Quick summary: You pay ₹60,000 rent every month. Your bank balance goes out, your landlord gets paid, and life moves on. But there is a step the income tax law requires you, the tenant, to take once a year that most people miss entirely: deducting 2% TDS from your rent, depositing it with the government, and filing an online form called Form 26QC. This is not something your landlord files. It is not something your employer handles. It falls squarely on you. Missing it attracts interest and penalties, and your landlord loses their TDS credit. This guide explains everything a tenant needs to know about Form 26QC, with worked examples and a step-by-step filing walkthrough.

What Is Form 26QC?

Form 26QC is a challan-cum-statement filed by tenants who are required to deduct TDS on rent under Section 194-IB of the Income Tax Act, 1961. The form serves two purposes at once: it deposits the TDS money with the Central Government and reports the details of the rent transaction to the Income Tax Department, all in one online submission.

The word “challan” refers to a payment receipt or deposit slip. The word “statement” means it also carries information about the transaction, like who paid whom, how much, and for which period. So Form 26QC is essentially: TDS payment plus report, combined into one form, filed online.

It was introduced when the government inserted Section 194-IB into the Income Tax Act in 2017 (effective from 1 June 2017) to bring large rental payments by individual tenants into the TDS net.

After you file Form 26QC, the next step is to download a TDS certificate called Form 16C from the TRACES portal and give it to your landlord. Think of Form 26QC as the filing you do with the government, and Form 16C as the receipt you hand to your landlord. The two are linked: Form 16C can only be generated after Form 26QC is filed.

Who Must File Form 26QC?

Section 194-IB applies to:

- Individual tenants or Hindu Undivided Families (HUFs) who are not required to get their accounts audited under Section 44AB of the Income Tax Act

- Who pay monthly rent exceeding ₹50,000 to a resident landlord

This covers a very wide group: salaried employees, freelancers, self-employed professionals, and HUFs who rent homes or office spaces in cities where rent levels are high.

Who Does NOT Need to File Form 26QC?

- Companies, partnership firms, LLPs, and trusts: These entities deduct TDS on rent under a different section (Section 194-I) and file a quarterly TDS return (Form 26Q), not Form 26QC.

- Individual tenants or HUFs whose accounts are required to be audited under Section 44AB: These also fall under Section 194-I, not 194-IB.

- Tenants whose monthly rent is ₹50,000 or below: No TDS obligation, no Form 26QC required.

- Tenants renting from an NRI landlord: Section 194-IB applies only to resident landlords. If the landlord is an NRI, different rules under Section 195 apply.

If you are a salaried employee in a metro city paying ₹55,000, ₹75,000, or ₹1,00,000 per month in rent to an Indian resident landlord, and your own accounts are not subject to tax audit, Form 26QC is your responsibility.

The TDS Rate Under Section 194-IB

The current TDS rate under Section 194-IB is 2%, applicable from 1 October 2024 onwards, as amended by the Finance Act (No. 2), 2024. For all of FY 2025-26 (April 2025 to March 2026), the rate is 2%.

If the landlord does not provide their PAN, TDS must be deducted at 20%. This is a steep jump, so always collect the landlord’s PAN at the start of the tenancy.

One important cap: the TDS deducted cannot exceed the rent payable for the last month of the tenancy. In most normal situations, 2% of twelve months of rent is well within one month’s rent, so this cap rarely comes into play.

The Key Timing Rule: TDS Is Deducted Once, Not Every Month

This is the most frequently misunderstood aspect of Form 26QC. Unlike TDS on salary (deducted every month) or TDS under Section 194-I (deducted periodically by audited entities), TDS under Section 194-IB is deducted only once, at the time of:

- Payment or credit of rent for the last month of the financial year (typically March, for a tenancy continuing through the year), OR

- Payment or credit of rent for the last month of the tenancy, if the tenant vacates before the financial year ends

Whichever of these happens earlier is when the deduction must be made. The TDS is calculated on the total annual rent paid during that financial year (or tenancy period), not just the last month’s rent.

A Worked Example

Let us walk through two scenarios.

Scenario 1: Full-year tenancy

Arjun pays ₹65,000 per month rent in Bengaluru from April 2025 to March 2026 (12 months). His landlord Mrs. Sharma is a resident Indian.

- Is Form 26QC required? Yes. Rent exceeds ₹50,000/month and both parties are Indian residents.

- When does Arjun deduct TDS? In March 2026, when he pays the last month’s rent.

- Total rent for the year: ₹65,000 x 12 = ₹7,80,000

- TDS at 2%: ₹7,80,000 x 2% = ₹15,600

- What Arjun pays Mrs. Sharma in March: ₹65,000 minus ₹15,600 = ₹49,400

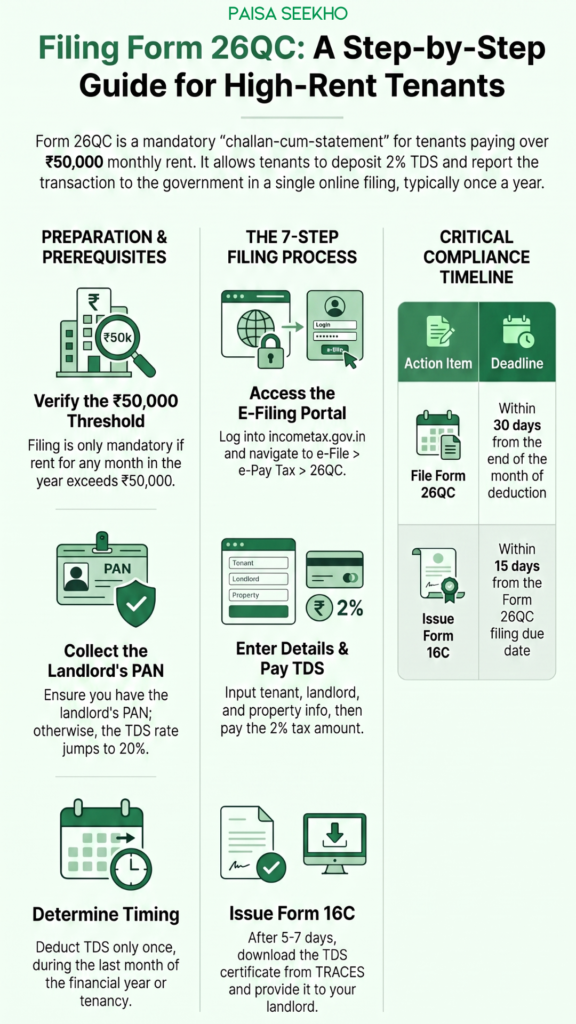

- When must Form 26QC be filed? Within 30 days from the end of March 2026, so by 30 April 2026

- When must Form 16C be issued to Mrs. Sharma? Within 15 days from the Form 26QC due date, so by 15 May 2026

Scenario 2: Mid-year vacation

Kavita pays ₹70,000/month in Delhi from April 2025 to September 2025 (6 months). She vacates in September.

- When does Kavita deduct TDS? In September 2025, the last month of her tenancy.

- Total rent paid: ₹70,000 x 6 = ₹4,20,000

- TDS at 2%: ₹4,20,000 x 2% = ₹8,400

- What Kavita pays her landlord in September: ₹70,000 minus ₹8,400 = ₹61,600

- Form 26QC due date: 30 days from the end of September 2025 = 30 October 2025

- Form 16C due date: 15 days from 30 October 2025 = 14 November 2025

Due Dates at a Glance

| Event | Timeline |

| Deduct TDS from last month’s rent | At the time of paying/crediting rent for the last month of FY or tenancy |

| File Form 26QC and deposit TDS | Within 30 days from the end of the month of TDS deduction |

| Issue Form 16C to landlord | Within 15 days from the Form 26QC due date |

For most tenants whose tenancy runs through the financial year, the typical flow is:

- Deduct TDS in March

- File Form 26QC by 30 April

- Issue Form 16C to landlord by 15 May

What Information Do You Need to File Form 26QC?

Have all of these ready before you start. The form must be completed within 30 minutes of starting on the portal; the session times out after that and you may have to begin again.

Your details (tenant):

- PAN

- Name and address

- Mobile number and email address

Your landlord’s details:

- PAN (mandatory; without it, TDS is at 20%)

- Name and address

- Whether they are an individual, HUF, company, or other entity

Property and tenancy details:

- Complete address of the rented property

- Type of property (residential or commercial)

- Start and end date of the tenancy period for which TDS is being deposited

- Whether there is more than one tenant or landlord

Payment details:

- Total rent paid during the tenancy period

- Date of payment or credit of the last month’s rent

- Date of TDS deduction

- TDS amount (2% of total rent, or as applicable)

How to File Form 26QC: Step by Step

Form 26QC is filed entirely online through the Income Tax Department’s e-filing portal. No TAN is required.

Step 1: Log into the Income Tax e-filing portal (incometax.gov.in) using your PAN and password.

Step 2: Go to e-File, then e-Pay Tax, then New Payment. Select 26QC (TDS on Rent of Property) from the list.

Step 3: The form opens in multiple sections. Fill in all required details:

- Tenant details section: Your PAN, name, address, mobile number, and email. The portal may auto-fill some details based on your registered profile.

- Landlord details section: Landlord’s PAN, name, and address. Verify the PAN carefully. A wrong PAN is the most common and most damaging error in Form 26QC, as it prevents the TDS credit from appearing in your landlord’s account.

- Property and tenancy section: Address of the rented property, property type, tenancy period start and end dates.

- Payment section: Total rent for the period, date of deduction, and TDS amount. The portal does not auto-calculate TDS; you must enter the correct figure.

Step 4: Review all entries carefully before proceeding.

Step 5: Select your payment mode: net banking, debit card, or pay later (offline via authorised bank).

Step 6: Complete the payment. On success, the portal generates a unique acknowledgement number and a challan counterfoil. Download and save both immediately.

Step 7: After 5 to 7 working days, log into TRACES (tdscpc.gov.in), navigate to Downloads → Form 16C, and enter the acknowledgement number to generate the TDS certificate. Download it, open it with the password (your PAN in lowercase), and share it with your landlord.

Multiple Landlords: Filing for Each Share

If the property has two or more co-owners (joint landlords), you must file a separate Form 26QC for each co-owner based on their ownership share.

For example, if a flat is jointly owned by a husband and wife with equal shares, and you pay ₹80,000/month rent:

- Each owner’s share = ₹40,000/month

- TDS for each = 2% x (₹40,000 x 12) = ₹9,600 per owner

- Two Form 26QCs filed, two Form 16Cs issued (one to each owner)

Check the rent agreement to understand how ownership is split. If the agreement does not specify shares, split equally.

Multiple Tenants: Who Files?

If there are multiple tenants sharing a property (for example, two flatmates), the compliance depends on how the rent agreement is structured:

- If the agreement names both tenants as co-lessees, each tenant files a separate Form 26QC for their proportionate share of the rent.

- If the agreement names only one tenant, that tenant bears the full TDS responsibility.

What If TDS on Rent Applies for Only Part of the Year?

If your monthly rent crosses ₹50,000 for some months but not all (for example, you renegotiated the rent mid-year), the TDS is calculated on the actual rent paid during the period in which the higher rent applied, in addition to the rent below the threshold for the remaining months.

However, the trigger for filing Form 26QC is whether the rent at any point during the year exceeds ₹50,000 per month. If it does, even for a single month, Section 194-IB applies, and TDS must be deducted on the total rent paid for the entire tenancy period covered by that agreement.

Penalties for Non-Compliance

| Default | Consequence |

| Not deducting TDS at all | Interest at 1% per month from the date it should have been deducted until actual deduction |

| Deducting TDS but not depositing it | Interest at 1.5% per month from the date of deduction to the date of deposit |

| Filing Form 26QC late | Late fee at ₹200 per day under Section 234E (capped at the TDS amount) |

| Non-filing or furnishing incorrect information | Penalty of ₹10,000 to ₹1,00,000 under Section 271H |

| Not issuing Form 16C to landlord on time | ₹100 per day under Section 272A(2)(g) |

The Section 271H penalty for non-filing may be waived if you file Form 26QC and pay the TDS amount along with interest and late fees within one year of the due date. After one year, relief becomes far harder to obtain.

Form 26QC vs Form 26QB: What Is the Difference?

Both forms deal with property and TDS. They are often confused.

| Form 26QC | Form 26QB | |

| What it covers | TDS on rent paid by individual/HUF tenants | TDS on purchase of immovable property |

| Legal section | Section 194-IB | Section 194-IA |

| Who files it | Tenant | Property buyer |

| Threshold | Monthly rent above ₹50,000 | Property value ₹50 lakh or more |

| TDS rate | 2% (from 1 October 2024) | 1% |

| Filed when | Once a year (at end of FY or tenancy) | For each payment or installment |

| TDS certificate | Form 16C | Form 16B |

| TAN required? | No | No |

For a detailed look at TDS on property purchases and Form 26QB, our existing guide to Form 26QB on PaisaSeekho explains the buying side of property TDS.

Form 26QC vs Quarterly TDS Returns (Form 26Q): What Is the Difference?

Salaried employees may wonder why this form exists separately from the quarterly TDS return system they may be familiar with through their employer. The answer lies in who is doing the deducting.

Employers, companies, and audited entities file Form 26Q (or Form 24Q for salary) every quarter through their TAN. They have a formal, ongoing TDS infrastructure.

Individual tenants under Section 194-IB are ordinary people, not businesses. Asking them to get a TAN, file quarterly returns, and maintain a TDS register would be a disproportionate burden. So Form 26QC was designed as a simpler, one-time-per-year challan-cum-statement that ordinary tenants can file online using only their PAN. Understanding how TDS works in the broader payroll context can be helpful. Our guide on how employers calculate TDS on salary covers the employer-side TDS framework for comparison.

What the Landlord Should Do After Receiving Form 16C

Once you have filed Form 26QC and issued Form 16C, the process passes to your landlord. Here is what they should do:

- Verify the details on Form 16C: Check that the PAN, rent amount, property address, and TDS figure are all correct.

- Cross-check with Form 26AS / AIS: The TDS credit should appear in Part F of their Form 26AS approximately 7 to 10 days after you file Form 26QC. If it does not appear, contact you (the tenant) to investigate.

- Report full rent income in their ITR: The landlord must declare the gross rent received (before TDS deduction) in their Income Tax Return, under the head “Income from House Property.” The TDS can then be claimed as a credit in Schedule TDS-2 of their ITR, reducing or offsetting their final tax payable.

If the landlord’s total tax liability is lower than the TDS deducted, they can claim the difference as a refund when filing their ITR. Our guide to income tax deductions and sections explains how landlords can reduce their taxable rental income through allowable deductions like property-related expenses.

Corrections to Form 26QC

Form 26QC corrections can be requested on the TRACES portal, but they are limited in what can be changed and require the landlord’s digital consent for most modifications.

This is why accuracy at the time of filing is so important. Always double-check:

- Both PAN numbers (yours and your landlord’s)

- The total rent amount for the period

- The tenancy period dates

- The date of TDS deduction

A wrong PAN is the most common mistake. It causes the landlord’s TDS credit to be mapped to a wrong PAN or simply disappear from their Form 26AS, leading to disputes and potential notices for both parties.

Important: Form 26QC Is Becoming Form 141

Under India’s Income Tax Act, 2025 (effective from 1 April 2026), Form 26QC has been renamed and restructured. According to the Income Tax Department’s own TDS compliance FAQs:

- Form 26QC is now replaced by Form No. 141 (Schedule C) under the new framework

- The corresponding TDS certificate changes from Form 16C to Form No. 132

- The underlying provision shifts from Section 194-IB (old Act) to Section 393(3) [Table: S.No. 2(ii)] of the Income Tax Act, 2025

- The due date (30 days from the end of the month of deduction) and the Form 132 issuance deadline (15 days from due date) remain unchanged

- The threshold of ₹50,000/month and the 2% TDS rate are retained

For FY 2025-26 (rent paid up to March 2026): continue using Form 26QC and issuing Form 16C as described in this article. These transactions are governed by the old Income Tax Act, 1961.

From Tax Year 2026-27 (rent from April 2026 onwards): use Form 141 (Schedule C) and issue Form 132 to your landlord.

Frequently Asked Questions

1. Do I need a TAN to file Form 26QC?

No. Section 194-IB specifically exempts tenants from obtaining a TAN. Your PAN and your landlord’s PAN are all that is required.

2. Do I file Form 26QC every month?

No. TDS under Section 194-IB is deducted once in a financial year, at the time of paying the last month’s rent (or the last month of tenancy if vacating early). You file Form 26QC once for that single deduction.

3. My rent is ₹48,000 per month. Do I need to file Form 26QC?

No. Section 194-IB applies only when the monthly rent exceeds ₹50,000. Below this threshold, there is no TDS obligation.

4. I forgot to deduct TDS this year. What should I do?

File Form 26QC as soon as possible. Pay the TDS amount due, along with interest at 1% per month for the period of non-deduction and 1.5% per month after the date TDS should have been deposited. A late filing fee of ₹200 per day under Section 234E also applies. The sooner you file, the lower the total penalty burden.

5. My landlord says they do not want me to deduct TDS. Can I skip it?

No. Deducting TDS is your legal obligation as a tenant under Section 194-IB if the conditions are met. Your landlord’s preference does not change this. They can claim the TDS as a credit in their ITR, which typically reduces their overall tax liability.

6. What if there are two landlords (co-owners) for the same property?

File a separate Form 26QC for each co-owner, based on their respective ownership share. Issue a separate Form 16C to each co-owner.

7. Can I file Form 26QC offline?

No. It is an entirely online process through the Income Tax e-filing portal (incometax.gov.in). Offline filing is not available.

8. The landlord has not received Form 16C yet. Can they still claim TDS credit?

Yes. If the TDS appears in their Form 26AS (which it should, after 5 to 7 days of Form 26QC processing), the landlord can use that Form 26AS entry to claim TDS credit in their ITR even without Form 16C. However, you are still legally required to issue Form 16C on time.

9. Does rent paid to a relative attract Section 194-IB?

Yes. Section 194-IB does not distinguish between a relative and an unrelated landlord. If you pay more than ₹50,000/month in rent to a relative who is a resident Indian, the TDS obligation applies.

Key Takeaways

- Form 26QC is the challan-cum-statement filed by individual and HUF tenants to deposit TDS on rent when monthly rent exceeds ₹50,000.

- The law governing this is Section 194-IB of the Income Tax Act, 1961.

- TDS is deducted at 2% (from 1 October 2024) of the total annual rent, in a single deduction made at the time of paying the last month’s rent of the financial year or tenancy.

- No TAN is needed. Only PANs of the tenant and landlord are required.

- Form 26QC must be filed within 30 days from the end of the month in which TDS was deducted. For most tenants, this is 30 April (for March deductions).

- After filing Form 26QC, download Form 16C from TRACES and issue it to your landlord within 15 days of the Form 26QC due date.

- For multiple co-owners, file a separate Form 26QC (and issue a separate Form 16C) for each owner.

- From Tax Year 2026-27 (rent from April 2026 onwards), Form 26QC is replaced by Form No. 141 (Schedule C) and Form 16C is replaced by Form No. 132 under the Income Tax Act, 2025.

Sources: Income Tax Department, Government of India: TDS Compliance FAQs; Income Tax Department: Form 26QC (Section 194-IB); Finance Act (No. 2), 2024: TDS Rate under Section 194-IB reduced to 2% effective 1 October 2024, as reported by Taxguru.

This article is for general information only and does not constitute tax or legal advice. For your specific situation, consult a chartered accountant or tax professional.