Quick summary: A Gold ETF is a way to own gold digitally, without buying jewellery or coins. You can invest in it in two ways. SIP means you put in a small, fixed amount every month. Lump sum means you put in one big amount at once. Neither one is always better. It depends on your situation. This guide explains both in simple words, with real examples, so you can pick the right one for you.

What Is SIP and What Is Lump Sum?

SIP stands for Systematic Investment Plan. You choose a fixed amount, say ₹2,000, and it gets invested every month automatically. You do not need to check gold prices or time your purchase. It just happens, month after month, like an EMI.

Lump sum means you invest a large amount all at once. For example, you get a bonus of ₹1,00,000 and you put the whole thing into a Gold ETF on the same day.

Both methods buy the same thing, units of a Gold ETF, which each represent a small amount of real, pure gold held safely by the fund. The only difference is how and when you put your money in.

What Is Rupee Cost Averaging, in Simple Words?

This is the main reason people choose SIP, so let us explain it clearly with a simple example.

Say you invest ₹5,000 every month in a Gold ETF.

- In Month 1, the price is ₹100 per unit. You get 50 units.

- In Month 2, the price falls to ₹80 per unit. You get 62.5 units.

- In Month 3, the price rises to ₹120 per unit. You get 41.6 units.

Notice what happened. When the price was low, your fixed ₹5,000 bought more units. When the price was high, it bought fewer units. Over time, your average cost per unit becomes lower than if you had just bought at one random price.

This is called rupee cost averaging. It does not guarantee profit. But it protects you from putting all your money in on a single bad day, when prices happen to be at their highest.

When Does Lump Sum Work Better?

Lump sum works best when gold prices are steadily going up, or when you believe prices are currently reasonable and about to rise.

Here is why. If you invest ₹1,00,000 as lump sum, your entire amount starts growing from day one. With SIP, only a small part of your money is invested each month, so the rest is sitting idle, waiting its turn, while the market may already be rising.

A simple example: Gold rises steadily for 12 months, from ₹100 to ₹150 per unit, a 50% rise.

- If you had invested ₹1,20,000 as a lump sum on day one, your money grows the full 50%, to ₹1,80,000.

- If you had invested ₹10,000 every month instead, only your first month’s ₹10,000 got the full 50% rise. Your later months got smaller and smaller gains, since prices were already higher by the time you invested. Your total gain would be noticeably less than the lump sum investor’s.

So the simple rule is: in a market that is steadily rising, lump sum usually wins. In a market that is falling or moving up and down, SIP usually wins, because it buys more units when prices dip.

Is There a Rule for Which One to Pick?

Yes, a simple one. Think about it this way:

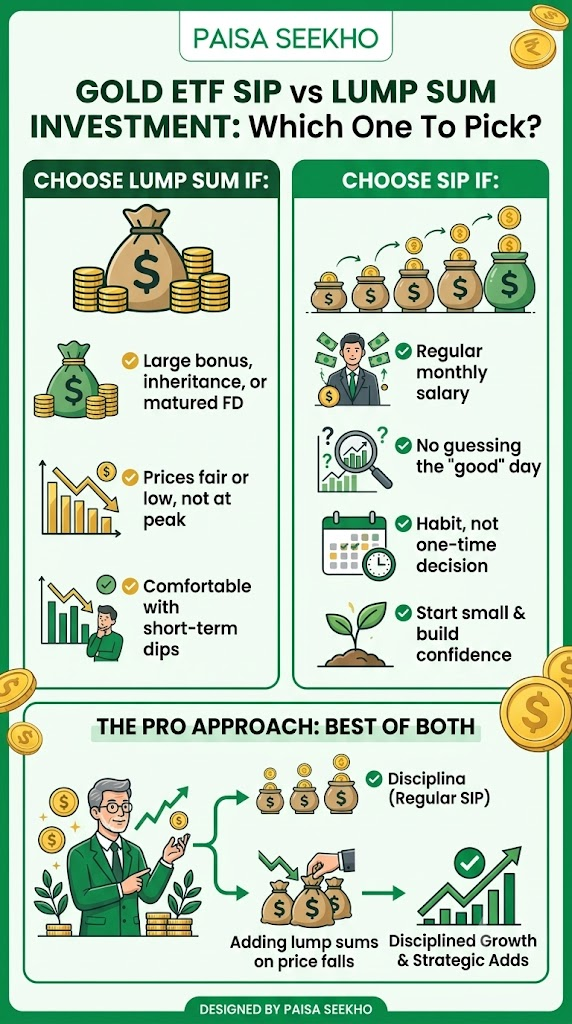

Choose lump sum if:

- You have a large amount of money sitting idle right now, a bonus, an inheritance, savings from an FD that matured

- You believe gold prices are currently fair or low, not at a peak

- You are comfortable seeing the value go down for a while if the market dips right after you invest

Choose SIP if:

- You get a regular monthly salary and want to invest a small part of it every month

- You do not want to guess whether today is a “good” day to buy gold

- You want a habit, not a one-time decision

- You are a first-time investor and want to start small and build confidence

Many experienced investors do not pick just one. They keep a small SIP running every month for discipline, and they add a lump sum whenever gold prices fall sharply or they have extra money to invest. This gives them the best of both approaches.

What Is the Minimum Amount Needed for Each?

- For a Gold ETF SIP: many platforms allow you to start with as little as ₹500 to ₹1,000 per month. Some Gold ETFs allow even smaller amounts, like ₹100, depending on the fund and the unit price on that day.

- For a Gold ETF lump sum: you can invest any amount as long as it covers at least one unit of the ETF at its current price, which is usually somewhere between ₹100 and ₹135 per unit as of 2026. So a lump sum of even ₹5,000 to ₹10,000 can buy several units in one go.

Note: to invest directly in a Gold ETF, you need a demat account, the same account used to buy shares. If you do not have one, you can invest through a Gold Mutual Fund instead, which invests in a Gold ETF on your behalf and does not need a demat account. This is a common and simple way to start a Gold SIP without any extra paperwork.

Does the Tax Rule Change Based on SIP or Lump Sum?

Yes, and this is an important, often-missed detail.

For a Gold ETF, if you hold your units for more than 12 months, your profit is taxed at a flat 12.5%. If you sell before 12 months, your profit is added to your income and taxed at your regular income tax slab rate, which can be much higher, up to 30% for some people.

With lump sum, this is simple. You have one purchase date. After 12 months from that one date, your entire investment qualifies for the lower 12.5% tax rate.

With SIP, it is more complicated. Each month’s SIP instalment has its own separate purchase date. So if you started a SIP in January 2025 and want to sell everything in March 2026:

- The January 2025 instalment has crossed 12 months, so it gets the lower 12.5% tax rate

- The instalments from the last few months, say, January to March 2026, have not crossed 12 months yet, so they get taxed at your regular income slab rate instead

This means a single sale of your SIP investment can be taxed at two different rates at the same time, part of it at 12.5%, and part of it at your slab rate. This is completely normal and not a mistake. It is simply how the tax rule works for SIP investments.

Practical tip: if you plan to sell your Gold ETF SIP investment, try to sell the oldest instalments first, the ones that have already crossed 12 months, and hold off selling your most recent instalments until they also cross the 12-month mark. This way, more of your profit gets taxed at the lower rate.

What Does This Look Like With Real Numbers?

Let us use a simple, round example to make this clear.

Priya’s SIP: Priya invests ₹5,000 every month in a Gold ETF, starting April 2025. By March 2026, she has made 12 monthly investments, totalling ₹60,000.

Rahul’s lump sum: Rahul invests the full ₹60,000 in one go, in April 2025.

If gold prices rise steadily through the year, Rahul’s lump sum captures the full rise on his entire ₹60,000 from day one. Priya’s SIP only slowly builds up, so her average purchase price ends up a bit higher than Rahul’s day-one price, meaning her total gain, in rupee terms, may be somewhat lower.

But if gold prices are choppy, going up and down through the year, Priya’s SIP could end up with a lower average cost per unit than Rahul’s single lump sum price, simply because she bought some units when prices happened to be low.

Neither Priya nor Rahul made a mistake. They simply picked different strategies, and each strategy performs differently depending on what the market actually does, which nobody can know in advance.

What Should a Beginner Do?

If you are new to investing and unsure which to choose, here is simple, practical guidance.

- Start with a SIP. It teaches you how the market moves, without the pressure of committing a large sum all at once. Even a small ₹1,000 to ₹2,000 monthly SIP is enough to build the habit and understand how gold prices behave over several months.

- If you already have a large amount sitting idle, an old FD that matured, a bonus you have not used, and you already understand that gold prices can go up and down, you can consider putting a portion of it as a lump sum, while continuing your regular SIP separately.

- Do not put your emergency fund into a Gold ETF as a lump sum. Gold prices can fall in the short term. Your emergency fund needs to be available at full value whenever you need it, not exposed to market ups and downs.

For more on how much gold you should hold overall and how this fits your age, see our gold allocation by age guide.

Common Questions People Get Wrong

“SIP always gives better returns than lump sum.”

This is not true. In a year when gold prices rise steadily without much fall, lump sum usually wins, since your full amount grows from day one. SIP wins mainly in years when prices fall or move up and down a lot.

“I should wait for gold prices to fall before starting my SIP.”

This defeats the whole purpose of SIP. The idea of SIP is that you do not need to guess the right time. You invest regularly, in good months and bad months, and let the averaging work over time.

“My SIP and lump sum will be taxed the same way.”

As explained above, this is not correct. Lump sum has one purchase date. SIP has many purchase dates, one for each instalment, and each one is tracked separately for tax purposes.

Frequently Asked Questions

1. Which gives higher returns, SIP or lump sum, in Gold ETF?

It depends entirely on how gold prices move during your investment period. If prices rise steadily without big dips, lump sum usually gives higher returns, since your full amount grows from the very first day. If prices are volatile or falling for a while, SIP usually does better, because it buys more units when prices are low.

2. Can I do both SIP and lump sum at the same time?

Yes. Many investors run a small, regular SIP every month for discipline, and also add a lump sum whenever they have extra money or when gold prices drop noticeably. There is no rule against doing both together in the same Gold ETF.

3. Do I need a demat account for a Gold ETF SIP?

Yes, for a direct Gold ETF. If you do not have a demat account, you can instead invest in a Gold Mutual Fund, also called a Fund of Funds, which invests in a Gold ETF for you and does not require a demat account. This is simpler for many beginners.

4. What is the minimum amount I can start with?

For a SIP, many platforms allow as little as ₹500 to ₹1,000 per month, and some funds allow even less. For a lump sum, any amount that can buy at least one unit works, and one unit typically costs somewhere between ₹100 and ₹135 as of 2026.

5. Why did my Gold ETF SIP get taxed at two different rates when I sold it?

Because each monthly instalment has its own purchase date. Instalments older than 12 months are taxed at the lower flat 12.5% rate. Instalments younger than 12 months are taxed at your regular income slab rate instead. Both rates can apply to the same sale, and this is completely normal.

6. Should I stop my SIP if gold prices fall sharply?

No, generally you should not. A sharp fall means your fixed monthly amount is now buying more units at a cheaper price, which is exactly what makes rupee cost averaging work in your favour over time. Stopping a SIP during a dip usually works against you, not for you.

Key Takeaways

- SIP means investing a small, fixed amount every month. Lump sum means investing a large amount all at once. Both buy the same Gold ETF units.

- Rupee cost averaging is the main benefit of SIP: your fixed monthly amount buys more units when prices are low and fewer units when prices are high, smoothing out your average cost over time.

- Lump sum usually wins when gold prices rise steadily. SIP usually wins when prices fall or move up and down a lot.

- Tax works differently for each. Lump sum has one purchase date, so the whole investment crosses the 12-month mark together. SIP has a separate purchase date for every monthly instalment, so parts of your investment can be taxed at 12.5% while other, more recent parts are taxed at your regular income slab rate.

- Beginners should generally start with SIP to build confidence and habit. A lump sum makes more sense once you have idle funds and are comfortable with gold’s short-term ups and downs.

- Many investors combine both: a steady monthly SIP for discipline, plus occasional lump sum additions when they have spare money or gold prices fall.

- Never put your emergency fund into a Gold ETF as a lump sum. Keep that money safe and easily available, not exposed to market swings.

Sources: Goodwill India: SIP vs Lump Sum Investment in Gold and Silver ETFs, January 2026; India Tax Tools: SIP vs Lump Sum Investment in 2026, Which Gives Better Returns?, February 2026; Lakshmishree: Best Gold ETFs in India 2026, February 2026; FinPlann: Best Gold ETFs 2026, Top Picks with Lowest Expense Ratios, April 2026.

This article is for general information only and does not give investment advice. Gold prices can go up or down, and past performance does not predict future results. Talk to a SEBI-registered investment advisor before making a decision.