Quick summary: The short answer is yes, gold has historically protected wealth during recessions, but with an important caveat. In the initial panic phase of a severe crisis, gold can fall alongside everything else as investors sell assets to raise cash. This happened in October 2008 (gold fell from $1,000 to $700 in weeks) and in March 2020 (gold dipped briefly before surging). Investors who understood this and held through the panic captured substantial gains. Those who panicked and sold captured neither the protection nor the subsequent rally. The lesson is not that gold is a perfect recession hedge. It is that gold is a resilient one, when held with conviction over the full cycle.

What History Shows: Gold in Every Major Recession

The evidence across the past 90 years is consistent enough to take seriously.

The Great Recession: 2007 to 2009

The most instructive recent example. From December 2007 (recession start) to June 2009 (recession end):

- Gold rose from approximately $803 per ounce to $934 per ounce: a gain of roughly 16%

- The S&P 500 fell over 50% in the same period

But there is a vital detail within this period that many gold articles skip. In October 2008, when Lehman Brothers collapsed and financial markets went into full panic, gold did not hold up. It fell sharply from near $1,000 to approximately $700 per ounce in weeks. Why? A liquidity crunch. When investors panic, they sell everything to raise cash: stocks, bonds, commodities, and gold. The difference is what happened next. Equity markets continued falling. Gold reversed sharply. By February 2009, gold was back above $900 while the Nifty and Sensex were still near their lows. By 2011, gold had surged to $1,917 per ounce: a 173% gain from the October 2008 panic low.

Investors who sold gold during the October 2008 crash captured the crash, not the protection. Investors who held through it captured one of the strongest gold rallies in decades.

In India: Indian equity markets (Sensex) fell approximately 60% from January 2008 to March 2009. Gold in rupees rose from approximately ₹10,800 per 10 grams in January 2008 to approximately ₹14,500 per 10 grams by mid-2009, a gain of roughly 34% during the same period when equity lost 60%. The rupee’s weakening against the dollar during the crisis amplified gold’s rupee returns, an effect unique to Indian investors that we covered in our gold as an inflation hedge article.

The COVID Recession: 2020

The sharpest GDP contraction in modern history. Again, gold showed the same initial-panic, then-surge pattern.

In March 2020, as global markets crashed and investors scrambled for liquidity, gold briefly dipped. Then:

- From January 2020 to its August 2020 peak, gold climbed from approximately $1,520 to over $2,070 per ounce: a gain of over 36%

- For the full year 2020, gold rose 25.1%

- In India: gold surged from approximately ₹40,000 per 10 grams in January 2020 to ₹56,200 in August 2020 (then an all-time high in rupees), a gain of approximately 40%

The Sensex fell over 40% in a matter of weeks in March 2020, recovered somewhat, but the full-year performance was near flat. Gold’s 40% gain in the same year was the starkest possible contrast.

The Dot-Com Recession: 2000 to 2001

As technology stocks collapsed and the S&P 500 fell 50%, gold began a long multi-year bull market. From approximately $250 per ounce in 2001, gold rose steadily to $1,920 by 2011: a decade-long gain of nearly 670%. The recession triggered the beginning of that secular bull market, as investors exited speculative technology bets and sought tangible assets.

The 1970s Stagflation

One of gold’s strongest periods ever. When the oil crisis of 1973 and 1979 combined with high unemployment and soaring inflation (the definition of stagflation), gold went from $35 per ounce (when Nixon closed the gold window in 1971) to $850 per ounce by 1980: a 2,300% gain over nine years. Stagflation is gold’s ideal environment: recession plus inflation simultaneously.

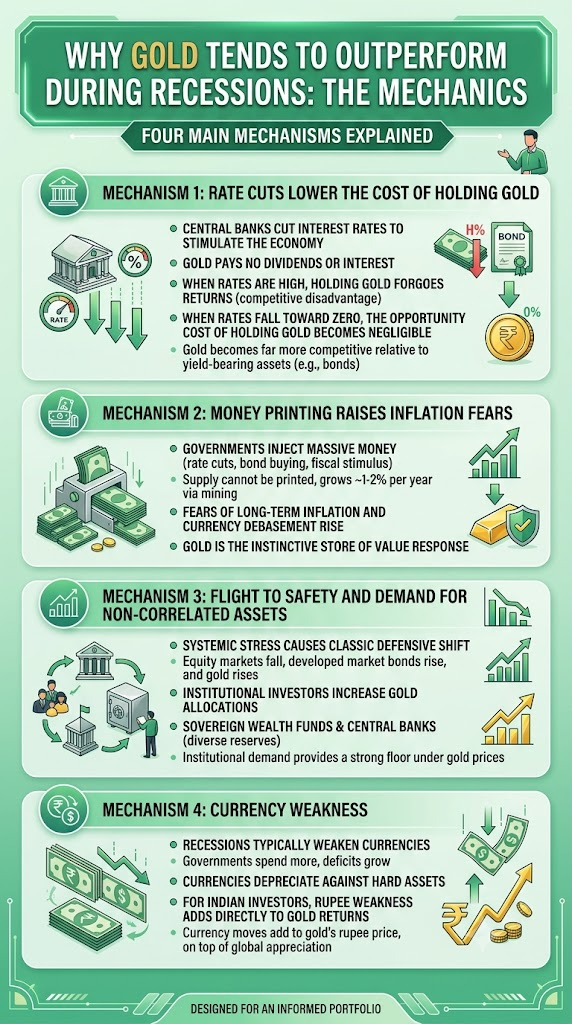

Why Gold Tends to Outperform During Recessions: The Mechanics

Understanding why gold rises during recessions is as important as knowing that it does. There are four main mechanisms.

Mechanism 1: Rate Cuts Lower the Cost of Holding Gold

Gold pays no dividend, no interest, no rent. During normal economic times, this is gold’s main competitive disadvantage: a bond or FD that yields 7% offers a tangible return that gold does not.

When recession hits, central banks cut interest rates aggressively to stimulate the economy. The RBI cut rates during 2020. The US Federal Reserve cut rates to near zero in both 2008 and 2020. When interest rates fall toward zero, the opportunity cost of holding gold (the return you forgo by holding gold instead of bonds) also falls toward zero. Gold becomes far more competitive relative to yield-bearing assets.

Mechanism 2: Money Printing Raises Inflation Fears

Central banks and governments respond to recessions by injecting massive amounts of money into the system: rate cuts, bond buying programmes (quantitative easing), fiscal stimulus packages. This expansion of the money supply raises fears of long-term inflation and currency debasement. Gold, which cannot be printed and whose supply grows by only about 1 to 2% per year through new mining, is the instinctive store of value response to this fear.

After the 2008 crisis, the US Federal Reserve expanded its balance sheet from approximately $900 billion to $4.5 trillion. After the COVID crisis, it expanded further to $9 trillion. Both episodes drove sustained gold bull markets.

Mechanism 3: Flight to Safety and Demand for Non-Correlated Assets

When equity markets fall, bonds rise (in developed countries), and gold rises. This is the classic defensive shift. Institutional investors, sovereign wealth funds, and central banks all increase gold allocations during periods of systemic stress. Central bank gold purchases hit record levels in 2022, 2023, and 2024, partly in response to geopolitical tension and partly to diversify away from US dollar reserves. This institutional demand provides a strong floor under gold prices during crises.

Mechanism 4: Currency Weakness

Recessions typically weaken currencies. Governments spend more, deficits grow, and currencies tend to depreciate against hard assets. For Indian investors, this effect is particularly powerful. The rupee weakened significantly during every Indian growth slowdown. During 2008, the rupee fell from approximately ₹39 to ₹52 against the dollar. During 2020, it fell from ₹71 to ₹77 before stabilising. These currency moves added directly to gold’s rupee returns for Indian investors, on top of the global gold price appreciation.

India’s Growth Slowdowns: Not Recessions, But the Same Gold Effect

India rarely experiences a technical recession (two consecutive quarters of GDP contraction in annual terms). But India has had multiple episodes of sharp economic stress that produced similar gold dynamics:

2008-2009:

Global financial crisis sharply affected Indian exports, manufacturing, and banking confidence. GDP growth slowed from 9% to 6.7%. Sensex fell 60%. Gold in rupees rose approximately 34%.

2012-2013:

The rupee depreciated sharply (from ₹50 to ₹68 against the dollar in a few months). Gold in rupees briefly touched ₹32,000 before correcting. This was a currency crisis episode rather than a full economic slowdown, but the gold-as-crisis-hedge dynamic operated clearly.

2020 (COVID):

India’s GDP contracted 7.3% in FY2020-21, the only genuine contraction in modern history. Gold surged. Sensex eventually recovered, but gold maintained its gains.

2025-2026 (global slowdown fears):

India’s growth is moderating from its 8%+ pace. Global tariff tensions, a slowing China, and geopolitical uncertainty are creating headwinds. Gold has surged over 67% in 2025. Central banks globally have been accumulating gold at record pace. Gold’s performance in the current environment is not accidental: it is responding precisely to the recession-risk signals the market is pricing.

When Gold Does NOT Work During Recessions: The Exceptions

Honesty requires covering the scenarios where gold underperforms even during economic weakness.

The Volcker Shock: 1980 to 1982

This is the most important counterexample. The US economy went into a severe recession in 1980-1982. By every historical precedent, gold should have held up. It did not. Gold fell from its $850 peak in January 1980 to below $300 by 1982, even as the recession deepened.

The reason: Paul Volcker, the US Federal Reserve Chairman, chose to fight inflation aggressively by raising interest rates to 20%. Real interest rates (nominal rates minus inflation) turned strongly positive. At 15-20% interest rates, bonds became extremely attractive, and the opportunity cost of holding non-yielding gold became enormous. Capital flooded into US dollar bonds, strengthening the dollar and crushing gold.

The lesson: gold underperforms during recessions when central banks fight inflation by raising rates aggressively. The opposite scenario from 2008 and 2020, where rates were cut. If a recession is accompanied by very high interest rates (a policy response to stagflation), gold’s recession-hedge property weakens.

The October 2008 Panic and March 2020 Dip

As covered above, gold briefly falls in the immediate panic phase of a crisis. This is not a failure of gold as a hedge. It is a liquidity crunch: investors sell what they can, not what they want to. Gold is liquid, so it gets sold. The protection comes to those who hold through the initial panic, not to those who sell into it.

Deflationary Recessions

If a recession brings genuine deflation (prices falling), gold’s role as an inflation hedge weakens. Cash becomes more valuable (deflation increases its purchasing power). This was partly the concern in 2008 before the stimulus programmes took hold. In practice, modern governments and central banks prevent sustained deflation through stimulus, which is why gold typically recovers quickly from deflationary initial panic.

Recession Scenarios and What Gold Does

| Recession Type | Gold’s Likely Response | Why |

| Standard recession (rate cuts, stimulus) | Rises over 6-12 months | Lower rates, money printing, risk-off demand |

| Stagflation (recession plus high inflation) | Strongest gold environment | Both the recession hedge and inflation hedge work simultaneously |

| Deflationary recession (no inflation, no stimulus) | Initially falls, may stay weak | No inflation hedge needed; cash is king |

| Policy tightening recession (high rate hikes) | Underperforms | High real interest rates make bonds more attractive than gold |

| Financial system crisis (banking collapse) | Initial dip, then strong rally | Liquidity panic first, then flight to safety |

The current global context (2026) most closely resembles a standard recession risk scenario: global growth slowing, central banks cutting or about to cut rates, geopolitical uncertainty elevated. This is the environment where gold has historically performed best.

What This Means for Your Portfolio Right Now

India is not in a recession and is unlikely to enter one given structural growth drivers. But global recession risks are elevated: US trade tensions, slowing Chinese demand, and monetary policy uncertainty create headwinds. These are precisely the conditions under which gold earns its portfolio insurance role.

Three practical implications:

Do not try to time gold around recession fears. By the time recession is formally declared (typically defined retroactively), gold has often already moved significantly. The best time to add gold to a portfolio is before a crisis, not during it. If you are already in recession, gold is expensive.

Hold through the panic. The October 2008 and March 2020 brief gold dips represent the exact wrong time to sell. Investors who sold gold at $700 in October 2008 missed gold’s recovery to $1,917 by 2011. A gold position you sell during a market panic provides no recession protection at all.

Think in terms of the full cycle, not the first three months. Gold’s recession protection is a 6 to 24-month phenomenon, not a same-day or same-week response. Patience is the primary prerequisite for gold’s recession-hedging property to work.

For your specific allocation by life stage, see our gold allocation by age guide. For the general case for gold in an Indian portfolio, see our gold investment portfolio guide.

Frequently Asked Questions

1. Did gold go up in every recession?

Not in every single recession, and not immediately in any recession. Gold briefly fell during the panic phases of 2008 and 2020 before rising strongly. During the 1980-82 US recession, gold fell sharply because the Federal Reserve aggressively raised rates to fight inflation. However, across the majority of major recessions since 1971 (when gold prices were freed from a fixed peg), gold has outperformed equities over the full recession cycle.

2. Should I buy gold now to protect against a possible recession?

If you do not already hold gold at your target allocation (5 to 15% of your investment portfolio), adding it gradually via a monthly SIP in a Gold ETF or Gold Mutual Fund makes sense as portfolio insurance regardless of recession timing. Trying to time gold purchases precisely around recession predictions is unreliable. The insurance value comes from holding it before the crisis, not buying it during the crisis.

3. What happened to gold in India specifically during the 2020 COVID recession?

Gold in rupees surged from approximately ₹40,000 per 10 grams in January 2020 to ₹56,200 per 10 grams by August 2020, a gain of approximately 40%. The rupee weakened against the dollar during the crisis, which amplified gold’s rupee returns for Indian investors on top of the global gold price gain. The Sensex fell over 40% in March 2020 before recovering.

4. Why did gold fall briefly in October 2008 if it is a safe-haven asset?

During extreme financial panics, investors sell all liquid assets to raise cash. Gold is highly liquid and was sold alongside equities in October 2008 as institutions and funds needed to meet redemptions and margin calls. This is a temporary liquidity effect, not a reflection of gold’s fundamental safe-haven properties. Gold reversed sharply once the immediate panic subsided and has recovered strongly from every such liquidity-driven dip in its history.

5. Is gold better than equity during a recession?

Over the period of the recession itself, yes, historically. During the 2008 recession, gold rose roughly 16% while equities fell over 50%. During 2020, gold rose 25% while equities crashed before recovering. However, in the recovery phase after a recession, equity typically surges and outperforms gold. The optimal strategy is to hold both: equity for long-term growth, gold as the portfolio anchor during downturns. See our gold allocation by age guide for how to balance the two across your career.

6. What about a stagflation scenario for India in 2026?

Stagflation (slow growth plus high inflation) is gold’s single strongest environment, as seen in the 1970s. India’s current trajectory is not stagflationary (inflation is moderating), but if food inflation spikes and global growth slows simultaneously, the conditions could tilt in that direction. Gold’s 67% rise in 2025 was partly driven by global stagflation fears, especially regarding the US economy. For Indian investors, this makes a 10 to 12% gold allocation particularly timely as an insurance position.

Key Takeaways

- Across every major recession since the 1970s, gold has outperformed equities over the full recession cycle. In 2008, gold rose roughly 16% while equities fell 50%. In 2020, gold gained 25 to 40% (in rupee terms) while equities crashed.

- Gold briefly falls during the initial panic phase of a severe crisis (October 2008, March 2020) as investors sell everything for liquidity. This is temporary. Investors who held through the panic captured the full recovery and subsequent rally.

- Stagflation is gold’s best environment: recession plus inflation simultaneously. The 1970s gold rally from $35 to $850 per ounce occurred during exactly this scenario.

- The exception is policy-tightening recessions: when central banks raise rates aggressively to fight inflation (the 1980-82 Volcker shock), gold underperforms even during economic weakness because high real interest rates make bonds more attractive.

- For Indian investors, rupee weakness during recessions amplifies gold’s rupee returns above and beyond global gold price movements, making gold a particularly effective recession hedge in the Indian context.

- The current global environment (2026): slowing growth, geopolitical tensions, and rate-cutting central banks is the classic setup where gold has historically delivered its recession-protection properties.

- Hold gold before the recession, not during it. Add it steadily via SIP. And hold through the inevitable panic dip, because patient holders have been rewarded in every major recession on record.

Sources: USA Gold: Gold During Recessions: Historical Performance and Strategy, March 2026; GoldSilver.com: How Gold Performs in Recessions: What History Tells Us, March 2026; Metals Mint: Gold: Safe Haven Demand Driving Prices; Attica Gold: Gold Price History in India, 60+ Years Historical Data, March 2026.

This article is for financial education and general information only. Past performance of any asset does not guarantee future returns. Consult a SEBI-registered investment advisor before making portfolio decisions.