Quick summary: If you set a target gold allocation a few years ago (say, 10% of your investment portfolio) and have not touched it since, there is a good chance gold’s extraordinary 2025-2026 rally has pushed that allocation well above what you originally intended, perhaps to 15% or even 20% of your total portfolio. This is exactly the situation rebalancing exists to fix. Rebalancing is not about predicting where gold goes next. It is a mechanical discipline that forces you to trim what has run up and top up what has lagged, keeping your risk aligned with your original plan rather than with whatever the market has recently done. This guide explains the three main rebalancing methods, why gold specifically needs a different threshold than your equity-debt split, the tax-efficient way to execute it in India, and a worked example you can adapt to your own numbers.

What Does Rebalancing Actually Mean, and Why Does Gold Need Its Own Rule?

When you first decided on a target allocation, say, 60% equity, 30% debt, and 10% gold, you were not choosing those numbers arbitrarily. You were expressing a specific risk tolerance and a specific role for each asset in your portfolio. Left alone, markets do not respect that plan. If gold rallies 40% in a year while equity is roughly flat, your 10% gold sleeve can silently balloon to 14% or 15% of your total portfolio, and your risk profile has changed without you making any deliberate decision about it.

Rebalancing is the practice of periodically nudging your portfolio back to its target weights: selling a portion of whatever has run up and reinvesting in whatever has lagged, or directing new contributions preferentially toward the underweighted sleeve. Large managers and research houses frame rebalancing exactly this way: a discipline to control tracking error and behaviour, not a way to time markets. The goal is not to maximise returns; it is to keep the risk you are actually carrying aligned with the risk you originally signed up for.

Why gold specifically needs a different rule than your equity-debt split:

Gold is typically a much smaller sleeve of a portfolio (5% to 15%, as covered in our earlier gold allocation by age guide) than equity or debt, and its price moves are often sharper and more episodic than the rest of a balanced portfolio. A rule designed for a 60/40 equity-debt split, where you act only after a full 5 percentage-point absolute drift, does not translate well to a 10% gold sleeve, since a 5 percentage-point move on a 10% starting position is a 50% relative swing, an enormous change that would trigger action far too late if you waited for an absolute band sized for your larger sleeves.

What Are the Three Main Rebalancing Methods?

There are three broad approaches, and most disciplined investors end up using a version of the third.

Calendar-based rebalancing

You pick a fixed review date, monthly, quarterly, half-yearly, or annual, and reset your portfolio back to target on that schedule regardless of how much drift has actually occurred. This is the easiest method to communicate and the simplest to execute alongside routine, salary-day contributions. Indian personal finance research commonly suggests a half-yearly or annual cadence for most investors, with more frequent checks reserved only for those running genuinely active strategies.

The drawback: you might rebalance when drift is negligible, wasting transaction costs and creating an unnecessary taxable event for a change that provided no meaningful risk reduction, or you might fail to act during a sharp mid-year move because your fixed date has not yet arrived.

Threshold-based rebalancing

Instead of acting on a fixed date, you act only when an asset’s weight drifts beyond a tolerance band you have set in advance. Two common formulations exist:

- An absolute band on large sleeves, such as plus or minus 5 percentage points on a 60% equity target (acting at 65% or 55%)

- The 5/25 rule for smaller sleeves, which is specifically designed for positions like a 10% gold allocation: you act when the sleeve moves by at least 5 percentage points in absolute terms, or by 25% in relative terms, whichever condition your specific rule specifies. On a 10% gold target, this means acting if gold falls below 7.5% (25% below target) or rises above 12.5% (25% above target).

This method delivers stronger risk control than a fixed calendar check and avoids unnecessary trades during calm periods, but it requires ongoing monitoring, since without a review date built in, an investor can simply forget to check during long stretches of quiet markets.

Hybrid rebalancing (calendar plus threshold)

This combines both approaches: you review your portfolio on a set timeline (say, twice a year), but you only actually execute trades if a sleeve has breached its predefined threshold during that review. This is the practical sweet spot most financial planners recommend. In practice, the hybrid method typically results in only one or two rebalancing events per year during normal markets, and three or four during genuinely volatile years, far fewer transactions than constant monitoring would trigger, with virtually identical risk outcomes to more frequent checking.

The practical recommendation for a gold sleeve specifically:

Put two review dates on your calendar (a common and sensible choice is January and July), and at each review, apply the 5/25 rule specifically to your gold allocation. Rebalance with new contributions first wherever possible; sell existing holdings only if the position remains out of band after directing fresh money.

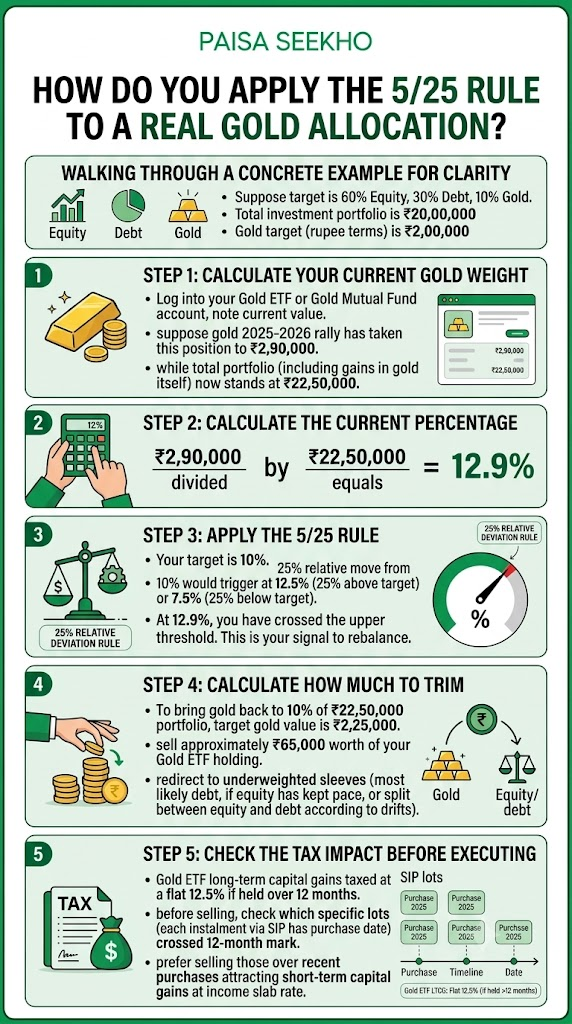

How Do You Apply the 5/25 Rule to a Real Gold Allocation?

Let us walk through this with concrete numbers, since the abstract rule becomes much clearer with an example.

Suppose your target allocation is 60% equity, 30% debt, and 10% gold, on a total investment portfolio of ₹20,00,000. Your gold target in rupee terms is therefore ₹2,00,000.

Step 1: Calculate your current gold weight.

Log into your Gold ETF or Gold Mutual Fund account and note the current value. Suppose gold’s 2025-2026 rally has taken this position to ₹2,90,000, while your total portfolio (including the gains in gold itself) now stands at ₹22,50,000.

Step 2: Calculate the current percentage.

₹2,90,000 divided by ₹22,50,000 equals approximately 12.9%.

Step 3: Apply the 5/25 rule.

Your target is 10%. A 25% relative move from 10% would trigger at 12.5% (25% above target) or 7.5% (25% below target). At 12.9%, you have crossed the upper threshold. This is your signal to rebalance.

Step 4: Calculate how much to trim.

To bring gold back to 10% of your ₹22,50,000 portfolio, your target gold value is ₹2,25,000. You would sell approximately ₹65,000 worth of your Gold ETF holding, and redirect that amount into your underweighted sleeves (in this case, most likely debt, if equity has kept pace with the overall portfolio growth, or split between equity and debt according to how each sleeve has drifted).

Step 5: Check the tax impact before executing.

As covered in our earlier articles in this series, Gold ETF long-term capital gains are taxed at a flat 12.5% if held over 12 months. Before selling, check which specific lots (if you have invested via SIP, each instalment has its own purchase date) have crossed the 12-month mark, and prefer selling those over more recently purchased units that would attract short-term capital gains at your income slab rate instead.

This same mechanical process, applied twice a year, is what prevents a genuinely good year for gold from silently turning into an accidentally oversized, risk-concentrated position.

How Should You Actually Execute the Trade in India, Tax-Efficiently?

Executing a rebalancing trade thoughtfully can meaningfully reduce both transaction costs and your tax bill.

Prefer contributions over sales wherever possible.

If you are still actively investing (through salary savings, a bonus, or maturing FDs), the most tax-efficient way to rebalance a sleeve that has fallen behind is to direct new money toward it, rather than selling an overweight sleeve to fund the underweight one. This avoids triggering any capital gains tax at all on the overweight position. Rebalancing with contributions first, and selling only if the position remains out of band afterward, is the standard best-practice sequence.

When you must sell, check your holding period carefully.

For Gold ETFs, the flat 12.5% LTCG rate applies only after 12 months of holding. If you have several tranches purchased at different times (common with SIP investors), selling your oldest, longest-held units first, assuming they qualify for LTCG treatment, keeps more of your gain taxed at the favourable flat rate rather than at your income slab rate.

Consider minimal-gain lots if you have a choice.

If your Gold ETF holdings were purchased across multiple transactions at different prices, selling the lots with the smallest embedded gain (rather than the largest) reduces the absolute tax you pay for the same rupee amount of rebalancing.

Do not let the tax tail wag the rebalancing dog entirely, but do not ignore it either.

A modest tax cost to correct a genuinely oversized risk concentration is usually still worth paying. The goal is to be deliberate about which specific units you sell, not to avoid rebalancing altogether because of the tax consequence.

For more on how Gold ETF taxation works in detail, including the 2024 change from indexation-based rates to the current flat 12.5% structure, see our gold vs fixed deposits guide, which covers this in depth.

Should You Rebalance Gold Differently When Prices Have Fallen, Not Risen?

Yes, and this is a psychologically harder version of the same discipline. Rebalancing is symmetric by design: it forces you to trim what has run up and add to what has lagged, and gold’s high volatility makes it a natural rebalancing contributor in both directions. A sharp gold rally that pushes your allocation from 10% to 14% is exactly when rebalancing captures profit by trimming back to target. A sharp drop that takes your allocation from 10% to 7% is exactly when the same rule tells you to add to gold at lower prices.

The trades that matter most for gold are often the psychologically hardest to execute. Selling gold after a strong rally, when the case for holding more of it feels strongest and headlines are most enthusiastic about further gains, is precisely the moment the rule says to trim back to target. Conversely, buying more gold after a sharp fall, when sentiment feels weakest, is precisely the moment the rule says to add. This is the entire value of having a mechanical rule in the first place: it removes the emotional decision at the exact moments emotion is most likely to lead you astray.

Does Your Time Horizon Change How You Should Rebalance Gold?

Yes, meaningfully. Gold’s role changes with your time horizon, and the same allocation can be sensible or reckless depending on how long you intend to hold it and how close you are to needing the money.

If you are decades from needing this money (your 20s to 40s):

A hybrid approach with a wider band (the 5/25 rule) and a semi-annual or annual review is appropriate. You have time to ride out gold’s episodic swings, and infrequent, disciplined rebalancing captures most of the benefit without excessive trading.

If you are within 5 to 7 years of a specific goal, or approaching retirement:

Tighter monitoring becomes more valuable, since sequence-of-returns risk (a market shock shortly before you need the funds) is a much bigger concern at this stage, as covered in our gold allocation by age guide. Consider a somewhat narrower band or a quarterly review specifically as you approach the point where you will start drawing down the portfolio.

If you have already begun drawing down your portfolio in retirement:

Rebalancing continues to matter, since maintaining your intended gold allocation still provides the same crisis-protection benefit covered in our gold during recession guide, but execution should prioritise using natural cash flows (interest, dividends, or planned withdrawals) over discretionary buying and selling wherever feasible, to minimise both transaction costs and tax events during a phase when you are also managing income needs.

What Are the Most Common Mistakes When Rebalancing Gold?

Rebalancing too frequently.

Checking and adjusting monthly, or even reacting to every short-term news headline about gold prices, generates unnecessary transaction costs and taxable events without any meaningful improvement in risk management. Research consistently shows that more frequent rebalancing beyond a certain point adds cost without adding benefit.

Never rebalancing at all.

The opposite failure is equally common and arguably more damaging: setting a target once and never revisiting it. A 10% gold target that silently becomes 20% because of a strong multi-year rally is a materially different, more concentrated portfolio than the one you originally designed, whether or not you consciously chose that outcome.

Reacting to short-term news instead of your rule.

Rebalancing is a long-term discipline designed specifically to resist emotional impulses, not to be triggered by them. Deciding to add to gold because of a dramatic headline about a geopolitical crisis, rather than because your threshold rule has actually been breached, defeats the purpose of having a mechanical system in the first place.

Ignoring the tax consequence of the rebalancing trade itself.

As covered above, selling without checking holding periods or lot-specific gains can needlessly convert what should be a 12.5% LTCG event into a slab-rate STCG event.

Applying the same band to gold as to your larger equity-debt sleeves.

As explained earlier, a 5 percentage-point absolute band designed for a 60% equity position is far too wide for a 10% gold position; the 5/25 relative rule is the more appropriate framework specifically for smaller sleeves like gold.

Frequently Asked Questions

1. How often should I rebalance my gold allocation?

For most individual investors, a hybrid approach works best: review your portfolio twice a year (a common choice is January and July), and only execute a trade if your gold allocation has actually breached your threshold (commonly the 5/25 rule) during that review. This typically results in just one or two actual rebalancing trades per year in normal market conditions.

2. My gold allocation grew from 10% to 13% after the 2025 rally. Should I sell?

Under the 5/25 rule, a move from a 10% target to 12.5% (a 25% relative increase) is the trigger point. At 13%, you have crossed this threshold, so yes, this is a reasonable point to trim your gold position back toward your 10% target and redirect the proceeds to your underweighted sleeves.

3. Is it better to rebalance by selling gold or by directing new contributions elsewhere?

Directing new contributions toward your underweighted sleeves, rather than selling your overweight gold position, is generally more tax-efficient, since it avoids triggering any capital gains tax at all. Use this approach whenever you have fresh money to invest; sell existing gold holdings only when contributions alone are insufficient to bring your allocation back within its target band.

4. Does rebalancing gold trigger tax even if I am just moving money within my own portfolio?

Yes. Selling Gold ETF units to rebalance is treated as a taxable sale for capital gains purposes, just like selling any other listed security, regardless of whether you plan to reinvest the proceeds elsewhere in your own portfolio. Gains are taxed at 12.5% if the units were held over 12 months, or at your income slab rate if held for less time.

5. Should I use the same rebalancing threshold for gold as I do for my equity and debt allocation?

No. Since gold is typically a much smaller sleeve than equity or debt, an absolute percentage-point band sized for your larger sleeves (such as plus or minus 5 percentage points on a 60% equity target) is generally too wide to be meaningful for a 10% gold position. The 5/25 relative rule, which triggers at a 25% relative move rather than a fixed absolute move, is better suited to smaller allocations like gold.

6. What if I do not have enough new contributions to rebalance without selling?

If your gold position has drifted meaningfully beyond your threshold and you do not have sufficient fresh contributions to correct it, selling the appropriate amount of gold and reinvesting in your underweighted sleeves is the correct action, even with the associated tax cost. A modest tax payment to correct a genuinely oversized risk concentration is usually a reasonable trade-off against the risk of an unintentionally concentrated portfolio.

Key Takeaways

- Rebalancing is a risk-management discipline, not a market-timing tool. It forces you to sell a little of what has appreciated and add to what has lagged, keeping your portfolio’s actual risk aligned with your original plan.

- Three main methods exist: calendar-based (fixed review dates), threshold-based (act only when drift exceeds a preset band), and hybrid (a scheduled review combined with a threshold trigger), with the hybrid approach being the practical recommendation for most investors.

- Gold needs its own threshold, distinct from your equity-debt split. The 5/25 rule (act when a sleeve moves 5 percentage points in absolute terms or 25% in relative terms, whichever is specified) is well suited to a typical 5% to 15% gold allocation.

- A practical cadence: review your full portfolio twice a year (for example, January and July), and apply the 5/25 rule specifically to your gold sleeve at each review.

- Rebalance with new contributions first wherever possible to avoid triggering capital gains tax; sell existing holdings only if the position remains out of band afterward.

- Check holding periods before selling Gold ETF units. The flat 12.5% LTCG rate applies only after 12 months; selling older, qualifying lots first (and minimal-gain lots where you have a choice) reduces your tax bill for the same rebalancing outcome.

- Rebalancing is symmetric: it should prompt you to trim gold after a strong rally just as readily as it prompts you to add to gold after a sharp fall, and both directions are equally valuable even though the second is often psychologically harder to execute.

Sources: Finnovate: Portfolio Rebalancing in India, Calendar vs Threshold Rules; Tata Mutual Fund: Rebalancing Your 2026 Portfolio, The 10% Gold Rule; OnlineGold.org: How Much Gold Should You Own? Portfolio Allocation Guide 2026, April 2026; The Arca Labs: Portfolio Rebalancing 2026, Strategy Guide, April 2026.

This article is for general financial education only and does not constitute investment advice. Past performance does not guarantee future returns. Consult a SEBI-registered investment advisor before making portfolio decisions, and a tax professional before executing any rebalancing trade with material capital gains implications.