Do you remember the day you got your first job offer? You saw the “Rs. 6 Lakhs CTC” printed on the letter, immediately did the quick mental math, “Okay, 6 Lakhs divided by 12 means I get Rs. 50,000 every month!”, and started planning how you would spend it.

Then, payday arrives. You check your bank account, and instead of Rs. 50,000, you see a credit message for Rs. 44,000. Your heart sinks. You furiously check your salary slip and spot a mysterious deduction labeled “TDS.”

If you felt a mild sense of betrayal in that moment, welcome to the club! Almost every young professional in India goes through this exact same financial rite of passage. At first glance, TDS feels like a penalty or a hidden fee that HR forgot to warn you about. But at Paisaseekho, we are here to tell you that it is neither of those things.

By the end of this guide, you will understand exactly why that money was deducted, how you can track every single rupee of it, and most importantly, how to legally claim it back if the government took more than they should have. Let’s solve the mystery.

What is TDS and Why Does the Government Deduct It?

TDS stands for Tax Deducted at Source.

Instead of waiting for you to collect your entire salary (or freelance fee) over 12 months and then asking you to pay a massive lump sum of income tax at the end of the year, the government uses a “pay-as-you-go” system. They instruct the person paying you, whether that is your employer, your freelance client, or your bank, to deduct a small percentage of tax before the money ever reaches your hands.

That deducted money is then directly deposited to the Income Tax Department under your PAN card number.

Why Does the Income Tax Department Love TDS?

There are two very practical reasons why the government relies heavily on the TDS system:

- To Prevent Tax Evasion: In the past, people would earn money in cash or through bank transfers and simply “forget” to declare it when filing their taxes. By catching the tax at the very source of the income, the government ensures nobody skips out on their responsibilities.

- To Keep the Country Running: The government needs money every single day to build highways, fund public hospitals, and pay salaries to the defense forces. If everyone only paid their taxes once a year in July, the country would run out of funds by October. TDS ensures the government has a steady, monthly stream of revenue.

Is TDS an Extra Tax on Top of My Income Tax?

This is the biggest myth among young earners! No, TDS is not an extra tax.

Here is the mindset shift you need to make right now: TDS is simply you paying your standard income tax in advance. Think of it as a digital locker managed by the government. Every time TDS is deducted from your paycheck, that money goes into your specific locker.

At the end of the financial year, when you finally calculate your total tax liability under the 2026 tax slabs, you can tell the government, “Hey, look at my locker. I already paid you this much via TDS.” If the money in your locker is more than the tax you actually owe, the government gives you the extra money back.

It is not lost money; it is your money.

Here are the next two sections of your guide. I have made sure to highlight the brand-new TDS threshold changes that recently came into effect for 2026 so your readers have the most up-to-date and accurate financial information available!

The Big Three: How TDS Works on Your Salary, Freelance Gigs, and FDs

As a young adult, you don’t need to memorize the entire Income Tax Act. However, you will constantly bump into three specific sections of the law. Understanding these “Big Three” will help you predict exactly how much money will hit your bank account every month.

1. TDS on Salary (Section 192)

If you are a full-time employee, your HR department is responsible for deducting your TDS under Section 192. Unlike other sections that have a fixed percentage (like 10%), TDS on salary is calculated based on your specific income tax slab.

At the start of the financial year (in April), your employer will ask you to choose between the Old and New Tax Regimes and declare your planned investments. They will then estimate your total annual tax liability and divide it by 12. That exact amount is deducted from your paycheck every month.

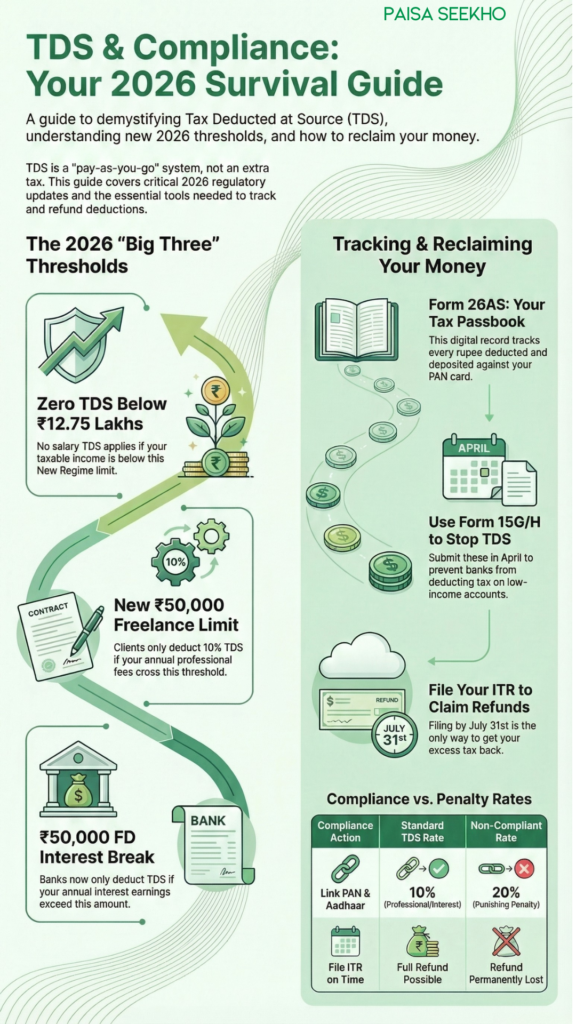

- Paisaseekho Pro-Tip: If your salary is below the taxable limit (effectively Rs. 12.75 Lakhs under the New Tax Regime in 2026), your employer should deduct zero TDS. If they are still deducting it, you need to talk to your payroll department immediately!

2. TDS for Freelancers and Creators (Section 194J)

If you are a freelancer, consultant, or creator, Section 194J is going to be your constant companion. Whenever a client pays you for your professional services, they are legally required to deduct TDS before clearing your invoice.

- The Rate: The standard deduction is 10% for professional services (like writing, designing, or consulting) and 2% for technical services.

- The 2026 Relief Update: Here is the good news! Following the recent budget updates for 2026, the government increased the threshold limit. Your client will only deduct TDS if the total amount they pay you in a single financial year crosses Rs. 50,000 (this used to be just Rs. 30,000). If you only bill a client for Rs. 40,000 for a one-off project, they should pay you the full amount without any TDS cuts.

3. TDS on Bank FDs and Savings (Section 194A)

You finally started building an emergency fund and locked some money into a Fixed Deposit (FD). But when the bank pays you interest, they also slice off a piece for the government under Section 194A.

- The Rate: Banks will automatically deduct a flat 10% TDS on your interest earnings.

- The 2026 Relief Update: Just like with freelancers, the government recently gave savers a massive break. In 2026, banks will only deduct TDS if your total interest earned across all branches crosses Rs. 50,000 in a year (this was recently increased from Rs. 40,000). For your senior citizen parents, this limit was doubled to a massive Rs. 1,00,000.

The “Save Me” Forms: How to Stop TDS with Form 15G & Form 15H

Let’s look at a very common scenario. Imagine you are a college student or a young professional currently taking a gap year. You have zero salary, but you have a large Fixed Deposit your grandparents gifted you that generates Rs. 60,000 in interest every year.

Because the interest crosses the Rs. 50,000 bank threshold, the bank will automatically deduct 10% (Rs. 6,000) as TDS. But wait, your total annual income is way below the basic taxable limit! You shouldn’t be paying any income tax, let alone TDS.

To solve this exact problem and stop the bank from taking your money, the government created two “Save Me” forms:

Form 15G (For Individuals Below 60 Years)

Form 15G is simply a self-declaration form you submit to your bank. By signing it, you are officially telling the government: “I promise that my total income for this financial year is going to be below the minimum taxable limit. Please instruct the bank not to deduct any TDS from my interest.”

- Once you submit this form, the bank will pay you your full FD interest without a single rupee cut.

Form 15H (For Senior Citizens)

This is the exact same concept as Form 15G, but it is specifically designed for your parents or grandparents who are 60 years of age or older. Since senior citizens have different tax exemptions, they use Form 15H to protect their pension or FD interest from unnecessary TDS deductions.

When Should You Submit These Forms?

Timing is everything. You should ideally submit Form 15G or 15H to your bank at the start of the financial year (in April). Most major banks allow you to fill out and submit these forms digitally through their net banking portals in less than two minutes.

Important Warning: Never submit a Form 15G if your total income is actually going to cross the taxable limit. Making a false declaration to avoid TDS is a serious offense and can attract heavy penalties from the Income Tax Department.

The Holy Trinity of Tax Tracking: Form 16, Form 26AS, and the AIS

Okay, so your employer, your freelance client, and your bank have all deducted TDS from your income. But how do you actually know they deposited that money with the government? What if your HR deducted Rs. 5,000 from your salary but just kept it for the company?

To ensure nobody steals your tax money, the Income Tax Department gives you three powerful tools to track every single rupee. We call this the Holy Trinity of Tax Tracking.

1. Form 16 & Form 16A (Your Deduction Certificates)

Think of this as your official receipt. If someone deducts TDS from your payment, they are legally required to give you a certificate proving they deposited it with the government.

- Form 16: This is issued by your employer at the end of the financial year (usually by mid-June). It contains a detailed breakdown of your salary, the tax-saving deductions you claimed, and the exact amount of TDS deducted and deposited.

- Form 16A: This is for non-salary income. If a freelance client or a bank deducts TDS from your invoice or FD interest, they must provide you with a Form 16A every quarter.

2. Form 26AS (Your Government Tax Passbook)

Form 16 is great, but what if you have two employers in a year, three freelance clients, and a couple of bank FDs? Managing all those separate certificates gets messy.

Enter Form 26AS. This is your consolidated annual tax passbook linked directly to your PAN card. You can download it directly from the Income Tax portal. It shows a complete, single-page summary of every single entity that has deducted TDS on your behalf and deposited it with the government.

- Paisaseekho Pro-Tip: Before you file your income tax return, always cross-check your Form 16 against your Form 26AS. If a TDS deduction shows up on your salary slip but is missing from your 26AS, it means your employer hasn’t paid the government yet!

3. AIS (Annual Information Statement)

In recent years, the government upgraded the old Form 26AS into something much more powerful: the AIS (Annual Information Statement).

While Form 26AS only shows your tax deductions, the AIS tracks your entire financial life. When you log into the AIS portal, you will see a detailed record of your mutual fund purchases, stock market sales, massive credit card bills, dividend income, and even foreign travel expenses. It is the ultimate dashboard showing exactly what the government knows about your money.

What is Advance Tax? (The Freelancer and Business Owner’s Rule)

If you are a salaried employee, you can comfortably skip this section. Your HR department calculates your tax, deducts the TDS every month, and handles all the compliance for you.

But if you are a freelancer, a YouTuber, or a startup founder, the burden of calculating and paying taxes falls entirely on your shoulders. The government does not want you to wait until July of the next year to pay your massive tax bill. They expect you to pay as you earn, which is why they created the Advance Tax rule.

Do You Need to Pay Advance Tax in 2026?

The rule is remarkably simple: If your estimated total tax liability for the financial year is expected to be more than Rs. 10,000 (after subtracting whatever TDS has already been deducted by your clients), you are legally required to pay Advance Tax.

What Are the Deadlines for Advance Tax?

You do not pay it all at once. The government kindly breaks it down into four quarterly installments throughout the financial year:

- On or before June 15th: Pay 15% of your total estimated tax.

- On or before September 15th: Pay 45% of your total estimated tax.

- On or before December 15th: Pay 75% of your total estimated tax.

- On or before March 15th: Pay 100% of your total estimated tax.

What Happens If You Forget to Pay?

If you miss these deadlines or underestimate your income and pay too little, the Income Tax Department will hit you with penalty interest under Sections 234B and 234C. They will charge you a 1% interest penalty per month on the unpaid amount until you finally clear your dues.

If you are running a successful side hustle or a full-time freelance gig, setting calendar reminders for the 15th of June, September, December, and March is an absolute must!

What Happens If You Don’t Link PAN and Aadhaar? (The Ultimate Compliance Rule)

Let’s take a quick break from tax sections and talk about a strict, non-negotiable compliance rule for 2026. For years, the government sent out reminders to link your PAN card with your Aadhaar card. If you are one of the few who kept ignoring those SMS alerts, you are in for a very expensive surprise.

If your PAN and Aadhaar are not linked, the Income Tax Department officially declares your PAN card as “inoperative.”

The Cost of an Inoperative PAN Card

An inoperative PAN card is essentially a frozen financial identity. Here is exactly how it destroys your finances:

- The 20% Penalty TDS: Remember how we said freelance clients and banks deduct a standard 10% TDS? If your PAN is inoperative, the law (Section 206AA) forces them to deduct TDS at a punishing 20% instead. You lose double the money upfront.

- Zero Refunds: You cannot file your Income Tax Return (ITR) with a dead PAN card. If you cannot file your ITR, you cannot claim a single rupee of that 20% TDS back as a refund. The money is permanently stuck with the government.

- Banking Paralysis: You won’t be able to open new bank accounts, invest in mutual funds, or get a credit card.

Paisaseekho Pro-Tip: If you just realized your PAN might be inactive, go to the official Income Tax e-filing portal immediately, pay the late penalty fee (usually Rs. 1,000), and initiate the linking process. It takes a few days to reflect, but it will save you thousands in excess TDS.

How to Get Your TDS Back? (The Ultimate Refund Process)

We have talked a lot about the government taking your money. Now, let’s talk about how you get it back.

The biggest myth among young taxpayers is: “Once TDS is deducted, the money is gone forever.” As we established earlier, TDS is just an advance payment. If the total money in your “government locker” (your Form 26AS) is greater than your actual tax liability for the year, you are entitled to an Income Tax Refund.

The 3-Step Process to Claim Your TDS Refund

Step 1: Calculate Your Actual Tax Liability

At the end of the financial year, sit down and calculate your actual tax under the Old or New Tax Regime. Let’s say you are a freelancer who earned Rs. 6 Lakhs this year. Your clients deducted 10% TDS, meaning Rs. 60,000 is sitting in your Form 26AS. However, under the 2026 New Tax Regime, your tax liability on a 6 Lakh income is effectively ZERO.

Step 2: File Your ITR (Income Tax Return) on Time

The government will not automatically send the money back to your account. You have to formally ask for it. The only legal way to claim a TDS refund is by filing your ITR before the deadline (usually July 31st). When you fill out the online form, the portal will automatically match your tax liability (Zero) against your paid TDS (Rs. 60,000) and show that you are owed a Rs. 60,000 refund!

Step 3: Pre-Validate Your Bank Account

Before you hit submit on your ITR, ensure you have a “pre-validated” bank account linked to your profile on the e-filing portal. The Income Tax Department will no longer send physical cheques; the refund amount (along with a small interest payout for the delay) will be directly credited via NEFT/RTGS to your validated bank account within a few weeks of processing.

Conclusion: Compliance is Just Financial Self-Care

When you first enter the workforce, words like “TDS,” “AIS,” and “Form 26AS” sound like a terrifying alphabet soup designed to confuse you. It is easy to feel overwhelmed and simply let HR or your CA handle everything blindly.

But true financial independence means knowing exactly where your money is at all times.

Tracking your TDS isn’t just about following government rules; it is a form of financial self-care. It ensures you aren’t paying double taxes, it protects you from fraudulent deductions, and it guarantees you get every single rupee of your hard-earned refund back into your bank account where it belongs.

Stop treating the Income Tax portal like a scary principal’s office. Log in today, download your AIS, check your Form 26AS, and take control of your financial footprint.

Frequently Asked Questions

1. Is TDS refundable?

Yes, absolutely! TDS is just an advance tax payment. If your total tax liability for the year is lower than the TDS deducted by your employer or clients, the government will refund the excess amount. You just need to file your Income Tax Return (ITR) to claim it.

2. How can I check if my employer actually deposited my TDS?

You can verify this by checking your Form 26AS or your Annual Information Statement (AIS). Log into the official Income Tax e-filing portal with your PAN and password, and download these statements. If the TDS your employer deducted is not showing up there, you need to contact your HR immediately.

3. What is the minimum salary for TDS deduction in 2026?

Under the default New Tax Regime for 2026, if your total taxable income is up to Rs. 12.75 Lakhs (including the standard deduction), your tax liability is zero due to government rebates. Therefore, your employer should deduct zero TDS from your salary.

4. Why did the bank deduct TDS on my FD when I don’t earn a salary?

Banks do not know your overall financial situation. The law tells them to blindly deduct 10% TDS the moment your Fixed Deposit interest crosses Rs. 50,000 in a year (Rs. 1 Lakh for senior citizens). If your total income is below the taxable limit, you must submit Form 15G (or Form 15H for senior citizens) to the bank in April to stop them from making this deduction.

5. What happens if I don’t file my ITR after TDS is deducted?

If you do not file your ITR, you will permanently lose your refund. The government does not automatically send the money back to your bank account. Furthermore, if your income was above the basic exemption limit and you ignored filing, you could receive a penalty notice from the Income Tax Department.

6. Can my client or employer deduct TDS if I don’t give them my PAN card?

Yes, and it will hurt your wallet. If you do not provide your PAN, or if your PAN is inactive because it isn’t linked to your Aadhaar, the law forces the deductor to apply TDS at a punishing rate of 20% instead of the standard 10%.

7. What is the difference between Form 16 and Form 26AS?

Form 16 is a certificate issued specifically by your employer showing the salary they paid you and the TDS they deducted. Form 26AS is your master tax passbook maintained by the government; it shows every single entity (employers, freelance clients, banks) that has deducted and deposited TDS against your PAN card.

8. Are freelancers required to pay Advance Tax?

Yes. If you are a freelancer, creator, or business owner, and your estimated tax liability for the year (after subtracting the TDS already deducted by clients) is more than Rs. 10,000, you must pay Advance Tax in four quarterly installments (June, September, December, and March).

9. How long does it take to get a TDS refund?

Once you file and successfully e-verify your Income Tax Return, it usually takes anywhere from 15 to 45 days for the Income Tax Department to process it. The refund is directly credited to your pre-validated bank account.

10. Does TDS apply to personal UPI transfers?

No. If you split a dinner bill with a friend or send money to your family via UPI, there is no TDS. TDS generally applies to business transactions, professional fees, salaries, rent above specific limits, and interest income.