Quick summary: Gold and real estate are India’s two most emotionally significant assets. The data on raw price appreciation clearly favours gold: according to a 2025 FundsIndia study, gold delivered a CAGR of 15% over 20 years, while real estate returned 7.8% and debt returned 7.6%. But this comparison is incomplete. Real estate offers rental income, leverage, and home loan tax benefits that gold cannot match. A ₹25 lakh investment in gold stays ₹25 lakh in gold. A ₹25 lakh down payment on real estate controls a ₹1 crore property. The leverage effect changes the return calculation entirely. This guide gives you the honest, complete comparison: returns, costs, taxes, liquidity, leverage, and who should choose what.

Has Gold Actually Outperformed Real Estate in India?

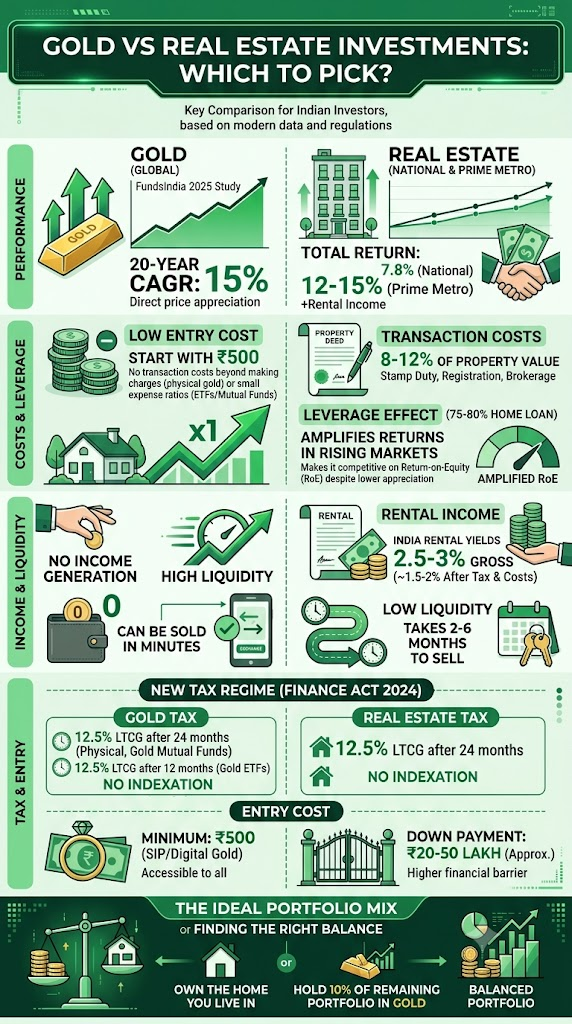

Over the last 20 years, gold’s CAGR was approximately 14 to 15% while real estate’s CAGR was approximately 7.7 to 7.8%, according to multiple data sets including the FundsIndia 2025 study and RBI gold price data.

Gold rose from ₹26,343 to ₹1,60,000 per 10 grams between 2015 and 2026, an absolute return of nearly 500%, or approximately 15% CAGR. For context, the Nifty 50 delivered approximately 12% CAGR over the same period, fixed deposits returned 6 to 7%, and real estate, depending on city and location, returned 8 to 10%.

The national average tells one story. Real estate prices rose at an average annual rate of just 3.94% over the past decade, based on data from urban apartment price trends. Rental yields from real estate remained at a modest 2.5 to 3%.

But averages can be misleading. Real estate, particularly in metropolitan cities like Bangalore, Hyderabad, and Mumbai, has historically offered 12 to 15% annualised returns when you combine rental income and property appreciation. Residential property prices in Bangalore, for example, appreciated by over 150% between 2010 and 2024.

This is the fundamental tension in the comparison: at the national average level, gold has clearly outperformed residential property. In specific high-growth urban locations, real estate has been competitive or better. The outcome depends heavily on which city, which neighbourhood, and which decade you pick.

Why Are Real Estate Transaction Costs So Much Higher Than Gold?

This is the aspect most real estate vs gold comparisons skip entirely, and it is critical.

When you buy a property in India, you pay:

- Stamp duty: 3% to 7% of the property value, varying by state (Maharashtra: 5%; Karnataka: 5%; Tamil Nadu: 7%; Delhi: 4-6%)

- Registration fees: Approximately 1% of the property value

- Brokerage: Typically 1% to 2% of the property value paid to the broker (buyer side)

- Legal and due diligence fees: ₹10,000 to ₹50,000 for document verification, title search, and property lawyer

- Home loan processing fees: 0.5% to 1% of the loan amount if you take a loan

In total, the upfront transaction costs of buying a property are 8% to 12% of the property value. On a ₹50 lakh property, you spend ₹4 to ₹6 lakh before you even own the property. This is money you need to recover through price appreciation before you break even.

When you sell, you also pay:

- Another 1% to 2% in brokerage (seller side)

- Advance tax or capital gains tax on profits (12.5% LTCG after 24 months under Finance Act 2024)

- Potential TDS by the buyer (1% if property value exceeds ₹50 lakh; covered in our Form 26QB guide)

Gold’s transaction costs, by comparison:

- Gold ETF: 0.1% to 0.5% annual expense ratio, plus broker brokerage of approximately 0.1% per trade (buy and sell)

- Physical gold coins: 2% to 5% buy-sell spread, no registration or stamp duty

- No annual property tax, no maintenance, no brokerage on sale except market price

A property that appreciates 10% in a year may actually net you only 6 to 8% after transaction costs are factored in. Gold at 10% appreciation nets approximately 9.5 to 9.9% after minimal costs. This gap compounds significantly over time.

Does Leverage Make Real Estate a Better Investment Than Gold?

Gold’s biggest structural disadvantage is that you cannot lever it efficiently. You can get a gold loan at 65% to 75% of the gold value from banks, but the rate is typically 9% to 12%, and you must repay interest in cash.

Real estate, however, is uniquely suited to leverage. Banks offer home loans at 8% to 9.5% interest (for purchase of residential property), covering 75% to 80% of the property value. You bring a 20% to 25% down payment and control the entire asset.

The leverage example:

You invest ₹25 lakh as a down payment on a ₹1 crore apartment. The property appreciates 10% in a year, to ₹1.1 crore.

Your gain is ₹10 lakh on an investment of ₹25 lakh: that is a 40% return on equity, before accounting for EMI payments and interest costs.

Now compare: if you had invested ₹25 lakh in gold at 15% annual return, your gain would be ₹3.75 lakh, a 15% return on your ₹25 lakh.

Leverage dramatically amplifies real estate returns in a rising market. The flip side: in a falling or stagnant market, leverage amplifies losses and you still owe the EMI regardless of what the property is worth.

Leverage is the primary reason why real estate has made many wealthy Indian investors very wealthy in the past 20 years, particularly in Mumbai, Bengaluru, and Delhi-NCR, even though the headline price appreciation of property (7-8% nationally) looks lower than gold’s headline appreciation (15% CAGR).

Does Real Estate Generate Better Income Than Gold?

Gold produces zero income. No rent, no dividend, no interest. The only return from gold is price appreciation.

Real estate generates rental income, but rental yields from real estate in India have remained at a modest 2.5 to 3%.

At current property prices in Indian metros, rental yields are low by global standards. A ₹1 crore flat in Bengaluru might rent for ₹25,000 to ₹35,000 per month (₹3 to ₹4.2 lakh per year), a yield of 3% to 4.2%. After property tax, maintenance society charges, and occasional vacancy, the effective net yield is closer to 2% to 3%.

However, in emerging Tier-2 cities or near infrastructure corridors, rental yields can be higher relative to current property prices. Areas near IT parks, educational institutions, or new metro stations can generate 4% to 5% yields.

Rental income is taxable under “Income from House Property” at your income tax slab rate, after a standard deduction of 30% on the gross rent. For someone in the 30% tax bracket, the effective post-tax yield on a 3% rental income is approximately 1.6% to 2%.

This rental income, though modest, is real cash in hand, something gold fundamentally cannot offer unless you specifically use a gold leasing scheme (available through some digital gold platforms, but a more complex and niche arrangement).

How Are Gold and Real Estate Taxed Differently in 2026?

Both gold and real estate saw significant tax changes from July 23, 2024 under the Finance Act, 2024. This is important context many comparisons miss.

Before July 23, 2024:

- Physical gold LTCG: 20% with indexation after 36 months

- Real estate LTCG: 20% with indexation after 24 months

After July 23, 2024 (current rules for AY 2026-27):

- Physical gold LTCG: 12.5% flat without indexation after 24 months

- Gold ETF LTCG: 12.5% flat without indexation after 12 months

- Real estate LTCG: 12.5% flat without indexation after 24 months

The removal of indexation from real estate is particularly significant. Indexation previously allowed sellers to inflate their “purchase price” by the inflation index, reducing the taxable gain substantially. With indexation gone, real estate LTCG is now taxed at 12.5% on the raw nominal gain.

This change made both assets equal in their capital gains tax treatment. A property that you bought for ₹50 lakh and sold for ₹1 crore (₹50 lakh gain) now attracts ₹6.25 lakh in LTCG tax. Previously with indexation, the tax would have been lower.

Tax benefits on a home loan (only under the old tax regime):

- Section 24(b): Up to ₹2 lakh per year deduction on home loan interest (self-occupied property)

- Section 80C: Principal repayment of home loan (within overall ₹1.5 lakh 80C limit)

Gold offers no such upfront tax deduction. For more on how to claim deductions on your ITR, see our income tax deductions guide.

Which Is More Liquid: Gold or Real Estate?

This is perhaps the starkest difference between the two assets.

- Gold (ETF): Can be sold any business day during market hours. Settlement in two working days. Proceeds in your bank account in 48 hours. Transaction cost: 0.1% brokerage plus exchange fees.

- Physical gold (coins/bars): Can be sold at a jeweller or bank on the same day, with a 3% to 5% price discount to the spot price.

- Real estate: Selling a property involves finding a buyer (weeks to months), negotiating price, signing a sale agreement, paying stamp duty and registration, getting buyer home loan approval (if applicable), and transferring the title. The entire process takes 2 to 6 months under ideal conditions. Legal disputes or title issues can extend this to years.

Gold is highly liquid. You can buy or sell it in various forms fairly easily and quickly. This liquidity gap matters enormously in crisis situations. If you need ₹5 lakh urgently for a medical emergency, you can sell Gold ETF units in 24 hours. You cannot sell a flat in 24 hours. This makes gold a superior emergency reserve asset and crisis hedge.

How Does RERA Change the Real Estate vs Gold Decision?

A genuine improvement in India’s real estate market is worth acknowledging. The Real Estate Regulatory Authority (RERA), established under the Real Estate (Regulation and Development) Act, 2016, has brought significant transparency and accountability:

- Builders must register projects with RERA before launching sales

- Delivery timelines are legally enforceable

- Funds collected from buyers must be held in a separate escrow account

- Dispute resolution mechanisms are established

RERA has materially reduced the risk of builder defaults and project delays, which were among the major concerns discouraging investment in under-construction properties. Digital land records in many states have also improved title clarity.

This regulatory improvement is a genuine argument in real estate’s favour for the 2026 investment environment. Real estate is more trustworthy now than it was in 2010 or 2014. That said, legal disputes, delayed registrations, and quality concerns still exist and require individual due diligence before any property purchase.

Gold vs Real Estate: A Direct Comparison

| Dimension | Gold ETF | Real Estate (residential) |

| 20-year CAGR (India) | ~15% | ~7.8% nationally; 12-15% in prime metros |

| Income generation | Zero | Rental yield ~2.5-3% |

| Entry cost | ₹500 minimum (SIP) | ₹20-50 lakh minimum (down payment) |

| Transaction cost | ~0.1% (buying + selling) | 8-12% upfront (stamp duty, registration, brokerage) |

| Liquidity | Instant (same business day) | 2-6 months minimum |

| Leverage | Not practically available | 75-80% loan-to-value (8-9.5% rate) |

| Maintenance | Near zero (expense ratio only) | 1-3% of value annually |

| Tax (LTCG, post July 2024) | 12.5% after 12 months | 12.5% after 24 months |

| Home loan tax benefits | None | Section 24(b) and 80C (old regime only) |

| Currency hedge | Yes (linked to USD/global gold price) | No (entirely rupee-denominated) |

| Inflation hedge | Strong over long term | Variable (depends on rental growth vs inflation) |

| Risk of legal dispute | None | Title disputes, builder delays, tenant conflicts |

| Divisibility | Can sell any fraction | Cannot sell one room; all-or-nothing |

Should You Choose Gold or Real Estate for Long-Term Wealth?

The framing of gold vs real estate as competitors for the same investment slot is flawed. Most Indian investors who own a home do not think of it as an investment; it is where they live. The real comparison is between investment gold (ETF) and investment real estate (a second property bought purely for returns).

On that basis:

Choose real estate (second property for investment) if:

- You are in a high-growth city (Bengaluru, Hyderabad, Pune, Chennai) where micro-market selection can deliver 10%+ price appreciation

- You have the capital for a meaningful down payment (₹20 lakh+)

- You can manage the illiquidity and are not likely to need those funds for 7 to 10 years

- You want rental income that can grow over time and beat inflation in that locality

- You understand property law, RERA regulations, and are willing to do due diligence on the title

Choose gold (ETF) if:

- You want a genuinely liquid portfolio hedge that does not require a 5-10 year lock-in

- Your capital is under ₹10 to ₹20 lakh and cannot justify a full property

- You want exposure across locations (gold is global; one property is one location)

- You want protection during crises and rupee depreciation

- You want zero maintenance, no tenant disputes, and instant exit

The practical truth: Most Indian middle-class families should own the home they live in (a real estate investment with lifestyle utility) and hold 10% of their remaining investment portfolio in gold for diversification and crisis protection. These are not alternatives. They serve different financial purposes.

For more on gold’s role in a portfolio by age, see our gold allocation by age guide.

Frequently Asked Questions

1. Gold has outperformed real estate over 20 years. Should I stop buying property?

Not necessarily. Price appreciation is only one dimension. Real estate with leverage (home loan) dramatically changes the return calculation. If you buy a ₹1 crore property with ₹25 lakh and it appreciates 10%, your return on equity is much higher than gold at 15% on your ₹25 lakh. The leverage effect is real estate’s core advantage that raw CAGR comparisons do not capture.

2. Rental yields in India are very low (2-3%). Is rental property still worth it?

In prime locations with strong infrastructure (IT corridors, metro-connected areas), rents have been rising faster than property prices, gradually improving yields. But for most Indian residential property at current valuations, rental yield alone does not justify the investment. The bet must be on price appreciation plus yield together, over a 7 to 10 year horizon.

3. I want to diversify from FDs. Should I buy gold or real estate?

If your total investable corpus is under ₹25 to ₹30 lakh, Gold ETF is the more practical choice: instant liquidity, no maintenance, no legal complexity, and lower entry barrier. Real estate at that corpus level means taking on a large loan for a modest property, with all the associated risks. For a deeper comparison of gold and FDs specifically, see our gold vs fixed deposits guide.

4. Does the removal of indexation benefit (Finance Act 2024) hurt real estate more than gold?

Real estate sellers who held properties for a long time had benefited significantly from indexation. The Finance Act 2024 change is therefore more impactful for long-hold property investors. Gold ETF investors holding for 12 to 24 months are now more favourably treated (12.5% vs the old complexity). The change broadly equalised the capital gains treatment of both assets.

5. My parents say land always beats gold. Are they wrong?

Agricultural land and land in the path of urban expansion have historically delivered extraordinary returns in India. Agricultural land near cities that get rezoned, or land in industrial corridors, can outperform gold by a large margin. However, this is a highly selective, concentrated, and illiquid bet requiring local knowledge, legal diligence, and long holding periods. For most urban salaried investors, the comparison is between residential property and gold, not raw land.

Key Takeaways

- Gold delivered a CAGR of 15% over 20 years vs real estate’s 7.8% nationally, according to FundsIndia’s 2025 study. However, prime metro real estate has returned 12-15% total when rental income is included.

- Real estate’s transaction costs of 8-12% of property value in stamp duty, registration, and brokerage are a major drag on net returns that raw CAGR comparisons ignore.

- Real estate’s leverage effect (75-80% home loan) dramatically amplifies returns in rising markets, making it potentially competitive with gold on a return-on-equity basis despite lower price appreciation.

- Rental yields in India are modest (2.5-3% gross; approximately 1.5-2% after tax and costs) but provide real cash income that gold cannot.

- Gold wins on liquidity: can be sold in minutes; real estate takes 2-6 months.

- Gold wins on entry cost: start with ₹500; real estate requires ₹20-50 lakh down payment.

- Tax treatment is now equal: both gold and real estate attract 12.5% LTCG after 24 months (gold ETFs after 12 months) with no indexation, following Finance Act 2024.

- For most Indians, the question is not gold or real estate, but the right mix: own the home you live in, hold 10% of your remaining portfolio in gold, and build wealth through equity.

Sources: FundsIndia Research: Gold Outperforms Equities and Real Estate Over 20-Year Period, December 2025, as reported by Geosquare.in; GoldAndIPO.com: Gold Price History India 10-Year Chart 2015-2026, April 2026; Address Advisors: Real Estate vs Gold, July 2025; Holistic Investment: Stocks vs Funds vs Gold vs Real Estate, Last 10 Years Returns Analysis, April 2026; SPJ Group: Gold vs Real Estate India Long-Term Wealth, February 2026.

This article is for general financial education only and does not constitute investment advice. Both gold and real estate are subject to market risks. Consult a SEBI-registered investment advisor or qualified real estate professional before making investment decisions.