Quick summary: A Gold ETF is designed to mirror the price of physical gold as closely as possible, but “as closely as possible” is doing real work in that sentence. Gold ETFs achieve this tracking through a structured mechanism: the fund holds actual physical gold (99.5% purity, as mandated by SEBI), and a set of large institutional players called Authorized Participants keep the ETF’s traded price aligned with the value of that underlying gold. The gap between what the ETF actually returns and what gold itself returns is called tracking error, and it is driven by a handful of specific, identifiable factors: expense ratios, cash held for redemptions, and execution timing. In 2026, India also made a genuinely significant change to how this tracking works at a structural level, shifting the entire industry’s valuation benchmark from international London prices to domestic spot prices. This guide explains the full mechanism, the tracking error breakdown, and what that 2026 shift means for you as an investor.

What Does It Actually Mean for an ETF to “Track” Gold?

A Gold ETF is a passively managed fund that invests predominantly in physical gold, endeavouring to track the spot price of gold in the domestic market, subject to tracking error. Each unit of the ETF typically represents a small fraction of a gram of gold (commonly around 1 gram per unit, though this varies by fund), and the fund’s Net Asset Value (NAV) is calculated based on the market value of the actual gold it holds in custody.

When you buy a Gold ETF unit, you are not buying a promise or a derivative contract disconnected from real gold. Under SEBI’s regulations for Gold ETFs, funds must value their underlying gold based on 0.995 fineness (99.5% purity), and the gold itself is held with regulated custodians, subject to regular audits and transparent holdings reporting, often on a monthly basis.

Because Gold ETFs trade on stock exchanges like the NSE and BSE, their market price can, at least in principle, diverge slightly from their NAV at any given moment, exactly the way any exchange-traded security’s market price can briefly diverge from its fundamental value. The mechanism described below is what keeps that divergence small and temporary rather than large and persistent.

How Does the Creation and Redemption Mechanism Actually Work?

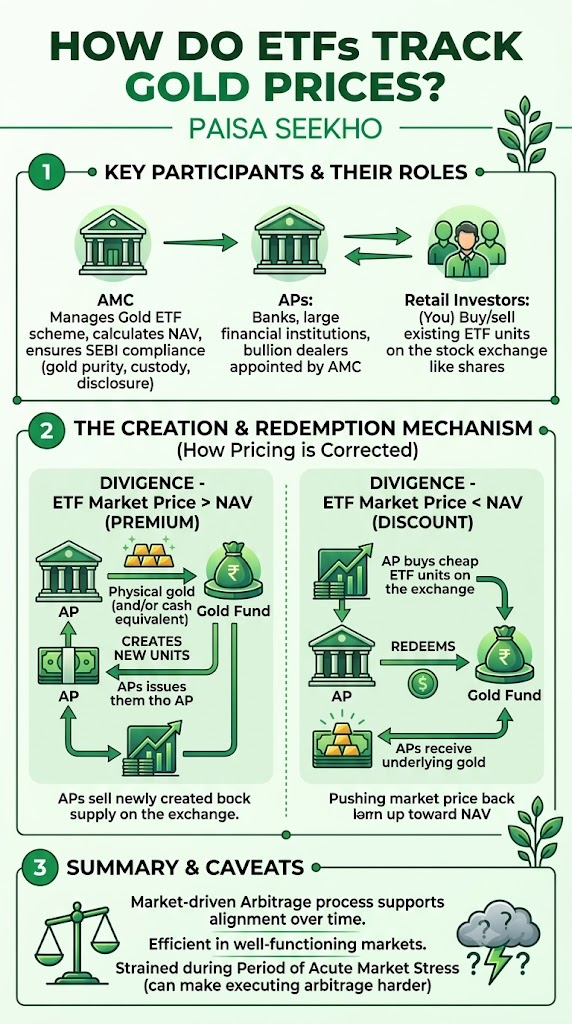

This is the structural core of how a Gold ETF stays aligned with gold prices, and it involves three distinct participants working together.

- The Asset Management Company (AMC) manages the Gold ETF scheme, calculates the daily NAV, and ensures regulatory compliance with SEBI’s requirements on gold purity, custody, and disclosure.

- Authorized Participants (APs) are typically large financial institutions, banks, or bullion dealers specifically appointed by the AMC. They are permitted to create or redeem ETF units directly with the fund, but only in large blocks called Creation Units (for example, a block might represent 100,000 or more ETF units at a time), not in the small, single-unit quantities that retail investors buy and sell.

- Retail investors (you) generally do not deal with the AMC directly at all. Instead, you buy and sell existing ETF units on the stock exchange, the same way you would buy or sell a company’s shares, at whatever price the market is currently offering.

Here is how the mechanism corrects price divergence: if the ETF’s market price on the exchange rises above its NAV (a premium, meaning the ETF is trading richer than the actual gold it represents), Authorized Participants have a profit incentive to create new units. They deliver gold (or, in some structures, cash equivalent to gold’s value) to the fund in exchange for new ETF units, which they can then sell on the open market at the elevated price, pocketing the difference. This selling pressure from the newly created supply pushes the ETF’s market price back down toward NAV.

Conversely, if the ETF trades at a discount (below NAV), Authorized Participants can buy up cheap ETF units on the exchange and redeem them directly with the fund in exchange for the underlying gold (or its cash equivalent) at the higher NAV value, again profiting from the gap. This buying pressure pushes the market price back up toward NAV.

This market-driven arbitrage process is what supports alignment between the ETF’s traded price and its NAV over time. It works efficiently in liquid, well-functioning markets, though it can be strained during periods of acute market stress, when even Authorized Participants may find it harder to execute the arbitrage smoothly.

What Is Tracking Error, and What Actually Causes It?

Tracking error refers to the difference between the return of a Gold ETF and the price movement of the gold it is designed to track. No Gold ETF, however well run, tracks its benchmark perfectly, and understanding exactly why is essential to interpreting any given fund’s performance correctly.

Expense ratio impact.

The annual management fee charged by the fund (typically ranging from roughly 0.1% to 0.5% for Indian Gold ETFs) is deducted directly from the fund’s NAV. This is the single most predictable and mechanical component of tracking error: if gold delivers a 12% return in a year but your ETF’s expense ratio is 0.5%, you should expect your ETF to deliver something close to 11.5%, purely from this fee drag, before any other factor comes into play.

Cash held for redemptions.

Gold ETFs typically keep a small portion, often 1% to 5% of their portfolio, in cash to manage day-to-day redemption requests and operational needs, rather than holding 100% of assets in physical gold at all times. Since this cash component does not move with gold prices, it creates a modest drag on returns specifically during periods when gold prices are rising (the cash portion simply misses out on the gold rally), and can work in the opposite, small favourable direction during periods when gold prices are falling.

Timing differences in gold purchases.

Fund managers may not always buy or sell physical gold at the exact same price or the exact same moment as the benchmark index they are tracking. These execution delays, however small individually, create incremental variations in performance that accumulate over time.

Currency movements (specific to Indian Gold ETFs).

Since international gold is priced in US dollars, Indian Gold ETF prices are affected by USD-INR currency movements, in addition to the underlying dollar price of gold itself. A change in the exchange rate can shift domestic gold prices even when international gold prices remain completely stable, and how precisely a fund’s valuation methodology captures this currency effect can itself be a source of tracking variation between funds.

A useful sanity check when evaluating any specific fund:

An ETF outperforming physical gold by a wide margin should be treated with just as much scrutiny as one underperforming it by a wide margin, since either outcome can indicate a breakdown in the fund’s replication strategy rather than genuinely superior management. The goal of a Gold ETF is close, faithful tracking, not outperformance.

What Changed in 2026: SEBI’s Shift to Domestic Spot Price Valuation

This is a genuinely significant structural development that materially affects how tracking error works for every Gold ETF in India going forward, and it is worth understanding in some detail.

Historically, Indian Gold ETFs were valued based on LBMA (London Bullion Market Association) fixing prices, the international benchmark for gold. This required fund houses to perform complex manual adjustments to translate that international benchmark into a domestically relevant NAV, accounting for USD-to-INR currency conversions, customs duties, Goods and Services Tax, and “notional” local premiums that varied inconsistently from one fund house to another. This patchwork of manual adjustments was itself a meaningful source of tracking error and inconsistency across different funds.

Following a comprehensive SEBI circular issued on 26 February 2026, which outlined the specific inadequacies of this previous international benchmark system, SEBI moved the entire industry toward anchoring Net Asset Values to domestic market realities directly, including domestic import duties, taxes, and regional supply-demand dynamics, rather than reconstructing a domestic price from a London benchmark plus manual adjustments. This regulatory pivot is designed specifically to eliminate the long-standing pricing gap that had affected Indian bullion investors, providing a more transparent and efficient pricing mechanism that more accurately reflects the actual replacement cost of gold within Indian borders.

What this means practically for you as an investor:

With valuation anchored to domestic spot prices rather than reconstructed from an international benchmark, the tracking error component that previously came from inconsistent manual adjustment methodologies across different fund houses should narrow. Major fund houses managing large gold and silver AUM are expected to see meaningful operational efficiencies from this change, and investors evaluating tracking error data from before versus after this transition should keep the regulatory shift in mind, since older tracking error figures reflect the previous LBMA-based methodology and may not be directly comparable to figures reported after the transition.

How Do You Actually Compare Tracking Error Across Different Funds?

If you are choosing between several Gold ETFs, tracking error (alongside expense ratio and liquidity) is one of the most useful comparison metrics, and here is how to read it correctly.

Look at tracking error over multiple time periods, not just one snapshot.

Comparing funds over 1-year, 3-year, and 5-year windows, where available, gives you a sense of consistency rather than a single point-in-time figure that could be distorted by a temporary anomaly.

Lower tracking error generally indicates closer alignment with actual gold price movements

However, the exact number that counts as “low” varies with fund structure and costs, so compare funds against each other rather than against an absolute universal benchmark.

Pay attention to the standard deviation of tracking error, not just the average.

A fund with a lower average tracking error but a higher standard deviation is, in effect, more “nervous,” meaning it deviates from gold prices more erratically, even if the average deviation looks similar to a steadier fund. A lower standard deviation usually signals steadier, more predictable tracking with less noise, generally reflecting fewer frictions from cash drag or creation-redemption timing issues.

High trading volume tends to correlate with lower effective tracking error.

ETFs with deep liquidity allow Authorized Participants to arbitrage price differences between market price and NAV faster and more efficiently, which helps keep the ETF’s traded price closely aligned with its underlying gold value. If you need to buy or sell quickly, low-volume ETFs can also expose you to wider bid-ask spreads, an additional real-world cost that sits alongside the expense ratio and is sometimes overlooked when comparing “official” tracking error figures across funds.

Do not evaluate tracking error in isolation from your specific goal.

If your priority is capturing short-term gold price moves or hedging equity portfolio volatility tactically, liquidity (the ability to enter and exit instantly without a large bid-ask cost) matters as much as, or more than, marginal differences in long-run tracking error. If your priority is long-term, buy-and-hold portfolio allocation, as covered in our earlier gold allocation by age guide, a slightly lower expense ratio and consistent low tracking error compound to a more meaningful difference over a 10-year-plus holding period.

Gold ETF vs Physically Backed Gold Funds vs Futures-Backed Products: Does Structure Matter?

Not all gold-linked exchange-traded products are structured identically, and the structure meaningfully affects how closely and how reliably a given product tracks the spot price of gold.

Physically backed Gold ETFs

This is the dominant structure in India and these hold actual gold bullion in custody and provide investors a beneficial ownership claim on that gold. In most funds, only Authorized Participants can redeem units for physical bars under specific conditions; retail investors typically receive cash on redemption rather than physical metal.

Gold mining equity ETFs

This is a structure more common in international markets, tracking indices of gold mining companies rather than gold itself. These do not hold gold directly at all. Their performance depends on the profitability, production costs, and management decisions of the underlying mining companies, and broader equity market conditions, meaning even when gold prices rise, mining stock-based products can underperform due to factors entirely unrelated to the gold price itself. Indian investors should be careful not to confuse these with physically backed Gold ETFs when researching options, since the underlying exposure is fundamentally different.

Futures-backed gold products

These derive exposure through futures contracts rather than physical holdings. These carry their own distinct tracking considerations, including roll costs (the cost of continuously replacing expiring futures contracts with new ones) and the possibility of a negative roll yield in certain market conditions, additional structural sources of tracking difference that do not apply to a physically backed ETF.

For most Indian retail investors seeking straightforward exposure that closely mirrors domestic gold prices, a large, physically backed Gold ETF with low expense ratio, strong AUM, and transparent, frequent audit reporting remains the most straightforward and well-understood option.

Frequently Asked Questions

1. Why does my Gold ETF sometimes show a slightly different return than the actual gold price that day?

This is the expected, normal operation of tracking error, not a malfunction. Contributing factors include the fund’s expense ratio (deducted continuously from NAV), a small cash buffer the fund holds for redemptions (which does not move with gold prices), and minor timing differences in when the fund manager actually executes gold purchases or sales relative to the reference benchmark. These effects are typically gradual and modest individually, though they compound over long holding periods.

2. Is a Gold ETF that has slightly outperformed physical gold a better fund?

Not necessarily, and in fact this deserves the same scrutiny as underperformance. A Gold ETF’s objective is close, faithful replication of the underlying gold price, not outperformance. A fund that consistently and significantly outperforms its benchmark may indicate an inconsistency or breakdown in its replication methodology rather than superior management, since a passively managed physical-gold fund has no legitimate mechanism to systematically beat the very asset it holds.

3. What changed with SEBI’s 2026 valuation reform, and does it affect my existing Gold ETF holdings?

Following a SEBI circular issued on 26 February 2026, Indian Gold ETFs moved from valuing their NAV based on international LBMA (London) gold prices with manual domestic adjustments, to anchoring NAV directly to domestic spot gold prices. This does not change the underlying gold your fund holds or your ownership of it; it changes the methodology used to calculate the fund’s daily NAV, and is expected to reduce tracking error and inconsistency across different fund houses going forward.

4. Does a Gold ETF’s tracking error include the impact of GST or import duties on gold?

Under the domestic spot price valuation methodology introduced in 2026, these domestic factors, including import duties and applicable taxes, are intended to be reflected directly and consistently in the domestic reference price used for NAV calculation, rather than requiring the kind of inconsistent manual notional adjustments that different fund houses previously applied under the older LBMA-based system.

5. Should I choose a Gold ETF purely based on which one has the lowest historical tracking error?

Tracking error is an important metric, but it should be considered alongside expense ratio, trading liquidity (daily volume and bid-ask spread), and fund size (AUM), particularly if you may need to trade in or out of the position at short notice. A fund with marginally higher historical tracking error but significantly better liquidity may still be the more practical choice depending on your specific investment goal, whether long-term buy-and-hold allocation or shorter-term tactical exposure.

6. Do Gold ETFs hold real, physical gold, or is it just a paper claim?

Physically backed Gold ETFs, the dominant and most common structure in India, do hold actual physical gold bullion (99.5% purity, as mandated by SEBI) in custody with regulated, audited custodians. This is distinct from purely derivative or futures-backed products, which derive exposure through contracts rather than direct physical holdings, and from gold mining equity products, which hold shares in mining companies rather than gold itself.

Key Takeaways

- A Gold ETF tracks gold prices through a creation and redemption mechanism: Authorized Participants create new units when the ETF trades at a premium to NAV and redeem units when it trades at a discount, an arbitrage process that keeps the ETF’s market price closely aligned with the value of its underlying gold holdings.

- Tracking error, the gap between the ETF’s return and gold’s actual price movement, is driven primarily by the fund’s expense ratio, a small cash buffer held for redemptions (typically 1% to 5% of the portfolio), and minor execution timing differences in the fund’s gold purchases.

- SEBI’s February 2026 circular shifted Indian Gold ETF valuation from the international LBMA (London) benchmark, which required inconsistent manual adjustments across fund houses, to direct domestic spot price valuation, a change expected to reduce tracking error industry-wide going forward.

- When comparing funds, look at tracking error across multiple time periods, consider the standard deviation (not just the average) for consistency, and weigh liquidity and expense ratio alongside tracking error rather than in isolation.

- Physically backed Gold ETFs (the dominant Indian structure) hold actual 99.5% purity gold in custody, distinct from gold mining equity products (which track mining company shares, not gold itself) and futures-backed products (which carry additional roll-cost considerations).

- An ETF that significantly outperforms physical gold deserves the same scrutiny as one that underperforms it, since both can indicate a breakdown in the fund’s replication strategy rather than genuinely superior tracking.

Sources: ICICI Direct: Gold ETF, Meaning, How It Works, Price Factors and Tracking Error, April 2026; FinancialContent: Gold Standard 2.0, India Decouples ETF Valuation from London Benchmarks in Regulatory Landmark, April 2026; Finology: Best Gold ETF in India 2026, Top Funds, Returns and Tax Guide, April 2026; TMGM: Top 5 Best Gold ETF in India for 2026, May 2026.

This article is for general financial education only and does not constitute investment advice. Past performance does not guarantee future returns. Consult a SEBI-registered investment advisor before making portfolio decisions, and always review the fund’s latest scheme documents before investing.