Quick summary: India gives you two main ways to own a piece of companies like Apple, Nvidia, or Amazon without leaving the country. The first is through international mutual funds, which pool money from Indian investors and deploy it into foreign stocks or global funds. The second is by directly investing overseas through the Liberalised Remittance Scheme (LRS). Both options are real and legal. But there is an important complication with international mutual funds right now: the Indian mutual fund industry has a government-set limit of $7 billion for total overseas investment. As of mid-2026, this limit is nearly exhausted, and many fund houses have temporarily paused or restricted fresh investments. This article explains what international funds are, how to invest in them when they are open, what the tax implications are, and what alternatives exist.

What Are International Mutual Funds?

An international mutual fund is a scheme that invests primarily in stocks, ETFs, or other funds listed in countries outside India. When you invest in one of these funds, your money effectively buys small pieces of companies listed on stock exchanges in the United States, Europe, Japan, South Korea, Taiwan, and other markets.

For investors in India, these funds offer something domestic funds cannot: geographic and currency diversification. India’s stock market is large, but it is concentrated in certain sectors (banks, IT services, FMCG, pharma). Industries like semiconductors, aerospace and defence, AI infrastructure, electric vehicles, global e-commerce, and streaming entertainment are far better represented abroad than in India. International funds fill this gap.

There is also a currency dimension. When you invest in an international mutual fund, the underlying investments are in foreign currencies, primarily the US dollar. If the dollar strengthens against the rupee over your holding period (which has been the historical trend), it adds to your returns. Of course, this works in reverse too if the rupee strengthens.

Types of International Mutual Funds Available in India

International mutual funds come in a few structural forms:

1. Fund of Funds (FoF):

This is the most common structure for international funds in India. An Indian fund house creates a scheme that uses your money to invest in a foreign mutual fund or ETF. For example, a “Nasdaq 100 FoF” buys units of a Nasdaq 100 ETF listed in the US. You are effectively investing two layers deep: the Indian fund, which then invests in a foreign fund. Each layer charges its own fee, which means FoFs are typically more expensive than direct funds.

2. Overseas equity schemes:

Some Indian fund houses directly buy foreign company shares in their portfolio, rather than routing through a foreign fund. These are rarer than FoFs.

3. Index-based international ETFs:

A few Indian mutual funds have created ETFs listed on Indian stock exchanges (NSE/BSE) that track global indices like the Nasdaq 100, S&P 500, or Hang Seng. You buy and sell these like any Indian equity ETF through your demat account.

Popular themes available in India (when open) (this is not investment advice – just a list of popular themes)

- US large-cap (S&P 500 index)

- US technology (Nasdaq 100, US Tech equity)

- Global diversified (MSCI World, Global Equity)

- European equities

- Asian and emerging markets (Greater China, ASEAN, Taiwan)

- Global consumer or thematic funds

The $7 Billion Problem: What Every Investor Must Know Right Now

This is the most important thing to understand before you invest. Unlike domestic mutual funds, which have no cap on inflows, international mutual funds in India are subject to an industry-wide investment limit set by SEBI.

The limit structure is:

- $7 billion total for all Indian mutual fund industry overseas investments combined (across all fund houses and all international schemes)

- $1 billion separate limit for investments specifically in overseas ETFs

These limits have been in place since SEBI’s circular dated June 3, 2021. The problem is that as the Indian market grew and more investors started putting money into international funds, the industry collectively approached and repeatedly bumped against the $7 billion ceiling.

Here is the timeline and current situation:

In January 2022, the industry breached the $7 billion limit for the first time, and SEBI directed all fund houses to stop accepting fresh subscriptions in international schemes. This caused significant inconvenience for investors who had active SIPs.

The restriction was partially eased when global market corrections brought the dollar value of the invested corpus below the limit. But the fundamental cap has never been raised.

As of mid-2026, the situation is as follows: the limit is once again nearly exhausted. Multiple fund houses have either suspended or restricted fresh investments:

- Nippon India Mutual Fund suspended fresh subscriptions in its international schemes from April 21, 2026

- Axis Mutual Fund suspended fresh inflows into select overseas schemes from May 6, 2026

- Kotak Mahindra Mutual Fund capped fresh investments

- Invesco Mutual Fund reopened three international FoFs from May 8, 2026 for limited headroom (subject to available capacity)

What this means in practice: as of writing in June 2026, you may find that some international fund schemes are closed for new investments while others are open with restrictions. The availability of specific funds can change from week to week depending on whether existing investors redeem, creating headroom.

Critically: this is not a fund quality issue. When a fund suspends fresh subscriptions due to the SEBI cap, your existing units are completely safe, continue to be invested and managed normally, and remain available for redemption at any time. Only new money coming in is restricted.

What should you do?

- Check the AMC’s website or your investment platform for the current status of any specific fund before investing

- If a fund you want is closed, either wait for it to reopen or consider alternatives (discussed below)

How to Check If a Fund Is Open for Investment?

Before putting money into any international mutual fund, verify its subscription status through any of these sources:

- The fund house’s official website (AMC website)

- Your investment platform (Groww, Zerodha Coin, Kuvera, etc.) will typically show “Not Available” or “SIP Paused” for restricted funds

- The AMFI website (amfiindia.com) periodically lists suspended schemes

How to Invest in International Mutual Funds (When a Fund Is Open)?

If a fund is accepting investments, here is how to invest:

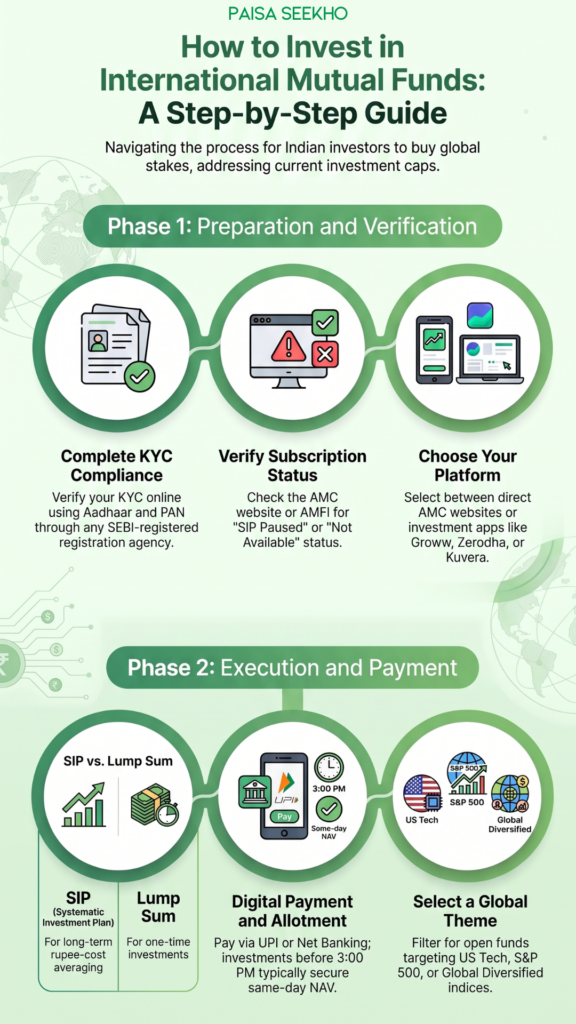

Step 1: Complete your KYC.

To invest in any mutual fund in India, including international ones, you need a verified KYC. If you have already invested in domestic mutual funds, your KYC is likely complete. If not, complete it online through any SEBI-registered KYC Registration Agency (Groww, Zerodha, Kuvera, or any AMC website) using your Aadhaar and PAN.

Step 2: Choose your platform.

You can invest through:

- Direct plans on the AMC website: Lower expense ratio, no distributor commission. Requires separate accounts per AMC.

- Investment platforms: Apps like Kuvera, Groww, Zerodha Coin, INDmoney, or Paytm Money aggregate multiple AMCs in one place. Easier to manage a portfolio. Most offer direct plans now.

- Your bank’s investment portal: HDFC, SBI, ICICI, and most other banks offer mutual fund investment through their net banking or mobile apps. These often offer regular plans with slightly higher expense ratios.

Step 3: Find an international fund that is currently open.

Search for “international fund,” “global fund,” “overseas fund,” or specific names like “S&P 500,” “Nasdaq,” or “US Equity” on your platform. Check the subscription status. Many platforms will mark restricted funds clearly.

Step 4: Choose between SIP and lump sum.

- SIP (Systematic Investment Plan): Invests a fixed amount every month. ₹500 per month is often the minimum for international FoFs, though this varies by fund. SIPs make sense for long-term wealth building with the benefit of rupee-cost averaging.

- Lump sum: A one-time investment. May be subject to specific per-investor or per-day caps even when a fund is nominally open, depending on available headroom.

Step 5: Complete payment.

Link your bank account and make the payment via UPI, NEFT, or net banking. Units are allotted at the NAV of the day the payment is processed. For investments placed before 3:00 PM on a business day, the same day’s NAV typically applies. After 3:00 PM, the next business day’s NAV applies.

Tax on International Mutual Funds: FY 2025-26 and FY 2026-27

This is a section where many investors are confused, because the tax rules for international funds changed significantly in 2023-24 and again in 2024-25. Here is the accurate current picture.

What category do international funds fall under?

International mutual funds, including FoFs that invest in foreign equities, are not considered equity-oriented funds for tax purposes in India. This is because “equity-oriented fund” is defined as a fund that invests at least 65% of its assets in Indian domestic equities. International funds invest abroad, so they do not meet this definition.

From FY 2025-26, international equity FoFs also no longer fall under “specified mutual funds” (the category created by Section 50AA that previously forced all gains to be taxed at slab rates regardless of holding period). The definition of “specified mutual fund” was narrowed by the Finance (No. 2) Act, 2024 to cover only funds investing more than 65% in debt instruments.

As a result, international equity FoFs are now taxed as follows for investments redeemed from FY 2025-26 onwards:

| Holding period | Tax treatment |

| Less than 24 months | Short-Term Capital Gains (STCG): taxed at your income slab rate |

| 24 months or more | Long-Term Capital Gains (LTCG): taxed at 12.5% flat (no indexation) |

Important distinctions to keep in mind:

- The ₹1.25 lakh annual LTCG exemption applies only to equity-oriented fund gains under Section 112A. It does not apply to international fund LTCG. Your first rupee of gain after 24 months is taxed at 12.5%.

- If you are in the 20% or 30% income tax slab, the 24-month LTCG rate of 12.5% is much better than being taxed at slab rate.

- The holding period of 24 months is an improvement over the earlier 36-month threshold for non-equity funds.

- SIP investments: each monthly SIP instalment is a separate purchase with its own 24-month clock. If you have been running a SIP since January 2024, the January 2024 instalment crossed 24 months in January 2026. The December 2024 instalment will only cross 24 months in December 2026. So a partial redemption will have a mix of STCG and LTCG components.

Dividend income

Any dividends paid by the fund (from IDCW plan units) are added to your total income and taxed at your applicable slab rate. TDS of 10% is deducted by the fund house if your annual IDCW from a single scheme exceeds ₹10,000. Use the Growth plan (not IDCW) if you want to avoid this and let your money compound.

What about the old “specified mutual fund” rules?

If you had invested in international funds before FY 2025-26 when they were classified as “specified mutual funds,” those older investments were taxed at slab rate regardless of holding period. Check with your tax advisor or review your unit purchase dates carefully when redeeming older units, as the tax treatment depends on when you invested.

For a detailed breakdown of your overall income tax liability when you redeem these funds, our income tax slabs guide has the current slab rates that will determine your STCG tax.

What Is an FoF Expense Ratio and Why Does It Matter?

International FoFs have a structural cost disadvantage: they charge fees at two levels.

- The Indian FoF charges an expense ratio (typically 0.3% to 1.5% for direct plans)

- The underlying foreign fund also charges its own expense ratio

This “double charge” can add up. For example, if the Indian FoF charges 0.5% and the underlying foreign fund charges 0.75%, the total annual cost is roughly 1.25% per year on your investment. Over a 10-year period, this compounds and can meaningfully reduce your net returns.

What to look for: Check the total expense ratio (TER) in the fund’s fact sheet. For direct plans (not regular plans), the TER tends to be lower. Prefer low-cost options when comparing similar funds.

The Alternative Route: LRS (Liberalised Remittance Scheme)

If you want to invest internationally and are frustrated by the $7 billion cap issue with mutual funds, there is another path: the Liberalised Remittance Scheme (LRS), which allows resident Indians to remit up to $250,000 per person per financial year for investments abroad.

Under LRS, you can open an account with an overseas broker (a few India-based platforms that facilitate this include INDmoney, Vested Finance, and Stockal) and directly buy:

- US-listed ETFs (like SPY for the S&P 500 or QQQ for the Nasdaq 100)

- Individual stocks listed on NYSE or NASDAQ

- Fractional shares of expensive stocks like Amazon or Google

The LRS route bypasses SEBI’s mutual fund cap entirely since the money goes directly abroad, not through an Indian fund.

Downsides of LRS investing:

- A Tax Collected at Source (TCS) of 0.5% is collected at the time of remittance (above ₹7 lakh per financial year). This is not an extra tax but a prepayment against your income tax, which you can claim back when filing your ITR.

- You need to report foreign assets and foreign income in your ITR (Schedule FA and Schedule FSI), which adds complexity

- Currency conversion costs apply when remitting

- You are responsible for choosing your own investments, unlike a mutual fund where a manager handles it

LRS is a good option for financially literate investors who want direct ownership of specific foreign assets. Mutual funds remain more suitable for beginners who want a managed, diversified exposure.

Why Invest Internationally? The Case for Diversification

Here is the honest case for international exposure, without overselling it:

- Access to sectors not well-represented in India: India’s market is strong in banking, IT services, FMCG, and pharma. But if you want exposure to global semiconductor leaders (TSMC, Nvidia, ASML), US consumer tech (Apple, Amazon, Microsoft), European industrial and defence companies, or pure-play AI infrastructure companies, you largely need to go international.

- Currency hedge: Historically, the Indian rupee has depreciated against the US dollar over time. When you hold dollar-denominated investments, this depreciation adds to your returns when converted back to rupees. This is not guaranteed, but it has been the trend over decades.

- True diversification: If all your money is in Indian stocks and the Indian market goes through a rough patch, international exposure means part of your portfolio might still be doing fine.

The other side:

- Foreign markets go through their own cycles and can decline sharply

- The $7 billion cap means you may not always be able to invest when you want to

- You cannot claim Section 80C or 80CCD-style deductions on international fund investments

- The expense structure is typically higher than direct domestic equity funds

A reasonable approach for most investors: use international funds as a satellite allocation (10% to 20% of your overall mutual fund portfolio) rather than the core.

Practical Tips Before Investing

Check the fund’s subscription status on the day you invest.

The situation with SEBI limits changes frequently. A fund that was open last week may be closed today. Always verify.

Prefer direct plans over regular plans.

Direct plans have lower expense ratios (no distributor commission). On platforms like Kuvera and Groww, you can choose direct plans. Our guide to best money apps in India covers the platforms where you can invest in direct plans.

Match the fund geography to your goal.

A Nasdaq 100 FoF is US technology-heavy. A global diversified FoF gives you a broader geographic spread. Think about which exposure you actually want.

Keep your holding period in mind for tax.

Hold for at least 24 months to benefit from the 12.5% LTCG rate. If you invest through SIP, the 24-month clock starts separately for each instalment.

Do not invest money you need soon. Like all market-linked investments, international funds can and do go down. These are long-term (5 years or more) investment instruments.

Frequently Asked Questions

1. Can I invest in US stocks through Indian mutual funds?

Yes. Several Indian fund houses offer schemes specifically focused on the US market, including S&P 500 index funds, Nasdaq 100 funds, and US tech equity funds. However, as of mid-2026, availability of fresh subscriptions in some of these is restricted due to the SEBI $7 billion cap.

2. Is there a minimum investment amount for international mutual funds?

The minimum varies by fund. Many FoFs have a minimum SIP of ₹500 per month and a minimum lump sum of ₹1,000. Check the fund’s Scheme Information Document (SID) for specifics.

3. My existing SIP in an international fund was paused. What happens to my money?

Your existing units remain safely invested. Your next SIP instalment may not get processed if the fund house has suspended registrations. Check with your AMC or platform. You can choose to redirect the SIP amount to an international fund that is currently open, or park it temporarily in a domestic fund.

4. Are international mutual funds safe?

They are market-linked investments and are not “safe” in the sense of being capital-guaranteed. The underlying foreign markets can decline, the rupee can strengthen reducing returns, and the funds carry currency and market risk. They are regulated by SEBI and administered by registered AMCs, so they are not unregulated. But “safe” depends on what you mean.

5. Can I invest in international funds through SIP after the SEBI limit is reached?

When a fund suspends new subscriptions due to the SEBI cap, even existing SIPs may get paused in some cases. The rules differ by fund house: some pause only new SIP registrations, while others also pause ongoing SIPs. Check the specific AMC’s announcement.

6. What is the difference between a direct plan and a regular plan for international funds?

A direct plan does not include the distributor’s commission in the expense ratio. It is cheaper and leads to higher long-term returns. A regular plan includes the commission for the financial advisor or distributor who sold you the fund. If you invest through an app yourself, you can typically choose the direct plan.

7. Do international funds provide any tax deduction?

No. Unlike ELSS funds (which provide an 80C deduction), investments in international mutual funds do not give you any upfront tax deduction. They are purely growth investments with favourable capital gains tax treatment on long-term redemptions.

Key Takeaways

- International mutual funds let Indian investors access global markets and companies without opening a foreign brokerage account.

- The most common structure is a Fund of Funds (FoF): an Indian fund that invests in a foreign fund or ETF.

- A critical constraint: SEBI caps the Indian mutual fund industry’s total overseas investment at $7 billion (plus $1 billion for overseas ETFs). As of mid-2026, this limit is nearly exhausted, and several major fund houses have suspended or restricted fresh subscriptions.

- Availability of specific funds fluctuates. Always check the current subscription status before investing.

- Tax for FY 2025-26: gains on redemption within 24 months are taxed at your slab rate (STCG). Gains after 24 months are taxed at 12.5% flat (LTCG), with no indexation and no ₹1.25 lakh exemption.

- The LRS route ($250,000/year remittance abroad) is an alternative for investors who want to directly buy foreign stocks or ETFs without the $7 billion cap problem.

- Use international funds as a satellite allocation (10 to 20% of portfolio), not as a core holding.

Sources: Securities and Exchange Board of India (SEBI): Circular on Overseas Investment Limits for Mutual Funds; AMFI India: Suspension notices from various AMCs, April-May 2026; Invesco India: International FoF reopening announcement, May 8, 2026; Kotak Mutual Fund Tax Reckoner FY 2025-26: International Fund of Funds taxation; Mirae Asset Mutual Fund Tax Reckoner FY 2025-26.

Mutual fund investments are subject to market risks. Read all scheme-related documents carefully before investing. This article is for general information only and does not constitute investment advice. For advice specific to your financial situation, consult a SEBI-registered investment advisor.