Quick summary: A persistent myth circulates among Indian salaried employees: that your EPF account stops earning interest if you do not transfer it within three years of switching jobs. This is not true under the current rules. According to the EPFO’s own official clarification, at present, all accounts will earn interest up to 58 years of age of a member, regardless of whether contributions have stopped. That said, leaving your EPF untransferred is still not a good idea, for reasons that have nothing to do with this particular myth. This guide explains exactly what does and does not happen to your EPF when you leave it behind after a job switch, and why transferring remains the smarter move despite the interest continuing.

Does Your EPF Really Stop Earning Interest After 3 Years of No Contribution?

This is the single most important myth to clear up, because it drives a lot of unnecessary panic.

This myth isn’t random. It comes from an old rule window that applied between 2011 and 2016. During that period, EPF accounts that did not receive contributions for 36 months were classified as inoperative, and interest was genuinely stopped on those accounts, specifically to discourage people from leaving old accounts unclaimed and to nudge them toward transferring or withdrawing.

That rule changed. Following a 2016 amendment, and confirmed through subsequent government clarifications, EPF accounts continue to earn interest even without new contributions, all the way until the member turns 58 years of age. The EPFO’s own official FAQ page states plainly: at present, all accounts will earn interest up to 58 years age of a member.

So if you switched jobs in 2020 and never transferred your EPF balance, that account has continued to earn the applicable EPF interest rate every year since, exactly as if it were an active, contributing account, right up until now, and will continue to do so until you turn 58.

Why the myth persists: old blog posts, forum threads, and word-of-mouth advice from the pre-2016 era continue to circulate. Many people who searched for this answer years ago still carry outdated information, and it gets repeated in casual conversation and even in some outdated financial content online.

What Does “Inoperative” or “Dormant” Actually Mean for an EPF Account?

Your EPF account can still be classified as inoperative or dormant, and this classification is real, but it does not mean what most people assume it means.

An account is classified as an inoperative account when contribution has not been received for 3 years after retirement, permanent migration abroad, or death of the member. This is a narrower and more specific definition than simply “changed jobs and stopped contributing.”

Critically, an account can be dormant (no fresh contributions) simply because you switched jobs and have not transferred it, while still being fully active for interest-earning purposes. The “inoperative” classification specifically concerns accounts where the underlying reason for non-contribution is retirement, migration abroad, or death, not merely an unfilled job transition.

For most salaried employees who switch jobs within India and simply forget to transfer, the old account keeps earning interest normally and remains fully accessible. It is not locked, frozen, or forfeited.

When Does an EPF Account Actually Stop Earning Interest?

There is exactly one trigger for interest actually stopping: the member turning 58 years of age, if the balance has not been withdrawn by then. After 58, if the amount remains unclaimed and un-withdrawn, interest accrual stops.

There is a second, much longer-term consequence to be aware of: if an account remains completely neglected for more than 7 years (with no claim, no withdrawal, no contact from the member), the balance can be transferred to the Senior Citizens’ Welfare Fund, at which point it stops earning interest through the standard EPF mechanism entirely, although it may still be reclaimable through a separate process.

So the realistic risk timeline looks like this:

- 0 to 3 years after last contribution: Account continues earning full EPF interest normally. No issue.

- 3+ years, if you are still working (job switch scenario): Interest continues. The account is not classified as inoperative in the retirement/migration/death sense, since you are still employed elsewhere.

- Until age 58: Interest continues to accrue on the balance regardless of contribution status.

- After age 58, if unclaimed: Interest stops accruing.

- After 7+ years of complete neglect: Risk of transfer to the Senior Citizens’ Welfare Fund.

If Interest Doesn’t Stop, Why Does It Still Matter Whether You Transfer?

This is the more important question, and it is where the “does interest stop” myth actually distracts from the real, practical reasons to transfer your EPF promptly.

Reason 1: The Five-Year Continuous Service Rule for Tax-Free Withdrawal

Generally, the entire EPF balance is tax-free if you withdraw it after completing five years of continuous service. This five-year period is calculated from the date you joined your first employer, not from each individual job. It can be continued when switching jobs, simply by transferring the EPF balance to the new employer.

If you do not transfer, and instead let your old EPF sit separately while starting a fresh EPF account with your new employer (or worse, withdraw the old one), you may inadvertently break the continuity of this five-year clock for tax purposes. If you transfer your EPF balance to the new employer, it is not treated as a withdrawal and remains tax-free, and your service period continues for the purpose of the five-year rule.

Practically: if you have 3 years of service with Employer A and then join Employer B, transferring your EPF means your continuous service clock keeps running toward the 5-year tax-free threshold. If you leave the old account untransferred and separately withdraw it later (perhaps out of confusion or convenience), that withdrawal could be treated as premature and become taxable, since it may not independently meet the 5-year threshold.

Reason 2: EPS (Pension) Continuity

Your EPF contribution includes a portion that goes into the Employees’ Pension Scheme (EPS), which builds your eventual pension entitlement. Pension eligibility calculations depend on your total years of contributory service being tracked continuously under a single, unified record. If you leave old EPF accounts scattered and untransferred across multiple employers, reconciling your total pensionable service at retirement becomes significantly more complicated, and there is a real risk of undercounting your service years if records are not properly linked.

Usually, transferring to your current UAN is better for long-term benefits and pension eligibility, precisely because it consolidates this service record cleanly.

Reason 3: KYC and Contact Information Decay

The longer an old EPF account sits untouched, the more likely it is that your registered mobile number, email address, or bank account details on that specific account have become outdated, especially if you changed your phone number or bank in the interim. This can make withdrawals more difficult later, particularly if the previous EPF account did not comply with KYC requirements or did not have current bank or Aadhaar information linked. When you eventually do need to access the funds (an emergency, a large purchase, retirement), you may find yourself stuck in a documentation and verification loop that a timely transfer would have avoided entirely.

Reason 4: Multiple Accounts Are Harder to Track and Reconcile

Even though each individual account keeps earning interest correctly, having your retirement savings fragmented across three, four, or five old employer accounts (a common outcome for someone who has changed jobs several times over a decade) makes it much harder to get a clear, single picture of your total retirement corpus. Consolidation through transfer gives you one number to track, one passbook to check, and one account to manage as you plan your retirement.

Reason 5: Risk of Forgetting Entirely

The most mundane but very real risk: people genuinely forget about old EPF accounts, especially from a first or second job many years in the past. If you eventually forget your old UAN, lose track of your old employer’s establishment details, or lose access to the mobile number and email registered against that account, recovering it becomes a genuinely time-consuming bureaucratic process involving EPFO grievance portals, physical visits to EPFO offices, and documentation requests. Transferring promptly when the details are fresh in your mind avoids this entirely.

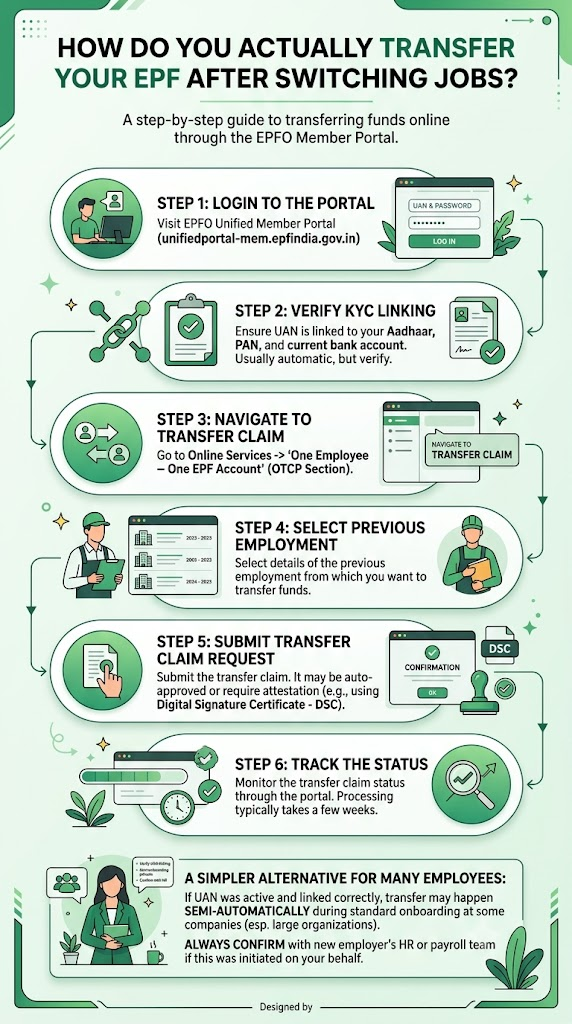

How Do You Actually Transfer Your EPF After Switching Jobs?

The process is done entirely online through the EPFO Member Portal, provided your UAN (Universal Account Number) is active and linked correctly.

- Step 1: Log into the EPFO Unified Member Portal (unifiedportal-mem.epfindia.gov.in) using your UAN and password.

- Step 2: Ensure your UAN is linked to your Aadhaar, PAN, and current bank account. This is typically done automatically when your new employer processes your joining, but it is worth verifying.

- Step 3: Navigate to the “One Employee – One EPF Account” (Online Transfer Claim Portal, OTCP) section under Online Services.

- Step 4: Select the previous employment details from which you want to transfer funds. The portal will show your service history linked to your UAN.

- Step 5: Submit the transfer claim request. Depending on whether Digital Signature Certificate (DSC) verification is available with your current or previous employer, the request may be auto-approved or may require attestation.

- Step 6: Track the status of the transfer claim through the portal. Processing typically takes a few weeks, though this can vary.

A simpler alternative for many employees: if your UAN was already active and correctly linked when you joined your new employer, the transfer may happen semi-automatically as part of the standard onboarding process at many companies, particularly larger organisations with dedicated HR/payroll compliance teams. Always confirm with your new employer’s HR or payroll team whether this has been initiated on your behalf.

What If You Have Multiple Old, Untransferred EPF Accounts From Several Jobs?

If you have changed jobs multiple times over the years and have several old, untransferred EPF accounts scattered across different UANs or under different establishment codes, you can still consolidate them, though it takes a bit more effort:

- First, check whether you have multiple UANs (this can happen if a previous employer generated a fresh UAN for you instead of linking to an existing one). If so, you need to first get the duplicate UANs merged through an EPFO grievance request.

- Once you are confirmed to have a single, correctly linked UAN, use the same Online Transfer Claim Portal (OTCP) process to pull each old account’s balance into your current, active EPF account one at a time.

- For very old accounts (from jobs a decade or more in the past) where records or contact details may be outdated, you may need to visit the relevant EPFO regional office in person or file a grievance through the EPFiGMS portal for manual assistance.

Is It Ever Better to Withdraw Instead of Transfer?

In most cases, no, transferring is the better move if you are still employed and building a career, because it preserves the tax-free five-year continuity, keeps your pension record clean, and consolidates your retirement corpus.

Withdrawal makes more sense only in specific situations:

- You are permanently leaving formal employment (retiring, moving abroad permanently, or transitioning entirely to self-employment with no further EPF contributions expected)

- You are unemployed for a continuous period of more than two months, in which case a full withdrawal is permitted under EPFO rules

- You have a genuine, immediate need that qualifies for an EPF advance (medical emergency, home purchase or construction, marriage, or education), which allows partial withdrawal while keeping the rest of the balance intact and continuing to earn interest

Withdrawing your EPF before completing five years of continuous service can trigger tax liabilities on the employer’s contribution and the interest earned, so this should not be treated as a convenient way to access cash unless one of the above genuine circumstances applies. For more on how EPF withdrawal is taxed, our income tax deductions guide covers the broader framework of how retirement savings interact with your tax return.

What Is Changing With EPFO 3.0?

The EPFO has been rolling out modernisation reforms under what is commonly referred to as EPFO 3.0, aimed at making transfers, withdrawals, and claims significantly faster and more automated. Key elements include more system-driven processes for claims, transfers, and other services with minimal manual intervention, intended to enable faster processing and less paperwork, alongside relaxed documentation requirements for certain types of withdrawals.

For employees who have been putting off transferring old EPF accounts because the process felt cumbersome, these ongoing reforms are gradually reducing that friction. It remains worth checking the EPFO portal periodically, since the process has been actively improving through 2025 and 2026.

Frequently Asked Questions

1. I switched jobs 4 years ago and never transferred my EPF. Have I lost the interest for these years?

No. Under the current rules, confirmed by the EPFO’s own official FAQ, your account has continued earning interest normally throughout this period, since interest accrues on all accounts until the member reaches 58 years of age, regardless of whether fresh contributions are being made. You have not lost any interest due to the delay in transferring.

2. Is my old EPF account safe if I never transfer it?

Yes. The Provident Fund enjoys protection against attachment by any court, as per Section 10 of the EPF & Miscellaneous Provisions Act, 1952. Your balance remains secure and continues to earn interest. The main risks of not transferring are practical ones (documentation decay, fragmented tracking, and complications with the tax-free continuity rule), not a risk of the money itself being lost or frozen.

3. Does not transferring affect my EPF pension (EPS) amount?

It can, indirectly, if it leads to your total pensionable service years not being correctly and continuously tracked across employers. Pension eligibility and calculation depend on your cumulative years of contributory service being properly linked. Transferring keeps this record clean and continuous, reducing the risk of a shortfall being identified only at retirement, when it is much harder to correct.

4. If I withdraw my old EPF instead of transferring, will it be taxed?

It depends on your total continuous service. If your combined service (old employer plus any prior linked employment) already exceeds 5 years at the time of withdrawal, it is generally tax-free. If it does not, the employer’s contribution and the interest portion can become taxable, and TDS may apply if the withdrawal amount exceeds ₹50,000 and your total service is under 5 years. Transferring rather than withdrawing avoids this risk entirely by preserving continuity toward the 5-year threshold.

5. How do I check if my old EPF account is still earning interest?

Log into the EPFO Unified Member Portal using your UAN and check your passbook for that specific account (or the linked service history under your UAN). The passbook shows year-by-year interest credits. If your UAN is properly linked across all your employment history, you should be able to see all your service history and corresponding balances in one place.

6. I have two different UANs from two different jobs because I wasn’t told my existing UAN. What should I do?

This is a common issue and needs to be resolved before you can transfer and consolidate your balances cleanly. Raise a grievance through the EPFiGMS portal (or visit your nearest EPFO office) requesting a UAN merger. Once merged into a single UAN, you can use the standard Online Transfer Claim Portal to consolidate all your old account balances into your current active account.

7. Should I prioritise transferring my EPF, or is it a low-priority task?

It is worth doing sooner rather than later, mainly because your details (UAN, linked mobile, bank account, employer records) are freshest and easiest to verify shortly after a job switch. The interest itself is not at risk regardless of when you transfer, but the administrative ease of doing it drops the longer you wait, especially if you change jobs again before getting around to it, since you would then be tracking two untransferred accounts instead of one.

Key Takeaways

- The most common belief, that EPF interest stops after 3 years of no contribution, is outdated. This was true only under a 2011-2016 rule that has since been amended. Under current EPFO rules, all EPF accounts earn interest until the member turns 58, regardless of whether contributions have stopped.

- An “inoperative” EPF account classification specifically applies to accounts with no contribution for 3 years following retirement, permanent migration abroad, or death, not simply a job switch where you continue working elsewhere.

- Interest genuinely stops only after age 58 if the balance remains unclaimed, and accounts neglected for more than 7 years risk being transferred to the Senior Citizens’ Welfare Fund.

- Despite interest continuing, transferring remains the smarter move for five practical reasons: preserving the 5-year continuous service rule for tax-free withdrawal, keeping your EPS pension record continuous and accurate, avoiding KYC and contact detail decay, consolidating your retirement corpus for easier tracking, and reducing the risk of forgetting the account entirely.

- The transfer process is done through the EPFO Unified Member Portal’s Online Transfer Claim Portal (OTCP), and is often partially automated by your new employer’s HR/payroll team during onboarding.

- Your EPF balance is legally protected from court attachment under Section 10 of the EPF & Miscellaneous Provisions Act, 1952, so an untransferred account is not at risk of being lost, only at risk of the practical complications described above.

Sources: Employees’ Provident Fund Organisation (EPFO): Official FAQs; Kustodian.Life: Does PF Interest Stop After 3 Years? EPFO Rules for Inactive Accounts Explained, 2026; Stable Money: Inoperative EPF Accounts, Reasons and Reactivation, October 2025; Poonawalla Fincorp: How Is EPF Withdrawal Taxed in India in 2026?, April 2026.

This article is for general information only and does not constitute financial or tax advice. For guidance specific to your EPF account or service history, consult the EPFO Member Portal or a qualified financial advisor.