Quick summary: When equity markets get choppy, most Indian investors instinctively think of two “safe” alternatives: gold and debt mutual funds. But these two assets behave very differently during volatility, and conflating them is a common mistake. Debt funds are designed to preserve capital and deliver steady, modest, predictable returns regardless of what is happening in equity or gold markets. Gold is a genuinely different animal: it can surge sharply during a crisis (as it did in 2008 and 2020), sit flat for years, or occasionally fall alongside equities during acute liquidity panics. This guide explains exactly how each asset behaves when markets get volatile, the current 2026 tax treatment (which has become notably less favourable for debt funds since 2023), and how to decide which one deserves a place in your portfolio right now.

What Exactly Is a Debt Fund and How Does It Behave in Volatility?

A debt mutual fund invests in fixed-income instruments: government securities, corporate bonds, treasury bills, and commercial paper. Instead of buying shares in companies, you are effectively lending money to governments and corporations in exchange for a defined interest return.

Debt funds come in several categories suited to different needs:

- Liquid funds: Invest in instruments maturing within 91 days. Extremely low volatility, near-instant redemption. Best for parking money you might need at any time.

- Ultra-short duration funds: Slightly longer maturity, marginally higher returns than liquid funds, still low volatility.

- Corporate bond funds: Invest in high-quality corporate debt, offering relatively steady returns with modest credit risk.

- Gilt funds: Invest primarily in government securities, offering high safety but with price fluctuations driven by interest rate movements.

How debt funds behave when equity markets crash:

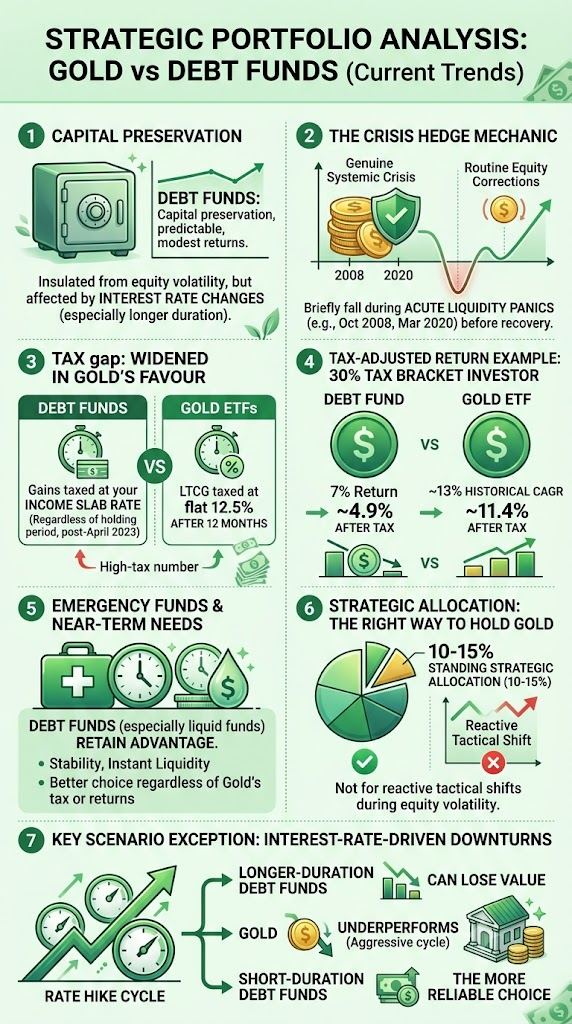

Generally, debt fund NAVs are far more stable than equity NAVs during a market crash. When the Sensex falls 20% in a month, a liquid fund or short-duration debt fund typically shows minimal to no decline, and may even continue posting small positive daily returns, because bond interest continues to accrue regardless of stock market sentiment.

The exception:

Longer-duration debt funds and gilt funds are sensitive to interest rate changes, not equity market volatility. If a market crash is accompanied by the RBI cutting interest rates (a common policy response to slow growth or a crisis), long-duration gilt funds can actually gain value, since bond prices rise when interest rates fall. Conversely, if inflation forces the RBI to raise rates during a period of stress, longer-duration debt fund NAVs can dip modestly.

Does Gold Actually Rise During Every Market Crash?

Not always, and this is where many investors get the comparison wrong. Gold’s behaviour during volatility is more complex than debt funds’ behaviour.

In genuine crisis-driven volatility (2008, 2020):

Gold has historically performed strongly. During the 2008 financial crisis, gold rose roughly 16% while equities fell over 50%. During the 2020 COVID crash, gold rose 25% to 40% (in rupee terms) for the full year while equities were volatile.

In the initial liquidity panic phase of a severe crisis:

Gold can briefly fall alongside equities, as investors sell everything, including gold, to raise cash. This happened in October 2008 (gold fell from around $1,000 to $700 per ounce in weeks before recovering sharply) and briefly in March 2020.

In moderate, non-systemic equity volatility (a 10-15% correction driven by valuation concerns, not a full crisis):

Gold’s reaction is much less predictable. It may rise modestly on risk-off sentiment, stay flat, or even decline if the correction is accompanied by a strengthening dollar or rising global interest rates.

The key distinction: gold responds most reliably to severe, systemic crises and currency or inflation concerns, not to routine equity market corrections. A 10% Nifty correction due to earnings disappointments or valuation resets does not reliably move gold in either direction. A genuine financial crisis, currency collapse, or geopolitical shock does.

Which Asset Actually Preserves Capital Better During a Downturn?

This depends on what kind of downturn you are worried about.

For a routine equity market correction (10-20% Nifty decline over a few months):

Debt funds are the more reliable capital preserver. Liquid and short-duration debt funds barely move regardless of equity volatility. Gold’s response to routine corrections is inconsistent, as explained above.

For a genuine systemic crisis (2008-style financial crisis, currency crisis, geopolitical shock):

Gold has historically not just preserved capital but significantly grown it, while debt funds preserve capital but do not typically deliver outsized gains (barring a sharp rate-cut-driven rally in long-duration funds).

For an interest-rate-driven downturn (RBI raising rates sharply to fight inflation):

This is where debt funds, particularly longer-duration ones, can actually lose value temporarily, since bond prices fall when rates rise. Short-duration and liquid funds are much more insulated from this risk. Gold’s behaviour during rate-hike cycles has historically been mixed to negative, since higher real interest rates increase the opportunity cost of holding a non-yielding asset like gold. The 1980-1982 period, when the US Federal Reserve raised rates aggressively, is the clearest historical example of gold underperforming during a recession because of rate hikes.

The practical framework:

If your primary concern is a short-term equity wobble and you need your money to sit safely, debt funds (particularly liquid or short-duration) are the more predictable choice. If your primary concern is a deep, systemic crisis (banking collapse, currency devaluation, geopolitical war), gold has the stronger historical track record.

How Are Gold and Debt Funds Taxed Differently in 2026?

This is where the comparison has changed significantly in recent years, and it materially affects the after-tax decision.

Debt Fund Taxation (Post April 2023 Rule)

For debt mutual fund units purchased on or after April 1, 2023, all capital gains, whether the units are held for one month or ten years, are taxed entirely at your income tax slab rate. There is no long-term capital gains benefit and no indexation, regardless of how long you hold the fund. This rule was introduced by the Finance Act, 2023 and continues to apply for FY 2025-26 (AY 2026-27) under Section 50AA and Section 2(42A) of the Income Tax Act, 1961.

This is a major disadvantage compared to the earlier regime (pre-April 2023), where debt funds held over 36 months qualified for LTCG at 20% with indexation, often resulting in very low effective tax.

For someone in the 30% tax bracket, a debt fund that returns 7% pre-tax now delivers approximately 4.9% after tax, regardless of the holding period. There is no reward for patience with debt funds anymore, from a tax perspective.

Note: Debt units purchased before April 1, 2023 continue to enjoy the older, more favourable LTCG treatment (20% with indexation after 36 months) if still held. This “grandfathering” only applies to pre-April 2023 purchases.

Gold Taxation (Post July 2024 Rule)

Gold’s tax treatment, by contrast, has become relatively more favourable in comparison:

- Gold ETFs: 12.5% flat LTCG after just 12 months of holding (a listed asset). STCG at slab rate if sold within 12 months.

- Physical gold, gold coins, gold mutual funds (Fund of Funds): 12.5% flat LTCG after 24 months. STCG at slab rate if sold within 24 months.

Gold ETFs, in particular, now enjoy a meaningful tax advantage over debt funds. A gold ETF investor in the 30% slab who holds for over 12 months pays only 12.5% on the gain, versus a debt fund investor in the same bracket paying 30% on the gain regardless of holding period.

The After-Tax Comparison

| Debt Fund (any holding period, post-April 2023 units) | Gold ETF (held over 12 months) | |

| Pre-tax return (illustrative) | 7% | 13% (10-year approx. CAGR) |

| Tax rate | Slab rate (up to 30%+cess) | 12.5% flat |

| After-tax return (30% slab) | ~4.9% | ~11.4% |

This tax gap is a genuinely important factor that many investors overlook when comparing gold and debt funds purely on the basis of “safety.” Gold’s post-tax return advantage for investors in higher tax brackets is now substantial, on top of its historically stronger long-term returns.

For more detail on how income tax slabs affect this calculation, see our income tax slabs guide.

Does Gold or Debt Fund Provide Better Income During Volatile Periods?

Debt funds have an advantage here that gold cannot match: they generate consistent, quantifiable income through interest accrual, which shows up as steady NAV appreciation. If you need to draw a predictable amount periodically (through a Systematic Withdrawal Plan), a debt fund is structurally suited for this because its returns are smoother and less dependent on market timing.

Gold produces no income at all. Its entire return comes from price appreciation, which is unpredictable in the short term. Gold is not a suitable instrument for anyone needing regular income or a Systematic Withdrawal Plan during a specific period, since you might be forced to sell during a price dip.

Which Should You Hold for Your Emergency Fund?

For an emergency fund specifically, liquid debt funds remain the superior choice over gold, for reasons distinct from the broader volatility discussion:

- Liquid funds have essentially no volatility and near-instant redemption (usually credited within 24 hours, sometimes with an instant redemption facility up to ₹50,000 per day).

- Gold ETF redemption takes a couple of working days for settlement, and the sale price is subject to whatever the market is doing that day, which can occasionally be an inconvenient time to sell (a temporary price dip during exactly the crisis that also created your emergency need).

- Debt fund NAVs do not experience the sharp day-to-day swings that gold can, even during severe crises.

Gold’s role is portfolio insurance for wealth preservation over years, not a substitute for the liquid, stable emergency reserve that a debt or liquid fund provides.

Should You Shift From Equity to Gold or Debt During Volatility?

This is the question most investors are really asking when they compare gold and debt funds “during market volatility”: should I move money out of equity and into one of these two options when markets look shaky?

The case against tactical shifting in general:

Timing market volatility is notoriously difficult. Moving out of equity into gold or debt during a downturn, and moving back into equity once things “look better,” tends to lock in losses and miss the recovery, which often happens faster and with less warning than investors expect.

If you must reduce equity exposure temporarily (genuine need for capital in the near term):

Debt funds, particularly liquid or short-duration funds, are the more appropriate parking spot. You are not trying to make a directional bet; you are trying to preserve capital predictably until you need it.

If your goal is structural portfolio insurance against systemic risk (not a short-term tactical move):

A standing 10 to 15% allocation to gold, maintained through calm and volatile periods alike, has historically provided better protection during genuine crises than shifting in and out of debt funds reactively. The key word is standing: gold works best as a permanent strategic allocation, not a market-timing tool.

The best-practice approach combines both, for different reasons:

- Debt funds (short-duration, liquid): for your emergency fund and near-term goals, regardless of market conditions

- Gold: as a standing 10 to 15% allocation for long-term crisis protection and inflation hedging

- Equity: as your core, long-term wealth-building engine, held through volatility rather than exited during it

For how to think about the right gold allocation at different life stages, see our gold allocation by age guide. For more on gold’s specific behaviour during recessions, see our gold during recession guide.

What Does the Broader Asset Allocation Picture Look Like in 2026?

A comprehensive comparison of asset classes for 2026 shows equities remaining a high-risk, high-return category, offering long-term returns of around 12 to 15%, with high liquidity and strong wealth creation potential, though volatility remains elevated. Cash and fixed deposits remain the safest instruments, delivering 5 to 7% returns with high liquidity and minimal volatility, but their low inflation-hedging capability limits their effectiveness for real wealth creation. From a taxation perspective, equities and equity-oriented funds continue to benefit from relatively favourable capital gains tax structures, while debt instruments and fixed deposits are taxed at slab rates, reducing post-tax returns. Real estate and gold fall in the mid-range with long-term capital gains tax implications.

This broader picture reinforces the specific gold vs debt fund comparison: debt funds sit at the lower-risk, lower-return, tax-disadvantaged end of the spectrum, best suited for capital preservation and predictable near-term needs. Gold occupies a genuinely different niche: moderate long-term returns, meaningful crisis-period upside, favourable current tax treatment, but with return unpredictability that makes it unsuitable as a primary capital-preservation tool for short-term needs.

Frequently Asked Questions

1. If gold has better long-term returns and better tax treatment than debt funds, should I just hold gold instead of debt funds?

No. They serve different purposes. Debt funds (particularly liquid funds) provide the stability, predictability, and instant liquidity needed for an emergency fund and near-term goals. Gold’s returns are far less predictable over 1 to 2 year periods and are not suitable for money you might need on short notice. Use debt funds for stability and near-term needs; use gold for long-term crisis protection and inflation hedging.

2. My debt fund lost value even though the stock market did not crash. Why?

This is likely a longer-duration debt fund or gilt fund reacting to rising interest rates, not equity market volatility. When the RBI raises interest rates, existing bond prices fall (since new bonds offer higher yields, making older, lower-yielding bonds less attractive), and this is reflected in the NAV of longer-duration debt funds. Liquid and short-duration funds are much less sensitive to this effect.

3. Does gold protect against a stock market crash caused by rising interest rates?

Not reliably. Gold’s crisis-hedge property works best during systemic financial crises, currency collapses, or extreme geopolitical shocks, not specifically during interest-rate-driven equity corrections. In fact, gold has historically underperformed during periods of aggressive rate hikes (such as 1980-1982 in the US), because higher real interest rates make yield-bearing assets more attractive relative to gold.

4. What is the after-tax difference between gold and debt funds for someone in the 20% tax bracket?

A debt fund earning 7% pre-tax delivers approximately 5.6% after tax at the 20% slab (regardless of holding period, under the post-April 2023 rule). A Gold ETF earning approximately 13% CAGR (10-year historical average) delivers approximately 11.4% after tax if held over 12 months (taxed at the flat 12.5% LTCG rate). The gap is significant, even before accounting for gold’s historically higher raw returns.

5. Are all debt funds equally safe during volatility?

No. Liquid funds and ultra-short duration funds are the safest and most stable, with minimal price fluctuation regardless of market conditions. Corporate bond funds carry modest credit risk (the possibility that a bond issuer defaults). Gilt funds and long-duration funds carry interest rate risk and can show meaningful NAV swings when interest rates move, even though the underlying government securities carry no credit risk. Choose the debt fund category based on your specific need: liquid funds for emergency funds, corporate bond or gilt funds for slightly longer horizons with an understanding of interest rate risk.

6. If markets are volatile right now, should I move my equity SIP money into gold temporarily?

Generally not advisable as a reactive, short-term tactic. Trying to time an exit from equity into gold during a downturn and a re-entry once markets recover is very difficult to execute successfully and often results in missing the recovery. A better approach is maintaining a standing gold allocation (10-15% of your portfolio) at all times, rather than shifting allocations reactively based on short-term market movements.

Key Takeaways

- Debt funds are designed for capital preservation and predictable, modest returns. They are largely insulated from equity market volatility but can be affected by interest rate changes (particularly longer-duration funds).

- Gold’s crisis-hedge property is strongest during genuine systemic crises (2008, 2020) but is unreliable during routine equity corrections and can even briefly fall during acute liquidity panics (October 2008, March 2020) before recovering.

- The tax gap has widened significantly in gold’s favour: debt fund gains (post-April 2023 units) are taxed entirely at your income slab rate regardless of holding period, while Gold ETF LTCG is taxed at a flat 12.5% after just 12 months.

- For a 30% tax bracket investor, a 7% debt fund delivers approximately 4.9% after tax, while a Gold ETF’s approximately 13% historical CAGR delivers approximately 11.4% after tax.

- For emergency funds and near-term needs, debt funds (especially liquid funds) remain the better choice due to their stability and instant liquidity, regardless of gold’s tax or return advantages.

- Gold works best as a standing strategic allocation (10-15% of portfolio) rather than a reactive tactical shift during periods of equity volatility.

- Interest-rate-driven downturns are the key exception: longer-duration debt funds can lose value when rates rise, and gold has historically underperformed during aggressive rate-hike cycles, making short-duration debt funds the more reliable choice in that specific scenario.

Sources: Business Today: Equity vs Debt vs Gold, What’s the Best Asset Class for 2026 Investors?, May 2026; ClearTax: Debt Mutual Fund Taxation in India, April 2026; Finnovate: Taxation of Gold in India, October 2025; HDFC Life: Debt Fund Tax Rules 2026, June 2026.

This article is for general financial education only and does not constitute investment advice. Past performance does not guarantee future returns. Consult a SEBI-registered investment advisor before making portfolio decisions.