TL;DR: Key Takeaways on How to Reduce Capital Gains tax

If you are short on time and need the absolute basics before filing your ITR, here is your quick cheat sheet:

- Selling Costs are Tax-Free: Any direct money you spend to sell your asset (like paying a real estate broker’s commission) is directly deducted from your taxable profit.

- Inflation is Your Friend: Always use “Indexation.” This legally adjusts your old purchase price to match today’s inflation, making your on-paper profit much smaller.

- The “House-for-a-House” Rule (Section 54): If you sell a residential house and use the profit to buy or build a new residential house, your capital gains tax drops to zero.

- The Government Bond Hack (Section 54EC): If you do not want to buy real estate, you can lock your profits in highly secure government bonds (like NHAI or REC) for 5 years to save up to ₹50 Lakhs in taxes.

- Shares to Bricks (Section 54F): You can sell gold, mutual funds, or shares and still save tax by buying a house. Just remember, you must invest the entire sale amount, not just the profit.

- Use the CGAS Account: If the ITR deadline is here but you haven’t found your dream house yet, park your money in a special “Capital Gains Account Scheme” (CGAS) at the bank to prove to the government you plan to buy a house soon.

Introduction

As a salaried individual working hard in India, you are already very familiar with the pain of taxes. Every single month, before your salary even hits your bank account, a significant chunk disappears as Tax Deducted at Source (TDS). You accept this as a normal part of life.

But then, a major financial event happens. You finally decide to sell that piece of land you held for ten years, or you cash out your massive mutual fund portfolio to fund your child’s education, or you sell your ancestral gold. You make a handsome, well-deserved profit.

Just as you are about to celebrate this financial milestone, the government steps in again and asks for a massive slice of your profit in the form of Capital Gains Tax. It can feel incredibly frustrating. You took the investment risk, you waited patiently for years, and now a huge portion of your reward is going to the tax department.

However, there is excellent news. You do not have to hand over all your profit to the taxman.

As we enter the official Income Tax Return (ITR) filing season for Assessment Year 2026-27, it is time to open the rulebook. The Income Tax Act of India is actually packed with totally legal, government-approved deductions that can help you significantly reduce capital gains tax. In some cases, you can legally bring your tax liability down to absolute zero!

Welcome to your comprehensive Paisaseekho guide. In this simple, easy-to-understand, jargon-free article, we are going to break down everything you need to know. We will explain the top 9 deductions available to salaried individuals in 2026. Whether you are selling gold, a residential apartment, or shares, we will show you the exact legal path to protect your wealth.

Understanding the Basics: What Exactly Are Capital Gains?

Before we jump into the strategies to reduce capital gains tax, let us make sure we understand what the term actually means.

Whenever you sell an asset (like a house, an apartment, gold jewelry, mutual funds, or stock market shares) for a price that is higher than what you originally paid for it, that extra profit is called a “Capital Gain.”

The Income Tax Department divides these profits into two distinct categories:

1. Short-Term Capital Gains (STCG):

If you buy an asset and sell it very quickly, it is considered short-term. For example, if you buy shares and sell them within a few months, or buy a house and sell it within a year, the profit is short-term. The government does not like quick “flipping,” so Short-Term Capital Gains are generally taxed at a much higher rate.

2. Long-Term Capital Gains (LTCG):

If you hold onto an asset patiently before selling it, it becomes long-term. For real estate (like a house or land), holding it for more than 24 months makes it long-term. For equity shares or equity mutual funds, holding them for more than 12 months makes them long-term.

Why does this matter?

It matters because the government rewards patient investors. Long-Term gains have a lower tax rate. More importantly, almost all the major, powerful tax-saving deductions we are about to discuss apply exclusively to Long-Term Capital Gains.

The 9 Powerful Deductions to Reduce Capital Gains Tax in 2026

If you want to keep your money in your own pocket, you need to know these nine specific sections of the Income Tax Act. Let us explore how each one works with simple, real-world examples.

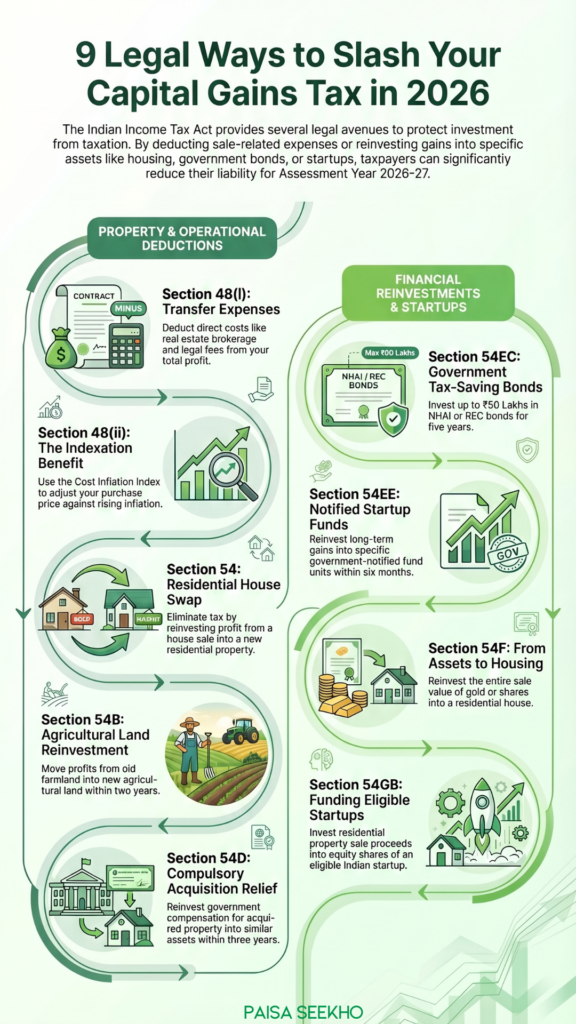

Deduction 1: Section 48(i) – Claiming Your Transfer Expenses

Let us start with the absolute basics. Selling a massive asset like a house is never free. You have to spend money just to make the sale happen. The government is fair enough to recognize this.

Under Section 48(i), any money you spend exclusively and wholly to transfer the asset can be deducted from your total profit before the tax is calculated.

Example: Imagine you sell your flat in Gurugram for ₹1 Crore. To find a buyer, you had to pay a real estate broker a 1% commission, which is ₹1 Lakh. You also spent ₹50,000 on a lawyer to draft the legal sale documents. You can combine these transfer expenses (₹1.5 Lakh) and subtract them directly from your sale value. You will not pay a single rupee of capital gains tax on that ₹1.5 Lakh.

Deduction 2: Section 48(ii) – The Magic of Indexation

Inflation is the silent thief that eats the value of your money. If you bought a house in 2010 for ₹20 Lakhs and sold it today for ₹80 Lakhs, your actual profit is not really ₹60 Lakhs, because ₹20 Lakhs in 2010 had much more buying power than it does today.

Section 48(ii) allows you to use the “Cost Inflation Index” (CII) provided by the government. This means you get to artificially adjust your original purchase price to match today’s inflation rate.

Example: Because of indexation, the tax department might say your ₹20 Lakh purchase price from 2010 is equal to ₹45 Lakhs in today’s money. Now, your taxable profit drops from ₹60 Lakhs down to just ₹35 Lakhs! This is one of the most powerful tools available to reduce capital gains tax on long-term assets. You can also use this indexation benefit on any money you spent making major improvements to the house (like adding a new floor).

Deduction 3: Section 54 – The Classic “House-to-House” Swap

This is perhaps the most famous and widely used tax deduction in India. It is designed for families who want to upgrade their living situation without getting penalized by taxes.

If you sell a residential house and make a Long-Term Capital Gain, you can claim a massive exemption under Section 54 if you use that profit to buy or construct a new residential house.

The Rules:

- You must buy the new house either 1 year before selling the old one or within 2 years after selling the old one.

- If you are constructing a house from scratch, you get 3 years to finish it.

- The new house must be located in India. You cannot sell a flat in Delhi and buy a villa in Dubai to save Indian taxes.

If your profit was ₹40 Lakhs, and you buy a new house worth ₹50 Lakhs, your entire capital gains tax becomes zero!

Deduction 4: Section 54B – Moving Your Agricultural Land

The government wants to protect farmers and agricultural production. If you, your parents, or your Hindu Undivided Family (HUF) sell a piece of agricultural land, you might face a heavy tax bill.

However, under Section 54B, you can completely wipe out this tax if you use the profit to buy another piece of agricultural land.

The condition here is that the old land must have been used for farming purposes for at least two years right before you sold it. Once you sell it, you have exactly two years to purchase the new farm land to claim the deduction.

Deduction 5: Section 54D – Compulsory Acquisition by the Government

Sometimes, you do not want to sell your property, but you are forced to. If the government decides they need to build a new highway, a metro line, or an airport right where your property stands, they will “compulsorily acquire” your land or building and pay you compensation.

Even though you didn’t want to sell, that compensation is technically a capital gain. To help you recover from this disruption, Section 54D allows you to take that compensation money and buy or construct a similar land or building within three years. If you do this, you can fully reduce capital gains tax on the forced sale.

Deduction 6: Section 54EC – The Famous Government Tax-Saving Bonds

What if you sell a house, but you do not want to buy another house? Maybe you are retiring and you just want safe, liquid cash. This is where Section 54EC comes to the rescue.

If you sell land or a building and make a long-term profit, you can take that profit and invest it into highly secure, government-backed bonds. The most common ones are issued by the National Highway Authority of India (NHAI) or the Rural Electrification Corporation (REC).

The Rules:

- You must invest the money into these bonds within 6 months of selling your property.

- The maximum limit you can invest to save tax is ₹50 Lakhs per financial year.

- Your money will be locked in these bonds for 5 years, but you will earn a steady annual interest on it during that time.

Deduction 7: Section 54EE – Investing in Startup Funds

To boost the Indian economy, the government launched Section 54EE. This section is very similar to the bonds mentioned above, but instead of building highways, your money goes towards funding new businesses.

If you make a long-term capital gain, you can invest the profits into specific “notified units” of specified funds created by the Central Government. Just like the bonds, you have a 6-month deadline to invest the money after the sale, and there is a strict maximum limit of ₹50 Lakhs.

Deduction 8: Section 54F – From Gold and Shares to a Dream Home

Earlier, in Section 54, we talked about selling a house to buy a house. But what if you sell something else?

Let’s say you have a massive portfolio of stock market shares, or you sell a large amount of physical gold. If you take the money from that sale and use it to buy a residential house, you can claim a deduction under Section 54F.

The Crucial Difference:

Under the normal Section 54, you only need to reinvest the profit to save tax. But under Section 54F, you must reinvest the entire net sale value (the total money you received, not just the profit) to make your tax zero.

Also, on the day you buy this new house, you are not allowed to own more than one other residential house in your name.

Deduction 9: Section 54GB – Funding an Eligible Startup

In 2026, the startup ecosystem in India is booming. The government actively encourages wealthy individuals to fund these new ventures.

If an individual or an HUF sells a residential property (a house or a plot) and makes a long-term capital gain, they can completely reduce capital gains tax by taking that net money and investing it into the equity shares of an “Eligible Startup” company.

To prevent abuse of this rule, the startup company is then legally required to use your invested money to purchase new, specified assets (like computers, machinery, or software) within one year. This is a brilliant way to save tax while becoming an angel investor in a growing business!

What is the Capital Gains Account Scheme (CGAS)?

As you read through these deductions, you might have noticed a common theme: deadlines.

To claim the exemption for buying a new house under Section 54 or 54F, the law gives you 2 to 3 years. But your Income Tax Return (ITR) is due this year!

So, how do you tell the tax department, “Please don’t tax me, I promise I will buy a house next year”?

You cannot just leave the cash sitting in your regular savings account. If July 31st (the ITR deadline) is approaching and you haven’t found the perfect house yet, you must transfer your capital gains money into a special bank account called the Capital Gains Account Scheme (CGAS).

Almost all major public sector banks (like SBI or PNB) offer this account. By depositing the money here before you file your ITR, you officially lock the funds for real estate purposes. The government accepts this deposit as “proof” of your intention to buy a house, allowing you to claim your deduction and successfully reduce capital gains tax in your current ITR filing.

Crucial ITR Filing Deadlines for AY 2026-27

Knowledge is only power if you act on it in time. As a salaried individual, your tax season follows a very strict calendar. Missing these dates can result in heavy penalties and the loss of your right to claim these valuable deductions.

- June 15, 2026: By this date, your employer is legally required to hand over your Form 16. This document is the foundation of your tax return, detailing your salary and the TDS already deducted.

- July 31, 2026: This is the absolute final deadline for individual, salaried taxpayers to file their Income Tax Return (ITR) for Assessment Year 2026-27. You must complete your ITR filing and claim all your capital gains deductions before midnight on this date.

Conclusion: Smart Planning Saves Money

Paying taxes is the duty of every responsible citizen, but paying more tax than the law requires is simply bad financial management.

The Income Tax Act is not just a book of punishments; it is a guidebook full of incentives. The government actually wants you to reinvest your money into the economy—whether that means buying a new home, funding infrastructure through NHAI bonds, or investing in the next generation of Indian startups.

When you sit down to tackle your ITR filing for 2026, take a close look at any assets you sold last year. Do not just blindly accept the massive tax calculation on your screen. Use the 9 deductions we outlined in this Paisaseekho guide to legally and effectively reduce capital gains tax. Keep your hard-earned wealth where it belongs: working for you and your family’s future.

Frequently Asked Questions (FAQs) About Capital Gains Tax Deductions

Q1: Can I claim a deduction if I sell a house and buy a commercial shop?

No. The exemptions under Section 54 and Section 54F are strictly designed for the purchase or construction of a residential house property. Buying a commercial office, a shop, or an empty agricultural plot will not help you reduce capital gains tax under these specific sections.

Q2: What happens if I buy the new house, but then sell it after one year?

The government prevents you from misusing these rules to simply “park” your money and avoid taxes. If you claim a deduction under Section 54 by buying a new house, you are legally required to hold onto that new house for a minimum “lock-in” period of 3 years. If you sell it before 3 years are up, the exemption is canceled, and you will have to pay the original capital gains tax along with heavy penalties.

Q3: Is there a maximum limit on how much tax I can save by buying a new house?

In recent budgets, the government introduced a cap to prevent ultra-rich individuals from saving tens of crores in taxes. Currently, the maximum deduction you can claim under Section 54 and Section 54F for reinvesting in a residential property is capped at ₹10 Crores. Any capital gains above this ₹10 Crore limit will be fully taxable.

Q4: Do I have to invest my money in 54EC bonds all at once?

No, you do not have to make a single lump-sum investment. You can invest in NHAI or REC bonds in multiple smaller installments. However, you must complete all your investments within exactly 6 months from the date you sold your original property, and the total combined investment cannot exceed the ₹50 Lakh limit in a financial year.

Q5: Can I use both Section 54 (buying a house) and Section 54EC (buying bonds) for the same property sale?

Yes, absolutely! This is a very smart strategy for large profits. If your capital gains are huge, you can use a portion of the profit to buy a new house (claiming Section 54) and invest the remaining profit into government bonds up to ₹50 Lakhs (claiming Section 54EC), thereby maximizing your tax savings.

Q6: What if the builder delays the construction of my new house beyond 3 years?

The law states you must finish construction within 3 years. However, various high court rulings have established that if the delay is entirely the fault of the builder and completely out of your control, the tax department generally allows the exemption to stand, provided you have already made the full payment to the builder.

Q7: Can a Non-Resident Indian (NRI) claim these capital gains deductions?

Yes. NRIs are fully eligible to claim deductions under Section 54, Section 54EC, and Section 54F, just like resident Indians. However, the new property they buy under Section 54 must be physically located within the borders of India.

Q8: If I sell a plot of land, can I use Section 54 to save tax?

No. Section 54 specifically applies only when you sell a residential house. If you sell an empty plot of land, it falls under Section 54F. To reduce capital gains tax under 54F, you must invest the entire net sale consideration (not just the profit) into buying or building a residential house.

Q9: Does the Capital Gains Account Scheme (CGAS) pay any interest?

Yes. The money you park in a CGAS account before filing your ITR does not sit idle. The bank will pay you interest on it. It usually earns an interest rate similar to a standard bank Fixed Deposit. However, remember that the interest you earn from this CGAS account is fully taxable as your regular income.

Q10: What is the deadline for salaried employees to file their ITR for AY 2026-27?

The official due date for individual taxpayers, whose accounts do not require a professional tax audit, is July 31, 2026. You should ideally wait until you receive your Form 16 from your employer (usually by June 15) so that your salary and TDS data match the government’s records perfectly before you file.

Source: