Quick summary: If your business or organisation deducts TDS from employee salaries, contractor payments, professional fees, rent, or interest, you are required by law to obtain a TAN (Tax Deduction and Collection Account Number) before you make your first deduction. Form 49B is the official application form for allotment of a TAN under Section 203A of the Income Tax Act, 1961. Without a TAN, your TDS returns will be rejected, banks will refuse your tax payment challans, and a penalty of ₹10,000 applies. This guide explains what TAN is, who needs it, who is exempt, how to fill and file Form 49B, and the key compliance consequences of not having one.

What Is TAN?

TAN stands for Tax Deduction and Collection Account Number. It is a 10-character alphanumeric identifier issued by the Income Tax Department of India to every person or entity that is required to deduct tax at source (TDS) or collect tax at source (TCS) under the Income Tax Act, 1961.

Think of it as a business-specific tax identity number specifically for TDS and TCS activity. Just as PAN is your personal income tax identifier, TAN is your deductor’s identifier. Every TDS return, TDS payment challan, TDS certificate, and official TDS-related correspondence must carry your TAN.

The Structure of a TAN Number

A TAN has a fixed format: four letters, five digits, and one letter (total 10 characters). For example: MUMR12345E

- First 3 letters (MUM): Represent the city or jurisdiction where the TAN was issued (e.g., MUM for Mumbai, DEL for Delhi, MAA for Chennai)

- 4th letter (R): The first letter of the name of the deductor or collector

- 5 digits (12345): A unique sequential number assigned to the deductor

- Last letter (E): A check digit for validation purposes

This structure means you can identify the issuing jurisdiction of any TAN just from the first three characters.

Who Must Obtain a TAN?

As per Section 203A of the Income Tax Act, every person who deducts or collects tax at source is required to obtain a TAN and quote it on all TDS/TCS returns, challans, certificates, and correspondence.

Common categories of entities that must have a TAN:

- Employers paying salary: Any company, firm, or individual paying salary above the basic exemption limit is required to deduct TDS under Section 192 and must have a TAN.

- Companies paying contractors: Entities paying contractors or sub-contractors above ₹30,000 per contract or ₹1 lakh aggregate per year under Section 194C.

- Entities paying professional fees: Companies or firms paying doctors, lawyers, architects, and other professionals above ₹30,000 per year under Section 194J.

- Entities paying rent: Any person (other than individual/HUF not in the audit category) paying rent above ₹2,40,000 per year under Section 194I.

- Banks and financial institutions: For TDS on interest, dividends, maturity proceeds, and other income.

- Government departments: All Central and State Government offices deducting TDS from salaries or payments.

- Companies paying dividends, winnings, commission, brokerage: Under the relevant sections of Chapter XVII.

- Entities collecting TCS: Sellers of specified goods (like scrap, alcohol, minerals, motor vehicles above ₹10 lakh) and specified services under Section 206C.

In essence: if a payment you make falls under any TDS or TCS provision of the Income Tax Act, you need a TAN before that payment is made.

Who Is Exempt from Obtaining a TAN?

This is a critical distinction, especially for individuals and HUFs. The Income Tax Act has created specific carve-outs where the deductor uses PAN instead of TAN. These are the same individual/HUF deductors covered by the “26Q series” of forms we covered in our earlier guides.

A person required to deduct tax under the following sections is not required to obtain a TAN and may use PAN in its place:

| Section | Who It Covers | Form Used Instead of TAN |

| Section 194-IA | Property buyers paying TDS on purchase of immovable property (₹50 lakh+) | Form 26QB |

| Section 194-IB | Individual/HUF tenants (not subject to audit) paying rent above ₹50,000/month | Form 26QC |

| Section 194M | Individuals/HUFs (not subject to audit) paying contractors or professionals above ₹50 lakh | Form 26QD |

| Section 194S | Specified persons deducting TDS on transfer of virtual digital assets | As notified |

So if you are a salaried employee buying a property and need to deduct TDS from the seller, you do not need a TAN. You file Form 26QB with your PAN. Similarly, if you pay rent above ₹50,000/month to your landlord, you deduct TDS under Section 194-IB and file Form 26QC with your PAN. No TAN is involved.

For a complete guide to the property TDS process, see our Form 26QB guide. For the rent TDS process, see our Form 26QC guide for tenants. For contractor and professional fee TDS by individuals, see our Form 26QD guide.

What Is Form 49B?

Form 49B is the prescribed application form under Rule 114A of the Income Tax Rules, 1962 for applying for a new TAN. Its full official name is: “Form of Application for Allotment of Tax Deduction and Collection Account Number under Section 203A of the Income Tax Act, 1961.”

A separate form (simply called “Form for Change or Correction in TAN Data”) is used if you want to update or correct details in an already-allotted TAN. Form 49B is only for first-time TAN applications.

What Form 49B Covers

Form 49B collects the following information from the applicant:

Category of Deductor/Collector:

The type of entity applying: Individual, HUF, Company, Central Government, State Government, Local Authority, Statutory/Autonomous Body, Partnership Firm, Association of Persons/Body of Individuals, or Artificial Juridical Person. Selecting the correct category determines how the rest of the form is structured.

Name:

Full name of the deductor/collector. For companies: the registered company name. For government departments: name of the office and ministry/department. For individuals: title (Shri/Smt/Kumari), first name, middle name, and surname.

Branch details:

Whether the TAN is being applied for the entire entity or a specific branch. A company may obtain a single TAN for all branches, or separate TANs for different branches. An individual or HUF may also obtain separate TANs for different businesses they run.

Whether applying for TDS, TCS, or both:

The form requires specifying whether the applicant is applying for TAN for tax deduction at source (TDS), tax collection at source (TCS), or both.

AO Code:

The Assessing Officer code, consisting of:

- Area Code: Identifies the city/region

- AO Type: Identifies the category of the assessing officer (e.g., Commissioner of Income Tax, Corporate Circle)

- Range Code and AO Number

The AO Code is not intuitive and must be looked up. The NSDL/Protean portal has a built-in AO Code search facility: select your state, category of deductor, and district, and the system suggests the correct AO Code. If you get this wrong, your TAN may be under the wrong jurisdictional circle, causing issues during tax assessments.

Address:

The address must be an Indian address. For branches, it is the branch address.

PAN of the applicant:

Mandatory. PAN must be mentioned if you (or the entity) have one. Without PAN, quoting Section 206AA, TDS deduction on payments to you is at a higher rate; it is similarly important for TAN-linked compliance.

Person responsible for deducting/collecting:

Name and designation of the individual who is responsible for TDS/TCS compliance (e.g., the CFO, Finance Manager, or Director). This person’s details appear on TDS certificates issued by the entity.

Contact details:

Telephone number or email ID (at least one is mandatory).

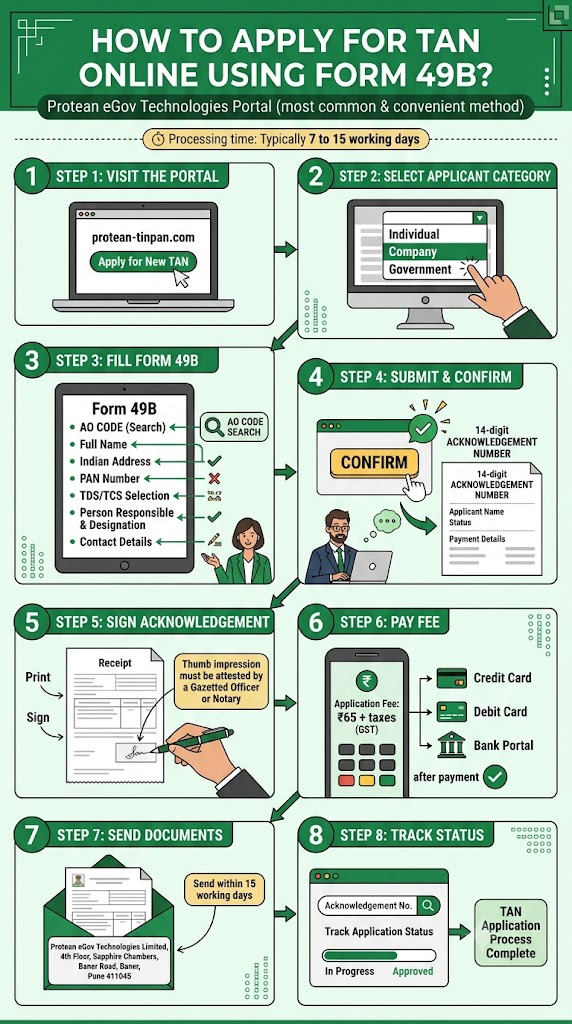

How to Apply for TAN Online Using Form 49B?

The online route through the Protean eGov Technologies portal is the most common and convenient method. Processing time is typically 7 to 15 working days.

- Step 1: Visit the Protean eGov TAN portal at protean-tinpan.com. Navigate to “Apply for New TAN.”

- Step 2: Select the applicable “Category of Deductors” from the dropdown menu (Individual, Company, Government, etc.).

- Step 3: Form 49B appears on screen. Fill in all required fields:

- AO Code (use the search function on the portal)

- Your full name or entity name

- Address (Indian address mandatory)

- PAN number

- Whether applying for TDS, TCS, or both

- Person responsible for TDS/TCS and their designation

- Contact details (phone and email)

- Step 4: Click “Confirm” to submit. An acknowledgement page appears showing a 14-digit acknowledgement number, applicant name, status, and payment details.

- Step 5: Print the acknowledgement page. Sign it in the box provided (or affix thumb impression, which must be attested by a Gazetted Officer or Notary).

- Step 6: Pay the application fee of ₹65 plus applicable taxes (GST). Payment can be made online via net banking, debit card, or credit card at the time of submission.

- Step 7: Send the signed acknowledgement to the NSDL/Protean address within 15 working days: Protean eGov Technologies Limited, 4th Floor, Sapphire Chambers, Baner Road, Baner, Pune 411045.

- Step 8: Track your application using the 14-digit acknowledgement number on the Protean portal.

How to Apply for TAN Offline?

- Step 1: Download Form 49B from the Income Tax Department website (incometaxindia.gov.in) or obtain a physical copy from any TIN-FC (Tax Information Network Facilitation Centre). A list of TIN-FC locations is available on the Protean portal.

- Step 2: Fill in the form in English, in block letters, with one character per box.

- Step 3: Sign the declaration section or affix a left-hand thumb impression (which must be attested).

- Step 4: Submit the completed Form 49B in duplicate at any TIN-FC along with the application fee (₹65 + applicable taxes).

- Step 5: The TIN-FC processes the application and the TAN is allotted within 7 to 15 working days. An acknowledgement number is provided.

No documents required for offline TAN application:

Unlike PAN card applications, no identity or address proof documents are required to be submitted with Form 49B. The Income Tax Department relies on the PAN number provided in the form to verify the identity.

Special Case: New Companies Under Incorporation

As confirmed by the Income Tax Department’s own TAN guidance, companies being incorporated for the first time can apply for a TAN simultaneously during company registration. Instead of filing a separate Form 49B, new companies can apply for TAN through the SPICe+ form (INC-32) during the MCA company registration process. This saves time by bundling TAN allotment with company incorporation.

Where TAN Must Be Quoted

Once obtained, TAN must be quoted on the following:

- All TDS and TCS returns (quarterly: Form 24Q for salary TDS, Form 26Q for non-salary TDS, Form 27Q for TDS on payments to non-residents, Form 27EQ for TCS)

- All TDS and TCS payment challans (monthly by the 7th of the following month)

- All TDS certificates issued to payees (Form 16, Form 16A, Form 16B, Form 16C)

- All applications and correspondence with the Income Tax Department relating to TDS and TCS

- TAN must also appear on all certificates, including Form 16A which is the TDS certificate for non-salary income. See our Form 16A explained guide for what these certificates contain. For salary TDS, TAN appears on Form 16. See our Form 16 Part A and Part B guide.

Penalties for Non-Compliance

The Income Tax Act provides two specific penalty provisions for TAN non-compliance:

- Section 272BB(1): A penalty of ₹10,000 for failure to apply for TAN when required or failure to comply with any provision of Section 203A.

- Section 272BB(1A): A penalty of ₹10,000 for quoting an incorrect TAN in any return, certificate, challan, or document where TAN is required.

Note that these are two separate penalties. If you do not have a TAN at all, you face Section 272BB(1). If you have a TAN but quote a wrong one (for example, a TAN belonging to another branch), you face Section 272BB(1A).

Practical consequences beyond the penalty:

- Banks will refuse to accept TDS challan deposits without a valid TAN

- TDS returns filed without TAN are rejected outright

- TDS credits do not get linked to payees’ Form 26AS without the correct TAN on the return, causing disputes and hardship for employees or vendors

TAN vs PAN: Key Differences

| TAN | PAN | |

| Full form | Tax Deduction and Collection Account Number | Permanent Account Number |

| Who needs it | Entities required to deduct or collect TDS/TCS | All persons required to pay income tax or make specified financial transactions |

| Legal section | Section 203A, Income Tax Act | Section 139A, Income Tax Act |

| Application form | Form 49B | Form 49A/49AA (now Forms 93/94/95/96 from April 2026) |

| Application portal | Protean (protean-tinpan.com) | Protean or UTIITSL |

| Structure | 10 alphanumeric (e.g., MUMR12345E) | 10 alphanumeric (e.g., ABCDE1234F) |

| Can an entity have multiple? | Yes (different TANs for different branches) | No (one PAN per entity) |

| Quoted on | TDS/TCS returns, challans, certificates | ITR, investment forms, financial transactions |

| Processing fee | ₹65 + taxes | ₹107 + taxes (domestic delivery) |

| Required for filing ITR? | No (TAN is for deductors, not for individual ITR) | Yes |

For more on the PAN application forms, see our Form 49A vs Form 49AA guide.

TAN Correction and Surrender

If you need to make changes to an existing TAN (address update, name change, new AO code after shifting premises, change of person responsible for TDS), or if you have obtained multiple TANs and want to surrender duplicates, use the separate “Form for Change or Correction in TAN Data” available on the Protean portal. This is not Form 49B.

Having more than one TAN is illegal. If you have been allotted a TAN in error or hold duplicate TANs, you must surrender the extra ones. Using multiple TANs simultaneously can cause reconciliation issues across your TDS returns and create compliance flags.

Frequently Asked Questions

1. Does every business in India need a TAN?

Any business that deducts TDS from salary, contractor payments, rent, professional fees, or any other payment covered under Chapter XVII of the Income Tax Act must have a TAN. A very small business that has no employees, does not pay contractors above the threshold, and does not make any other TDS-applicable payments may not need one. However, as soon as any TDS obligation arises, a TAN must be obtained before the first deduction.

2. Can an individual apply for a TAN?

Yes. An individual running a business with employees or making TDS-applicable payments must obtain a TAN. However, individuals who only need to deduct TDS on property purchase (Section 194-IA), rent payment (Section 194-IB), or contractor/professional payments above ₹50 lakh (Section 194M) do not need a TAN. They use PAN and the respective 26Q series forms.

3. How long does it take to get a TAN after filing Form 49B?

Typically 7 to 15 working days after the acknowledgement is sent to Protean. The TAN is sent to the address mentioned in Form 49B and/or communicated by email.

4. Can a company have multiple TANs for different branches?

Yes. A company can have separate TANs for different branches, divisions, or locations, or a single TAN for the entire company. The choice is made during Form 49B application by selecting “single TAN for entire company” or applying separately for each branch. Multiple TANs are useful for large organisations where each branch operates independently, files its own TDS returns, and issues its own certificates.

5. What happens if TDS is deducted but no TAN is quoted on the challan?

The challan will be rejected by the bank. TAN is mandatory on all TDS payment challans. If TDS was deducted but the payment cannot be deposited due to missing TAN, it creates a compliance default (interest and penalty under Section 201(1A)).

6. Is Form 49B relevant under the new Income Tax Act, 2025?

The new Income Tax Act, 2025 (effective from 1 April 2026) restructures and renumbers many provisions. The TAN requirement under Section 203A of the old Act will have a corresponding provision in the new Act. Form 49B itself may be renumbered or redesigned under the Income Tax Rules, 2026 (similar to how PAN application forms 49A and 49AA were replaced by Forms 93-96 from April 2026). For the most current form for TAN applications, always check the Protean portal and the Income Tax Department’s official notifications.

7. I run a freelance business and pay no employees. Do I need a TAN?

If you have no TDS obligations (no salary payments, no qualifying contractor or professional payments, no qualifying rent payments under Section 194I), you do not need a TAN. However, if your freelance business grows and you hire employees or make qualifying TDS-applicable payments, you must apply for a TAN before making those payments.

Key Takeaways

- Form 49B is the application form for allotment of a TAN under Section 203A of the Income Tax Act, 1961, read with Rule 114A.

- TAN is mandatory for every person or entity required to deduct TDS or collect TCS under Chapters XVII-B and XVII-BB of the Income Tax Act.

- Key exemptions: Property buyers (Section 194-IA, use Form 26QB), individual/HUF tenants (Section 194-IB, use Form 26QC), and individual/HUF payers of contractors/professionals above ₹50 lakh (Section 194M, use Form 26QD) do not need a TAN; they use PAN instead.

- TAN is a 10-character alphanumeric number (e.g., MUMR12345E) where the first three characters identify the city/jurisdiction.

- Form 49B can be filed online at the Protean eGov portal (protean-tinpan.com) or offline at any TIN-FC. Application fee: ₹65 plus applicable taxes. No supporting documents are required.

- TAN must be quoted on all TDS/TCS returns, challans, certificates, and correspondence with the Income Tax Department.

- Failure to obtain TAN or quoting an incorrect TAN both attract a penalty of ₹10,000 each under Section 272BB.

- New companies being incorporated can apply for TAN through the SPICe+ process (INC-32) without filing a separate Form 49B.

- TAN and PAN are distinct: one entity can have multiple TANs (for different branches) but only one PAN.

Sources: Income Tax Department, Government of India: Tax Deduction Account Number; Income Tax Department: Section 203A FAQ; Protean eGov Technologies: TAN Application; Vakilsearch: TAN Application in India 2026, Form 49B Online Process, June 2026.

This article is for general information only and does not constitute tax or legal advice. For guidance on your specific TDS compliance situation, consult a Chartered Accountant.