TL;DR: The Key Takeaways of Old vs New Tax Regime

- The Core Difference: The New Tax Regime offers lower tax slab rates but removes over 70 common deductions (like 80C, HRA, and LTA). The Old Tax Regime charges higher slab rates but allows you to heavily reduce your taxable income through investments and rent receipts.

- The 2026 Default Rule: The New Regime is the default for FY 2025-26. If you do not explicitly inform your HR that you want the Old Regime in April, they will automatically deduct your TDS based on the New Regime.

- The “Zero Investment” Winner: If your salary is up to Rs. 12.75 Lakhs, you pay absolutely zero tax under the New Regime without needing to make a single forced investment.

- The “Heavy Investor” Winner: If you pay high rent in a metro city (HRA) and max out your 80C (Rs. 1.5 Lakhs) and home loan interest, the Old Regime usually saves you more money once your salary crosses the Rs. 15 Lakh mark.

Note: This comparison is based on the updated standard deduction (Rs. 75,000) and Section 87A rebate limits for FY 2025-26 (AY 2026-27).

1. Old vs New Tax Regime Dillema

It happens every single year. The first week of April rolls around, and an automated email from your HR department lands in your inbox:

“Action Required: Please declare your Income Tax Regime for the financial year.”

If you are like most young professionals, you stare at that email in total paralysis. You open a new tab, search for a tax calculator, get completely overwhelmed by the jargon, and blindly ask your office best friend what they chose. The fear is real—what if picking the wrong regime costs you Rs. 50,000 in extra taxes?

Take a deep breath. At Paisaseekho, we want to completely eliminate this April anxiety.

Choosing between the Old vs New Tax Regime is not a permanent life sentence, nor is it a test of your financial intelligence. It is simply a mathematical formula based entirely on your current lifestyle.

If you are living at home with zero rent, your answer will be different from your colleague who is paying Rs. 30,000 a month for a flat in Bangalore and actively paying off an education loan. This guide is your ultimate showdown. We are going to strip away the complex CA terminology and give you a foolproof framework to figure out exactly which regime leaves the most money in your bank account in 2026.

2. The New Tax Regime: The “Minimalist” Option

Let’s start with the government’s favorite child. For the 2026 financial year, the New Tax Regime is officially your default setting. If you ignore that HR email, this is the regime you will automatically be placed in.

The philosophy behind the New Regime is pure minimalism: Give people lower tax rates, but take away the headache of claiming deductions.

Who is it for?

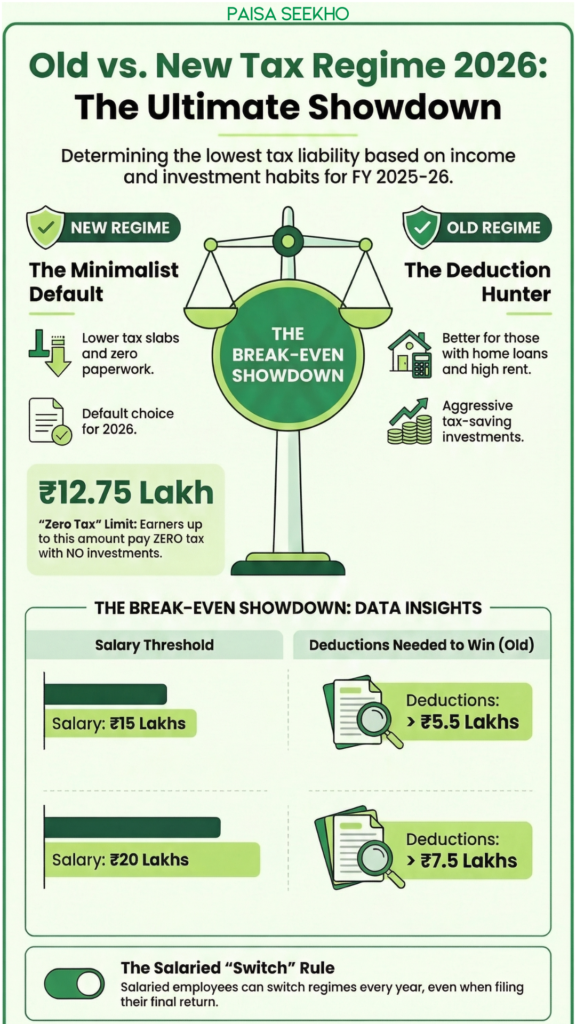

This regime is the undisputed champion for young earners living in their hometowns (no rent), professionals who hate locking their money into 15-year schemes like PPF, and anyone whose total salary is under Rs. 12.75 Lakhs.

The Pros: High Liquidity & Zero Stress

- The Zero-Tax Magic: Thanks to the Rs. 75,000 Standard Deduction and the Section 87A rebate, you can earn a gross salary of up to Rs. 12.75 Lakhs and pay exactly zero income tax.

- Higher Monthly Take-Home: Because you aren’t forced to lock up Rs. 1.5 Lakhs in Section 80C investments just to save tax, you have way more cash in hand every month to spend on travel, experiences, or high-risk investments like stocks and crypto.

- Zero March Panic: You never have to scramble to buy a terrible traditional insurance policy at the last minute or beg your landlord for a PAN card to generate rent receipts.

The Cons: The Deduction Slaughter

To give you those beautifully low tax slabs (0%, 5%, 10%, etc.), the government had to take something away. Under the New Regime, you lose almost every single deduction you grew up hearing about:

- No HRA (House Rent Allowance) exemption for your rent.

- No Section 80C (Say goodbye to tax breaks on ELSS, PPF, and Life Insurance).

- No Section 80D (No tax benefit for paying health insurance premiums).

- No Section 24(b) (No deduction for the interest paid on a self-occupied home loan).

Wait, What Actually Survives?

The New Regime is strict, but it isn’t entirely heartless. You still get to claim two major benefits:

- The Rs. 75,000 Standard Deduction: A flat discount on your salary before any tax is calculated.

- Section 80CCD(2): If your employer contributes up to 10% (or 14%) of your basic salary directly into an NPS (National Pension System) account, that entire amount is still 100% tax-free!

3. The Old Tax Regime: The “Deduction Hunter” Option

If the New Regime is so simple and offers a massive Rs. 12.75 Lakh tax-free limit, why did the government even keep the Old Tax Regime alive in 2026?

Because for a very specific group of disciplined investors and big spenders, the Old Regime is still the ultimate wealth-hacking tool. The Old Regime charges you much higher tax percentages upfront, but it allows you to aggressively bring down your “taxable income” by using dozens of legal deductions.

Who is it for?

This regime is built for professionals paying high rent in expensive metro cities like Mumbai, Bangalore, or Gurgaon. It is also the undisputed champion for people actively paying off a home loan or those who effortlessly max out their Rs. 1.5 Lakh PPF/Mutual Fund quotas every year.

The Pros: Maximizing the “Cheat Codes”

- The Holy Trinity: You get to claim the three biggest tax-savers: HRA (House Rent Allowance), Section 80C (up to Rs. 1.5 Lakhs for ELSS, PPF, Life Insurance), and Section 80D (Health Insurance premiums for you and your parents).

- Home Loan Magic: Under Section 24(b), you can deduct up to Rs. 2 Lakhs of the interest you pay on your home loan.

- Higher Income Savings: If your salary is significantly high (e.g., Rs. 20 Lakhs) and you maximize every single deduction available, your final tax bill under the Old Regime can actually be lower than the New Regime.

The Cons: The Paperwork Trap

- Lower Standard Deduction: While the New Regime gives salaried employees a flat Rs. 75,000 discount, the Old Regime restricts this Standard Deduction to just Rs. 50,000.

- Cash Flow Lock-Up: To save tax, you are forced to lock away your cash. Pumping Rs. 1.5 Lakhs into a 15-year PPF account means you have less liquid money today.

- The Proof Panic: You have to painstakingly collect and submit rent agreements, landlord PAN cards, medical bills, and mutual fund statements to your HR team. If you miss the deadline, your TDS goes through the roof!

4. The Break-Even Point (The Magic Number)

This is the most important section of this entire guide.

How do you actually choose between the old vs new tax regime? You find your Break-Even Point. This is the exact amount of deductions you need to claim for the Old Regime to match (and eventually beat) the New Regime.

Let’s look at three realistic salary scenarios for 2026 to see exactly where that line is drawn:

Scenario A: The Rs. 10 Lakh to Rs. 12.75 Lakh Salary

- The Winner: The New Regime (Instantly)

- The Math: Do not even open a tax calculator. Because of the Rs. 75,000 Standard Deduction and the Section 87A rebate, if your CTC is Rs. 12.75 Lakhs or below, your tax under the New Regime is exactly ZERO. Under the Old Regime, you would have to scramble to find lakhs in deductions just to get the same zero-tax result.

Scenario B: The Rs. 15 Lakh Salary

- The Winner: It depends on your rent.

- The Math: At a Rs. 15 Lakh salary, the New Regime calculates a relatively low tax. To beat it using the Old Regime, you need to prove roughly Rs. 5.5 Lakhs in total deductions (this includes your Rs. 50,000 standard deduction).

- Can you reach 5.5 Lakhs? If you max out 80C (1.5L) + pay health insurance (25K) + claim a heavy HRA because you live in Bangalore (say, 3L), you easily cross the break-even point. The Old Regime is better for you. If you live at home with your parents and pay zero rent, stick to the New Regime.

Scenario C: The Rs. 20 Lakh Salary

- The Winner: The Old Regime (Usually)

- The Math: At this income level, the New Regime slabs start biting harder. To make the Old Regime win, you need roughly Rs. 7.5 Lakhs in total deductions.

- Can you reach 7.5 Lakhs? This is usually possible if you are paying off a home loan (Rs. 2 Lakh deduction) plus maximizing your 80C (Rs. 1.5 Lakh) plus claiming HRA/LTA. If you are a heavy investor or a new homeowner, the Old Regime will leave more money in your pocket.

5. The “Can I Switch Back?” Rule

One of the biggest reasons young professionals panic in April is the fear of commitment. They think that if they click “New Regime” on the HR portal, they are locked into it forever.

Thankfully, the Income Tax Department is surprisingly flexible, but only for some people. The rules for switching regimes depend entirely on how you earn your money.

For Salaried Employees: Ultimate Flexibility

If your only source of income is your salary (and maybe some savings bank interest or house property income), you have the ultimate cheat code: You can switch regimes every single year.

- What if you have a baby, buy a house, and suddenly have massive deductions next year? No problem. Just switch back to the Old Regime.

- The Ultimate Hack: You can declare the New Regime to your HR in April for easy TDS deductions, but when July comes and it is time to officially file your Income Tax Return (ITR), you can recalculate everything. If the Old Regime suddenly saves you more money, you can simply select the Old Regime on the tax portal and claim a refund!

For Freelancers & Business Owners: The “Once in a Lifetime” Trap

If you are a founder, a full-time freelancer, or anyone filing taxes under “Income from Business or Profession” (like the Section 44ADA cheat code we discussed in our Business Taxation guide), the government is very strict.

- The Rule: You only get a “once in a lifetime” chance to opt out of the default New Regime and switch to the Old Regime.

- If you switch to the Old Regime this year, but then decide to go back to the New Regime next year, the doors lock behind you. You can never return to the Old Regime again for the rest of your life (unless you shut down your business and become a salaried employee). Choose very carefully!

6. The Paisaseekho Checklist: How to Choose between old vs new tax regime in 5 Minutes

You now know the pros, the cons, and the break-even math. It is time to stop procrastinating and reply to that HR email.

Here is your foolproof, 5-minute action plan to pick your 2026 tax regime:

- Estimate Your CTC: Look at your appraisal letter. What is your expected gross salary for this financial year? If it is under Rs. 12.75 Lakhs, stop here. Reply to HR with “New Regime” and go enjoy your day.

- List Your Guaranteed Deductions: If you earn over Rs. 15 Lakhs, take a piece of paper. Write down your guaranteed investments. How much will automatically go into EPF? Are you definitely paying Rs. 20,000 in rent every month? Are you already paying an EMI on a home loan?

- Use the Official Calculator: Do not try to do the complex slab math in your head. Go to the official Income Tax India portal and open their free “Tax Calculator.”

- Compare the Final Number: Plug your salary and your guaranteed deductions into the calculator. It will instantly show you exactly how much tax you will pay under the Old vs. the New Regime side-by-side.

- Hit Send: Whichever number is lower, that is your winner. Reply to the HR email confidently.

7. Conclusion: Don’t Let the Tail Wag the Dog

There is an old saying in finance: “Do not let the tax tail wag the investment dog.”

This means you should never make a massive life or financial decision purely to save a few thousand rupees in tax. Do not lock your money into a 15-year PPF account if you plan to move abroad in three years, just because you want the Old Regime to work for you. Do not take on a Rs. 1 Crore home loan simply for the Section 24(b) tax deduction if you aren’t ready to buy a house.

Let your life goals dictate your investments, and let the simple math dictate your tax regime.

If your lifestyle naturally creates heavy deductions (rent, home loans, aggressive wealth building), the Old Regime is your best friend. If you prefer high liquidity, zero paperwork, and a massive tax-free base, embrace the New Regime minimalist lifestyle.

Your Next Step: You have 5 minutes right now. Pull up the Income Tax Calculator, plug in your new salary, and find your break-even point today!

Top 10 Frequently Asked Questions about the old vs new tax regime

1. Which tax regime is better for a salary of Rs. 15 Lakhs in 2026?

If you have zero investments and pay no rent, the New Tax Regime is mathematically better. However, if you live in a metro city and can claim a high House Rent Allowance (HRA) along with your full Rs. 1.5 Lakh Section 80C limit (PPF/ELSS), the Old Tax Regime will likely save you more money. You need roughly Rs. 5.5 Lakhs in total deductions for the Old Regime to win at this salary level.

2. Can I claim HRA (House Rent Allowance) in the New Tax Regime?

No. The New Tax Regime strips away almost all major exemptions, including HRA, LTA (Leave Travel Allowance), and Section 80C. If your rent is your biggest monthly expense and you want a tax break for it, you must opt for the Old Tax Regime.

3. Is the Rs. 75,000 Standard Deduction available in both regimes?

No. For the 2026 financial year, salaried employees and pensioners get a massive Rs. 75,000 standard deduction under the New Tax Regime. If you choose the Old Tax Regime, your standard deduction is capped at the classic Rs. 50,000.

4. What happens if I forget to tell HR which tax regime I want?

If you ignore the HR email in April, your company is legally required to deduct your TDS based on the New Tax Regime, as it is the default system for FY 2025-26.

5. Can I switch from the New Regime to the Old Regime while filing my ITR?

Yes, but only if you are a salaried employee. Even if your HR deducted TDS all year based on the New Regime, you can calculate your taxes under the Old Regime in July, switch on the portal, and claim a refund. However, if you have business or freelance income, you only get a “once in a lifetime” chance to switch back to the Old Regime.

6. Do I need to submit investment proofs to HR if I choose the New Regime?

Generally, no! Because the New Regime doesn’t allow deductions for rent, mutual funds, or life insurance, you do not have to scramble for receipts in February. The only exception is if you are claiming the Section 80CCD(2) deduction for your employer’s contribution to your NPS account.

7. How is a Rs. 12.75 Lakh salary tax-free in the New Regime?

It is a combination of two rules: First, you subtract the Rs. 75,000 standard deduction from your Rs. 12.75 Lakh salary, bringing your taxable income down to exactly Rs. 12 Lakhs. Second, under Section 87A, the government gives a full tax rebate on any income up to Rs. 12 Lakhs. Therefore, your calculated tax drops to zero.

8. Can I claim my home loan interest in the New Tax Regime?

No. The deduction of up to Rs. 2 Lakhs on home loan interest (Section 24b) for a self-occupied property is only available under the Old Tax Regime. If you are paying heavy EMIs on your primary residence, the Old Regime is usually the smarter mathematical choice.

9. Which tax regime is better for freelancers?

For most young freelancers and creators earning under Rs. 75 Lakhs, the New Tax Regime combined with Section 44ADA (declaring 50% profit) is incredibly powerful and requires almost zero paperwork.

10. Can I claim health insurance premiums (Section 80D) in the New Regime?

No. You cannot claim tax deductions for your own or your parents’ health insurance premiums under the New Tax Regime. If you pay massive premiums for senior citizen parents, you might want to calculate your break-even point under the Old Regime.