Quick summary: If your business turnover crosses ₹1 crore or your professional income crosses ₹50 lakh in a financial year, you are required under Section 44AB of the Income Tax Act to get your books of accounts audited by a Chartered Accountant. That CA then submits an audit report in one of two forms. If your accounts are already audited under another law (like the Companies Act), the CA uses Form 3CA. If your accounts are audited only for income tax purposes and no other law requires an audit, the CA uses Form 3CB. Both forms are always accompanied by a detailed statement called Form 3CD. This guide explains what all three forms cover, who uses which, and what it means for your business or profession.

What Is a Tax Audit Under Section 44AB?

A tax audit is not the same as a regular statutory audit done for companies under the Companies Act. A tax audit under Section 44AB of the Income Tax Act, 1961 is a specific check of your financial records conducted by a Chartered Accountant (CA) who holds a full-time Certificate of Practice from the Institute of Chartered Accountants of India (ICAI). The purpose is to verify that:

- Your income and expenses are correctly recorded and reported

- You have correctly computed your taxable income

- You have complied with TDS obligations, cash transaction rules, and other income tax provisions

- You have not overstated deductions or understated income

The requirement for a tax audit was introduced by the Finance Act, 1984, effective from Assessment Year 1985-86. It was designed to discourage tax evasion by creating an independent verification layer for high-turnover taxpayers.

When the CA completes the audit, they submit a formal audit report to the Income Tax Department through the e-filing portal. That report is submitted in either Form 3CA or Form 3CB, plus the mandatory accompanying Form 3CD.

Who Needs a Tax Audit? Section 44AB Thresholds for FY 2025-26

Before understanding the forms, you need to know whether a tax audit applies to you at all for the current financial year.

Under Section 44AB of the Income Tax Act, a tax audit is mandatory in the following situations for FY 2025-26:

| Category | Condition |

| Business (any type of entity) | Total sales, turnover, or gross receipts exceed ₹1 crore in the financial year |

| Business (enhanced digital threshold) | Turnover exceeds ₹1 crore but does not exceed ₹10 crore, provided that cash receipts are 5% or less of total receipts AND cash payments are 5% or less of total payments |

| Professional (doctor, lawyer, CA, architect, etc.) | Gross receipts exceed ₹50 lakh in the financial year |

| Presumptive taxpayer under Section 44AD (business) | Opts to declare income below 8% (or 6% for digital receipts) of turnover, AND total income exceeds the basic exemption limit |

| Presumptive taxpayer under Section 44ADA (professional) | Opts to declare income below 50% of gross receipts, AND total income exceeds the basic exemption limit |

A few important points:

- The ₹10 crore digital threshold applies only to businesses, not professionals. For professionals, the audit limit is ₹50 lakh regardless of how they receive payments.

- Tax audit applicability is assessed fresh for each financial year. Being audited one year does not automatically mean the next year requires an audit.

- Entities already covered by audit under another law (Companies Act, LLP Act, Co-operative Societies Act) do not need a separate fresh audit under the Income Tax Act. They simply use the existing audit to certify income tax compliance as well.

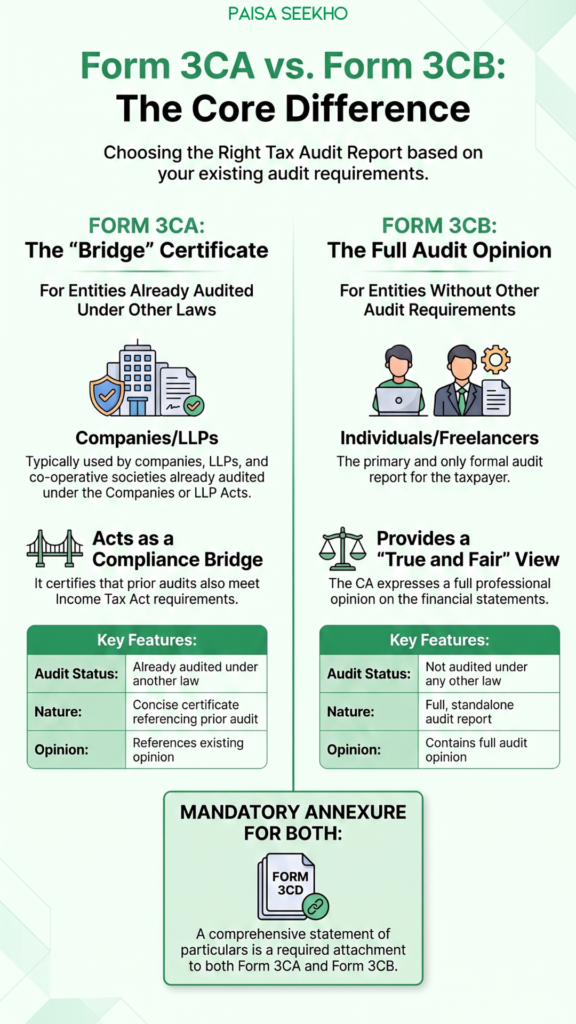

The Core Difference Between Form 3CA and Form 3CB

This is the heart of the article and the question most business owners or their accountants face: which form applies to us?

The answer depends entirely on whether your accounts are already required to be audited under any other law in force in India.

Form 3CA: For Those Already Audited Under Another Law

Form 3CA is used when the taxpayer carries on a business or profession and is already required to get their accounts audited under any law other than the Income Tax Act. In such cases, the accounts have already been examined under that other law. The CA submits Form 3CA to certify that those accounts also comply with the requirements of Section 44AB of the Income Tax Act.

Think of Form 3CA as a certificate saying: “These accounts were already audited under [Company Law / LLP Act / etc.], and based on that audit, they also meet the income tax audit requirements.”

Who typically uses Form 3CA:

- Companies: All companies registered under the Companies Act, 2013 are required to get their accounts audited under that Act. So any company that also crosses the Section 44AB threshold uses Form 3CA.

- Limited Liability Partnerships (LLPs): LLPs above a certain threshold are required to get audited under the LLP Act, 2008. They use Form 3CA.

- Co-operative societies: Covered by state co-operative society laws that require audits.

- Certain banks and insurance companies: Covered by sector-specific legislation.

What Form 3CA contains:

- Name, address, and PAN of the assessee

- Date of the audit report

- A reference to the specific law under which accounts were audited (for example, Companies Act, 2013)

- A statement that the accounts were audited under that law before the due date for furnishing the return under Section 44AB

- A declaration that all particulars in the attached Form 3CD are true and correct

- Any qualifications or observations the CA wishes to add

- CA’s name, membership number, Firm Registration Number (FRN), signature, and stamp

The form is relatively concise because the heavy lifting (the actual audit opinion) has already been done under the other law. Form 3CA serves primarily as a declaration and a bridge between that other audit and the income tax reporting requirements.

Form 3CB: For Those Not Audited Under Any Other Law

Form 3CB is used when the taxpayer carries on a business or profession and is not required to get their accounts audited under any law other than the Income Tax Act. For these taxpayers, the income tax audit is the only formal audit they undergo, and so Form 3CB serves as the primary, full-length audit report.

Think of Form 3CB as the CA’s complete opinion on your accounts, prepared entirely for income tax purposes.

Who typically uses Form 3CB:

- Sole proprietorships: A shop owner, a trader, or any individual running their own business without any company or LLP structure. No other law mandates an audit for them, so Form 3CB is used.

- Partnership firms (non-LLP): Traditional partnership firms (governed by the Indian Partnership Act, 1932) are not required to get a statutory audit under any other law. If their turnover crosses ₹1 crore, they use Form 3CB.

- Freelancers and independent professionals: A freelance designer, consultant, or IT contractor whose gross receipts cross ₹50 lakh files under Form 3CB.

- Hindu Undivided Families (HUFs) with business income: Similar to sole proprietorships.

What Form 3CB contains:

- Name, address, and PAN of the assessee

- The assessment year and the previous year (financial year) to which the audit pertains

- Address where the books of accounts are maintained and branches if any

- A full audit examination statement: the CA declares that they have examined the Balance Sheet and Profit and Loss Account for the relevant year

- An audit opinion on whether the accounts give a true and fair view of the state of affairs and the profit or loss

- Any observations, qualifications, or matters the CA wishes to flag

- A declaration that the particulars in the attached Form 3CD are true and correct to the best of the CA’s knowledge and belief

- CA’s name, membership number, Firm Registration Number, signature, date, place, and stamp

Unlike Form 3CA, Form 3CB includes a full audit opinion because this is the only audit being conducted on these accounts. The CA is taking full professional responsibility for expressing a view on whether the financial statements are true and fair.

Form 3CA vs Form 3CB: A Side-by-Side Comparison

| Form 3CA | Form 3CB | |

| Used when | Accounts already audited under another law (Companies Act, LLP Act, etc.) | Accounts not audited under any other law |

| Who files it | Companies, LLPs, co-operative societies | Proprietorships, partnership firms, HUFs, individuals/freelancers |

| Nature of the form | A certificate referencing the prior audit | A full, standalone audit report |

| Contains full audit opinion? | No, references opinion already given under other law | Yes, CA gives a full true-and-fair-view opinion |

| Legal basis | Rule 6G(1)(a) of Income Tax Rules, 1962 | Rule 6G(1)(b) of Income Tax Rules, 1962 |

| Must be accompanied by | Form 3CD | Form 3CD |

| Filed by | Chartered Accountant via DSC on e-filing portal | Chartered Accountant via DSC on e-filing portal |

| Taxpayer must approve? | Yes, after CA files | Yes, after CA files |

What Is Form 3CD?

Regardless of whether Form 3CA or Form 3CB is used, both must be filed together with Form 3CD. You cannot file either form without Form 3CD. It is a mandatory annexure to the audit report.

Form 3CD is a detailed statement of particulars that gives the Income Tax Department a comprehensive picture of the taxpayer’s financial position and compliance record. It is divided into two parts:

Part A (Clauses 1 to 8): Basic details of the assessee including name, address, PAN, nature of business or profession, and the method of accounting used (cash or mercantile basis).

Part B (Clauses 9 to 44): The substantive part, covering a wide range of disclosures including:

- Details of turnover, gross receipts, or sales

- Amounts of expenditure, purchases, and income

- TDS compliance: whether TDS was deducted and deposited on all applicable payments

- Whether cash transactions exceeded the limits prescribed under Section 40A(3) (payments above ₹10,000 in cash for business expenses)

- Depreciation claimed, method used, and whether it is as per Income Tax rules

- Amounts inadmissible under various sections (unamortised expenses, unexplained investments, etc.)

- Details of deductions claimed under Sections 80C, 80G, 80-IC, 80IB, and others

- Details of losses carried forward or set off

- International transactions or specified domestic transactions requiring transfer pricing documentation

- Income or expenditure that is subject to tax at special rates

- Whether the accounts are maintained on a computer-based system or manually

The CA examines all of these items and certifies whether the disclosures are true and correct. If there are issues, the CA notes them as qualifications or observations.

Form 3CD preparation and review: The management of the business or profession is responsible for preparing the information that goes into Form 3CD. The CA reviews this, verifies it against the books of accounts, and submits the form.

The Filing Process: Step by Step

The entire tax audit report filing process is electronic. Here is how it works for FY 2025-26 (AY 2026-27):

Step 1: The taxpayer appoints a Chartered Accountant with a valid Certificate of Practice and adds the CA as an Authorised Representative on the Income Tax e-filing portal.

Step 2: The CA logs into the e-filing portal using their own credentials and accesses the taxpayer’s assigned forms.

Step 3: The CA fills in Form 3CA or Form 3CB (as applicable) and Form 3CD using the offline utility provided by the portal.

Step 4: The CA uploads the completed forms along with supporting documents (balance sheet, profit and loss account, and other annexures) and signs them using their Digital Signature Certificate (DSC).

Step 5: Once the CA submits the forms, the taxpayer receives a notification on their e-filing account.

Step 6: The taxpayer logs in and either accepts or rejects the audit report. If the taxpayer finds any error, they can reject it and the CA must make corrections and resubmit.

Step 7: On acceptance by the taxpayer, the audit report is formally submitted to the Income Tax Department.

Due Dates for FY 2025-26

The tax audit report for FY 2025-26 (Assessment Year 2026-27) must be filed by 30 September 2026 as per the standard deadline under Section 44AB. This date is specifically for taxpayers who are not involved in international transactions requiring a transfer pricing audit.

For taxpayers who have entered into international transactions (and therefore also require a transfer pricing report under Section 92E), the deadline is 31 October 2026.

Note that for the previous year (FY 2024-25, AY 2025-26), the CBDT extended the standard deadline from 30 September 2025 to 31 October 2025. Such extensions are announced by CBDT if needed and may also apply to future years, though they cannot be relied upon in advance.

ITR filing deadline for audited taxpayers: Those required to get a tax audit must file their Income Tax Return by 31 October 2026 for FY 2025-26. The return cannot be filed before the audit report is accepted.

Penalty for Not Getting a Tax Audit Done

If you are required to get a tax audit done under Section 44AB but fail to do so, the penalty under Section 271B is the lower of:

- 0.5% of your total sales, turnover, or gross receipts for the year, OR

- ₹1,50,000

For example, a partnership firm with ₹1.5 crore in turnover that fails to get a tax audit done faces a penalty of ₹75,000 (0.5% of ₹1.5 crore), since this is lower than ₹1,50,000.

The penalty may be waived if you can show a reasonable cause for the failure. Courts and tribunals have accepted reasons such as the sudden death or resignation of the CA, labour strikes or lockouts, and loss of accounts due to fire or floods. Simply being busy or not being aware of the law does not qualify as a reasonable cause.

Note: Budget 2026 has proposed converting this from a “penalty” to a “fee” under the new Income Tax Act, 2025, to reduce the scope for litigation. The financial impact on the taxpayer remains the same.

Common Mistakes to Avoid

Choosing the wrong form:

A private limited company or an LLP must use Form 3CA, since their accounts are already audited under the Companies Act or LLP Act. Using Form 3CB for a company would be incorrect.

Submitting Form 3CA without Form 3CD:

Both parts must be submitted together. Form 3CD cannot be omitted regardless of which audit form is used.

Not approving the audit report on time:

Once the CA files the forms, the taxpayer must log in and accept the report before the due date. Simply waiting for your CA to file without actively approving the form can result in the audit report not being registered.

Engaging a CA without a Certificate of Practice:

Only a CA who holds a full-time Certificate of Practice (COP) from ICAI can conduct a tax audit and issue the audit report. An employee CA or a CA without a COP cannot conduct or certify a Section 44AB audit.

Assuming the statutory audit covers income tax audit requirements automatically:

A company’s statutory audit under the Companies Act does not replace the need to file the audit report in Form 3CA with the Income Tax Department. Both are separate compliances.

Important: Form 3CA, 3CB, and 3CD Are Merging Into Form 26

Under the Income Tax Act, 2025 (effective from 1 April 2026) and the Income Tax Rules, 2026, Forms 3CA, 3CB, and 3CD are all being consolidated into a single new form called Form No. 26. This unification is part of the broader simplification effort under the new Act.

For FY 2025-26 (income earned up to 31 March 2026): the audit report continues to be filed in Forms 3CA/3CB and 3CD as described in this article.

For Tax Year 2026-27 (income from April 2026 onwards): the consolidated Form No. 26 under the Income Tax Rules, 2026 will apply. The underlying concept (two tracks based on whether a separate statutory audit exists) is expected to be retained in the new form, but the structure and numbering will change.

Frequently Asked Questions

1. Who can conduct a tax audit under Section 44AB?

Only a Chartered Accountant who holds a full-time Certificate of Practice (COP) from ICAI. An internal accountant, a CA employee, or a CA without a COP cannot conduct this audit. The CA must be appointed by the taxpayer.

2. My turnover was ₹1.1 crore last year, so I got a tax audit done. This year it is ₹85 lakh. Do I still need an audit?

No. Tax audit applicability is assessed each year independently based on that year’s turnover. If your turnover for FY 2025-26 is ₹85 lakh, a tax audit is not required (assuming you are a business, not a professional, and meet no other audit triggers).

3. I am a freelance consultant earning ₹55 lakh. Which form does my CA use?

Your CA will use Form 3CB, since your accounts are not audited under any other law. As a freelancer (professional), your gross receipts exceed ₹50 lakh, so a tax audit under Section 44AB is mandatory.

4. Our company (private limited) had a turnover of ₹5 crore. Which form applies?

Form 3CA. Your company’s accounts are already audited under the Companies Act, 2013 by your statutory auditor. The income tax audit report is filed in Form 3CA alongside Form 3CD.

5. Does the taxpayer or the CA file Form 3CD?

The CA files Form 3CD on the e-filing portal. However, the information in Form 3CD is based on data provided by the management of the business. The CA verifies the information and certifies its correctness. After the CA submits, the taxpayer must approve the report on their own e-filing account.

6. Can the same CA who does the statutory audit also do the tax audit?

Yes. There is no restriction on the same CA conducting both. In fact, for companies, it is common (and often more efficient) for the same firm to do both the statutory audit and prepare the tax audit report in Form 3CA.

7. What happens if the CA and the taxpayer disagree on something in the audit report?

The CA has the right to note qualifications or observations in Form 3CA/3CB or Form 3CD if they believe certain disclosures or treatments are incorrect. These observations become part of the official audit report and may draw attention from the Income Tax Department during scrutiny.

8. Is the income tax audit report the same as filing the ITR?

No. These are separate steps. The tax audit report (Forms 3CA/3CB and 3CD) must be submitted by the CA and accepted by the taxpayer first. Only after this can the taxpayer file their Income Tax Return. The ITR due date for audited taxpayers is typically 31 October.

Key Takeaways

- Form 3CA and Form 3CB are both tax audit report forms filed under Section 44AB of the Income Tax Act, 1961, governed by Rule 6G of the Income Tax Rules, 1962.

- Form 3CA applies when the taxpayer’s accounts are already audited under another law such as the Companies Act or LLP Act. It is used by companies, LLPs, and similar entities.

- Form 3CB applies when the taxpayer’s accounts are not audited under any other law. It is used by proprietorships, partnership firms, HUFs, and individual professionals or freelancers.

- Both forms must be filed together with Form 3CD, a detailed statement of particulars covering income, deductions, TDS compliance, cash transactions, and other key financial disclosures.

- Only a CA with a valid Certificate of Practice from ICAI can conduct a tax audit and sign the report.

- For FY 2025-26, the tax audit report is due by 30 September 2026 (31 October 2026 for those with international transactions). The ITR for audited taxpayers is due by 31 October 2026.

- Non-compliance attracts a fee of the lower of 0.5% of turnover/gross receipts or ₹1,50,000 under Section 271B.

- From Tax Year 2026-27 (income from April 2026 onwards), Forms 3CA, 3CB, and 3CD are unified into a new Form No. 26 under the Income Tax Act, 2025.

Sources: Income Tax Department, Government of India: Form 3CA-3CD User Manual; Income Tax Department: Section 44AB; ClearTax: Tax Audit Section 44AB; Legal Suvidha: Section 44AB Tax Audit Limit FY 2025-26.

This article is for general information only and does not constitute tax or professional advice. For your specific situation, consult a practising Chartered Accountant.