TL;DR: Key Takeaways on NRI Property Sales

If you have a meeting with your property broker in five minutes, here is the absolute quickest summary of what you need to know:

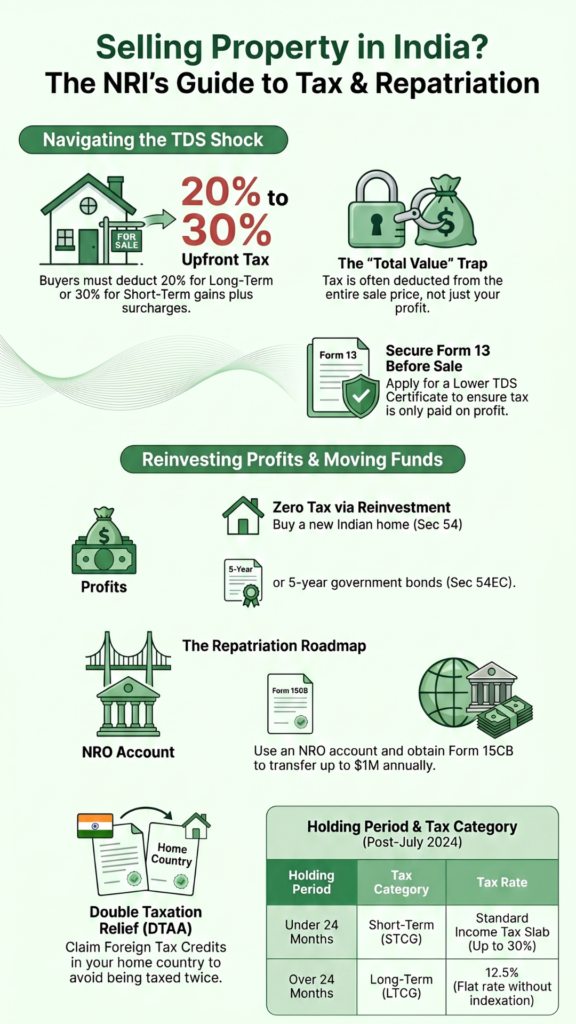

- The High TDS Shock: While resident Indians face only a 1% TDS when selling property, buyers purchasing from an NRI must deduct a massive 20% to 30% TDS (plus surcharge and cess).

- The Total Value Trap: The worst part is that this high TDS is usually deducted on the total sale value of the property, not just your profit!

- The Savior (Form 13): To fix this cash flow nightmare, NRIs must apply for a Lower TDS Certificate (Form 13) before the sale. This allows the buyer to deduct tax only on your actual profit.

- The Tax Rates: If you hold the property for more than 24 months, it is Long-Term Capital Gains (LTCG). For properties bought after July 2024, the tax is 12.5% (without indexation). If sold within 24 months, it is Short-Term (STCG) and taxed at your regular slab rate (up to 30%).

- Tax Exemptions: You can save your capital gains tax completely by reinvesting the profit into a new residential house in India (Section 54) or specific government bonds (Section 54EC).

- Moving the Money: To take the money out of India, it must go into an NRO account first. You will need a Chartered Accountant to issue Form 15CB before the bank allows you to transfer the funds abroad.

Introduction

If you are a Non-Resident Indian (NRI) living in the United States, the UK, the UAE, or anywhere else across the globe, you likely have a strong emotional and financial connection to India. For decades, one of the favorite investment strategies for NRIs has been buying real estate back home. Whether it is a luxury apartment in Mumbai, a villa in Bengaluru, or an ancestral plot of land in Kerala, Indian property has always been viewed as a solid, secure investment.

But what happens when you finally decide it is time to sell that property?

Many NRIs assume the selling process will be simple. They think they will just find a buyer, sign the registration papers, take the cash, and transfer the money abroad.

Unfortunately, that is not how the system works. In 2026, the Income Tax Department of India has very strict, highly monitored rules for NRIs. If you sell a property as an NRI, you are instantly hit with Tax Deducted at Source (TDS) rates that are drastically higher than what a regular resident Indian would pay. If you do not plan properly, a massive chunk of your sale money will be locked away by the government before it even reaches your bank account.

But do not panic! The Indian tax code also provides perfectly legal pathways to lower this tax burden and bring your money home safely.

1. The TDS Difference: Why Do NRIs Pay So Much Upfront?

To understand the tax shock that NRIs face, we need to compare them to regular, resident Indians.

When a resident Indian sells a house worth ₹80 Lakhs, the buyer is required by law to deduct 1% TDS (Tax Deducted at Source) and deposit it with the government. So, the buyer holds back ₹80,000 and gives the seller the remaining ₹79,20,000. It is a very small, manageable deduction.

But the rules change completely if the seller is an NRI.

Under Section 195 of the Income Tax Act, the government looks at NRIs differently. Because an NRI lives outside the country, the Indian government is afraid that the NRI might take the entire sale money, fly back to the US or Dubai, and simply “forget” to pay their Indian income taxes.

To prevent this from happening, the government forces the buyer to deduct a massive amount of tax upfront before handing over the money.

- If the property is sold within 2 years (Short-Term), the TDS rate can be 30%.

- If the property is sold after 2 years (Long-Term), the TDS rate is generally 20% (or 12.5% depending on the specific asset rules, plus applicable surcharge and a 4% health and education cess).

If a buyer fails to deduct this massive TDS and the NRI leaves the country without paying tax, the Income Tax Department will actually catch the buyer and force them to pay the NRI’s tax bill! Because of this strict rule, buyers are incredibly careful and will absolutely insist on deducting the highest possible TDS.

2. Understanding Your Actual Tax: STCG vs. LTCG

It is very important to understand that TDS is not your final tax. TDS is just an “advance tax” collected by the government. Your actual, final tax liability depends on how long you owned the property and how much profit you made.

This profit is called a Capital Gain.

What are Short-Term Capital Gains (STCG)?

If you buy a house or a piece of land and sell it within 24 months (2 years), the government considers you a short-term investor.

- Any profit you make is simply added to your total income in India for that year.

- It is taxed according to your standard income tax slab rate. If your profit is huge, you will easily hit the highest tax bracket, meaning you will pay a flat 30% tax on your profit.

What are Long-Term Capital Gains (LTCG)?

If you patiently hold the property for more than 24 months, the government rewards you with a lower tax rate.

However, the rules for LTCG recently underwent a massive change in the Indian Union Budget.

- The New 2024/2026 Rule: For any property purchased on or after July 23, 2024, the Long-Term Capital Gains tax is a flat 12.5%. However, the government has removed the “indexation benefit” (the ability to adjust your purchase price for inflation).

- The Old Property Rule: For older properties bought before July 2024, there are specific grandfathering rules where taxpayers can calculate their tax at 20% with the indexation benefit, or 12.5% without it, depending on what benefits them more.

Regardless of the exact percentage, LTCG is always much cheaper than STCG. Therefore, if you are an NRI thinking about selling a property you bought 20 months ago, it is highly advisable to wait four more months so you can qualify for the much cheaper Long-Term Capital Gains tax bracket!

3. The Ultimate Cash Flow Nightmare: TDS on the “Total Sale Value”

Now we reach the biggest problem that NRIs face when selling real estate in India.

Let us look at a simple math example.

Imagine you bought an apartment in Delhi five years ago for ₹90 Lakhs.

Today, you sell that exact same apartment for ₹1 Crore (₹100 Lakhs).

Your actual profit (Capital Gain) is only ₹10 Lakhs.

Logically, you should only pay tax on that ₹10 Lakh profit. But remember Section 195? The law tells the buyer to deduct 20% TDS (plus surcharge and cess).

Because the buyer does not know your original purchase price, they are legally advised to deduct that massive 20% TDS on the Total Sale Value!

- Total Sale Value: ₹1 Crore.

- 20% of ₹1 Crore = ₹20 Lakhs!

The buyer will deduct ₹20 Lakhs and give you a cheque for only ₹80 Lakhs.

This is an absolute disaster. You bought the house for ₹90 Lakhs, but you are only getting ₹80 Lakhs in your hand! Your entire capital is locked up by the Income Tax Department.

Yes, you can file your Income Tax Return (ITR) at the end of the year, show that your real tax on the ₹10 Lakh profit is very small, and claim a refund for the excess TDS. But getting a massive ₹20 Lakh refund from the government takes months, sometimes years, of tedious paperwork and follow-ups.

4. How can Form 13 (Lower TDS Certificate) Help?

How do you stop the buyer from deducting TDS on the total sale value? How do you protect your cash flow?

The answer is Form 13.

Before you finalize the sale and sign the registration papers, you (the NRI seller) must apply for a “Lower TDS Certificate” or a “Nil Deduction Certificate” under Section 197 of the Income Tax Act. You do this by filing Form 13 online on the Income Tax Portal.

How Form 13 Works:

- You hire an Indian Chartered Accountant (CA).

- The CA calculates your exact capital gains. They show the government your original purchase papers, your exact profit, and your final estimated tax liability.

- The Income Tax Officer reviews your application. If they agree with the math, they will issue a formal, stamped certificate.

- This certificate specifically instructs the buyer: “Do not deduct 20% on the ₹1 Crore total value. Only deduct a specific lower percentage based on the actual profit.”

If you hand this certificate to your buyer, they will deduct a much smaller, reasonable amount, and you will receive the vast majority of your sale money directly in your bank account on the day of the sale.

Important Warning: Applying for Form 13 is not an overnight process. The Income Tax Department can take anywhere from 30 to 45 days to process the application and issue the certificate. You must start this process the moment you find a buyer, long before the final registration date.

5. How to Legally Save Your Capital Gains Tax

Just because you made a profit does not mean you have to hand it all over to the government. The Income Tax Act provides several brilliant, 100% legal exemptions that allow NRIs to reduce their capital gains tax to absolute zero.

These exemptions require you to reinvest your profit back into the Indian economy.

A. The “New House” Exemption (Section 54)

If you sell a residential house and make a long-term capital gain, you can claim an exemption under Section 54 if you use that profit to buy or construct a new residential house in India.

- The Timeline: You must buy the new house either 1 year before the sale or within 2 years after the sale. If you are constructing a new house, you have 3 years.

- The Restriction: The new property must be located within the borders of India. You cannot sell a house in Mumbai and use the profit to buy a house in London to claim this Indian tax exemption.

B. The “Other Asset to House” Exemption (Section 54F)

What if you sell a commercial shop, or an empty plot of land?

You can use Section 54F. If you sell any long-term asset (other than a residential house) and use the entire sale money (not just the profit) to buy a new residential house in India, your capital gains tax is completely waived off.

C. The Government Bond Exemption (Section 54EC)

What if you do not want to buy another house? What if you are tired of managing Indian real estate from abroad?

You can use Section 54EC. You can take your long-term capital gains profit and invest it into specific, ultra-safe bonds issued by government-backed companies like the National Highway Authority of India (NHAI) or the Rural Electrification Corporation (REC).

- The Limit: You can invest a maximum of ₹50 Lakhs per financial year in these bonds.

- The Lock-in: Your money will be locked in these bonds for exactly 5 years. You will earn a steady annual interest rate (usually around 5% to 6%) during this time, and at the end of 5 years, you get your principal back.

(Pro Tip: Even if you plan to use these exemptions, the buyer will still try to deduct the high TDS. You must mention your intention to reinvest when you apply for the Form 13 Lower TDS Certificate so the tax officer issues a “Nil” deduction certificate!)

6. The Repatriation Challenge: How to Move the Money Abroad

For most NRIs, selling the property is only half the battle. The real goal is getting that massive sum of money out of India and into their local bank account in the US, UK, or UAE.

The Reserve Bank of India (RBI) controls the flow of foreign exchange very tightly. You cannot simply open your Indian banking app and wire ₹1 Crore to a foreign bank account. There is a strict, legal pathway you must follow, known as the Repatriation Process.

Here is exactly how you move your property sale money abroad:

Step 1: The NRO Account

When the buyer gives you the money, it cannot go directly to your foreign account. The money must first be deposited into your Non-Resident Ordinary (NRO) bank account in India. (An NRO account is specifically meant to hold income earned within India, like rent or property sale proceeds).

Step 2: The Limit Check

The RBI allows NRIs to freely repatriate (transfer out) up to $1 Million USD per financial year from their NRO account without seeking special RBI permission. For almost all regular property sales, this limit is more than enough.

Step 3: Form 15CA and Form 15CB

Before the bank allows the money to leave the country, they need absolute proof that you have paid all your Indian taxes on that specific money.

- You must hire a Chartered Accountant (CA).

- The CA will review your property sale, ensure the TDS was deducted correctly, and ensure there are no pending taxes.

- The CA will then issue a certificate called Form 15CB.

- Using this CA certificate, you will log into the Income Tax Portal and fill out a self-declaration document called Form 15CA.

Step 4: The Bank Transfer

You take the 15CB, the 15CA, the property sale deed, and the bank’s specific outward remittance forms, and submit them to your NRO bank branch. Once the bank’s compliance team verifies that the tax department is satisfied, they will convert the Rupees into your foreign currency and wire it to your overseas account.

7. Beware of the Double Taxation Trap (DTAA)

There is one final danger that NRIs must be aware of: being taxed twice on the exact same property sale.

Let us say you are an NRI living in the United States. You sell an apartment in Pune and make a handsome profit. You go through the entire process, pay your 12.5% Long-Term Capital Gains tax to the Indian government, and transfer the money to your US bank account.

At the end of the year, the Internal Revenue Service (IRS) in the US might look at your global income and say: “Hey, you made a massive profit selling real estate. You owe us Capital Gains Tax in the US too!”

If you are not careful, you could end up paying tax to both the Indian government and the US government, completely destroying your profit.

The Solution: Double Taxation Avoidance Agreement (DTAA)

India has signed special treaties called DTAAs with over 80 countries, including the US, the UK, Canada, the UAE, and Australia.

The purpose of this treaty is simple: A person should not pay tax twice on the same income.

Under the DTAA, if you have already paid Capital Gains tax in India, you can claim a Foreign Tax Credit in your home country. This means when you file your tax returns in the US or UK, you can show them the receipt proving you paid taxes to the Indian government. The foreign government will subtract the Indian tax you paid from your total tax bill, saving you from double taxation.

Always consult with a tax professional in your country of residence to ensure you file the correct forms to claim these DTAA benefits!

Conclusion

Selling a property as a resident Indian is mostly about finding the right buyer and negotiating the best price. But selling a property as a Non-Resident Indian is a complex, heavily regulated tax operation.

The rules around NRI taxes on selling property in 2026 are strict, but they are not impossible to navigate. The entire system is built to reward those who plan ahead and penalize those who rush.

If you wait until the last minute, you will fall into the trap of a massive 20% or 30% TDS deduction on your total sale value, locking up your hard-earned capital for months. But if you take a deep breath, hire a competent Chartered Accountant, apply for your Form 13 Lower TDS Certificate 45 days in advance, and explore your Section 54/54EC exemptions, you can protect your wealth entirely.

Indian real estate is a fantastic asset class. By understanding the tax laws, you ensure that when it is finally time to sell, the profits stay right where they belong: in your pocket.

Frequently Asked Questions (FAQs) About NRI Property Sales

Q1: How much TDS is deducted when an NRI sells a property in India?

Unlike resident Indians who pay 1% TDS, buyers must deduct 20% TDS (plus surcharge and cess) for Long-Term Capital Gains, or 30% for Short-Term Capital Gains, when buying from an NRI.

Q2: Does the buyer deduct TDS on the profit or the total sale value?

By default, the law requires the buyer to deduct the massive TDS on the Total Sale Consideration (the full property price). To stop this, the NRI seller must obtain a Form 13 Lower TDS certificate from the Income Tax Department.

Q3: What is Form 13 and why is it so important for NRIs?

Form 13 is an application for a “Lower or Nil TDS Certificate.” It allows the Income Tax Officer to calculate your actual capital gains tax and instruct the buyer to deduct only that specific amount, protecting the NRI from massive, unfair upfront deductions on the total sale value.

Q4: Can an NRI claim exemptions to avoid capital gains tax?

Yes, absolutely! NRIs can claim exemptions under Section 54 (by reinvesting the profit into a new residential house in India) or Section 54EC (by investing the profit into specific 5-year government bonds up to ₹50 Lakhs).

Q5: How long does it take to get a Form 13 certificate?

Once your Chartered Accountant applies for it online, the Income Tax Department usually takes between 30 to 45 days to process and issue the Form 13 certificate. You must apply well in advance of the final property registration date.

Q6: What is the difference between Long-Term and Short-Term Capital Gains for property?

If you sell the property within 24 months of buying it, it is a Short-Term Capital Gain (taxed at your regular slab rate). If you hold it for more than 24 months, it becomes a Long-Term Capital Gain, which generally enjoys a lower tax rate (like 12.5% for properties bought after July 2024).

Q7: Can I transfer the property sale money directly to my US/UK bank account?

No. The buyer must first transfer the money into your Indian NRO (Non-Resident Ordinary) bank account. From there, you must complete the repatriation process to move the money abroad.

Q8: What are Form 15CA and Form 15CB?

These are mandatory documents required to transfer money out of India. Form 15CB is a certificate issued by a Chartered Accountant verifying that you have paid all necessary taxes. Form 15CA is your online self-declaration based on that CA certificate. Your bank will demand both before wiring the money abroad.

Q9: How much money can an NRI legally take out of India per year?

Under the Reserve Bank of India (RBI) guidelines, an NRI can freely repatriate up to $1 Million USD per financial year from their NRO account, provided all taxes have been cleared.

Q10: Will I be taxed in India and also in the country where I currently live?

You might be liable, but you can avoid double payment using the Double Taxation Avoidance Agreement (DTAA). If India has a DTAA treaty with your current country of residence, you can claim a “Foreign Tax Credit” so that the tax you paid in India is subtracted from your tax bill in your home country.