Quick summary: Gold has delivered one of its strongest runs in decades, surging over 67% globally in 2025 and reaching approximately ₹1.45 lakh per 10 grams domestically in 2026. If you have been wondering whether to add gold to your portfolio or increase what you already hold, the short answer most financial planners agree on is: 5% to 15% of your investment portfolio, with 10% as the most commonly cited starting point for Indian investors. Below that, gold adds little meaningful protection. Above that, it starts to drag on long-term returns. This guide explains the right allocation, how to hold gold in India, and what has changed in 2026.

Why Gold Belongs in an Indian Portfolio

Gold is not a growth asset. Over long periods, equities have significantly outperformed gold. The Nifty 50 and Sensex have compounded at rates that gold simply cannot match over 15 to 20 year horizons.

So why does every serious financial planner in India recommend some gold allocation? Four reasons specific to the Indian context:

1. It does not move with the stock market.

Gold has a low or negative correlation with Indian equities. When the Nifty or Sensex falls sharply, gold often holds its value or rises. The World Gold Council’s 2026 India research shows that gold has historically shown strong resilience during episodes of systemic risk, often delivering positive returns while limiting portfolio losses. This smoothing effect is the primary reason for holding gold.

2. It protects you when the rupee weakens.

Gold is priced globally in US dollars. When the Indian rupee depreciates against the dollar (which it has done consistently over the decades), your gold investment in rupee terms rises even if the dollar price of gold stays flat. For Indian investors in particular, gold offers an additional layer of resilience by amplifying returns during periods of rupee depreciation.

3. It is a proven inflation hedge.

When prices rise rapidly, cash loses purchasing power. Gold typically maintains its value against inflation over the long run, making it a reliable store of value across economic cycles.

4. Indians already understand gold.

With Indian households estimated to hold over 25,000 tonnes of gold, there is deep cultural familiarity with the asset. The challenge for most Indian investors is not whether to hold gold, but how to hold it efficiently and in what proportion.

How Much Gold: The 5–15% Framework

Wealth advisors typically suggest 5% to 15% depending on your risk appetite, investment horizon, and the market cycle. The sweet spot is around 10%, with tactical tilts up to 15% in uncertain phases.

This range comes from decades of portfolio research. Here is how to think about your specific number within that range:

Hold closer to 5–8% if:

- You are in your 20s or early 30s with a long investment horizon (15+ years) and a heavy equity allocation

- Your income is stable and growing, and you do not need a safety buffer

- You already have significant real estate holdings (real estate itself acts as an inflation hedge)

- You are comfortable riding out equity market volatility

Hold closer to 10% if:

- You have a balanced portfolio (mix of equity and debt)

- You are building towards a 7 to 15 year financial goal (a home purchase, a child’s higher education)

- You want portfolio insurance without sacrificing too much equity upside

Hold up to 12–15% if:

- You are in your 40s or 50s and shifting toward capital preservation

- You have a large portion of your wealth in a single asset class (like one company’s equity or one property)

- Current macro conditions are highly uncertain (elevated geopolitical tensions, currency risk)

Never go above 15–20%:

Beyond this level, gold’s non-yielding nature (gold pays no dividends, no interest) begins to meaningfully drag on your portfolio’s long-term compounding. Overweighting gold when equity is already under-allocated can slow goal progress.

One important distinction:

The 5–15% refers to your investment portfolio, not your total net worth. Gold jewellery that you wear and would never sell is not investment gold. Do not count it. Investment gold is what you hold specifically for financial returns and can liquidate when needed.

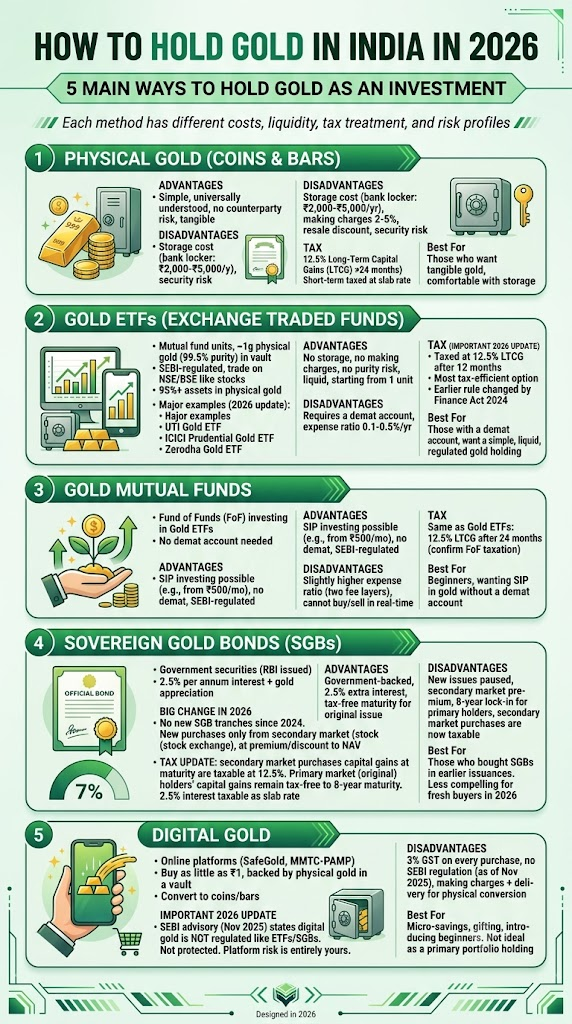

How to Hold Gold in India in 2026

There are five main ways to hold gold as an investment in India. Each has different costs, liquidity, tax treatment, and risk profiles.

1. Physical Gold (Coins and Bars)

Gold coins and bars (certified 24-karat purity) are the most direct form of gold ownership. Buying from a reputable bank (SBI, HDFC Bank, or ICICI Bank) or a certified jeweller (BIS hallmarked) ensures purity.

Advantages:

Simple, universally understood, no counterparty risk, tangible. Disadvantages: Storage cost (bank locker: ₹2,000 to ₹5,000 per year), making charges can be 2–5% on coins, resale discount at most jewellers. Security risk if stored at home. Tax: 12.5% Long-Term Capital Gains (LTCG) if held for more than 24 months. Short-term gains taxed at slab rate.

Best for:

Those who want tangible gold and are comfortable with the storage and security logistics.

2. Gold ETFs (Exchange Traded Funds)

Gold ETFs are mutual fund units that each represent approximately 1 gram of physical gold (99.5% purity) held in a vault. They are listed and traded on NSE and BSE like stocks, and their price moves in line with gold prices.

As per SEBI guidelines, at least 95% of a Gold ETF’s assets are invested in physical gold. Major Gold ETFs available in India include UTI Gold ETF (known for low tracking error), ICICI Prudential Gold ETF (large AUM of over ₹22,000 crore, highly liquid), and Zerodha Gold ETF (low expense ratio).

Advantages:

No storage concerns, no making charges, no purity risk, fully SEBI-regulated, can be bought and sold in real time during market hours, starting from 1 unit (approximately ₹900 to ₹1,500 depending on the ETF). Disadvantages: Requires a demat account. Expense ratio of 0.1% to 0.5% per year. Tax (important 2026 update): Gold ETFs are now taxed at 12.5% LTCG after 12 months. This is the most tax-efficient gold investment option in 2026. The earlier rule (20% with indexation after 36 months) was changed by the Finance Act 2024, effective July 23, 2024.

Best for:

Those with a demat account who want a simple, liquid, SEBI-regulated gold holding.

3. Gold Mutual Funds

Gold mutual funds are Fund of Funds (FoF) that invest in Gold ETFs. The key practical advantage: you do not need a demat account to invest. You can invest via SIP (Systematic Investment Plan) starting at ₹500 per month directly through an AMC or investment platform.

Advantages:

SIP investing possible, no demat account needed, SEBI-regulated.

Disadvantages:

Slightly higher expense ratio than direct Gold ETFs (since you pay two layers of fees: the FoF’s fee + the underlying ETF’s fee). Cannot be bought and sold in real time (like a regular mutual fund, priced at NAV at end of day). Tax: Same as Gold ETFs: 12.5% LTCG after 24 months (FoF taxation differs slightly; confirm with your AMC).

Best for:

Beginners who want to start a monthly SIP in gold without setting up a demat account.

4. Sovereign Gold Bonds (SGBs)

SGBs are government securities issued by the Reserve Bank of India on behalf of the Government of India, denominated in grams of gold. They offer 2.5% per annum interest (paid semi-annually) in addition to gold price appreciation.

The big change in 2026: The government has not issued new SGB tranches since 2024. New SGBs can currently only be purchased from the secondary market (stock exchange), where they trade at a premium or discount to NAV.

Tax update:

If you buy SGBs from the secondary market (stock exchange), your capital gains at maturity are now taxable at 12.5%. If you had bought SGBs from the primary market (original RBI issuance) and hold them to the 8-year maturity, the capital gains remain tax-free. The 2.5% interest is taxable as per your income slab rate in all cases.

Advantages:

Government-backed, 2.5% extra interest, original-issue holders get tax-free maturity. Disadvantages: New issues paused, secondary market prices at a premium, 8-year lock-in for primary market holders, secondary market purchases are now taxable. Best for: Those who bought SGBs in earlier issuances (very favourable product for them). Less compelling for fresh buyers in 2026 given the tax treatment change and lack of new issuances.

5. Digital Gold

Digital gold platforms (SafeGold, MMTC-PAMP) allow you to buy as little as ₹1 worth of gold online, backed by physical gold in a vault. You can also convert your digital gold balance into coins or bars delivered to your home.

Important 2026 update:

SEBI issued an advisory in November 2025 clarifying that digital gold is not regulated like ETFs or SGBs and is not protected under the same regulatory framework. The platform risk is yours entirely.

Disadvantages:

3% GST on every purchase (which eats into short-term returns), no SEBI regulation as of November 2025, conversion to physical gold involves making charges and delivery fees. Best for: Micro-savings (very small amounts), gifting, or introducing beginners to gold investing. Not ideal as a primary portfolio holding.

Gold in India 2026: What the Numbers Say

The context matters for your allocation decision. Here are the current data points from credible sources:

- Gold prices have crossed $5,000 per ounce globally and have reached approximately ₹1.45 lakh per 10 grams domestically.

- In 2025, gold surged over 67%, and the momentum continued into 2026 due to multiple structural drivers including geopolitical uncertainty and central bank accumulation.

- January 2026 gold ETF inflows hit ₹24,040 crore, nearly matching active equity inflows. This shows how seriously Indian investors are taking gold as a financial instrument rather than just a physical asset.

- The World Gold Council’s 2026 India-specific research notes that gains in Indian equities have moderated amid elevated valuations, while monetary easing has compressed yields on debt instruments, making gold stand out as a notable outperformer.

Does this mean you should rush to buy gold at current prices? Not necessarily. After a 67% rally, gold is not cheap. The right approach is to build your allocation gradually over 6 to 12 months through monthly investments (SIP in Gold ETF or Gold Mutual Fund), rather than making a large lump sum purchase at current highs.

Taxation of Gold vs Other Investments in 2026

One of the most common questions is: does it make more sense to invest in gold or in something like ELSS or NPS from a tax perspective?

| Investment | Tax Benefit at Entry | LTCG Tax | Holding Period for LTCG |

| ELSS (Equity Linked Savings Scheme) | Yes, Section 80C deduction (old regime only) | 12.5% | 12 months |

| NPS (National Pension System) | Yes, Section 80CCD(1B) up to ₹50,000 (old regime) | Withdrawal taxed differently | Long-term (till retirement) |

| Gold ETF | No | 12.5% | 12 months |

| Physical Gold | No | 12.5% | 24 months |

| Sovereign Gold Bonds (primary, original) | No | Nil (if held to 8-year maturity) | 8 years |

Gold provides no upfront tax deduction. For those maximising deductions under the old tax regime, ELSS and NPS take priority before gold. For those already maximising deductions, gold is a portfolio diversifier, not a tax tool. For more on deductions available to you, see our income tax deductions guide. For how NPS fits into your retirement strategy, see our NPS changes July 2026 guide.

Common Mistakes Indian Investors Make with Gold

Counting jewellery as investment gold.

Most families significantly overestimate their investment gold allocation because they include jewellery they would never sell. Be honest about what is truly liquid and available for rebalancing.

Buying at peaks driven by headlines.

The instinct to buy gold when its price is in the news is usually wrong. The best time to add gold is when equity markets are doing well (gold is cheaper then) and when you are rebalancing an under-allocated position.

Never rebalancing.

Letting a winning gold sleeve balloon distorts risk. Rebalance on a calendar basis every 6 to 12 months, or on a threshold basis if gold drifts more than 20% from your target allocation.

Paying high making charges on jewellery.

Making charges on gold jewellery can range from 10% to 25% of the gold value. This is a sunk cost from day one. Investment-grade gold coins and Gold ETFs have far lower entry costs.

Ignoring the SGB opportunity.

Those who bought SGBs in original issuances between 2015 and 2024 at significantly lower gold prices and hold them to 8-year maturity are sitting on tax-free gains plus 2.5% annual interest. If you hold original-issue SGBs, continue to hold them.

How to Start Building Your Gold Allocation?

If you are starting from zero:

- Step 1: Calculate your current investment portfolio value (equity mutual funds + stocks + debt funds + FDs + PPF + NPS, but exclude real estate, provident fund, and jewellery).

- Step 2: Decide on your target gold percentage (start with 10% as a default).

- Step 3: Calculate the gap. If your portfolio is ₹5 lakh and you want 10% in gold, you need ₹50,000 in investment gold.

- Step 4: Do not buy it all at once. Split the ₹50,000 into 6 to 12 monthly SIP instalments in a Gold Mutual Fund or Gold ETF.

- Step 5: Review your gold allocation every 6 months and rebalance if it has drifted more than 2 to 3 percentage points from your target. Trim if gold has risen above your ceiling; top up if it has fallen below your floor.

For platforms to start investing in Gold ETFs and mutual funds, our best money apps guide for India covers the options available on popular investment platforms.

Frequently Asked Questions

1. Does physical gold I already own count towards my portfolio allocation?

Only if it is in a form you could actually liquidate when needed (certified gold coins or bars, not jewellery with sentimental value). Be realistic. Most Indian families hold far more jewellery than investment gold. Count only what you would genuinely sell.

2. Should I switch from physical gold to Gold ETFs?

For new purchases going forward, yes, Gold ETFs are more efficient: no storage cost, no making charges, better liquidity, and the same tax rate (12.5% LTCG after 12 months). Selling physical gold attracts the same 12.5% LTCG if held over 24 months. Switching has a tax event at the point of selling the physical gold, so plan it carefully.

3. Are Sovereign Gold Bonds still worth buying in 2026?

For new investors, the SGB story is more complicated than it was before 2024. New issuances are paused. Secondary market purchases are taxable at 12.5% at maturity (not tax-free like primary issuances). At premium prices, Gold ETFs are now equally or more attractive. For those who already hold primary SGBs, hold to maturity.

4. Is it a good time to buy gold given prices are near all-time highs?

Gold prices in 2026 are elevated after a multi-year run. Timing the market in any asset class is unreliable. If you are under-allocated to gold relative to your target, start a systematic monthly investment over 6 to 12 months. This rupee-cost averages your entry price and reduces the risk of a large investment at a peak.

5. Should I prefer gold or international mutual funds for portfolio diversification?

They serve different roles. Gold is a hedge against equity market crashes and currency weakness. International mutual funds give you exposure to global economic growth. Both can coexist in a portfolio: gold for protection, international equity for diversification of growth. However, note that international fund availability is currently constrained by SEBI’s $7 billion overseas investment cap. See our international mutual funds guide for the current status.

6. How is gold taxed if sold within 12 months?

Short-term capital gains on gold (held under 12 months for Gold ETFs, under 24 months for physical gold) are added to your total income and taxed at your applicable income tax slab rate. There is no flat short-term tax rate for gold like the 20% STCG on equity.

Key Takeaways

- The recommended gold allocation for Indian investors is 5% to 15% of the investment portfolio, with 10% as the most commonly cited benchmark by SEBI-registered advisors and the World Gold Council.

- Gold’s value in a portfolio is not as a growth engine but as portfolio insurance: it protects against market crashes, inflation, and rupee depreciation.

- Gold ETFs are the most tax-efficient and cost-effective way to hold investment gold in 2026: 12.5% LTCG after 12 months, SEBI-regulated, no storage costs.

- Sovereign Gold Bonds remain excellent if you already hold primary-issue SGBs; for fresh buyers, the tax treatment change and lack of new issuances make them less compelling.

- Digital Gold is convenient for micro-savings but not ideal as a primary portfolio holding due to 3% GST and lack of SEBI regulation (as of November 2025).

- Do not count gold jewellery as investment gold unless you are genuinely willing to sell it.

- Build your gold position gradually over 6 to 12 months via SIP rather than a lump sum at current elevated prices.

- Rebalance your gold allocation every 6 to 12 months to keep it within your target band.

Sources: World Gold Council: Why Gold in 2026? An Anchor for Indian Portfolios, March 2026; Finnovate: How Much Gold Should You Hold in Your Portfolio?; Finology: Best Gold ETF in India 2026; Liquide: Best Ways to Invest in Gold in India 2026.

Mutual fund investments are subject to market risks. This article is for general information and financial education only. It does not constitute investment advice. Consult a SEBI-registered investment advisor before making portfolio decisions.