Quick summary: Picture this. You are at a medical shop, your bank balance is running low, and the bill is ₹3,500. Instead of panicking or calling someone for money, you simply scan the QR code on the counter and pay using a credit limit your bank has already pre-approved for you, directly inside your PhonePe or Google Pay app. That is what a credit line on UPI does. It is borrowed money you can spend instantly, the same way you spend from your bank account through UPI, without needing a physical credit card.

The Basics: What Is a Credit Line?

Before getting to the UPI part, let us quickly understand what a credit line is.

A credit line (also called a line of credit) is a pre-approved loan limit that a bank or financial institution gives you. You do not get the money in your account upfront. Instead, the bank says: “You can borrow up to ₹X whenever you need it.” You only borrow what you actually use, and you only pay interest on the amount you actually use, not on the entire limit.

Think of it like the borrowing limit on a credit card, but without a physical card. If your credit line limit is ₹30,000 and you use ₹10,000 for a purchase, you pay interest only on ₹10,000. The remaining ₹20,000 sits as available credit until you need it.

So What Is a Credit Line on UPI?

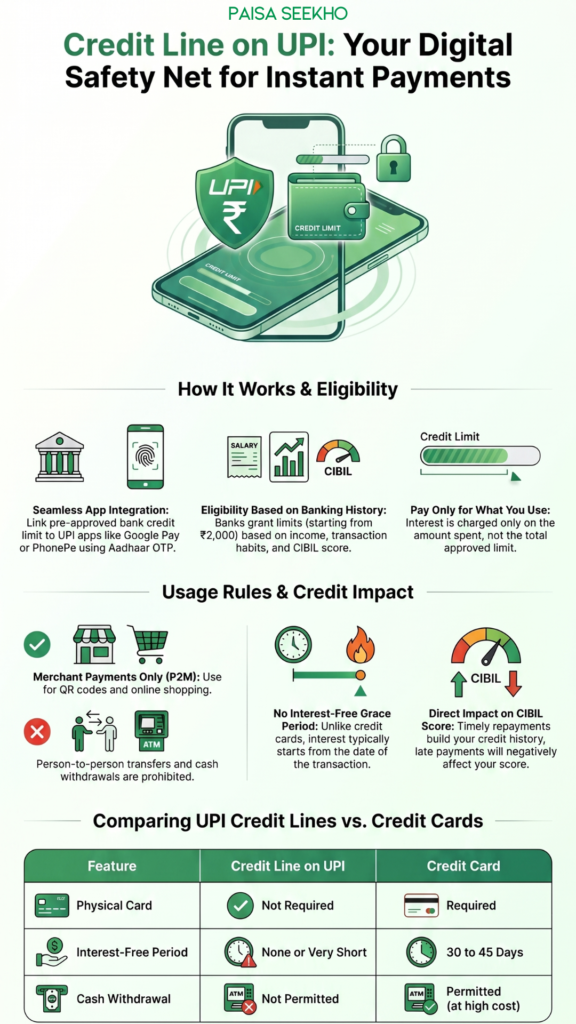

A credit line on UPI takes this concept and plugs it directly into the UPI system you already use every day, on apps like PhonePe, Google Pay, Paytm, and BHIM.

When a bank pre-approves a credit line for you, they give you a special UPI-linked account connected to that credit limit. You add this credit line account to your UPI app, just like you add a bank account. When you make a payment at any merchant (scan a QR code, pay online), you can choose to pay from this credit line account instead of your regular savings account. The money is borrowed from the bank at that moment. You repay it later, based on the terms your bank sets.

The Reserve Bank of India (RBI) officially enabled this feature through its circular dated 4 September 2023 (RBI/2023-24/58), which expanded the scope of UPI to include pre-sanctioned credit lines from Scheduled Commercial Banks as a funding account. The National Payments Corporation of India (NPCI) followed this up with an Operating Circular on 20 September 2023 to lay out the technical rules for banks and UPI apps. The feature went live progressively through late 2023 and 2024, and is now available across most major banks and UPI apps as of 2025-26.

How Does It Work? A Step-by-Step Example

Let us follow Priya, a 26-year-old who works at a small company in Nagpur. She does not have a credit card but her bank (HDFC) has pre-approved her for a credit line on UPI.

Step 1: Approval.

HDFC looks at Priya’s bank account history, salary credits, and credit score. They decide she is eligible for a ₹25,000 credit line.

Step 2: Linking.

Priya opens her Google Pay app, goes to the “Link Credit Line” section, selects HDFC Bank, completes an OTP verification with Aadhaar, and sets a UPI PIN specifically for this credit line account.

Step 3: Making a payment.

At a pharmacy, the bill is ₹2,200. Priya scans the QR code. She sees two options on the payment screen: her savings account (balance ₹800) and her HDFC Credit Line (available limit ₹25,000). She selects the credit line and pays.

Step 4: Repayment.

At the end of the billing cycle (say, by the 5th of next month), Priya receives a bill for ₹2,200 plus any interest or fees as per her bank’s terms. She pays it back through a UPI transfer to her credit line account.

Simple. No card, no separate loan app, no waiting for disbursal.

Who Can Get a Credit Line on UPI?

The eligibility criteria vary by bank, but here are the common requirements:

- You must be at least 18 years of age

- You must have a valid UPI-linked bank account with a participating bank

- Your KYC (Know Your Customer) must be complete with the bank

- A reasonable credit score is required. Many banks look for a CIBIL score of around 650 or above, though this varies

- Banks also look at your income history, banking habits, and existing relationship with them

Since the bank is lending money, they assess your creditworthiness before offering you a credit line. Not everyone who applies will get approved, and the credit limit offered will differ from person to person.

Banks use your UPI transaction history and banking data to make these decisions, which is actually a big deal for financial inclusion. Many people in tier 2 and tier 3 cities who do not have a credit card history can still build a credit line eligibility through consistent UPI usage and salary credits.

Where Can You Use It?

A credit line on UPI can be used for P2M transactions only, which means Person-to-Merchant payments. In simpler terms, you can use it to pay:

- Shops and kirana stores that accept UPI (QR code payments)

- Online websites and apps that accept UPI

- Bill payments, subscriptions, food delivery, and so on

There are two things you cannot do with a credit line on UPI:

- Transfer money to another person (P2P). You cannot send money from your credit line to a friend or family member’s account. It is designed only for paying merchants.

- Withdraw cash. As per NPCI rules, acquirers (banks and merchants) must ensure cash withdrawals at merchant points are not permitted through credit line UPI accounts.

This restriction is intentional. The RBI’s design ensures the feature is used for genuine purchases, not for cash-based workarounds.

How Much Can You Borrow?

The credit limit depends entirely on what your bank decides to offer you. Limits can be as low as ₹2,000 for new-to-credit users and can go up to ₹60,000 or more for users with a stronger credit profile.

As you use the credit line responsibly and repay on time, banks may increase your limit over time. The system is designed to reward good repayment behaviour.

What Does It Cost?

This is the most important part to understand before you use a credit line on UPI.

What is free:

- Linking your credit line account to a UPI app: no charge

- The transaction itself: no per-transaction fee

What costs money:

- Interest on the amount used: Once you spend from your credit line, that amount is a loan. Interest is charged on the outstanding balance. The rate varies by bank, and each bank must share a Key Fact Statement (KFS) with you at the time of onboarding, listing all charges clearly.

- Late payment fees: If you do not repay by the due date, a late fee is charged. The account may also get locked until dues are cleared.

- Processing fees: Some banks may charge a one-time or annual fee for the credit line facility. Check your bank’s specific terms.

As NPCI has clarified, fees vary by bank, and users should ask their bank about applicable interest rates and charges before activating the credit line.

One important note: interest is usually charged from the date of the transaction. Unlike most credit cards, which offer an interest-free grace period of 30 to 45 days, many UPI credit lines do not offer the same grace period. Always read the terms your bank provides.

The August 2025 Update: Purpose-Based Rules

In July 2025, NPCI issued a new circular (effective 31 August 2025) that brought in a significant new rule: credit line payments through UPI must be used only for the purpose the loan was originally approved for.

What does this mean in practice? If a bank sanctioned your credit line specifically for personal expenses, you cannot use it to make business payments. If a loan was approved for education, the transactions should reflect that. Banks and UPI apps are now required to tag merchants by category (using Merchant Category Codes) so that the system can enforce this end-use requirement.

This may sound technical, but for most everyday users spending on groceries, medicine, utilities, and everyday purchases with a general personal credit line, nothing changes. The rule mainly affects purpose-specific credit lines (like a business loan or an education loan routed through UPI).

The June 2026 RBI Update: Same Rules as Regular Loans

Just recently, on 23 June 2026, the RBI issued a fresh directive with an important clarification. According to Business Standard, the RBI said that all pre-sanctioned credit lines offered through UPI must now follow the same prudential norms (regulatory rules about loan classification, provisioning, and reporting) as the underlying credit product, regardless of whether the credit is delivered through a UPI app or a bank branch.

In plain language: a loan delivered through a UPI app is still a loan. It must be treated exactly the same way by the bank as any other loan of that type. Banks cannot use the UPI delivery channel to give loans that would be regulated differently. This is a move to prevent regulatory shortcuts and ensure that borrowers are protected by the same rules that apply to all lending in India.

For users, this is actually a good thing. It means the credit you access through UPI is fully regulated, just like a regular personal loan or overdraft.

Credit Line on UPI vs Credit Card: What Is the Difference?

Many people wonder whether a credit line on UPI is just a credit card without the plastic. They are similar in some ways but different in important ones.

| Credit Line on UPI | Credit Card | |

| Physical card needed? | No | Yes (usually) |

| Best for | Small-ticket everyday purchases | Large purchases, travel, rewards |

| Interest-free period | Often none or very short | Usually 30 to 45 days |

| Interest rate | Varies by bank; can be higher | Typically 36% to 42% per annum if you carry a balance |

| Credit limit | Usually lower (starts at ₹2,000 to ₹60,000+) | Often higher |

| Cash withdrawal? | Not permitted | Permitted but expensive |

| P2P transfers? | Not permitted | Not applicable |

| Reward points / cashback | Limited or none currently | Rich rewards programs |

| International use? | Not currently | Yes |

| Who it suits | First-time credit users, no credit card holders | Frequent spenders who can repay in full monthly |

The key message: a credit line on UPI is not a replacement for a credit card. It is a complementary tool, especially valuable for people who do not qualify for a credit card yet or who want a simple, small-ticket borrowing option built into their UPI app.

Credit Line on UPI vs Buy Now Pay Later (BNPL)

You may have also seen “Pay Later” options on Swiggy, Amazon, or Flipkart. These are BNPL products, and they are similar to a credit line but with one key difference: most BNPL options work only on specific merchant platforms.

A credit line on UPI, by contrast, works at any merchant that accepts UPI, which in India means practically every shop, restaurant, pharmacy, and online store. That universality is its biggest advantage over BNPL.

How to Get a Credit Line on UPI

Here is the general process, though steps may vary slightly by bank and app:

- Open your UPI app (PhonePe, Google Pay, Paytm, etc.)

- Look for a section called “Credit Line,” “Pay Later,” “Loans,” or something similar

- Select your bank from the list of participating banks

- Complete the credit assessment: submit PAN, Aadhaar, and income details as requested

- Wait for the bank’s approval. This is usually quick, sometimes within minutes for pre-approved users

- Once approved, complete Aadhaar OTP verification and set a separate UPI PIN for the credit line account

- The credit line account now appears as a funding option when you make UPI payments

Dos and Don’ts

Do:

- Use it for genuine short-term needs, like a medical bill or an urgent household expense

- Read the Key Fact Statement (KFS) your bank provides before activating

- Always repay on time to protect your CIBIL score

- Use it to build a credit history if you are new to credit

Do not:

- Use it for non-essential or impulsive purchases just because it feels like “free money”

- Forget the repayment date. Late fees and interest can add up quickly

- Share your UPI PIN for the credit line with anyone

To track your spending across all sources (including credit line repayments), having a good budgeting habit helps. Our guide to personal finance tools for beginners in India covers apps and methods that make tracking easier. Similarly, if you are looking for apps to manage your money on a day-to-day basis, our best free budgeting apps for Indians guide has practical recommendations.

Does It Affect Your Credit Score?

Yes. A credit line on UPI is a credit product, which means it is reported to credit bureaus like CIBIL, Equifax, and CRIF.

Timely repayments will improve your credit score over time. For someone who has never taken a loan or owned a credit card, this can be a useful way to start building a credit history.

Missed or late repayments will hurt your credit score and show up as a negative mark. Defaults are reported to the credit bureau and can affect your ability to get loans, credit cards, or even home loans in the future.

Frequently Asked Questions

1. Is a credit line on UPI the same as having a credit card on UPI?

No. A credit card linked to UPI (like a RuPay credit card) uses your physical credit card account as the funding source. A credit line on UPI is a separate, pre-approved borrowing facility directly linked to your UPI ID, with no physical card involved.

2. Can I transfer money to a friend from my UPI credit line?

No. Credit line on UPI is only for P2M (merchant) payments. You cannot use it to send money to another person.

3. Can I withdraw cash using my UPI credit line?

No. NPCI rules explicitly prohibit cash withdrawals at merchant points through credit line UPI accounts.

4. What happens if I do not repay on time?

Your credit line account may get locked until dues are cleared. Late fees and interest will be charged. The default will also be reported to credit bureaus, which can lower your CIBIL score.

5. Is the credit line on UPI safe?

Yes. The system uses the same UPI security infrastructure: device binding, a separate UPI PIN, and end-to-end encryption. The feature is regulated by RBI and operates within the NPCI framework. Transactions are visible in your app’s transaction history in real time.

6. Can I have credit lines from multiple banks on the same UPI app?

This depends on the bank. Some banks restrict users to one credit line account at a time. Check your bank’s terms for clarity.

7. Will this feature replace credit cards someday?

Probably not entirely, at least not for large-ticket spending, international transactions, or premium rewards usage. But for small, everyday purchases in India, credit lines on UPI are increasingly seen as the more accessible, inclusive alternative. As of 2026, the two products are complementary rather than competitive.

Key Takeaways

- A credit line on UPI is a pre-approved borrowing limit from your bank, linked directly to your UPI app, allowing you to pay merchants even when your bank account balance is low.

- The RBI enabled this feature through its circular dated 4 September 2023. NPCI issued operational guidelines on 20 September 2023.

- It can only be used for merchant payments (P2M). No P2P transfers, no cash withdrawals.

- Linking the account is free. But interest is charged on the amount borrowed, and late fees apply if you miss repayment.

- From August 2025, NPCI requires transactions to match the declared loan purpose (purpose tagging).

- From June 2026, the RBI has directed that all UPI credit lines must follow the same prudential norms as the underlying loan product.

- It is a great tool for first-time credit users, but like all borrowed money, it must be used with discipline and repaid on time.

Sources: Reserve Bank of India Circular RBI/2023-24/58, dated 4 September 2023: Operation of Pre-Sanctioned Credit Lines at Banks through UPI; NPCI Operating Circular UPI-OC-171, dated 20 September 2023: Pre-Sanctioned Credit Lines at Banks through UPI; Business Standard: RBI aligns prudential norms for UPI-linked credit lines with base loans, 23 June 2026; NPCI Circular dated 10 July 2025, effective 31 August 2025: Updated guidelines for UPI credit lines.

This article is for general information only and does not constitute financial advice. For specific guidance on whether a credit line on UPI is right for you, consult your bank or a qualified financial advisor.