Quick summary: From July 1, 2026, the Pension Fund Regulatory and Development Authority (PFRDA) is rolling out a revised charge structure for Central Recordkeeping Agencies (CRAs) that manage all NPS accounts. If you have a National Pension System account and you have not contributed to it in a long time, you need to know how dormant account charges will now work. And if you have a Tier II NPS account, the way your annual maintenance charge is calculated is also changing. This article explains all the July 1 changes clearly, along with the other major NPS rule updates from 2026 that affect how much you get at retirement, when you can exit, and who can now offer NPS to you.

First: What Is NPS and How Does It Work?

The National Pension System (NPS) is a government-backed, market-linked retirement savings scheme regulated by the PFRDA. You can open it if you are an Indian citizen between 18 and 85 years of age.

When you open an NPS account, you get a unique Permanent Retirement Account Number (PRAN). Within that PRAN, you can have two types of accounts:

- Tier I: The primary pension account. It has a minimum contribution requirement and strict rules on withdrawals. Contributions here get tax benefits.

- Tier II: An optional, flexible account. You can deposit and withdraw freely. No lock-in, but generally no tax benefit for private sector employees (unlike Tier I).

The money you deposit is invested in a mix of equity, corporate bonds, and government securities, depending on the scheme and the allocation you choose. At retirement, part of the corpus must be used to buy an annuity (monthly pension), and the rest can be taken as a lump sum.

For salaried employees, NPS offers one of the most powerful tax-saving options available, especially through:

- Section 80CCD(1): Deduction on your own contribution (within the overall ₹1.5 lakh limit under Section 80C)

- Section 80CCD(1B): Additional deduction of up to ₹50,000 for self-contributions over and above Section 80C

- Section 80CCD(2): Deduction on employer’s NPS contribution, with no upper limit for private sector employees under the new tax regime

NPS July 1, 2026 Changes: What Is Actually Changing?

These changes come from PFRDA Circular No. PFRDA/2026/23/REG-CRA/01 dated April 29, 2026, which clarifies the charge structure for CRAs (the companies that maintain and operate NPS account records). The two main CRAs in India are Protean eGov Technologies and KFintech. The changes come into effect from July 1, 2026.

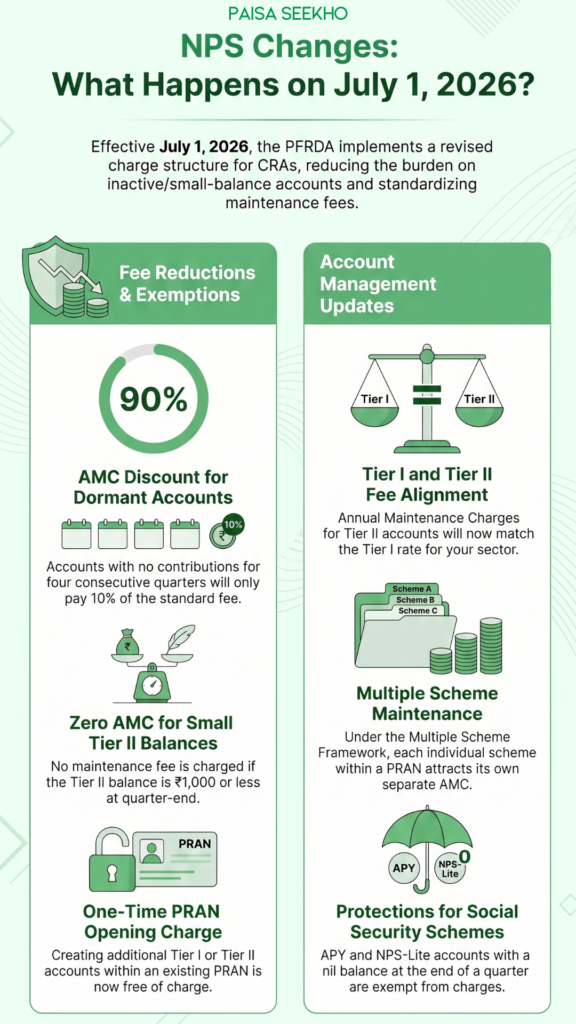

Change 1: Dormant Accounts Now Get a Reduced AMC

This is the most significant change for people who opened an NPS account years ago but have not contributed to it recently.

What is a dormant NPS account?

Under the new rules, an NPS account is classified as dormant if no contribution has been received into it for four consecutive quarters (which is one full year). An account that was dormant but receives a contribution will be flagged as “active” at the start of the next quarter.

What happens to the annual maintenance charge (AMC) on a dormant account?

From July 1, 2026, the AMC on a dormant Tier I or Tier II NPS account will be just 10% of the applicable standard AMC, not the full amount. This is a protective measure. Instead of penalising people with a full fee for an inactive account, the regulator has reduced the charge drastically as long as the account sits idle.

For example, if the standard AMC for your account type is ₹1,000 per year (charged quarterly as ₹250 per quarter), a dormant account will only attract ₹100 per year (₹25 per quarter) until you start contributing again.

What should you do?

If you have an NPS account you have not touched in a year or more, check its status. From July 1, 2026, it will be officially flagged as dormant, and a reduced AMC will apply. This is not a problem in itself but is a good reminder to either reactivate the account (start contributing again) or check that your account details like nominee, contact information, and KYC are up to date.

Change 2: Tier II AMC Is Now Aligned With Tier I

Previously, Tier I and Tier II accounts could have different AMC structures depending on the CRA. From July 1, 2026:

- The AMC for a Tier II account will be set equal to the AMC applicable to the Tier I account under the same sector (Government sector or Private sector).

- This brings uniformity across account types.

- Exception: If your Tier II account balance is ₹1,000 or less at the end of a quarter, no AMC will be charged on that Tier II account for that quarter. This protects subscribers with very small Tier II balances from being charged more than their balance justifies.

Change 3: Each Scheme Within a PRAN Is Treated as a Separate Account

Under the Multiple Scheme Framework (MSF), which was introduced earlier in 2026, NPS subscribers can now hold more than one scheme under the same PRAN. The July 1 clarification confirms that each such scheme will be treated as a separate account for AMC purposes. This means:

- If you have two schemes under your Tier I account, each scheme attracts its own AMC separately.

- This applies to both Tier I and Tier II.

For most subscribers with a single scheme (the default or lifecycle fund), this changes nothing. It mainly affects subscribers who have opted into the MSF and are running multiple pension fund schemes.

Change 4: PRAN Opening Charge Is Now a One-Time Fee

The PRAN opening charge applies only once, at the time your PRAN is first created. From July 1, 2026, there is no charge for activating or opening additional Tier I or Tier II accounts within an existing PRAN. If you already have a PRAN but have not yet opened a Tier II account, adding one costs you nothing.

Change 5: APY and NPS-Lite Nil-Balance Accounts Are Exempt from AMC

If you have an Atal Pension Yojana (APY) account or an NPS-Lite (Swavalamban) account with a nil balance at the end of a quarter, the AMC will be zero. This protects low-income subscribers in social security-focused schemes from being depleted by maintenance charges on empty accounts.

The Bigger Picture: Other Major NPS Changes in 2026

The July 1 changes are important but mostly administrative (fees and account classification). Alongside those, PFRDA has also made some significant rule changes in 2025-2026 that directly affect how much money you get at retirement and how flexible NPS is as a retirement tool. Here is a consolidated picture.

You Can Now Withdraw More as a Lump Sum at Retirement

Old rule: At superannuation (retirement at 60), you were required to use at least 40% of your NPS corpus to purchase an annuity (a monthly pension product). You could take only 60% as a lump sum.

New rule (effective 2025-26): For non-government sector NPS subscribers, the mandatory annuity purchase has been reduced to just 20% of the corpus. You can now take up to 80% as a lump sum at retirement, provided your total corpus exceeds ₹12 lakh.

This is a meaningful change for private sector subscribers who were reluctant to lock away 40% of their corpus in low-yielding annuity products.

For smaller corpuses: If your total NPS corpus at retirement is ₹8 lakh or less, you can withdraw 100% as a lump sum, with no obligation to purchase an annuity at all. The earlier threshold for this was ₹2.5 lakh, so this is a significant increase in the lump-sum-exit option for smaller savers.

You Can Now Stay Invested in NPS Until Age 85

NPS subscribers can now stay invested in the system until age 85, up from the earlier limit of 70 years. This is relevant for people who want to stay invested longer, especially if they have other income sources and do not need to draw down the NPS corpus immediately at 60.

Partial withdrawals from Tier I remain allowed (up to 25% of your own contributions) under specified circumstances like higher education, marriage, purchase or construction of a home, or critical illness, and subject to conditions.

Systematic Unit Redemption: A New Way to Withdraw

PFRDA has introduced a new withdrawal mode called Systematic Unit Redemption (SUR). Instead of withdrawing the entire lump sum at once, subscribers from both the government and non-government sectors can now draw down their NPS corpus gradually over a period of at least six years. Units are redeemed systematically, similar to how a Systematic Withdrawal Plan (SWP) works in mutual funds.

This gives retirees more flexibility to manage their withdrawals based on actual cash flow needs rather than being forced to take everything out at once.

Multiple Scheme Framework: Invest in More Than One Scheme

From 2026, NPS subscribers can invest in more than one scheme under the same PRAN through the Multiple Scheme Framework. Earlier, a subscriber could invest through only one pension fund manager per account.

Under MSF:

- You can split your NPS contributions across multiple schemes, choosing based on risk appetite and goals.

- This allows better diversification within your pension savings.

- Different pension fund managers have launched MSF schemes catering to different risk profiles.

For beginners, the default or auto-choice lifecycle funds still work perfectly well. MSF is more relevant for subscribers who want more hands-on control.

Banks Can Now Become Pension Fund Managers

From January 1, 2026, Scheduled Commercial Banks (SCBs) are allowed to sponsor and manage NPS. Earlier, only non-bank entities were pension fund managers. This change means more banks may start actively offering NPS products and services, making the scheme more accessible, especially in tier 2 and tier 3 cities where bank branches are often the primary financial touchpoint.

New Investment Options: Gold and Silver ETFs

Pension funds under NPS can now invest in Gold and Silver ETFs as part of their equity portfolio, with an allocation cap of up to 5% of the equity portfolio in Gold/Silver ETFs. This adds a commodity-linked layer to the portfolio, which can provide a hedge against inflation over the long term.

What These Changes Mean for You, Depending on Where You Stand

If you are a young salaried employee in the private sector (20s to 30s) with a corporate NPS account:

The biggest benefit for you is the Section 80CCD(2) deduction on your employer’s NPS contribution, which is allowed even under the new tax regime. The July 1 changes will not materially affect you since you are contributing regularly and your account is not dormant. The MSF option gives you more investment control if you want it.

If you opened an NPS account for tax saving a few years ago but stopped contributing:

July 1, 2026 is directly relevant to you. Your account will be officially classified as dormant, and the AMC drops to 10% of normal. Check your account status, update your KYC and nominee details, and consider whether to reactivate by making contributions. Even a small contribution once a year is enough to keep the account active.

If you are a government employee under NPS:

The All India Services (Implementation of NPS) Rules, 2026, notified by the Ministry of Personnel on April 22, 2026, formalise the framework for IAS, IPS, and IFoS officers. For central government employees more broadly, you continue contributing 10% of (Basic + DA), your employer contributes 14%, and the July 1 charge changes apply to your CRA fee structure as well.

If you are approaching retirement (50s to 60s):

The reduced annuity requirement (20% instead of 40%) and the higher lump sum threshold (100% withdrawal for corpus up to ₹8 lakh) are the most impactful changes. The SUR option gives you more control over how you draw down your corpus. Our guide to income tax deductions and sections covers how NPS withdrawals are taxed at the time of exit.

NPS and Taxes: A Quick Refresher

Since NPS is frequently discussed as a tax-saving tool, here is a concise summary of how contributions and withdrawals are taxed:

At the contribution stage:

- Section 80CCD(1): Your own contribution is deductible, subject to 10% of salary, within the overall ₹1.5 lakh Section 80C limit

- Section 80CCD(1B): An additional ₹50,000 deduction on your own contributions, over and above Section 80C. Available under the old tax regime.

- Section 80CCD(2): Deduction on employer’s NPS contribution. Available under both old and new tax regimes. No monetary limit for private sector employees, though capped at 14% of Basic + DA.

At the withdrawal stage:

- Lump sum withdrawal of up to 60% of corpus at retirement: Tax-free under Section 10(12A)

- Amount used to purchase annuity: Tax-free at the time of purchase, but the annuity income received monthly is taxable as per your slab rate

- Partial withdrawals during the accumulation phase (up to 25% of own contributions, under qualifying circumstances): Tax-free under Section 10(12B)

- Lump sum withdrawal on death: The full corpus is paid to the nominee, and it is tax-free

For the additional 20% that non-government subscribers can now withdraw as a lump sum (since the annuity requirement is reduced from 40% to 20%), that extra 20% is taxable as per your income tax slab at the time of withdrawal. Only 60% of the corpus remains fully tax-exempt as a lump sum. The new flexibility is real, but plan for the tax on the additional 20%.

Our income tax slabs guide explains the current slab rates to help you plan how this withdrawal will be taxed.

What to Do Before July 1, 2026

Since July 1 is just days away, here is a practical checklist:

- Check if your NPS account is dormant. Log into the NPS portal (npscra.nsdl.co.in or the KFintech portal, depending on your CRA) or through your bank’s NPS interface. If you have not contributed in the last 12 months, it will be flagged dormant from July 1.

- Update your KYC and nominee details. Dormant accounts often have outdated details. Take this as an opportunity to ensure everything is current, especially your mobile number, email, and nominee.

- Decide whether to reactivate. Even a small contribution reactivates the account and brings it back to full active status from the next quarter. If you want to keep the account alive and growing, resume contributions.

- If you have a Tier II account with a small balance: Check whether your balance is ₹1,000 or less. If so, no AMC will be charged from July 1. If it is slightly above ₹1,000, consider whether you want to add to it or let it ride.

- If you are considering opening a new NPS account: The PRAN opening charge is now one-time. Adding a Tier II account later costs nothing extra. There is no financial reason to delay.

Frequently Asked Questions

1. What exactly is changing in NPS from July 1, 2026?

Three specific changes kick in from July 1: dormant accounts (no contributions for four consecutive quarters) will be officially flagged as dormant and charged only 10% of the normal AMC; Tier II account AMC is aligned with Tier I AMC in the same sector; and PRAN opening charges are officially confirmed as a one-time fee only.

2. Will my NPS account be closed if it becomes dormant?

No. A dormant NPS account is not closed or terminated. It continues to exist, remains invested in the market, and continues to earn returns. It is just charged a lower AMC. You can reactivate it at any time simply by making a contribution.

3. I have a Tier II NPS account with ₹800 in it. Will I be charged AMC?

No. Effective July 1, 2026, Tier II accounts with a corpus of ₹1,000 or less at the end of a quarter are exempt from AMC. You will not be charged anything until your balance crosses ₹1,000.

4. Does the reduced annuity requirement (20% instead of 40%) apply to government employees?

The reduced annuity requirement and the enhanced lump sum flexibility primarily apply to non-government sector NPS subscribers. Government sector employees follow specific rules set by the government. If you are a central government employee, check with your HR or accounts department for rules applicable to you.

5. How much of my NPS corpus is tax-free at retirement?

The lump sum withdrawal of up to 60% of the total corpus at retirement is tax-free under Section 10(12A). If you withdraw the additional 20% (now allowed instead of mandatory annuity purchase), that portion is taxable at your slab rate. The annuity income received monthly after buying the annuity with 20% of the corpus is also taxable as income.

6. What is the Multiple Scheme Framework in NPS?

MSF allows NPS subscribers to invest in more than one pension fund scheme under the same PRAN, enabling diversification across fund managers and investment styles. It is optional. If you do not opt for it, your existing single-scheme arrangement continues unchanged.

7. Can I now open NPS through my bank?

From January 1, 2026, Scheduled Commercial Banks can act as pension fund managers under NPS. Many banks already offered NPS as Points of Presence. Now banks can also manage the pension funds directly, which should result in broader product availability over time.

Key Takeaways

From July 1, 2026, three specific NPS changes take effect per PFRDA Circular No. PFRDA/2026/23/REG-CRA/01 (dated April 29, 2026):

- Dormant accounts (no contribution for four consecutive quarters) attract only 10% of the standard AMC.

- Tier II AMC is aligned with Tier I AMC under the same sector. Tier II accounts with a corpus of ₹1,000 or less at the end of a quarter attract zero AMC.

- PRAN opening charge is one-time only. Opening additional Tier I or Tier II accounts within an existing PRAN is free.

Beyond July 1, the key 2026 NPS changes that affect your retirement are:

- Reduced annuity requirement: Non-government subscribers can now annuitise just 20% of the corpus (down from 40%), taking up to 80% as a lump sum.

- Full withdrawal for smaller corpuses: 100% lump sum exit if your corpus is ₹8 lakh or less (up from ₹2.5 lakh).

- Extended investment period: Stay in NPS until age 85.

- Systematic Unit Redemption: A new phased withdrawal option of at least 6 years.

- Multiple Scheme Framework: Invest in more than one scheme under the same PRAN.

- Banks as pension fund managers: SCBs can now manage NPS funds from January 2026.

Sources: PFRDA Circular No. PFRDA/2026/23/REG-CRA/01 dated April 29, 2026: Charge Structure of CRAs under Pension Schemes, as reported by Taxguru; Business Today: NPS charge structure updated, May 2026; HDFC Pension: Recent NPS Changes 2026; PFRDA Exits and Withdrawals Regulations 2015 as amended, summarised by CAalley.com.

This article is for general information and does not constitute financial or investment advice. For decisions specific to your retirement planning, consult a SEBI-registered investment advisor or a qualified financial planner.