Quick summary: From 1 July 2026, a revised version of the RBI’s grievance redressal mechanism, the Reserve Bank-Integrated Ombudsman Scheme (RB-IOS), 2026, has come into force, replacing the earlier 2021 framework. If you have ever struggled with an unauthorised transaction, a delayed refund, an ATM dispute, or poor service from your bank, NBFC, or payment provider, this is the free, government-backed complaint mechanism designed specifically to resolve exactly that kind of issue. The revised scheme brings faster timelines, wider coverage, and, most notably, sharply higher compensation limits than before. This guide explains who is covered, how to actually file a complaint, what timelines apply, and what changed from the old 2021 scheme.

What Is the RBI Integrated Ombudsman Scheme?

The Integrated Ombudsman Scheme is a grievance redressal mechanism operated by the RBI that allows customers to file complaints against regulated financial entities if they face deficiencies in service. It follows the “One Nation, One Ombudsman” principle, meaning customers do not have to identify a specific ombudsman office based on their geographic location; a single, unified national platform handles all complaints regardless of where you live or bank.

The RBI first introduced the Banking Ombudsman Scheme back in 1995 to resolve customer complaints against banks. Over the following decades, the scheme was expanded and eventually consolidated into a single Integrated Ombudsman Scheme in 2021, bringing together what were previously three separate schemes covering banks, NBFCs, and digital transactions. The revised 2026 version supersedes that 2021 framework, refining and strengthening it further.

Filing a complaint under the scheme is completely free of cost, and the process is designed to be simple and non-adversarial: customers may represent themselves throughout, without needing a lawyer.

Which Entities Does the Scheme Cover?

The RB-IOS, 2026 applies broadly across India’s regulated financial sector. It covers:

- Commercial banks

- Regional rural banks

- Scheduled and certain co-operative banks, including urban co-operative banks meeting the prescribed deposit threshold

- Non-Banking Financial Companies (NBFCs) with assets of ₹100 crore and above

- Non-bank Prepaid Payment Instrument (PPI) issuers (this includes many wallet and prepaid card providers)

- Payment system participants

- Credit Information Companies (the bureaus that maintain your CIBIL, Experian, or CRIF records)

- Other regulated entities notified by the RBI under the framework

If your issue is with any of these categories of institutions and relates to a genuine deficiency in service, this scheme is your recourse.

What Kinds of Complaints Can You File?

Customers can file complaints relating to deficiencies in service, and the scope is genuinely broad. Common categories include:

- Unauthorised transactions on your account or card

- ATM and card disputes (failed withdrawals, wrongly debited amounts)

- Digital payment failures, including UPI and other electronic payment issues

- Delays in refunds

- Loan servicing issues (incorrect EMI deductions, foreclosure disputes, documentation problems)

- Credit report errors (incorrect entries in your CIBIL or other bureau records)

- Disputes over charges and fees levied without proper disclosure

- Deposit account problems

- Payment settlement failures

- Harassment by recovery agents

- Any other customer service deficiency by a regulated entity

What is explicitly excluded:

Complaints related to commercial decisions, matters that are sub judice (already before a court), employer-employee disputes, or services outside RBI’s regulatory purview will not be entertained under this scheme.

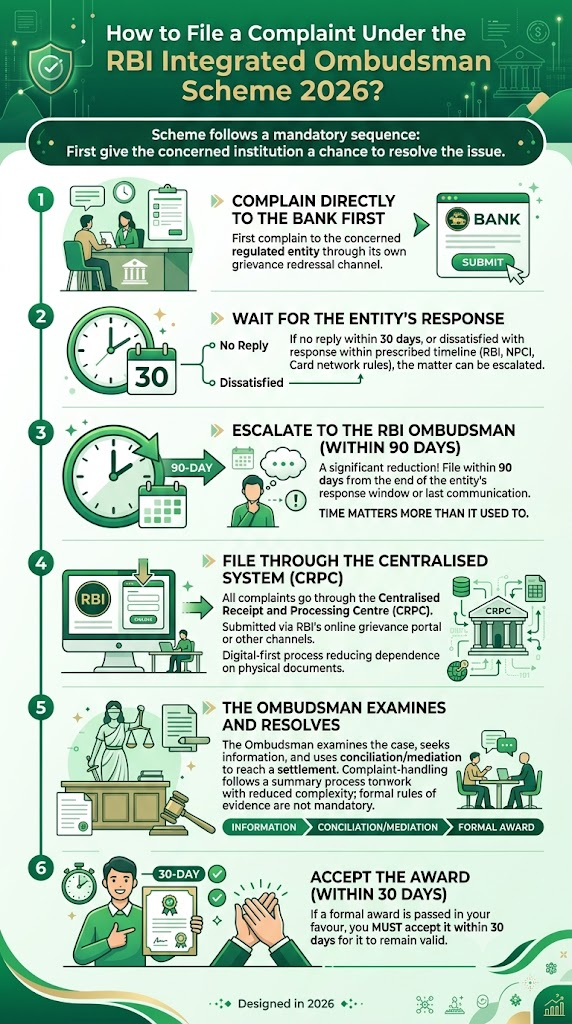

What Is the Correct Process for Filing a Complaint?

The scheme follows a mandatory sequence: you cannot go straight to the RBI Ombudsman without first giving the concerned institution a chance to resolve the issue.

Step 1: Complain directly to the bank or financial institution first.

Before approaching the RBI Ombudsman, customers must lodge a complaint with the concerned regulated entity through its own grievance redressal channel.

Step 2: Wait for the entity’s response.

If the entity does not reply within 30 days, or replies within the timeline prescribed by the RBI, NPCI, or applicable card network rules but the customer remains dissatisfied with the response, the matter can then be escalated.

Step 3: Escalate to the RBI Ombudsman within 90 days.

A complaint must be filed with the RBI Ombudsman within 90 days from the date on which the regulated entity’s response timeline expires, or from the date of the last communication received from the entity, whichever is later. This 90-day window is a significant reduction from the earlier 2021 scheme, which allowed customers a full year to escalate. Under the revised provisions, this timeline has been meaningfully tightened, so acting promptly once the bank’s response window lapses now matters considerably more than it used to.

Step 4: File through the centralised system.

All complaints are processed through the Centralised Receipt and Processing Centre (CRPC), which conducts an initial check before formally registering the complaint. Complaints can be submitted through the RBI’s online grievance portal or other officially notified channels, and the digital-first approach is designed to reduce dependence on physical documentation or in-person submissions, saving both time and cost for consumers.

Step 5: The Ombudsman examines and resolves.

The Ombudsman may seek further information and documents from both the customer and the regulated entity, attempt resolution through conciliation or mediation, and if a settlement cannot be reached, pass a formal award. Under the new scheme, complaint-handling proceedings follow a summary process with reduced procedural complexity; formal rules of evidence are not mandatory, which is intended to ease the burden on complainants and prevent cases from getting stuck on technicalities.

Step 6: Accept the award within 30 days.

If the Ombudsman passes a formal award in your favour, you must accept it within 30 days for it to remain valid.

Who Handles Your Complaint, and What Powers Do They Have?

Under the revised scheme, the RBI appoints one or more of its officers as RBI Ombudsman and Deputy Ombudsman, generally for a three-year term. One of the notable changes in the 2026 scheme is the expanded role given to Deputy Ombudsmen specifically. They can examine complaints relating to deficiencies in service, reject complaints that do not satisfy maintainability criteria, facilitate settlements between parties, assist in expediting complaint resolution, and close complaints falling under specified provisions of the scheme. This expanded delegation is intended to speed up processing by not requiring every single complaint to pass through the Ombudsman personally.

Regulated entities are required to cooperate fully and submit information to the Ombudsman within prescribed timelines as part of this process.

How Much Compensation Can You Actually Get?

This is the single most significant upgrade in the 2026 scheme compared to its predecessor, and it is worth understanding the two separate compensation categories clearly.

Up to ₹30 lakh for consequential financial loss:

If a deficiency in service by the regulated entity caused you a direct, quantifiable financial loss, the Ombudsman can now award compensation of up to ₹30 lakh to cover that loss.

Up to ₹3 lakh for loss of time, expenses, harassment, and mental anguish:

Separately, and in addition to the financial loss compensation above, the Ombudsman can award up to ₹3 lakh specifically for the time you spent pursuing the complaint, expenses you incurred in the process, and any harassment or mental anguish caused by the deficiency in service.

Together, this means a genuinely serious case involving both a substantial financial loss and considerable personal hardship could see compensation running into several lakhs, a materially higher ceiling than what was available under the 2021 scheme.

What Are the Other Major Changes From the 2021 Scheme?

Beyond the headline compensation increase, several structural changes distinguish the 2026 scheme from its predecessor.

Tighter complaint-filing window:

As covered above, the time limit to escalate to the RBI Ombudsman has been reduced from one year (under the 2021 scheme) to 90 days from the expiry of the entity’s response window or the date of the last communication, whichever is later. This is a significant reduction and means customers now need to act considerably faster once they receive (or fail to receive) a response from their bank.

No limit on dispute value:

The revised scheme removes any cap on the underlying value of the dispute itself, meaning complaints involving larger sums are not automatically excluded from the mechanism the way earlier, narrower schemes sometimes constrained matters by value.

Expanded Deputy Ombudsman powers:

As discussed above, Deputy Ombudsmen can now independently examine, reject on maintainability grounds, facilitate settlements, and close specified categories of complaints, a broader delegation than existed previously.

Summary proceedings with relaxed evidentiary rules:

The requirement for formal rules of evidence has been removed for these proceedings, intended to help resolve cases that might otherwise stall on procedural technicalities, particularly benefiting small and medium-value grievances that often got delayed under stricter procedural regimes.

Reinforced compliance obligations on regulated entities:

Banks, NBFCs, and other covered institutions are required to review and align their internal grievance handling and escalation processes to ensure all service-related complaints are covered under the new scheme. Institutions must also provide prior intimation to the RBI’s Consumer Education and Protection Department (CEPD) for any change in the appointment or contact details of their Principal Nodal Officer (the internal official responsible for coordinating with the Ombudsman’s office), and must display the salient features of the scheme, a copy of the RB-IOS 2026 itself, and updated Principal Nodal Officer contact details on their website and at their branches.

What Happens to Complaints Filed Before 1 July 2026?

This is an important transitional detail. Complaints submitted before 1 July 2026 continue to be governed by the provisions of the Integrated Ombudsman Scheme, 2021, not the new 2026 framework. Only new complaints filed from the rollout date onward fall under RB-IOS, 2026. If you already have a pending complaint from before the transition date, its processing timelines, compensation limits, and procedural rules remain those of the 2021 scheme until it is resolved.

Can Someone File a Complaint on Your Behalf?

Customers can represent themselves throughout the process, or appoint an authorised representative to file and pursue the complaint on their behalf. This is particularly useful for senior citizens or persons with disabilities who may find it difficult to navigate the process independently. However, a customer’s lawyer specifically cannot represent them in these proceedings; the authorised representative must be someone other than a practising advocate acting in that professional capacity, consistent with the scheme’s intentionally non-adversarial, informal character.

Why Does This Matter for the Digital Payments Era?

India’s rapid expansion of digital payments and fintech services has increased the need for an effective grievance redressal mechanism, and the coverage of PPI issuers, payment system participants, and credit information companies under this scheme reflects that reality directly. If you have faced a failed UPI transaction that was not reversed promptly, an incorrect entry in your credit report affecting your loan or credit card application, or a dispute with a prepaid wallet provider, these are all now squarely within scope of a single, unified complaint mechanism rather than requiring you to figure out which of several overlapping older frameworks applied to your specific situation.

For related consumer protection changes affecting credit products specifically, see our RBI credit card rules 2026 guide, which covers a parallel set of RBI reforms including anti-mis-selling protections and weekly credit bureau reporting that intersect with the kind of disputes this Ombudsman scheme is designed to resolve.

Frequently Asked Questions

1. Does it cost anything to file a complaint under the RBI Integrated Ombudsman Scheme?

No. Filing a complaint under the scheme is completely free of cost. There is no fee at any stage of the process, from initial filing through to a formal award, if one is issued.

2. Can I go directly to the RBI Ombudsman without first complaining to my bank?

No. You must first lodge a complaint with the concerned regulated entity (your bank, NBFC, or other covered institution) through its own grievance redressal channel. Only if the entity fails to respond within 30 days, or you remain dissatisfied with its response, can you escalate to the RBI Ombudsman.

3. How long do I have to escalate to the RBI Ombudsman once my bank responds?

Under the revised 2026 scheme, you must file with the RBI Ombudsman within 90 days from the date the entity’s response timeline expires, or from the date of its last communication to you, whichever is later. This is a significant reduction from the one-year window that applied under the earlier 2021 scheme, so do not delay once you have received (or failed to receive) a response from your bank.

4. What is the maximum compensation I can receive?

The Ombudsman can award up to ₹30 lakh for consequential financial loss arising from a deficiency in service, plus a separate amount of up to ₹3 lakh for loss of time, expenses, harassment, and mental anguish. These two compensation categories are distinct and can both apply to a single case, depending on the facts.

5. Does the scheme cover NBFCs and payment wallet providers, or only banks?

It covers a wide range of RBI-regulated entities: commercial banks, regional rural banks, certain co-operative banks, eligible NBFCs (with assets of ₹100 crore and above), non-bank Prepaid Payment Instrument issuers, payment system participants, and credit information companies. It is not limited to traditional banks.

6. Can my complaint that I filed in June 2026 still get resolved, or does it fall under the new scheme?

Complaints filed before 1 July 2026 continue to be governed by the Integrated Ombudsman Scheme, 2021, including its procedural rules and compensation limits. Only complaints filed on or after 1 July 2026 fall under the revised RB-IOS, 2026 framework.

7. Can I hire a lawyer to represent me before the RBI Ombudsman?

No, a customer’s lawyer cannot formally represent them in these proceedings. However, you can appoint an authorised representative, which is particularly useful for senior citizens or persons with disabilities, to help file and pursue the complaint on your behalf.

8. What kinds of issues are NOT covered by this scheme?

Complaints related to purely commercial decisions made by the bank, matters already pending before a court, employer-employee disputes, or services that fall outside RBI’s regulatory jurisdiction will not be entertained under this scheme.

Key Takeaways

- The Reserve Bank-Integrated Ombudsman Scheme (RB-IOS), 2026 came into force on 1 July 2026, replacing the earlier 2021 framework, and provides a single, free, “One Nation, One Ombudsman” mechanism for resolving complaints against RBI-regulated entities.

- It covers commercial banks, regional rural banks, certain co-operative banks, eligible NBFCs, PPI issuers, payment system participants, and credit information companies.

- The mandatory process is: complain to the entity first, wait 30 days (or the applicable prescribed period) for a response, then escalate to the RBI Ombudsman within 90 days of the response deadline expiring or the last communication received.

- Compensation limits have increased significantly: up to ₹30 lakh for consequential financial loss, plus up to ₹3 lakh separately for loss of time, expenses, harassment, and mental anguish.

- The complaint-filing window has been tightened from one year to 90 days compared to the 2021 scheme, making prompt escalation more important than before.

- Deputy Ombudsmen now have expanded powers to examine, reject, settle, and close complaints independently, and proceedings follow a summary process with relaxed evidentiary requirements.

- Complaints filed before 1 July 2026 continue under the 2021 scheme’s rules; only complaints filed on or after that date fall under the new RB-IOS, 2026 framework.

- Filing a complaint is entirely free, and customers can represent themselves or appoint an authorised representative (though not a lawyer) throughout the process.

Sources: Business Today: RBI Revamps Customer Grievance Redressal, Here’s What Changes for Bank, NBFC Customers, July 2026; Upstox: New RBI Ombudsman Scheme Explained, How to File a Complaint and Get Up to ₹30 Lakh in Compensation, January 2026; Vinod Kothari Consultants: RBI Integrated Ombudsman Scheme 2026, Key Changes, January 2026; Indian Cooperative: RBI Ombudsman Framework Reduces Complaint Filing Window to 90 Days, January 2026.

This article is for general information only and does not constitute legal advice. For guidance specific to your complaint, refer to the official RBI Integrated Ombudsman Scheme, 2026 document or consult a qualified professional.