Quick summary: TIS stands for Taxpayer Information Summary. Think of it as a short, clean summary sheet that adds up all your income under a few simple categories, salary, interest, dividend, and so on. It is built from a longer, more detailed document called AIS (Annual Information Statement). This guide explains TIS using real numbers and simple examples, so you understand exactly what you are looking at when you open it.

What Is TIS, in One Line?

TIS takes all the detailed entries in your AIS and adds them up by category. Instead of showing you 15 separate FD interest entries from 3 different banks, TIS simply shows you one number: total interest income, ₹42,000.

This makes TIS much easier to read than AIS. AIS is the detailed version, showing every single transaction. TIS is the summary version, showing only the totals.

The information flows in this order:

Form 26AS → AIS → TIS → Your pre-filled ITR

The Two Numbers TIS Shows You

For every category, TIS shows two figures side by side. Understanding the difference between these two is the whole point of this article.

1. Processed value. This is the total the tax department’s computer system calculated automatically, after removing duplicate entries. For example, if your bank reported your FD interest twice by mistake, the system removes the duplicate and shows you the correct, single total.

2. Derived value. This is the final total, after taking into account any feedback you gave. If you told the system that one entry was wrong, or did not belong to you, the derived value adjusts to reflect that. This derived value is the one used to pre-fill your ITR.

In simple words: the processed value is “what the computer thinks is correct.” The derived value is “what the computer thinks is correct, after also listening to you.”

Example 1: Salary Income

Rohit works at a private company in Pune. His employer reports his salary through the TDS return.

- In AIS: Rohit sees one detailed entry, “Salary received from XYZ Pvt Ltd, ₹8,40,000, TDS deducted ₹45,000.”

- In TIS: Under the category “Salary,” Rohit simply sees:

- Processed value: ₹8,40,000

- Derived value: ₹8,40,000

Since there is only one employer and no errors, both values are the same. Rohit’s ITR will show ₹8,40,000 as his salary income, pre-filled automatically.

Example 2: Interest Income With a Duplicate Entry

Priya has fixed deposits in two different branches of the same bank.

- The bank accidentally reports her FD interest twice in its filing, once as ₹18,000 and once again as the same ₹18,000, due to an internal reporting error at the bank’s end.

- In AIS: Priya sees two separate entries for the same ₹18,000, making it look like she earned ₹36,000 total.

- In TIS: The system’s de-duplication rules catch this and remove the double-counted entry.

- Processed value: ₹18,000 (the system has already corrected the duplicate)

- Derived value: ₹18,000

This is exactly why TIS is useful. It catches this kind of double-counting automatically, so Priya does not need to worry about her interest income appearing twice in her ITR.

Example 3: A Genuine Error That Needs Your Feedback

Anil sees a strange entry in his AIS: “Cash deposit ₹12,00,000” under his PAN, from a bank he has never opened an account with.

This is clearly a mistake, perhaps someone else’s transaction got linked to Anil’s PAN by error.

- In TIS, before Anil takes any action:

- Processed value: ₹12,00,000

- Derived value: ₹12,00,000 (since no feedback has been given yet, the derived value simply matches the processed value)

- Anil logs into the AIS section, finds this entry, and submits feedback marking it as “Not related to me.”

- In TIS, after Anil’s feedback is recorded:

- Processed value: ₹12,00,000 (this does not change, since it just reflects what was originally reported)

- Derived value: ₹0 (this changes, because Anil’s feedback has now been factored in)

Notice something important: the processed value stays exactly the same. It is simply a record of what was reported. Only the derived value changes, and it is the derived value that gets used to pre-fill Anil’s ITR. This means Anil’s ITR will correctly show ₹0 for this specific entry, protecting him from being taxed on money that was never his.

Example 4: Dividend Income From Multiple Companies

Meena holds shares in four different companies and received dividends from all of them during the year.

- In AIS, she sees four separate entries, one for each company, showing the exact company name and dividend amount for each.

- In TIS, under the category “Dividend,” she sees just one combined number:

- Processed value: ₹22,500 (the total of all four dividends added together)

- Derived value: ₹22,500 (since Meena has no disputes with any of these entries)

When Meena files her ITR, the pre-filled dividend income field shows ₹22,500 directly, without her needing to manually add up four separate numbers herself.

Example 5: A Capital Gains Entry That Needs Checking

Suresh sold mutual fund units during the year. Both his fund house (the AMC) and the registrar (CAMS or KFintech) reported the same transaction separately, a known, common issue with capital gains reporting.

- In AIS, Suresh sees the same redemption reported twice, once from the AMC and once from the registrar.

- In TIS, the system’s de-duplication rules are designed to catch this, but capital gains transactions are more complex than simple interest or dividend entries, so duplication sometimes still slips through.

- Processed value: ₹3,60,000 (this may incorrectly include both reported entries if the system’s automatic de-duplication did not catch this specific overlap)

- Derived value: ₹3,60,000 (still matching the processed value, since Suresh has not yet reviewed and corrected it)

What Suresh should do: go into the detailed AIS entries under the capital gains category, identify the duplicate, and submit feedback marking one of the two entries as “Information is duplicate.” Once this feedback is processed, the derived value in TIS will correct itself to show the true, single amount of ₹1,80,000.

This example shows why capital gains entries, especially from mutual fund redemptions, deserve extra-careful checking in TIS before you file, since duplication here is a genuinely common issue.

What Categories Does TIS Actually Show?

TIS organises your entire financial year into simple, standard categories. The most common ones you are likely to see are:

- Salary

- Interest income (savings account, fixed deposits, recurring deposits)

- Dividend income

- Sale of securities and mutual funds (capital gains)

- Sale of immovable property

- Purchase of immovable property

- Business receipts (if applicable)

- GST turnover (if you are GST registered)

- Foreign remittances

- Tax payments (advance tax, self-assessment tax)

- TDS and TCS details

Not every category will apply to every person. A salaried employee with a couple of FDs will mostly see just two or three categories with actual numbers; everything else will show as zero or simply not appear.

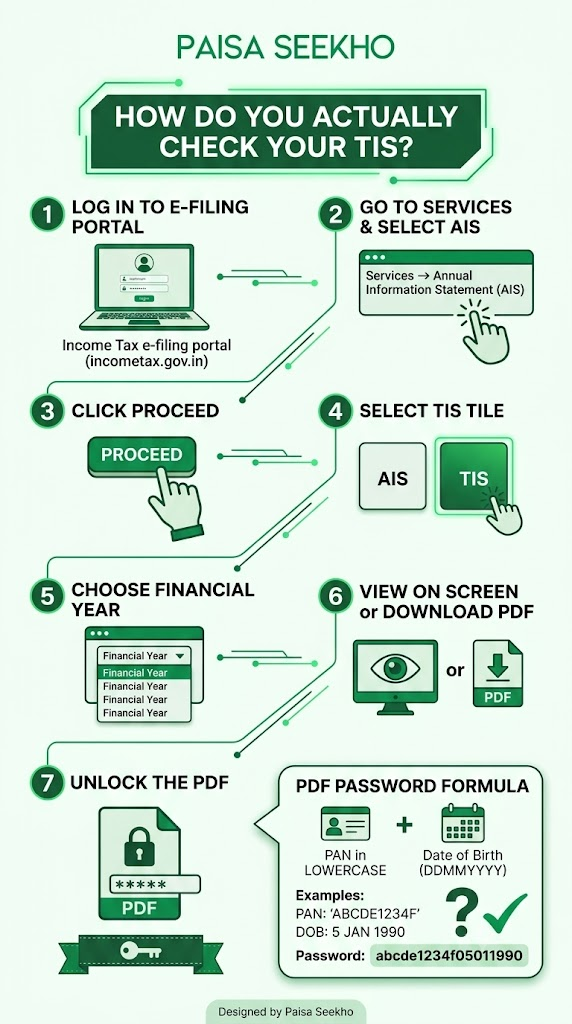

How Do You Actually Check Your TIS?

- Log in to the Income Tax e-filing portal at incometax.gov.in

- Go to Services, then click Annual Information Statement (AIS)

- Click Proceed

- You will see two tiles: AIS and TIS. Click on the TIS tile

- Choose the relevant financial year

- You can view it on screen, or download it as a PDF

The PDF password is your PAN number in lowercase, followed immediately by your date of birth in DDMMYYYY format, with no space. For example, if your PAN is ABCDE1234F and your date of birth is 5 January 1990, the password would be abcde1234f05011990.

Why Should You Bother Checking TIS Before Filing?

Because the derived value shown in TIS is exactly what gets automatically pre-filled into your ITR. If TIS shows a wrong number, your pre-filled ITR will carry that same wrong number forward, unless you catch it and fix it first.

Checking your TIS before you start filling your ITR takes just a few minutes, and it helps you in three ways:

- You confirm all your real income is being captured correctly

- You catch any duplicate or wrongly-linked entries before they cause a problem

- You avoid a mismatch notice later, since the tax department automatically compares what you declare in your ITR against what TIS shows

What Should You Do If You Disagree With a TIS Entry?

You cannot edit the TIS directly. Instead, you go to the detailed entry in AIS (not TIS), find the specific transaction, and submit feedback there. Common feedback options include:

- “Information is correct”

- “Information is not fully correct”

- “Information relates to a different PAN or year”

- “Information is duplicate”

- “Information is denied”

Once you submit this feedback in AIS, the derived value in TIS updates to reflect it, usually the same day or within a short time. You can then re-check TIS to confirm the correction has gone through before you file your return.

Frequently Asked Questions

1. What is the difference between AIS and TIS?

AIS is the detailed statement, showing every individual transaction reported against your PAN, one entry at a time. TIS is the summary, adding up all those entries into one clean total for each category, like salary or interest. AIS is for checking the fine details. TIS is for a quick, category-wise overview.

2. Which value should I trust, processed or derived?

The derived value is the more accurate one for filing purposes, since it reflects any corrections you have made through your AIS feedback. However, always double-check both values against your own actual records, bank statements, salary slips, rather than blindly trusting either one.

3. Can I edit the numbers directly in TIS?

No. TIS is a summary that is generated automatically. To correct anything, you go to the specific entry in AIS and submit feedback there. The correction then flows into TIS automatically.

4. Does the derived value in TIS always match Form 26AS?

Not necessarily, and this is important. If there is any mismatch between Form 26AS and AIS/TIS, especially for TDS credit, you should rely on Form 26AS, since that is the document that determines your actual TDS credit. TIS is useful for a broad income overview, but TDS credit specifically comes from Form 26AS.

5. I checked TIS today, but I made a fixed deposit yesterday. Will it show up immediately?

No. There is a delay between when a transaction happens and when the bank or institution reports it to the tax department. TIS and AIS keep updating throughout the year as more data comes in, so a very recent transaction may take some time to appear.

6. Is checking TIS compulsory before filing my ITR?

It is not a strict legal requirement, but it is very strongly recommended. Since the derived value in TIS is what gets pre-filled into your ITR, skipping this check means you might file a return with an error you could have easily caught and fixed beforehand.

Key Takeaways

- TIS is a simple, category-wise summary built from your detailed AIS. Salary, interest, dividend, and other income types are each shown as one clean total.

- TIS shows two numbers for every category: the processed value (calculated by the system automatically) and the derived value (after your feedback is factored in).

- The derived value is what gets pre-filled into your ITR, so it is the number that matters most before you file.

- If you spot a wrong or duplicate entry, you cannot fix it directly in TIS. You must go to the specific entry in AIS and submit feedback there.

- Capital gains entries, especially mutual fund redemptions, are a common place where duplicate reporting slips through, so check these carefully.

- Always check both TIS and Form 26AS. For TDS credit specifically, Form 26AS is the document that matters most.

- Checking TIS takes just a few minutes and can save you from a mismatch notice later.

Sources: Income Tax Department, Government of India: FAQs on AIS (Annual Information Statement); Income Tax Department: Annual Information Statement (AIS); ClearTax: Taxpayer Information Summary (TIS), Meaning, PDF Password Format and How to Download It; Taxguru: Taxpayer Information Summary (TIS), June 2026.

This article is for general information only and does not give tax advice. Always cross-check your AIS and TIS against your actual bank statements, salary slips, and other records before filing your return. Consult a Chartered Accountant if you find something you are unsure about.