Quick summary: Two Gold ETFs can hold identical, 99.5% purity physical gold and still cost you very different amounts to actually trade, purely because of liquidity. Liquidity is not about how good the fund is at tracking gold; it is about how cheaply and quickly you can convert your ETF units back into cash, or cash into units, at a fair price, on any given day. A fund with low trading volume can cost you 0.5% to 1% just crossing the bid-ask spread on entry and exit. This is a cost that never appears on any factsheet’s headline numbers. This guide explains exactly what liquidity means for a Gold ETF, how to check it yourself before placing an order, and when it genuinely matters versus when it barely matters at all.

What Does “Liquidity” Actually Mean for a Gold ETF?

ETF liquidity refers to how easily and quickly an ETF can be bought or sold in the market without causing a significant impact on its price. It determines your ability to enter or exit a position at the desired price and with minimal slippage, the difference between the price you expected and the price you actually got.

This is a genuinely separate concept from the fund’s expense ratio (an annual, ongoing fee) and its tracking error (how faithfully it mirrors gold prices over time), both covered in our companion articles on expense ratio comparison and tracking error. Liquidity is specifically about the cost and ease of the transaction itself, at the moment you buy or sell.

Where Does Gold ETF Liquidity Actually Come From?

ETF liquidity is influenced by two distinct sources, and understanding both explains why a low-volume fund is not necessarily as illiquid as it might first appear.

Primary market liquidity

This comes from the ETF issuer and Authorised Participants (APs), large institutions that can create or redeem ETF units directly with the fund in large blocks, as covered in detail in our how Gold ETFs track gold prices guide. This mechanism ensures the ETF’s price remains close to its Net Asset Value, regardless of how much day-to-day trading is happening on the exchange itself.

Secondary market liquidity

This is what most retail investors actually experience: the ease of buying or selling existing ETF units directly on the stock exchange, at whatever price other buyers and sellers, along with designated market makers, are currently quoting.

This is why trading volume alone does not tell the whole story.

Even if a Gold ETF does not trade frequently on the exchange, Authorised Participants can still create or redeem units in the primary market, which provides a liquidity backstop that a simple volume chart does not capture. That said, for a typical retail investor placing a normal-sized order through their broker, secondary market conditions, trading volume, market maker presence, and the resulting bid-ask spread, are what you will actually experience and pay for.

What Is the Bid-Ask Spread, and Why Does It Matter So Much?

The bid-ask spread is the difference between the highest price buyers are currently willing to pay (the bid) and the lowest price sellers are currently asking (the ask) for the same ETF unit. A narrower spread means lower transaction costs and better pricing; a wider spread quietly eats into your returns, particularly for frequent traders or large orders.

How to think about the actual cost this imposes:

In theory, the fund’s fair value sits somewhere near the midpoint of the bid-ask spread. If you buy at the ask price, you are paying slightly above this fair value; if you sell at the bid, you are receiving slightly below it. As one detailed cost analysis illustrates, the trading cost incurred by an investor crossing a spread of, say, 0.033% works out to roughly half that figure, around 0.0165%, since that is the premium paid over the fair midpoint to complete the transaction. For a fund with a much wider spread, this crossing cost is correspondingly larger and directly reduces your net return on that specific transaction, independent of anything the fund’s expense ratio or tracking performance might otherwise suggest.

What actually drives the spread wider or narrower:

- Trading volume: an increase in the volume of units being traded generally results in tighter spreads, since more buyers and sellers are actively quoting prices close to fair value.

- Underlying asset liquidity: since gold itself is a globally, continuously traded asset, the underlying liquidity of physical gold generally supports tight spreads for well-established Gold ETFs, though fund-specific factors (AUM, market maker participation) still create meaningful differences between individual funds.

- Market volatility: spreads tend to widen during periods of higher volatility, since market makers face greater risk in continuously quoting firm buy and sell prices when the underlying asset is moving sharply.

- Market maker competition: the more market makers actively quoting a specific fund, the tighter the resulting spread tends to be, since competition among liquidity providers compresses the gap between their buy and sell quotes.

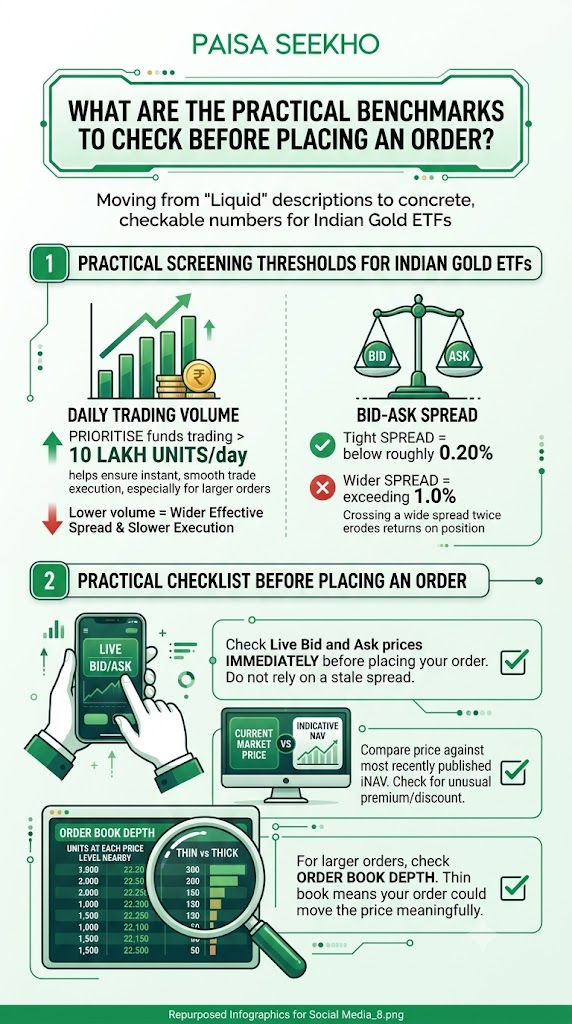

What Are the Practical Benchmarks to Check Before Placing an Order?

Rather than relying purely on qualitative descriptions like “liquid” or “illiquid,” here are concrete, checkable numbers commonly used as practical screening thresholds for Indian Gold ETFs.

- Daily trading volume: prioritise funds trading in excess of roughly 10 lakh units per day to help ensure instant, smooth trade execution, particularly important if you are placing a larger single order. Funds with meaningfully lower daily volume than this can still be traded, but you should expect a wider effective spread and potentially slower execution for sizeable orders.

- Bid-ask spread as a percentage of price: a spread below roughly 0.20% is generally considered reasonably tight and acceptable; a spread exceeding 1.0% is a signal of low liquidity that should give a large order placer real pause, since crossing that spread twice (once on entry, once eventually on exit) could meaningfully erode returns on the position.

Practical checklist before placing an order:

- Check the live bid and ask prices displayed on your trading platform immediately before placing your order, rather than relying on a stale, previously observed spread.

- Compare the current market price against the fund’s most recently published indicative NAV to check whether the ETF is trading at an unusual premium or discount at that moment.

- For a larger order, consider checking the order book depth, not just the top bid and ask, but how many units are available at each price level nearby, since a thin order book means your own order could itself move the price meaningfully as it gets filled.

Does Liquidity Matter Differently for a Lump Sum Investment Versus a SIP?

Yes, genuinely and significantly, and this is one of the most practically useful distinctions to internalise.

- For a lump sum investment, prioritise a high-liquidity ETF even if its expense ratio is marginally higher than a smaller, lower-cost alternative. A single, sizeable order placed in a thinly traded fund risks a meaningfully worse execution price than the same order placed in a deeply liquid fund, and this one-time cost can easily exceed what a small expense ratio difference would have cost you over several years.

- For a Systematic Investment Plan (SIP), particularly one routed through a Gold Mutual Fund (Fund of Funds) rather than a direct ETF purchase, liquidity of the underlying instrument matters considerably less. Since a Gold FoF transacts at the fund’s official NAV rather than at a live, exchange-traded bid-ask price, the retail investor is insulated from the day-to-day spread dynamics that a direct ETF buyer or seller experiences.

- For an investor gradually accumulating a direct Gold ETF position through small, periodic manual purchases rather than through a FoF’s automated SIP mechanism, liquidity still matters, though the impact of a modest spread is proportionally smaller on each individual small transaction than it would be on one large lump sum order.

How Do Major Indian Gold ETFs Actually Compare on Liquidity?

Liquidity rankings shift over time as AUM and trading patterns evolve, but the broad, persistent pattern among Indian Gold ETFs looks like this:

- Nippon India ETF Gold BeES is consistently cited as the most liquid Gold ETF in India by a wide margin, a position it has held since being the country’s original Gold ETF, launched in 2007. Its combination of the largest AUM and the highest daily trading volume in the category gives it the deepest order book and, generally, the tightest effective spreads for large orders.

- ICICI Prudential Gold ETF and SBI Gold ETF also feature prominently among the more liquid options, with substantial AUM and generally strong trading volume, making them reasonable alternatives for investors who want solid liquidity without necessarily defaulting to the single largest fund.

- Newer or smaller entrants, including some lower-expense-ratio funds, can offer genuinely attractive headline costs but may trade with meaningfully lower daily volume, translating into wider effective spreads for larger orders, even though their published expense ratio looks more attractive on paper.

- The practical trade-off in one sentence: a fund like Nippon India ETF Gold BeES may carry a somewhat higher expense ratio than some competitors, but for an active trader or anyone placing a large single order, the tighter effective spread and superior execution quality can offset, or even outweigh, that difference. For a smaller, long-term SIP investor, this liquidity premium matters considerably less, and a lower expense ratio fund may be the more sensible choice.

Is a High-Volume Gold ETF Automatically the Better Choice?

Not necessarily, and it is worth being precise about why. Many investors assume that higher daily trading volume automatically means better liquidity, but this is only partially true. Some ETFs may show reasonable traded volume yet still exhibit broader spreads or less depth at large order sizes, since liquidity also depends on how effectively market makers and Authorised Participants are supporting the fund behind the scenes, not purely on the raw volume figure.

The right framing:

Use trading volume as a useful, easily checkable proxy for likely liquidity, but confirm with the actual live bid-ask spread at the specific moment you intend to trade, particularly for anything beyond a small, routine transaction. For most retail investors making modest, periodic purchases, even a moderately liquid fund is unlikely to impose a materially damaging cost; the liquidity consideration becomes progressively more important as your order size and trading frequency increase.

How Does Liquidity Interact With Tracking Error?

There is a genuine, positive relationship worth understanding here, connecting this article to our companion piece on tracking error. Deep liquidity allows Authorised Participants to arbitrage price differences between the ETF’s market price and its NAV more quickly and efficiently, which helps keep the ETF’s traded price closely aligned with the value of its underlying gold. In practical terms, high trading volume and strong market maker support often correlate with, and can partly explain, lower observed tracking error for a given fund, since the correction mechanism that keeps price aligned with NAV functions more efficiently when there is more active trading and arbitrage activity happening continuously throughout the day.

This does not mean liquidity and tracking error always move in perfect lockstep across every fund, but it is a genuine, mechanically sensible connection: a fund’s liquidity profile and its tracking quality are related aspects of the same underlying market efficiency, not two entirely independent, unconnected metrics.

Frequently Asked Questions

1. What is a “good” bid-ask spread for a Gold ETF in India?

A spread below roughly 0.20% of the unit price is generally considered reasonably tight and acceptable for most retail purposes. A spread exceeding 1.0% signals meaningfully lower liquidity and warrants caution, particularly for larger orders, since crossing that spread on both entry and eventual exit could impose a real, if hidden, cost on your position.

2. Does a lower daily trading volume always mean I will get a bad price?

Not necessarily for a small, routine order. Lower volume does raise the likelihood of a wider spread and, for larger orders, potential price impact as your own order moves through the order book. For modest, periodic retail purchases, even a moderately liquid fund is often perfectly workable; the concern scales up meaningfully with order size and trading frequency.

3. Should I choose the most liquid Gold ETF even if it has a higher expense ratio?

It depends on your investment style. For a large, one-time lump sum investment, prioritising liquidity even at a somewhat higher expense ratio is generally the more sensible trade-off, since a poor execution price on a large order can cost more than several years of a modest expense ratio difference. For a small, long-term SIP, particularly through a Gold Mutual Fund rather than a direct ETF, liquidity of the underlying instrument matters considerably less, and prioritising a lower expense ratio becomes more reasonable.

4. Does liquidity affect Gold Mutual Funds (FoFs) the same way it affects direct Gold ETFs?

No, not directly. A Gold Mutual Fund transacts at its official NAV rather than a live, exchange-traded price, so the retail investor in a FoF is largely insulated from the day-to-day bid-ask spread dynamics that a direct Gold ETF buyer or seller experiences. This is one of the practical trade-offs of the FoF structure: less exposure to secondary market liquidity conditions, in exchange for a typically higher combined expense ratio, as covered in our expense ratio comparison article.

5. Why is Nippon India ETF Gold BeES consistently described as the most liquid Gold ETF in India?

Primarily because it was India’s original Gold ETF, launched in 2007, and has since accumulated by far the largest AUM and the highest sustained daily trading volume in the category. This long track record and scale have made it the default choice for many institutional and active retail traders specifically seeking deep liquidity, even though its expense ratio tends to sit at the higher end of the category.

6. How can I check the current bid-ask spread for a specific Gold ETF before I invest?

Log into your brokerage or trading platform and look at the live order book for the specific fund, which displays the current best bid and ask prices in real time. Comparing this spread, expressed as a percentage of the current price, against the roughly 0.20% “tight” and 1.0% “wide” benchmarks discussed above gives you a practical, immediate read on that fund’s current liquidity condition, which can vary somewhat from day to day depending on overall market activity.

Key Takeaways

- Gold ETF liquidity is a distinct concept from expense ratio and tracking error: it measures how cheaply and quickly you can actually buy or sell units, not the fund’s ongoing cost or its long-run fidelity to gold prices.

- Liquidity comes from two sources: primary market liquidity (Authorised Participants creating/redeeming large blocks directly with the fund) and secondary market liquidity (day-to-day trading on the exchange, which is what most retail investors actually experience).

- The bid-ask spread is the practical cost of trading liquidity; a tighter spread means lower transaction costs. Practical benchmarks: below 0.20% is generally tight and acceptable; above 1.0% signals low liquidity warranting caution.

- Daily trading volume above roughly 10 lakh units is a commonly used practical threshold suggesting reasonably smooth execution for Indian Gold ETFs.

- Liquidity matters far more for lump sum investments than for small, periodic SIP contributions, and matters considerably less if you are investing through a Gold Mutual Fund (FoF) that transacts at NAV rather than a live exchange price.

- Nippon India ETF Gold BeES consistently ranks as the most liquid Gold ETF in India, owing to its status as the original fund and its resulting scale, though this liquidity premium often comes with a somewhat higher expense ratio than some competitors.

- Trading volume is a useful proxy but not a perfect guarantee of liquidity; always check the live bid-ask spread at the actual moment of your intended trade, particularly for any order beyond a small, routine size.

- Liquidity and tracking error are mechanically connected: deeper liquidity supports more efficient arbitrage by Authorised Participants, which in turn tends to support tighter tracking of the fund’s price to its underlying gold value.

Sources: m.Stock: ETF Liquidity, Bid-Ask Spreads and Trading Volume Guide, June 2025; TMGM: Top 5 Best Gold ETF in India for 2026, May 2026; Lakshmishree: Best Gold ETFs in India 2026, Returns, Expense Ratio and Top Picks, May 2026; Morningstar: How to Choose the Right Gold ETF, February 2026; Finology: Best Gold ETF in India 2026, Top Funds, Returns and Tax Guide, April 2026.

This article is for general financial education only and does not constitute investment advice. Bid-ask spreads and trading volumes fluctuate and should be checked live before trading. Past performance does not guarantee future returns. Consult a SEBI-registered investment advisor for personalised guidance.