Quick summary: Most people only think about TDS in the context of salary or bank interest. But if you are an individual or a Hindu Undivided Family (HUF) who pays a contractor, architect, lawyer, interior designer, or any other professional more than ₹50 lakh in a financial year, you are legally required to deduct TDS before making the payment and then file an online form called Form 26QD. This obligation exists even if the payment is for a personal project like building your own home. The TDS rate is 2% and you do not need a TAN to comply. This guide explains who needs to file Form 26QD, when it applies, how the threshold works, and walks through worked examples.

What Is Form 26QD?

Form 26QD is a challan-cum-statement filed online by individuals or HUFs who deduct TDS on high-value payments made to resident contractors and professionals under Section 194M of the Income Tax Act, 1961. Like Form 26QB (for property purchase TDS) and Form 26QC (for rent TDS), it combines the TDS payment with the reporting of the transaction in a single online step, without requiring the filer to obtain a TAN.

Section 194M was introduced by the Finance Act, 2019, effective from 1 September 2019. Before this section existed, individuals and HUFs who were not required to have their accounts audited had no legal obligation to deduct TDS on payments made to contractors or professionals, even when those payments ran into crores. This created a significant gap in the tax net. Section 194M was designed specifically to close this loophole.

The corresponding TDS certificate issued after filing Form 26QD is Form 16D, which the payer downloads from the TRACES portal and hands to the contractor or professional.

Why Section 194M Exists: The Loophole It Closed

To understand Form 26QD, it helps to understand the problem it was designed to solve.

Companies, partnership firms, and individuals or HUFs whose turnover crosses the tax audit threshold under Section 44AB are already required to deduct TDS on contractor payments (Section 194C), professional fees (Section 194J), and commission (Section 194H). They must obtain a TAN and file quarterly TDS returns.

But ordinary individuals and HUFs who are NOT required to get their accounts audited were completely outside this system. A wealthy individual building a luxury home and paying a contractor ₹1.5 crore, or paying an architect ₹60 lakh, had no TDS obligation at all. These large payments moved without any tax trail.

Section 194M changed this. Now, if such a person’s payments to a resident for covered services cross ₹50 lakh in a year, they must deduct TDS at 2% and file Form 26QD. They still do not need a TAN, and they do not need to file quarterly TDS returns. Just one form per qualifying payment, online, using their PAN.

Who Must File Form 26QD?

You are required to file Form 26QD if all of the following apply to you:

- You are an individual or a Hindu Undivided Family (HUF)

- You are not required to get your accounts audited under Section 44AB of the Income Tax Act (i.e., you are not a business with turnover above the audit threshold, and not a professional with gross receipts above ₹50 lakh)

- You are paying a resident (Indian resident) person for contractual work, professional services, or commission/brokerage

- Your aggregate payments to that person during the financial year exceed ₹50 lakh

Who Does NOT Need to File Form 26QD?

- Companies, firms, LLPs, and trusts: These entities already deduct TDS under Sections 194C, 194J, or 194H using a TAN and quarterly TDS returns.

- Individuals or HUFs who are required to get their accounts audited: These are covered by Sections 194C, 194H, and 194J and already use the regular TDS return system.

- Anyone paying a non-resident: For non-resident payees, Section 195 applies, and a TAN is required.

- Anyone whose total payments to a single person stay below ₹50 lakh in the year: Below this threshold, no TDS obligation under Section 194M.

What Payments Does Section 194M Cover?

Section 194M applies to three broad categories of payments:

1. Contractual work (including supply of labour): Any payment made to a resident for executing work under a contract. This includes construction, civil work, repair and renovation, manufacturing or supplying goods made from materials provided by the payer, housekeeping, security, catering, transportation under contract, and similar services.

2. Professional services: Fees paid to any person exercising a profession, including lawyers, doctors, engineers, architects, accountants, chartered accountants, interior decorators, technical consultants, advertising professionals, film directors, and similar service providers.

3. Commission or brokerage (other than insurance commission): Any payment for mediating or facilitating a transaction, including real estate brokerage, stock market broking, and general commission arrangements.

Notably, insurance commission is excluded. Payments to insurance agents are covered under Section 194D, not Section 194M.

Also importantly: Section 194M explicitly covers personal payments. If you hire a contractor to build your own home or renovate your flat (not for business purposes), and the payments exceed ₹50 lakh, Section 194M still applies. This is different from most other TDS sections, which are primarily business-oriented.

The TDS Rate Under Section 194M

The current TDS rate under Section 194M is 2%, effective from 1 October 2024, as amended by the Finance Act (No. 2), 2024. For FY 2025-26 (April 2025 to March 2026), all qualifying payments attract TDS at 2%.

No surcharge or health and education cess is added to this rate. So the deduction is a flat 2% on the qualifying amount.

If the payee (contractor/professional) does not provide their PAN: TDS must be deducted at 20% under Section 206AA. Always collect the PAN of the contractor or professional before making any payment.

The ₹50 Lakh Threshold: How It Actually Works

This is the most critical and most misunderstood aspect of Section 194M. Understanding the threshold mechanism correctly can save you from errors and unexpected TDS obligations.

Key rules about the threshold:

Rule 1: The threshold is per payee, not per transaction.

You look at total aggregate payments made to a single resident person during the financial year, not each individual payment in isolation.

Rule 2: It is per financial year.

The count resets to zero every 1 April.

Rule 3: TDS applies on the entire cumulative amount, not just the amount above ₹50 lakh.

Once you cross the ₹50 lakh mark, TDS is deducted on the total amount paid so far (including payments made before the threshold was crossed), and on each subsequent payment as it is made.

Rule 4: TDS is deducted at the point the threshold is crossed.

If earlier payments were below ₹50 lakh and you did not deduct TDS, that is fine. Once a payment pushes the aggregate above ₹50 lakh, you deduct TDS on the full cumulative amount on that date.

Rule 5: For Form 26QD, you enter the date the threshold was crossed as the deduction date.

The form has a single “Date of Payment/Credit” field. When the threshold is crossed in a later payment, enter that date as the deduction date and consolidate the prior payments.

Worked Examples

Example 1: Paying a contractor in a single payment

Rajiv is building a house in Pune. He is salaried and his accounts are not audited. He hires a civil contractor and pays them ₹75 lakh as a lump sum in August 2025.

- Does Section 194M apply? Yes. Rajiv is an individual not subject to audit, and he is paying a resident contractor more than ₹50 lakh.

- TDS calculation: 2% x ₹75,00,000 = ₹1,50,000

- What Rajiv pays the contractor: ₹75,00,000 minus ₹1,50,000 = ₹73,50,000

- TDS deposited with government via Form 26QD: ₹1,50,000

- Form 26QD due date: Within 30 days from end of August 2025 = 30 September 2025

- Form 16D issued to contractor: Within 15 days from 30 September = 15 October 2025

Example 2: Payments in installments crossing the threshold mid-year

Meera hires an interior designer for her office renovation in Delhi. She is an HUF and not subject to tax audit. The payments are made in stages:

- April 2025: ₹20 lakh advance paid (total so far: ₹20 lakh, below ₹50 lakh, no TDS yet)

- August 2025: ₹35 lakh paid on completion of first phase (total so far: ₹55 lakh, threshold CROSSED)

At the August 2025 payment, the threshold is crossed. TDS is now required on the cumulative total of ₹55 lakh.

- TDS calculation: 2% x ₹55,00,000 = ₹1,10,000

- Meera deducts ₹1,10,000 from the August payment

- What Meera pays the designer in August: ₹35,00,000 minus ₹1,10,000 = ₹33,90,000

- Form 26QD due date: Within 30 days from end of August 2025 = 30 September 2025

- Deduction date entered in Form 26QD: August 2025 (the date the threshold was crossed)

- If more payments are made later in the same year, TDS at 2% must be deducted on each subsequent payment as well

Example 3: Payment that stays under the threshold

A HUF pays a chartered accountant ₹45 lakh in professional fees during FY 2025-26. The threshold of ₹50 lakh is not crossed. No TDS under Section 194M, no Form 26QD required.

Due Dates at a Glance

| Event | Timeline |

| Deduct TDS from payment to contractor/professional | At the time of payment or credit, whichever is earlier |

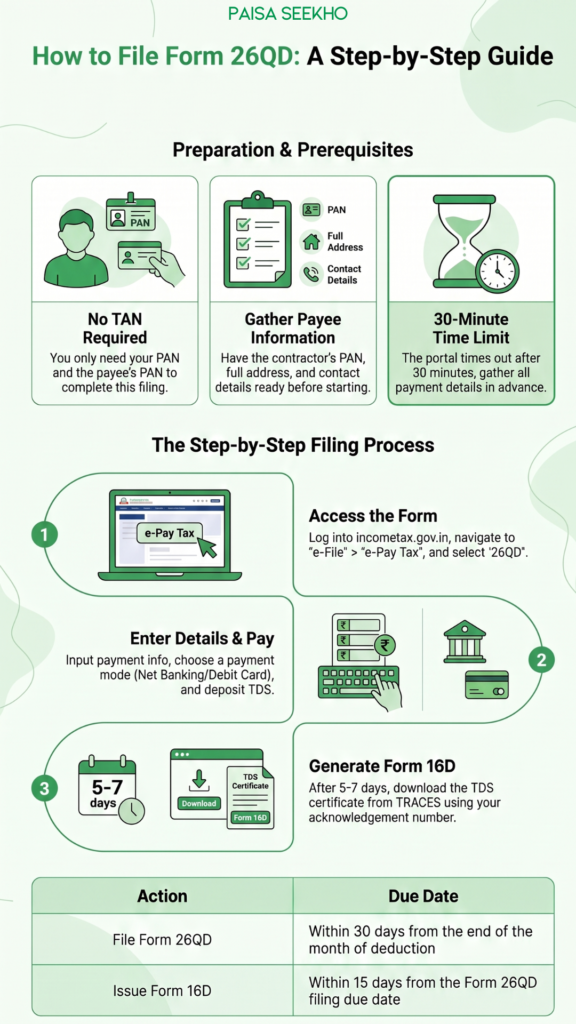

| File Form 26QD and deposit TDS | Within 30 days from the end of the month in which TDS was deducted |

| Issue Form 16D to the payee | Within 15 days from the Form 26QD due date |

Example: TDS deducted on 15 August 2025. Form 26QD due by 30 September 2025. Form 16D due by 15 October 2025.

What Information Do You Need Before Filing?

Have all of the following ready. The portal times out after 30 minutes from when you start, so gathering this in advance avoids losing your progress.

Your details (the deductor):

- PAN

- Name and address

- Contact number and email

Payee details (contractor or professional):

- PAN (mandatory; without it, TDS is 20%)

- Name and address

- Whether they are an individual, firm, company, or other entity

Payment details:

- Nature of the payment (contractor work, professional fees, or commission)

- Total amount paid or credited in the current financial year so far (aggregate)

- Date of payment or credit (or the date the threshold was crossed)

- Date of TDS deduction

- TDS amount

How to File Form 26QD: Step by Step

Form 26QD is filed entirely online through the Income Tax Department’s e-filing portal. No TAN is required.

Step 1: Log into the Income Tax e-filing portal (incometax.gov.in) using your PAN and password.

Step 2: Go to e-File, then e-Pay Tax, then New Payment. Select 26QD (TDS on Contractor Payment) from the list.

Step 3: Fill in the form across its sections:

- Taxpayer info section: Your PAN, name, and address. The system will auto-populate some details from your registered profile.

- Payee details section: Payee’s PAN, name, and address. Verify the PAN carefully. A wrong PAN means the TDS credit will not appear in the contractor’s Form 26AS.

- Contract details section: Nature of payment (contractual work, professional services, or commission/brokerage), financial year, and whether the payee is a resident.

- Payment info section: Aggregate amount paid during the year, amount of current payment, date of credit/payment (the threshold-crossing date if applicable), and TDS deducted.

Step 4: Review all entries and confirm.

Step 5: Select your payment mode (net banking, debit card, or offline via authorised bank) and complete the TDS deposit.

Step 6: On successful payment, download the acknowledgement number and challan. You will need the acknowledgement number to download Form 16D from TRACES.

Step 7: After 5 to 7 working days, log into the TRACES portal (tdscpc.gov.in), navigate to Downloads → Form 16D, and submit a request using the acknowledgement number. Download the certificate, open the ZIP file (password is your PAN in lowercase), and give Form 16D to your contractor or professional.

The Disallowance Risk: A Strong Reason to Comply

There is a financial cost to non-compliance beyond just interest and penalties. Under Section 40(a)(ia) of the Income Tax Act (now Section 35(b) of the new Income Tax Act, 2025), 30% of any sum paid to a resident on which TDS was deductible but not deducted or deposited on time shall be disallowed while computing your taxable income from business or profession.

If you are a small business owner or professional who makes such payments, failing to deduct TDS means you could lose 30% of the expense deduction when calculating your taxable profit. This is on top of the interest and penalty exposure.

For purely personal payments (like building your home), the disallowance does not apply in the same way since there is no business income computation. But the interest and penalty consequences still apply.

Penalties for Non-Compliance

| Default | Consequence |

| TDS not deducted at all | Interest at 1% per month from the date TDS was deductible to the date it is actually deducted |

| TDS deducted but not deposited | Interest at 1.5% per month from the date of deduction to the date of deposit |

| Late filing of Form 26QD | Late fee at ₹200 per day under Section 234E (capped at TDS amount) |

| Non-filing or incorrect information in Form 26QD | Penalty of ₹10,000 to ₹1,00,000 under Section 271H |

| Not issuing Form 16D on time | ₹100 per day under Section 272A(2)(g) |

| 30% expense disallowance | 30% of the payment disallowed in business income computation if TDS not deducted or deposited on time |

The Section 271H penalty for non-filing may be waived if you file Form 26QD, pay the TDS, and settle the interest and late fee within one year of the original due date. After one year, this relief is rarely available.

What the Payee (Contractor or Professional) Should Do

If you are the contractor or professional who has received a payment with TDS deducted, here is what to do:

- Give your PAN to the payer before receiving any payment. Without it, TDS is 20% instead of 2%.

- Collect Form 16D from the payer. This is your official proof of TDS deduction.

- Check your Form 26AS or AIS about 7 to 10 days after the payer files Form 26QD. The TDS credit should appear there. If it does not appear, contact the payer to investigate.

- Report the full gross income in your ITR. The payment you received, before TDS was deducted, is your income. Report it in full in the relevant schedule of your ITR, whether under Income from Business and Profession or Income from Other Sources.

- Claim the TDS as a credit in your ITR. The TDS deducted by the payer reduces your final tax payable for the year, or creates a refund if you have overpaid.

Section 194M vs Section 194C / 194H / 194J: What Is the Difference?

The coverage and applicability of these sections often confuses people. Here is the key distinction:

| Section 194M (Form 26QD) | Sections 194C / 194H / 194J | |

| Who deducts TDS | Individuals/HUFs NOT liable to audit | Companies, firms, and individuals/HUFs liable to audit |

| Threshold | ₹50 lakh aggregate per payee per year | Section 194C: ₹30,000 per transaction or ₹1 lakh per year; 194J: ₹30,000 per year; 194H: ₹15,000 per year |

| TDS rate | 2% (from 1 October 2024) | Varies: 194C at 1%/2%; 194H at 5%; 194J at 2%/10% |

| TAN required? | No | Yes |

| Form used | Form 26QD | Form 26Q (quarterly TDS return) |

| TDS certificate | Form 16D | Form 16A |

| Personal payments covered? | Yes | Generally no |

The simplest way to think about it: Section 194M catches high-value payments by ordinary individuals and HUFs that would otherwise have no TDS obligation. The regular sections (194C, 194H, 194J) cover businesses and audited entities with lower thresholds and a more structured TDS infrastructure.

Form 26QD vs Form 26QB and Form 26QC: Quick Comparison

Across this series of articles, we have covered the “26Q family” of challan-cum-statements for individual and HUF filers. Here is how they all fit together:

| Form | Section | Who Files | What It Covers | Threshold |

| Form 26QB | 194-IA | Property buyer | TDS on property purchase | ₹50 lakh+ transaction value |

| Form 26QC | 194-IB | Tenant | TDS on rent paid by individual/HUF | Monthly rent above ₹50,000 |

| Form 26QD | 194M | Individual/HUF payer | TDS on contractor/professional payments | ₹50 lakh aggregate per year |

If you are building a house, for example, you may need to file both Form 26QB (for the land or flat purchase, if applicable) and Form 26QD (for contractor and architect payments). Our existing guide to Form 26QB on PaisaSeekho covers the property purchase side in detail.

Important: Form 26QD Is Becoming Form 141

Under the Income Tax Act, 2025 (effective from 1 April 2026), Form 26QD is being restructured. According to the Income Tax Department’s TDS Compliance FAQ:

- Form 26QD is merged into a new consolidated form called Form No. 141 (Schedule D) for transactions from 1 April 2026 onwards

- The underlying provision shifts from Section 194M (old Act) to Section 393(1) [Table: S.No. 6(ii)] of the Income Tax Act, 2025

- The corresponding TDS certificate also transitions: Form 16D becomes Form No. 132 under the new framework

- The same due dates apply: Form 141 must be filed within 30 days of deduction, and Form 132 must be issued within 15 days of the Form 141 due date

For all qualifying payments made on or before 31 March 2026: continue using Form 26QD and issuing Form 16D.

For qualifying payments made from 1 April 2026 onwards (Tax Year 2026-27): use Form 141 (Schedule D) and issue Form 132.

Frequently Asked Questions

1. I paid a lawyer ₹60 lakh for personal legal work. Does Section 194M apply?

Yes. Section 194M covers professional services for personal as well as business purposes. If you paid a resident lawyer more than ₹50 lakh in a financial year and you are an individual/HUF not subject to audit, you must deduct 2% TDS and file Form 26QD.

2. I paid a contractor ₹30 lakh and a separate professional ₹25 lakh in the same year. Does the threshold add up?

No. The ₹50 lakh threshold is per payee, not in aggregate across all payments you make. The contractor and the professional are two different people. Neither payment individually crosses ₹50 lakh, so no TDS is required for either.

3. I paid the same contractor ₹30 lakh in FY 2024-25 and ₹25 lakh in FY 2025-26. Does the carryover count?

No. The threshold resets to zero on 1 April every year. Last year’s payments do not carry over into the new financial year.

4. Do I need a TAN to file Form 26QD?

No. Section 194M specifically exempts payers from obtaining a TAN. Your PAN is sufficient to file Form 26QD and download Form 16D from TRACES.

5. The contractor does not have a PAN. What do I do?

You must deduct TDS at 20% instead of 2%. Insist on collecting a valid PAN before making any payment. Paying 20% TDS on a large contractor payment is a significant additional cost for the contractor, and in practice, this is strong motivation for them to provide their PAN.

6. I made payments to the same architect across multiple months. When exactly do I file Form 26QD?

You file Form 26QD at the point when the aggregate crosses ₹50 lakh. At that crossing point, deduct TDS on the entire cumulative amount paid so far, and file Form 26QD within 30 days from the end of that month. For any subsequent payments to the same architect in the same year, deduct TDS on each payment individually and file a separate Form 26QD for each.

7. Can the contractor or professional ask for a lower TDS deduction?

Yes. The payee can apply to the Assessing Officer under Section 197 for a nil or lower TDS certificate, if their estimated tax liability justifies it. If the AO issues such a certificate, the payer deducts TDS at the lower rate specified.

Key Takeaways

- Form 26QD is the challan-cum-statement filed by individuals and HUFs NOT subject to audit who pay a resident contractor, professional, or commission agent more than ₹50 lakh in a financial year.

- It is governed by Section 194M, introduced by the Finance Act, 2019.

- The TDS rate is 2% (from 1 October 2024). Without the payee’s PAN, it jumps to 20%.

- The ₹50 lakh threshold is per payee per year, checks aggregate payments, and once crossed, TDS applies on the entire cumulative amount, not just the excess.

- No TAN required. PAN is sufficient.

- Form 26QD must be filed within 30 days from the end of the month of TDS deduction.

- After filing, download Form 16D from TRACES and issue it to the payee within 15 days from the Form 26QD due date.

- Section 194M covers personal payments too, such as paying a contractor to build your home.

- Non-deduction can result in 30% disallowance of the expense in business income computation, along with interest and penalty exposure.

- From Tax Year 2026-27 (payments from April 2026 onwards), Form 26QD is replaced by Form No. 141 (Schedule D) and Form 16D becomes Form No. 132 under the Income Tax Act, 2025.

Sources: Income Tax Department, Government of India: TDS Compliance FAQs; TRACES: FAQs of Form 26QD; Finance Act (No. 2), 2024: Section 194M TDS rate reduced to 2% effective 1 October 2024, as reported by Taxguru.

This article is for general information only and does not constitute tax or legal advice. For your specific situation, consult a chartered accountant or tax professional.