few lakhs of income into this bucket. The government taxes this bucket at 0%. It’s completely free.

- The Second Bucket (5%): Once the first bucket is full, the rest of your income spills into the second bucket. The government takes just 5% of whatever is inside this specific bucket.

- The Final Bucket (30%): You only pay 30% tax on the exact amount of money that spills over into the final, highest bucket—not on the money sitting safely in the earlier, lower-taxed buckets!

Let’s look at a quick example:

Imagine the 30% tax slab starts at Rs. 24 Lakhs, and you earn Rs. 25 Lakhs. You do not pay 30% on Rs. 25 Lakhs (which would be a brutal Rs. 7.5 Lakhs). Instead, your first 24 Lakhs are taxed at much lower percentages (0%, 5%, 10%, etc.). You only pay that scary 30% rate on the extra Rs. 1 Lakh that spilled over into the final bracket!

This is why moving into a higher tax bracket is nothing to fear. You will always take home more money when you get a raise.

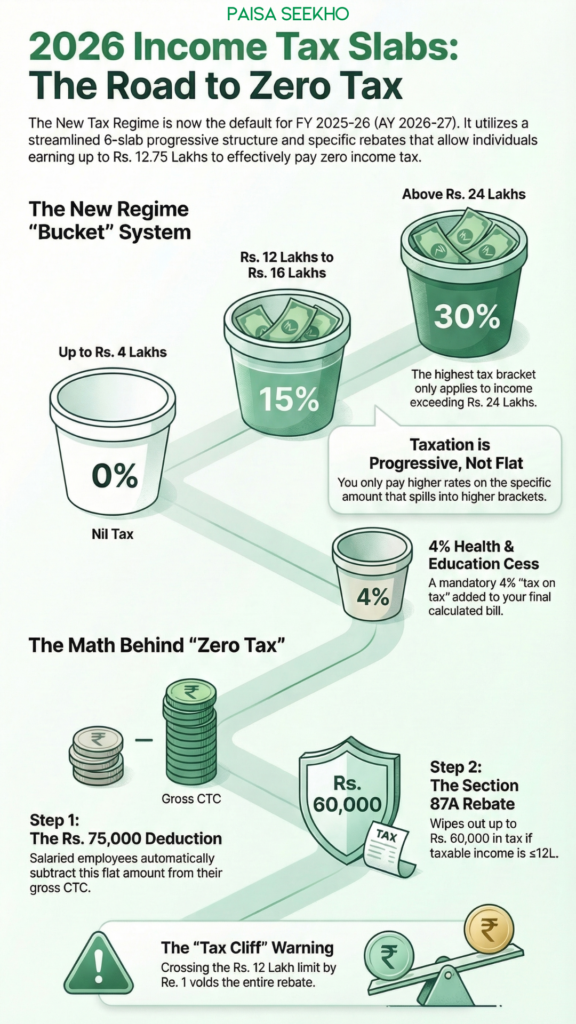

3. The New Tax Regime Slabs (The 2026 Default)

If you are filing your taxes for the current financial year (FY 2025-26), the government has officially made the New Tax Regime your default setting.

This regime was designed for ultimate simplicity. It strips away almost all the confusing paperwork and deductions (like Section 80C, HRA, and LTA) but replaces them with much lower, wider tax slabs.

Here is the exact 6-slab structure you need to know for 2026:

- Up to Rs. 4 Lakhs: 0% (Nil)

- Rs. 4 Lakhs to Rs. 8 Lakhs: 5%

- Rs. 8 Lakhs to Rs. 12 Lakhs: 10%

- Rs. 12 Lakhs to Rs. 16 Lakhs: 15%

- Rs. 16 Lakhs to Rs. 20 Lakhs: 20%

- Rs. 20 Lakhs to Rs. 24 Lakhs: 25%

- Above Rs. 24 Lakhs: 30%

If you look closely, you will see that the dreaded 30% tax rate does not even kick in until you cross a massive Rs. 24 Lakhs in annual income!

4. The Magic of Section 87A: How Rs. 12.75 Lakhs Becomes Tax-Free

Right now, you are probably looking at those slabs and thinking: “Wait a minute. The 0% bucket stops at Rs. 4 Lakhs. So how is everyone saying that I don’t have to pay tax if I earn over Rs. 12 Lakhs?”

This is where the magic of the Indian tax code comes in. The government uses two specific tools to completely wipe out the tax liability for middle-class earners:

1. The Rs. 75,000 Standard Deduction

If you are a salaried employee (or a pensioner), the government automatically gives you a flat discount on your income before calculating any tax. In the 2026 budget updates, this standard deduction is fixed at Rs. 75,000.

- Let’s say your CTC is exactly Rs. 12.75 Lakhs. You immediately subtract the Rs. 75,000 deduction.

- Your actual taxable income drops to exactly Rs. 12 Lakhs.

2. The Section 87A Rebate (The Ultimate Tax Saver)

Now, let’s run that remaining Rs. 12 Lakhs through the new tax slabs we just learned:

- Your first 4 Lakhs (0%) = Rs. 0

- Your next 4 Lakhs (5% of 4L) = Rs. 20,000

- Your final 4 Lakhs (10% of 4L) = Rs. 40,000

- Total Calculated Tax = Rs. 60,000

Does that mean you have to pay the government Rs. 60,000? No! Under Section 87A, the government promises that if your total taxable income is up to Rs. 12 Lakhs, they will give you a “rebate” (a full discount) on your calculated tax, up to a maximum of Rs. 60,000.

Because your calculated tax is exactly Rs. 60,000, the Section 87A rebate completely cancels it out. Your final payable tax becomes a beautiful, perfect ZERO.

The “Cliff” Warning

There is one massive catch to Section 87A. It is a strict “all or nothing” rule. If your taxable income crosses that Rs. 12 Lakh limit by even a single rupee (e.g., your taxable income is Rs. 12,00,001), the magical Rs. 60,000 rebate vanishes completely into thin air. You will instantly owe the full tax amount calculated across all the slabs.

This is exactly why tracking your annual bonuses and side-hustle income is so important before the financial year ends!

5. The Old Tax Regime Slabs (The Deduction Route)

If the New Tax Regime is the default for 2026, why would anyone still care about the Old Tax Regime?

Because the Old Regime is the ultimate playground for “Deduction Hunters.” If you are currently paying off a massive education loan, dropping heavy rent in a metro city (HRA), and maxing out your Rs. 1.5 Lakh Section 80C investments, the Old Regime might still save you more money.

However, because you get to claim all those juicy deductions, the government charges you much higher tax percentages early on.

Here are the classic Old Tax Regime slabs (for individuals under 60 years of age):

- Up to Rs. 2.5 Lakhs: 0% (Nil)

- Rs. 2.5 Lakhs to Rs. 5 Lakhs: 5%

- Rs. 5 Lakhs to Rs. 10 Lakhs: 20%

- Above Rs. 10 Lakhs: 30%

Notice the massive jump? The moment your taxable income crosses Rs. 5 Lakhs, you are immediately thrown into the heavy 20% tax bucket!

Paisaseekho Pro-Tip: The magical Section 87A rebate we just talked about works differently here. Under the Old Regime, the rebate only protects you if your taxable income is up to Rs. 5 Lakhs. If you earn exactly 5 Lakhs, the government forgives your Rs. 12,500 tax bill. If you earn Rs. 5,00,001, you owe the full amount!

6. What is Surcharge & Cess: The Hidden “Tax on Tax”?

You have calculated your income, filled your tax buckets, and arrived at your final tax number. You are done, right?

Not quite. The Income Tax Department always has a little extra surprise waiting for you at the checkout counter. Before you pay your bill, you have to add the Cess and, if you are earning the big bucks, a Surcharge.

The 4% Health & Education Cess (For Everyone)

No matter who you are, what regime you choose, or how much you earn, the government adds a mandatory 4% “Cess” to your final tax bill.

- The Math: This 4% is calculated on your tax amount, not your total income!

- If your calculated tax is Rs. 1,00,000, the 4% Cess adds Rs. 4,000 to your bill. Your final payable amount is Rs. 1,04,000.

- The government uses this specific pool of money purely to fund public health and education initiatives across India.

The High-Earner Surcharge (The “Rich Tax”)

If your career takes off and you start earning a massive salary, the government asks you to contribute a little more to the nation’s growth. A Surcharge is literally a “tax on your tax.”

- This extra fee only kicks in once your taxable income crosses Rs. 50 Lakhs in a single financial year.

- It starts at a 10% surcharge for income between Rs. 50 Lakhs and Rs. 1 Crore, and scales all the way up depending on how many crores you make.

- Good News for 2026: If you opt for the New Tax Regime, the government recently capped the maximum possible surcharge at 25% (down from a punishing 37% in the Old Regime), bringing the highest effective tax rate down significantly for top-tier founders and executives.

7. Let’s Do The Math (Real-World Scenarios)

Theory is great, but let’s see how these buckets actually work in real life. We are going to calculate the tax for two different Paisaseekho readers using the New Tax Regime for 2026.

Grab a paper napkin and follow along!

Scenario A: The Freelance Designer (Tax = Zero)

Meet Aisha. She is a freelance UI/UX designer who made exactly Rs. 10 Lakhs this year. Because she is a freelancer, she does not get the Rs. 75,000 standard deduction that salaried employees get, so her taxable income remains Rs. 10 Lakhs.

Let’s fill her tax buckets:

- Bucket 1 (0 to Rs. 4 Lakhs): The first 4 Lakhs are taxed at 0%. (Tax = Rs. 0)

- Bucket 2 (Rs. 4 Lakhs to Rs. 8 Lakhs): The next 4 Lakhs spill into the 5% bucket. 5% of 4 Lakhs is Rs. 20,000. (Tax = Rs. 20,000)

- Bucket 3 (Rs. 8 Lakhs to Rs. 12 Lakhs): She only has 2 Lakhs left (from 8L to 10L) to spill into this 10% bucket. 10% of 2 Lakhs is Rs. 20,000. (Tax = Rs. 20,000)

Total Calculated Tax: Rs. 40,000. Wait, does she pay this? No! Because her total income is under the Rs. 12 Lakh limit, Section 87A steps in and gives her a full rebate. Her final tax bill is wiped out to Rs. 0.

Scenario B: The Salaried Techie (The Progressive Effect)

Meet Rahul. He is a mid-level software engineer with a CTC of Rs. 18 Lakhs. Since he is salaried, he immediately gets the flat Rs. 75,000 Standard Deduction.

- His actual Taxable Income drops to: Rs. 17,25,000.

Since Rs. 17.25 Lakhs is higher than the Rs. 12 Lakh limit, he loses the Section 87A rebate and has to pay tax. Let’s fill his buckets:

- Bucket 1 (0 to 4L at 0%): Rs. 0

- Bucket 2 (4L to 8L at 5%): Rs. 20,000

- Bucket 3 (8L to 12L at 10%): Rs. 40,000

- Bucket 4 (12L to 16L at 15%): Rs. 60,000

- Bucket 5 (16L to 20L at 20%): He only has Rs. 1.25 Lakhs spilling into this bucket (from 16L up to 17.25L). 20% of 1.25 Lakhs is Rs. 25,000.

Total Calculated Tax: Rs. 0 + 20,000 + 40,000 + 60,000 + 25,000 = Rs. 1,45,000. Now, we add the mandatory 4% Health & Education Cess (4% of 1,45,000 = Rs. 5,800).

Rahul’s Final Tax Payable: Rs. 1,50,800.

The Big Takeaway: Even though Rahul earns enough to reach the 20% tax bracket, the government didn’t take 20% of his entire Rs. 17.25 Lakh income (which would have been a terrifying Rs. 3.45 Lakhs). Because of the progressive buckets, his effective tax rate is actually less than 9% of his total salary!

8. Conclusion: Don’t Let the Math Intimidate You

We started this guide with the panic of getting a raise and jumping into a higher tax slab. Hopefully, you now see exactly why that fear is completely irrational.

The Indian tax slab system is explicitly designed to be fair. It taxes you absolutely nothing when you are just starting out and trying to find your financial footing, and it only asks for a higher percentage on the specific extra money you make once you can truly afford it.

Do not let the complex percentages or the fear of the Income Tax Department dictate your career choices. A higher salary or a bigger freelance project will always result in more money hitting your bank account at the end of the month, regardless of the tax bracket it pushes you into.

Your Next Step: Stop relying on blind calculations from HR. Pull out your latest salary slip right now. Subtract your Rs. 75,000 standard deduction, take your remaining income, and literally draw out the buckets on a piece of paper. Figure out exactly which bracket your final rupee lands in. Once you see the math with your own eyes, you take back complete control of your paycheck!

Top 10 Frequently Asked Questions (People Also Ask)

1. What is the basic exemption limit for income tax in 2026?

Under the default New Tax Regime for FY 2025-26, the basic exemption limit (the amount on which you pay 0% tax) is Rs. 4 Lakhs. Under the Old Tax Regime, the basic exemption limit remains Rs. 2.5 Lakhs for individuals under the age of 60.

2. Is a salary of Rs. 12 Lakhs tax-free in 2026?

Yes! Thanks to the expanded Section 87A rebate in the New Tax Regime, if your taxable income is exactly Rs. 12 Lakhs or less, the government gives you a full tax rebate (up to Rs. 60,000). For salaried employees who get the Rs. 75,000 standard deduction, this means a gross salary of up to Rs. 12.75 Lakhs is effectively tax-free.

3. What happens if my salary crosses Rs. 12 Lakhs by just a little bit?

This is known as the “tax cliff.” The Section 87A rebate is strictly for taxable incomes up to Rs. 12 Lakhs. If your taxable income becomes Rs. 12,00,010, the entire rebate vanishes, and you will have to pay the standard tax calculated across the slabs (which would be around Rs. 60,000+). Always track your side income and bonuses carefully!

4. Who can claim the Rs. 75,000 Standard Deduction?

The standard deduction is exclusively available to salaried employees and pensioners. If your income comes entirely from freelance work, a business, or capital gains, you cannot claim this Rs. 75,000 flat discount on your taxes.

5. Do I pay 30% tax on my entire salary if I earn Rs. 25 Lakhs?

Absolutely not. India uses a progressive tax system. You only pay 30% on the portion of your income that strictly exceeds the Rs. 24 Lakh threshold. Your first 24 Lakhs are taxed progressively at much lower rates (0%, 5%, 10%, 15%, 20%, and 25%).

6. Can I still choose the Old Tax Regime in 2026?

Yes, you can. While the New Tax Regime is the default, you can actively choose to switch to the Old Tax Regime if you have significant tax-saving investments (like PPF or ELSS under Section 80C) or heavy deductions like House Rent Allowance (HRA) and home loan interest.

7. What is the Health and Education Cess?

The Health and Education Cess is a mandatory 4% extra charge added to your final calculated income tax. It is not calculated on your total income, but on the tax amount itself. The government uses these funds specifically for nationwide health and education programs.

8. Are the tax slabs different for senior citizens?

Yes, but only under the Old Tax Regime. Senior citizens (60 to 80 years) get a higher basic exemption limit of Rs. 3 Lakhs, and super senior citizens (above 80 years) get an exemption up to Rs. 5 Lakhs. Under the New Tax Regime, the slabs are exactly the same for everyone, regardless of age.

9. What is a Surcharge, and do I have to pay it?

A surcharge is essentially a “tax on your tax” for high-income earners. You only need to worry about it if your total taxable income crosses Rs. 50 Lakhs in a single financial year. If you earn under that, your surcharge is zero.

10. How do I switch my tax regime?

If you are a salaried employee, you can declare your preferred regime to your HR department at the start of the financial year (in April) so they deduct the correct TDS. You also get a final chance to switch regimes when actually filing your Income Tax Return (ITR) in July.