TL;DR: Key Takeaways on the 2026 Banking Boom

If you are just sipping your morning tea and need the fast facts, here is the quick summary of what is happening in the Indian banking sector:

- The Big Headline: In FY26, bank loans (credit) grew by 16%, while bank savings (deposits) only grew by 13.4%.

- The Borrowing Boom: Large corporations, MSMEs, and regular retail customers (taking gold loans and vehicle loans) are aggressively borrowing money from banks to fuel their growth.

- The Missing Deposits: Regular citizens are taking their savings out of traditional low-interest bank accounts and pouring them into the stock market and mutual fund SIPs for better returns.

- The Credit-Deposit Ratio: Because loans are growing faster than deposits, banks are facing “tight liquidity.” Their safety buffer of cash is shrinking.

- The Bank’s Solution: To survive, banks are borrowing billions from the wholesale market through “Certificates of Deposit” (CDs) to ensure they have enough money to lend.

- The Impact on You: Because banks are desperate for your savings, FD interest rates will likely remain high for the rest of 2026. Conversely, getting a cheap loan might become slightly more difficult.

Introduction

Have you ever stopped to think about how a bank actually makes its money? At its core, a bank is basically a very simple trading business. But instead of buying and selling shoes, smartphones, or vegetables, a bank buys and sells money.

Here is the basic recipe: The bank “buys” money from you in the form of a Fixed Deposit (FD) or a Savings Account and pays you an interest rate of, say, 7%. Then, the bank takes that exact same money and “sells” it to a homebuyer or a massive corporation as a loan, charging them an interest rate of 10%. The 3% difference in the middle is how the bank pays its employees, keeps the ATM lights on, and makes a massive profit.

In banking terms, the money you give the bank is called a “Deposit,” and the money the bank gives out is called “Credit” (or loans).

For this system to work perfectly, the bank needs a healthy balance. Water needs to flow into the tank (deposits) at roughly the same speed it flows out (loans). But in the financial year ending March 2026 (FY26), the Reserve Bank of India (RBI) released data showing that the Indian banking tank is facing a very unique problem.

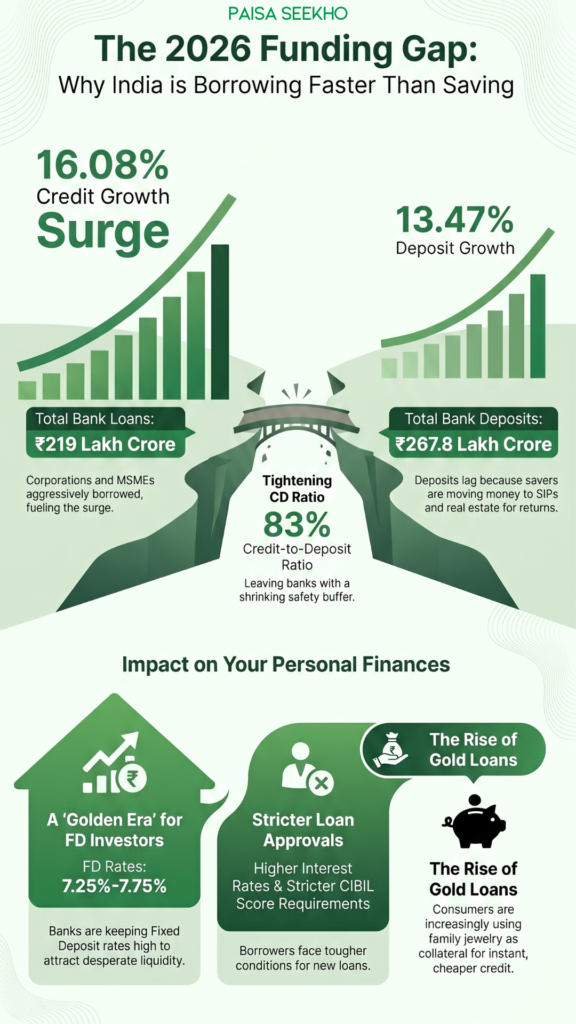

According to the latest RBI data, bank credit grew by a massive 16.08% over the last year, hitting a record ₹219 lakh crore. However, deposits only grew by 13.47%, reaching ₹267.8 lakh crore.

Simply put: Indians (and Indian companies) are borrowing money much faster than they are saving it in the bank.

In this comprehensive, easy-to-understand Paisaseekho guide, we are going to dive deep into this banking phenomenon. We will explore why everyone is suddenly taking massive loans, why you and I are no longer putting all our money in bank FDs, and most importantly, how this “funding gap” directly impacts your loan EMIs and your future returns.

1. Decoding the FY26 Data: The 16% Surge Explained

When you see a percentage like “16% growth” in a newspaper, it is hard to visualize exactly how much money we are talking about. Let us put the RBI’s March 31, 2026 data into absolute numbers so you can see the sheer scale of the Indian economy.

- Total Bank Credit (Loans Given Out): The total outstanding loans in the Indian banking system reached an unbelievable ₹219 Lakh Crore. To put that in perspective, in the last financial year alone, banks distributed over ₹30 lakh crore in new loans to the public and businesses!

- Total Bank Deposits (Money Saved): The total money kept in savings accounts, current accounts, and FDs reached ₹267.8 Lakh Crore. In absolute terms, deposits rose by roughly ₹31.7 lakh crore.

While the absolute amount of deposits is still technically higher than the total loans (which is a legal requirement to prevent banks from going bankrupt), the speed at which the loan book is growing is the fastest we have seen since FY24.

This creates a scenario known in the financial world as a Widening Gap. If you are running a marathon at 10 kilometers per hour, but the person chasing you is running at 15 kilometers per hour, they are eventually going to catch up. In this scenario, the loans are chasing the deposits.

2. Why is Everyone Borrowing?

Why are banks suddenly writing so many loan cheques? Is the average Indian suddenly going on a massive shopping spree? Well, retail loans are a part of the story, but the real drivers behind this 16% explosion are massive corporations and clever small businesses.

Here are the three main reasons credit demand has skyrocketed in 2026:

A. The “Corporate Shift” from Bonds to Banks

When a massive company like Tata, Reliance, or L&T wants to build a new factory, they do not just swipe a credit card. They usually raise money in one of two ways: they either borrow from a bank, or they issue “Corporate Bonds” in the open market for investors to buy.

In early 2026, the global financial markets were a mess. Because of inflation and the ongoing West Asia conflict, the interest rates in the global bond market became incredibly high. Furthermore, borrowing money from overseas in US Dollars became highly risky because the Indian Rupee was fluctuating.

So, what did the smart CFOs of these massive corporations do? They canceled their global bond plans and walked straight into their local SBI or HDFC branch. Domestic bank borrowing simply became cheaper and more reliable than issuing bonds, leading to a massive surge in corporate credit.

B. The Rise of the MSME Engine

Micro, Small, and Medium Enterprises (MSMEs) are the absolute backbone of the Indian economy. For years, these small factory owners and traders struggled to get formal bank loans. However, thanks to a massive push towards digitalization, GST tracking, and cash-flow-based lending algorithms, banks can finally trust small businesses. MSMEs are currently borrowing aggressively to buy new machinery, expand their warehouses, and hire more workers to meet India’s booming domestic consumption demand.

C. The Retail Gold and Auto Loan Rush

On the consumer side, things are equally hot. The data highlights a massive uptick in specific retail segments. Vehicle loans hit record highs in FY26 as the middle class upgraded their cars and two-wheelers. More interestingly, as we discussed in our previous Paisaseekho articles, Gold Loans have seen explosive traction. People are using their idle family jewelry as collateral to unlock instant, cheap credit to fund everything from medical emergencies to home renovations.

3. Where Did the Deposits Go? The Mutual Fund Migration

If the economy is doing so well and businesses are growing, why is deposit growth lagging behind at 13.4%? Where is the Indian middle class putting their monthly salary if not in a bank savings account?

The answer is simple: Financial Awareness.

Ten years ago, the default action for any Indian who saved ₹10,000 at the end of the month was to walk to the bank and open a Fixed Deposit. The bank was the ultimate destination for safety and growth.

But the 2026 Indian consumer is much smarter. They have realized that keeping money in a savings account that pays 3% interest, while inflation is running at 5% or 6%, is mathematically losing them money. They have discovered the power of the stock market.

The SIP Revolution

Instead of giving their money to the bank, retail investors are pouring their wealth into Mutual Funds through Systematic Investment Plans (SIPs). The Indian mutual fund industry has seen record-breaking inflows month after month. Retail investors are willingly taking on a little more risk in exchange for 12% to 15% annual returns in the equity markets.

Furthermore, the booming real estate sector in Tier-1 and Tier-2 cities is absorbing massive amounts of household savings as people invest in physical property rather than paper deposits.

Because of this massive migration of wealth to mutual funds and real estate, the banks are struggling to collect the “raw material” (deposits) they desperately need to fund their loans.

4. The Problem: Understanding the Credit-Deposit (CD) Ratio

To truly understand why banking executives are sweating over these numbers, we need to look at a metric called the Credit-Deposit Ratio, or CD Ratio.

Think of a bank like a giant water tank.

- The Deposits are the water flowing into the tank from the city supply.

- The Credit (Loans) is the water flowing out of the tap to water the garden.

The RBI enforces strict rules. A bank is not legally allowed to lend out 100% of the money it receives. They have to keep a specific chunk locked safely with the RBI (Cash Reserve Ratio) and invest another chunk in super-safe government bonds (Statutory Liquidity Ratio) to ensure that if there is a crisis, the bank has cash to pay its depositors.

Ideally, a bank wants a CD ratio of around 70% to 75%. This means for every ₹100 they get in deposits, they safely lend out ₹75.

In late FY26, the overall banking system’s CD ratio started creeping dangerously high, peaking near 81% to 83% in certain fortnights. This indicates that the system’s liquidity is extremely tight. The bank’s safety buffer is shrinking.

The Emergency Fix: Certificates of Deposit (CDs)

So, if a bank has promised a ₹500 crore loan to a corporate client but does not have enough fresh retail deposits to cover it, what do they do? Do they cancel the loan?

No, they borrow money themselves!

Banks turn to the wholesale market and issue something called a Certificate of Deposit (CD). It is basically the bank begging other financial institutions (like massive insurance companies or mutual funds) for a short-term, bulk cash loan. In the final quarter of FY26 alone, Indian banks aggressively raised over ₹5.27 trillion through these CDs just to keep their lending engines running!

5. What Does This “Funding Gap” Mean for YOU?

This is not just high-level economic theory. The fact that bank credit is growing at 16% while deposits lag at 13.4% has a direct, tangible impact on your personal wallet in 2026.

A. Great News for FD Investors

If you are someone who loves the safety of Fixed Deposits, this is your golden era. Banks are absolutely desperate for your money. Because they need deposits to fund their massive loan pipelines, they cannot afford to lower their FD interest rates. Even if the RBI hints at cutting the Repo rate later this year, commercial banks will fight tooth and nail to keep their FD rates highly attractive (currently hovering around 7.25% to 7.75% for top private banks) to lure you away from the stock market.

B. Bad News for Borrowers

If the bank has to pay high interest rates to attract depositors, their “cost of funds” goes up. Banks will never absorb this extra cost themselves; they will pass it directly to the borrower.

If you are planning to take a new Home Loan, Auto Loan, or Personal Loan, expect the banks to be very strict. The days of ultra-cheap, highly discounted promotional interest rates are temporarily paused. Furthermore, because liquidity is tight, banks will become much pickier about who they lend to, meaning your CIBIL score needs to be absolutely flawless to get a loan approved quickly.

C. The Push for “Salary Accounts”

Have you noticed your bank manager calling you more frequently, asking if you can transfer your company’s “salary accounts” to their branch?

Because bulk borrowing through Certificates of Deposit is very expensive for the bank, their ultimate goal is to capture CASA (Current Account and Savings Account) deposits. CASA money is the cheapest money for a bank because they only pay you 3% interest on it. Expect massive marketing campaigns and freebies from banks trying to convince you to open zero-balance savings accounts or premium current accounts in the coming months.

Conclusion

The 16% credit growth recorded in FY26 is a massive compliment to the Indian economy. It proves that businesses are optimistic, factories are expanding, and consumers feel confident enough about their future income to take on debt. It is the ultimate sign of a nation on the move.

However, the banking system cannot run on optimism alone; it runs on cold, hard cash.

The divergence between the booming credit demand and the sluggish deposit growth is the biggest challenge facing Indian bank CEOs today. While the banks are currently managing the gap by relying on short-term market borrowings, this is not a sustainable long-term solution.

As an everyday consumer, your job is simple: take advantage of the chaos! Use the banks’ desperation to lock in the highest possible Fixed Deposit rates for your emergency funds, avoid taking unnecessary high-interest personal loans, and continue building your long-term wealth through diversified investments. The Indian banking engine is roaring; just make sure you are in the driver’s seat.

Frequently Asked Questions (FAQs) About Bank Credit Growth

Q1: What does “Bank Credit Growth” actually mean?

Bank credit growth simply refers to the increase in the total amount of money that banks have lent out to individuals, businesses, and corporations in the form of loans over a specific period.

Q2: Why did bank credit grow by 16% in FY26?

The massive 16% growth was driven primarily by large corporations shifting away from expensive bond markets to cheaper domestic bank loans, combined with a huge surge in retail borrowing for vehicles, gold loans, and MSME business expansions.

Q3: Why are bank deposits growing much slower than loans?

Bank deposit growth is lagging at 13.4% because the Indian middle class is becoming more financially literate. Instead of locking all their money in low-interest savings accounts or traditional FDs, people are aggressively investing their surplus cash into the stock market, Mutual Fund SIPs, and real estate for higher returns.

Q4: What is the “Credit-Deposit (CD) Ratio”?

The CD ratio is a mathematical metric that shows how much a bank lends out of the deposits it has collected. For example, a CD ratio of 80% means that for every ₹100 the bank receives in deposits, it lends out ₹80 as credit.

Q5: What happens if a bank’s CD ratio gets too high?

If a bank’s CD ratio gets too high (e.g., crossing 85%), it means the bank has “tight liquidity.” They do not have enough cash buffer left to handle sudden withdrawals or economic emergencies. To fix this, they are forced to aggressively raise FD rates or borrow expensive money from the market.

Q6: Will FD interest rates go up because of this deposit shortage?

Yes. Because banks are facing a severe funding gap, they are desperate to attract new savings. Therefore, it is highly likely that Fixed Deposit (FD) interest rates will remain elevated and highly attractive throughout 2026 as banks compete for your money.

Q7: How does this situation affect my chances of getting a personal loan?

When banks are tight on cash, they become highly selective about who they lend to. While you can still get a loan, banks will scrutinize your CIBIL score much more strictly, and you may find that the interest rates on personal loans are slightly more expensive as the bank passes on its higher funding costs to you.

Q8: What is a “Certificate of Deposit” (CD)?

A Certificate of Deposit is a short-term financial instrument issued by banks to raise bulk money from the wholesale market (like massive mutual funds or insurance companies). Banks issue these CDs when they run out of regular retail deposits but still need cash to fund approved corporate loans.

Q9: Are my savings safe if the banks are lending so much money?

Yes, your savings are completely safe. Indian banks are strictly regulated by the RBI, which mandates them to maintain a Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) to ensure they always have enough liquid assets to pay back depositors. Additionally, your deposits are insured up to ₹5 Lakhs by the DICGC.

Q10: Can the RBI fix this widening gap between credit and deposits?

The RBI does not directly control consumer behavior, but it guides the market. The RBI has been actively holding talks with bank CEOs, urging them to find innovative ways to boost retail deposit mobilization and cautioning them against over-relying on short-term wholesale borrowing to fund their long-term loans.