Quick summary: The data on gold as an inflation hedge in India is genuinely compelling over long periods. Over 41 years, gold has returned an average of 10% annually in rupees while Indian CPI inflation averaged 7.3%. When inflation rose above 6%, gold averaged 12% returns. But here is the honest part: gold does not hedge inflation every year, every quarter, or every month. In 2013 and 2014, gold fell 20 to 30% while Indian inflation was above 9%. Gold is an imperfect, long-run hedge, not a reliable short-term one. Understanding exactly when and why it works is what makes this article worth reading.

What Does “Hedge Against Inflation” Actually Mean?

Before the data, the definition. An inflation hedge is an asset that maintains or increases its purchasing power when prices rise. In other words, if everything in your basket of goods gets 6% more expensive, an asset that returned 6% is exactly an inflation hedge. An asset that returned 10% is better than an inflation hedge. An asset that returned 3% is a partial hedge. A savings account returning 2% while inflation runs at 6% is not a hedge at all.

For an Indian investor in 2026, this matters because:

- Savings account interest rates: approximately 3 to 4% per year

- Fixed deposit rates: approximately 6.5 to 7.5%, but after-tax returns at 30% slab rate come to 4.5 to 5.25%

- India’s CPI inflation target: 4%, with a 2 to 6% tolerance band

- Medical inflation in India: running at 12 to 14% annually

- Higher education inflation: typically 8 to 10% annually

If your savings are earning 4 to 5% after tax while the things you actually spend money on are getting 6 to 14% more expensive each year, you are losing ground. This is the problem gold, equities, real estate, and other growth assets all try to solve.

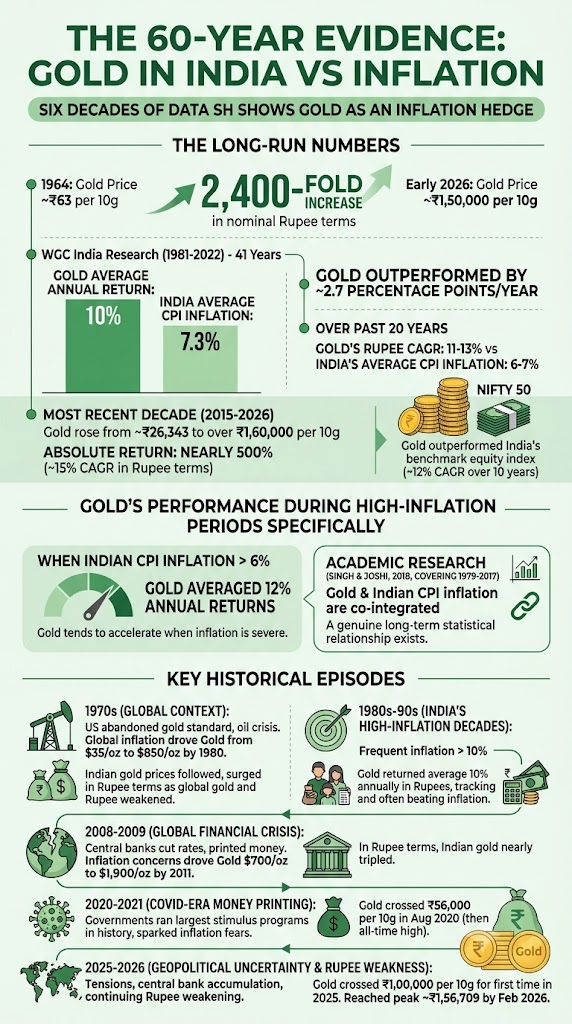

The 60-Year Evidence: Gold in India vs Inflation

The data on gold as an inflation hedge in India stretches back over six decades and covers some of the most turbulent economic periods in the country’s history.

The Long-Run Numbers

The price of gold in India moved from approximately ₹63 per 10 grams in 1964 to approximately ₹1,50,000 per 10 grams in early 2026. That is a 2,400-fold increase in nominal rupee terms over 62 years.

More specifically, the World Gold Council’s India-focused research, drawing on data from 1981 to 2022, finds that over a 41-year period, gold delivered an average annual return of 10% in rupees. India’s average CPI inflation over the same period was 7.3%. Gold outperformed inflation by approximately 2.7 percentage points per year on average.

Over the past 20 years specifically, gold’s rupee CAGR of 11 to 13% has consistently beaten India’s 6 to 7% average CPI inflation.

And over the most recent decade (2015 to 2026), gold in India rose from approximately ₹26,343 per 10 grams to over ₹1,60,000: an absolute return of nearly 500%, or approximately 15% CAGR in rupee terms. For context, the Nifty 50 delivered approximately 12% CAGR over this same 10-year period. Gold actually outperformed India’s benchmark equity index over the last decade.

Gold’s Performance During High-Inflation Periods Specifically

The World Gold Council’s India research finds that gold has historically performed best precisely when inflation is highest. When Indian CPI inflation rose above 6%, gold averaged 12% annual returns. In other words, gold does not just passively track inflation, it tends to accelerate when inflation is severe. Academic research (Singh and Joshi, 2018, covering 1979 to 2017) concluded that gold and Indian CPI inflation are co-integrated, meaning there is a genuine long-term statistical relationship between the two.

Key Historical Episodes

The 1970s (global context):

When the US abandoned the gold standard in 1971 and the oil crisis drove global inflation, gold went from $35 per ounce to $850 per ounce by 1980. Indian gold prices followed and surged dramatically in rupee terms as both global gold and the rupee weakened.

The 1980s-90s (India’s high-inflation decades):

India experienced frequent inflation above 10%. Gold returned an average of 10% annually in rupees during this period, tracking and often beating inflation.

2008-2009 (global financial crisis):

As central banks worldwide cut rates to near zero and printed money aggressively, inflation concerns drove gold from approximately $700/oz to $1,900/oz by 2011. In rupee terms, Indian gold nearly tripled in this period.

2020-2021 (COVID-era money printing):

Gold crossed ₹56,000 per 10 grams in August 2020 (then an all-time high) as governments ran the largest stimulus programmes in history, sparking inflation fears.

2025-2026 (geopolitical uncertainty and rupee weakness):

Gold crossed ₹1,00,000 per 10 grams for the first time in 2025 and reached a peak of approximately ₹1,56,709 by February 2026. Geopolitical tensions, central bank accumulation, and a continued weakening of the rupee drove this rally.

Why Gold Hedges Inflation Better in India Than Anywhere Else

Here is a fact that most gold articles skip over: Indian investors consistently get better rupee returns from gold than international investors get in dollar terms. The reason is the rupee’s structural depreciation.

The Rupee Depreciation Multiplier

Gold is priced globally in US dollars. When you buy gold in India, you buy it in rupees. If the dollar price of gold stays exactly flat for one year but the rupee depreciates from ₹83 to ₹85 against the dollar (approximately 2.4% depreciation), your gold is worth 2.4% more in rupees even though the global gold price did not move.

The rupee has depreciated from approximately ₹63 per dollar in 2015 to approximately ₹85 per dollar in 2026, a decline of 35% over 11 years. This currency depreciation has added roughly 3 to 4% per year to the rupee returns of gold for Indian investors, on top of global gold price movements. This is gold as a currency hedge as well as an inflation hedge.

Since rupee depreciation is partly driven by India’s higher inflation relative to the US and other developed economies, this effect is structurally persistent, not a temporary aberration. As long as India’s inflation exceeds that of the US (which is the historical norm), the rupee will tend to depreciate, adding to gold’s rupee returns.

The Cultural Demand Floor

India is the world’s second-largest consumer of gold. Festivals (Akshaya Tritiya, Dhanteras, Diwali), weddings, and auspicious occasions drive periodic demand spikes. This cultural demand does not disappear during inflationary periods. If anything, when people distrust the currency and financial system, physical gold demand in India increases. This creates a domestic demand floor that makes gold relatively more resilient in India than in countries where gold is purely a financial asset.

Food Inflation and the CPI Basket

India’s CPI basket has food items comprising approximately 45.9% of total weight. Food prices are volatile and often inflation is driven by food prices: vegetables, pulses, edible oils. Gold has historically responded well to spikes in food-driven inflation in India because food price spikes signal broader economic stress and purchasing power erosion. When families see onion prices triple or cooking oil double in price, gold buying increases as a store of value.

When Gold Fails as an Inflation Hedge

Here is what a serious article on this topic must not skip. Gold is not a reliable inflation hedge over every time period. Academic research (Baur, 2025, covering 1971 to 2025) confirms that gold did not consistently hedge against inflation in every month, quarter, and year. Over long time spans, gold prices vastly exceeded inflation rates. But in the short run and in specific multi-year periods, gold has significantly underperformed inflation.

The 2013-2015 Failure

Indian CPI inflation was running between 9% and 11% from 2010 to 2014 (one of the most inflationary periods in recent Indian history). Gold should theoretically have performed strongly. It did not. After peaking in 2011, global gold prices fell nearly 40% by 2015, and rupee gold prices also declined significantly despite high Indian inflation. Anyone who bought gold in 2011 expecting inflation protection was disappointed for several years.

Why the 2013-2015 Period Failed

Gold’s inflation hedge property depends critically on real interest rates. When central banks raise nominal interest rates faster than inflation rises (so real interest rates go positive or high), gold typically underperforms because:

- High real rates increase the opportunity cost of holding gold (gold pays no interest)

- Rising rates attract capital into bonds, pulling money away from gold

- A stronger dollar (which often accompanies rate hikes) makes dollar-priced gold more expensive for everyone else, reducing demand

From 2013 to 2015, the US Federal Reserve was signalling the end of quantitative easing and beginning to talk about rate hikes. This strengthened the dollar and pushed gold down globally, overriding the Indian inflation signal.

The Academic Consensus

Research consistently finds that gold is better described as a hedge against extreme inflation and financial crises than against moderate, everyday inflation. It primarily reacts to large inflation shocks, not to average inflation rates. A 4-5% inflation environment does not strongly drive gold prices. A 10%+ inflation environment or a financial crisis does.

The practical takeaway:

Do not hold gold expecting it to precisely track your monthly grocery bill. Hold gold expecting it to protect you during prolonged crises, currency collapses, and severe inflation spikes. Over 10 to 20 year periods, this protection is statistically well-supported. Over 1 to 3 year periods, it is unreliable.

Gold vs Other Inflation Hedges in India

Indian investors have multiple tools to fight inflation. Where does gold fit?

| Asset | Annual Return (10-year CAGR, approx) | Inflation Beat? | Liquidity | Tax (LTCG) |

| Gold ETF | 15% (2015-2026 in INR) | Yes, significantly | High | 12.5% after 12 months |

| Nifty 50 (equity) | 12% | Yes | High | 12.5% after 12 months |

| Fixed Deposit | 6.5-7.5% (current) | Barely, after-tax often no | Medium | Slab rate |

| PPF | 7.1% (current rate) | Marginally | Low (15-year lock) | Tax-free |

| Real Estate | Varies widely by city | Often yes, with leverage | Very low | 12.5% after 24 months |

| Savings account | 3-4% | No | Very high | Slab rate |

The verdict:

- Gold is a better inflation hedge than FDs and savings accounts over long periods

- Gold is comparable to equity over recent periods but more volatile in shorter windows

- PPF is the best tax-adjusted inflation hedge for the risk it carries, but the 15-year lock-in and ₹1.5 lakh annual cap limit how much it can absorb

- Real estate hedges inflation well but is illiquid and requires large capital commitments

Gold’s unique position: it is the only mainstream inflation hedge that is liquid (can be sold today), has no counterparty risk (unlike an FD, which depends on the bank remaining solvent), and provides currency protection (unlike all rupee-denominated instruments).

For tax-saving options that also partially hedge inflation, see ourincome tax deductions guide which covers PPF, ELSS, and NPS. For how NPS specifically protects retirement savings against inflation, see our NPS changes July 2026 guide.

Specific Inflation Scenarios and What Gold Does

Scenario 1: Moderate inflation (4-6% CPI)

Gold’s response is unpredictable over 1 to 3 years. Over 10 years, it will likely beat this inflation. Do not count on gold for short-term inflation protection at moderate rates.

Scenario 2: High food inflation (vegetable, onion, oil spikes)

Indian gold demand historically rises during food price spikes. Cultural buying increases. Gold prices in rupees tend to rise, though not in a predictable short-term ratio.

Scenario 3: Rupee depreciation (currency weakness)

Gold is the strongest hedge for this. A 10% rupee depreciation immediately adds approximately 10% to your gold’s value in rupees, all else equal. If you hold rupee-denominated savings (FDs, PPF, savings accounts), currency weakness destroys their purchasing power for imported goods. Gold protects against this.

Scenario 4: Global crisis (financial system stress, geopolitical war)

Gold’s strongest performance period. In every major global crisis since 1970, gold has been a store of value while other assets fell. This is gold’s clearest and most consistent property.

Scenario 5: Domestic monetary tightening (RBI raising rates)

Gold typically underperforms when the RBI raises rates significantly. Higher real interest rates (positive after adjusting for inflation) make gold less attractive relative to FDs and bonds. This was the experience in 2013-2015.

How Much Inflation Protection Should Come From Gold?

Given everything above, gold should be one tool in your inflation protection toolkit, not the only one. A diversified approach:

- Gold: 10% of portfolio. Long-run inflation hedge, currency hedge, crisis hedge. Held for 7 to 10+ years ideally.

- Equity (diversified mutual funds): 50 to 60% of portfolio. Best long-run inflation beater for genuine wealth growth.

- PPF/NPS: Tax-free or tax-efficient real returns; inflation-beating over 15+ years.

- Health insurance: Protects against the 12 to 14% medical inflation that no investment can predictably match. This is not an investment but a shield. See our health insurance premium guide 2026.

- FDs: For short-term (1 to 3 year) liquidity needs; not ideal for inflation protection after tax.

For the specific allocation of gold by your age and life stage, see our gold allocation by age guide. For how to invest in gold across vehicles, see our gold investment portfolio guide.

Frequently Asked Questions

1. Is gold better than an FD for fighting inflation?

Over 10 years or more, yes. Gold’s 11 to 13% CAGR in rupees over the past 20 years has significantly outpaced FD returns after tax (4.5 to 5.25% at 30% slab). Over 1 to 3 years, gold’s returns are unpredictable and can be negative while FD returns are guaranteed. For a 5-year+ horizon: gold. For a 1 to 2 year horizon: FD.

2. Why did gold fall in 2013-2015 even though Indian inflation was high?

Gold’s price is set globally in US dollars. Rising US real interest rates in 2013-2015 (as the Federal Reserve signalled the end of quantitative easing) pushed global gold prices down. This overrode India’s domestic inflation signal. Gold is an imperfect hedge because external factors (especially US monetary policy and the dollar) can dominate domestic inflation in the short run.

3. Should I buy gold to protect against rising vegetable prices?

Gold is not a month-to-month hedge against grocery bills. It is a long-run store of value. For short-term spikes in food prices, there is no investment hedge (you simply pay more for food). Gold’s protection operates over years and decades, not weeks and months.

4. Is physical gold or Gold ETF a better inflation hedge?

Both track the same underlying price, so the inflation-hedging property is identical. Gold ETF is more cost-efficient (no making charges, no storage cost, lower friction on buying and selling). Physical gold has an advantage in extreme scenarios (power outages, system failures, civil unrest) where electronic access to funds might be limited. For practical purposes in 2026, Gold ETF is the better vehicle.

5. Gold in rupees has outperformed even equity over the last 10 years. Does that mean I should hold more gold than equity?

No. The 10-year window (2015-2026) was an unusually strong period for gold driven by COVID, geopolitical tensions, rupee weakness, and central bank accumulation. Over 20 to 30 years, equity typically outperforms gold significantly in India. Gold’s job is risk reduction and inflation protection, not maximum wealth creation. Equity remains the primary wealth builder. Gold is the portfolio insurance.

6. With RBI cutting interest rates in 2025-26, is this good for gold?

Yes. Lower interest rates reduce the opportunity cost of holding gold (gold pays no interest; when everything else also pays little, gold becomes relatively more attractive). Rate cuts also tend to weaken the currency over time, adding to gold’s rupee returns. The current monetary easing cycle is supportive for gold.

Key Takeaways

- Over 41 years, gold delivered an average annual return of 10% in rupees while CPI inflation in India averaged 7.3%: a real return of approximately 2.7% per year over inflation.

- Gold averaged 12% returns when Indian inflation exceeded 6%, making it a particularly strong hedge during high-inflation episodes.

- Over the last decade (2015-2026), gold’s 15% CAGR in rupees beat even the Nifty 50’s 12% CAGR, driven partly by global gold prices and partly by rupee depreciation.

- The rupee depreciation multiplier is unique to Indian investors: 3 to 4% annual rupee weakness against the dollar adds structurally to gold’s rupee returns, on top of global price movements.

- Gold is not a reliable month-to-month or year-to-year inflation hedge. In 2013-2015, gold fell 20 to 30% while Indian inflation ran above 9%. Rising real interest rates drove this.

- Gold hedges best against large inflation shocks, currency crises, and financial system stress, not moderate everyday inflation.

- Gold should be one part of a diversified inflation defence: alongside equity for long-run growth, PPF/NPS for tax-efficient stable returns, and health insurance for medical inflation.

- For most Indian investors, 10% of the investment portfolio in gold provides meaningful inflation protection without sacrificing too much long-term compounding.

Sources: World Gold Council: Investment Update: Gold amid Higher Inflation and Rising Bond Yields in India; GoldAndIPO: Gold Price History India, 10-Year Data 2015-2026; Baur, D.G. (2025): Is Gold an Inflation Hedge? SSRN Working Paper No. 5389663; India Inflation Calculator: Gold CAGR vs CPI, 20-Year Data.

Mutual fund investments are subject to market risks. Past performance does not guarantee future returns. This article is for financial education only and does not constitute investment advice. Consult a SEBI-registered investment advisor for personalised guidance.