Quick summary: Buying a flat or plot worth ₹50 lakh or more? The law puts a tax responsibility on you, the buyer, that most people discover only at the last minute. You must deduct 1% TDS from the amount you pay the seller and deposit it with the government using an online form called Form 26QB. If you skip this, you face penalties and your seller cannot claim their TDS credit when filing their income tax return. This guide explains exactly what Form 26QB is, when it applies, how to file it, and walks through a real example so the numbers make sense.

What Is Form 26QB?

Form 26QB is an online challan-cum-statement filed by a property buyer under Section 194-IA of the Income Tax Act, 1961. The name might sound complicated, but the idea is simple: it is the form through which a buyer simultaneously reports a property TDS deduction to the Income Tax Department and pays that TDS to the government in a single online step.

Think of Form 26QB the way you might think of a payment slip that also includes a report. By submitting it, the buyer does two things at once: tells the government “I bought a property from this person and deducted TDS,” and hands over the TDS money itself.

Once Form 26QB is processed, the TDS credit shows up in the seller’s Form 26AS (their annual tax credit statement), and the buyer can then download a TDS certificate called Form 16B to formally hand over to the seller. Understanding how TDS works in India generally can be useful here. If you are new to how TDS works on your salary, our guide on how your employer calculates your TDS is a good starting point before diving into property-specific rules.

When Does Form 26QB Apply?

Form 26QB is required when all three of the following conditions are met:

- You are buying immovable property (land, building, flat, office, shop, plot) other than agricultural land.

- The seller is a resident Indian. If the seller is an NRI, a completely different set of rules under Section 195 applies, and Form 26QB cannot be used.

- The total sale consideration or stamp duty value is ₹50 lakh or more, whichever is higher.

That third point needs a little unpacking. Until October 2024, TDS was calculated only on the actual sale price agreed between buyer and seller. The Finance Act (No. 2), 2024 changed this from 1 October 2024: TDS is now calculated on the higher of the sale consideration or the stamp duty value (also called the circle rate or ready reckoner value of the property as assessed by the state government).

This rule applies to every type of buyer: individuals, HUFs, companies, partnership firms. There is no category of buyer who is exempt if the conditions above are met.

What Is Agricultural Land?

Agricultural land is excluded from Form 26QB requirements. However, the exclusion only applies to rural agricultural land. Urban agricultural land (land near a municipality or cantonment board with a population above 10,000, or within certain distances from municipal limits) is still covered under Section 194-IA. When in doubt, check the property’s classification carefully.

What is the TDS Rate Under Section 194-IA?

The TDS rate is 1% of the higher of sale consideration or stamp duty value. There are no surcharge or cess additions to this rate.

If the seller does not provide their PAN, the rate jumps to 20% under Section 206AA. Always collect the seller’s PAN before making any payment.

A Worked Example

Let us walk through a real-world example to make all of this concrete.

The situation: Priya is buying a 2BHK flat in Pune from Suresh. The agreed sale price is ₹75,00,000. The stamp duty value of the flat (as per the state government’s circle rate) is ₹82,00,000. Priya pays the full amount in one go. Both buyer and seller are resident Indians. Suresh has provided his PAN.

Step 1: Check if Form 26QB applies. Sale consideration = ₹75,00,000. Stamp duty value = ₹82,00,000. Both are above ₹50,00,000. Section 194-IA applies. Form 26QB must be filed.

Step 2: Calculate TDS. TDS is on the higher of the two values. Here, ₹82,00,000 (stamp duty value) is higher. TDS = 1% of ₹82,00,000 = ₹82,000

Step 3: What Priya pays. Priya deducts ₹82,000 from the payment before handing it over to Suresh. Priya pays Suresh: ₹75,00,000 minus ₹82,000 = ₹74,18,000 Priya deposits ₹82,000 as TDS via Form 26QB.

Step 4: When to file. Say Priya made the payment on 18 March 2026. TDS is deducted on the same day. Form 26QB must be filed within 30 days from the end of March 2026, which is 30 April 2026.

Step 5: What happens next. After Form 26QB is filed and processed (5 to 7 working days), the ₹82,000 TDS credit appears in Suresh’s Form 26AS. Priya then downloads Form 16B from the TRACES portal and gives it to Suresh. Suresh uses this to claim TDS credit when he files his ITR and reports the capital gains from this property sale. If you want to understand how income tax slabs and rates work for individuals, our income tax slabs guide for 2026 covers the latest numbers.

Due Dates at a Glance

| Event | Timeline |

| Deduct TDS from seller’s payment | At the time of payment or credit, whichever is earlier |

| File Form 26QB and deposit TDS | Within 30 days from the end of the month of deduction |

| Download and issue Form 16B to seller | Within 15 days from the due date of Form 26QB |

So if TDS was deducted in March, Form 26QB is due by 30 April, and Form 16B must be given to the seller by 15 May.

How to File Form 26QB: Step by Step

Form 26QB is filed entirely online through the Income Tax Department’s e-filing portal. No TAN is required. You need your PAN and the seller’s PAN.

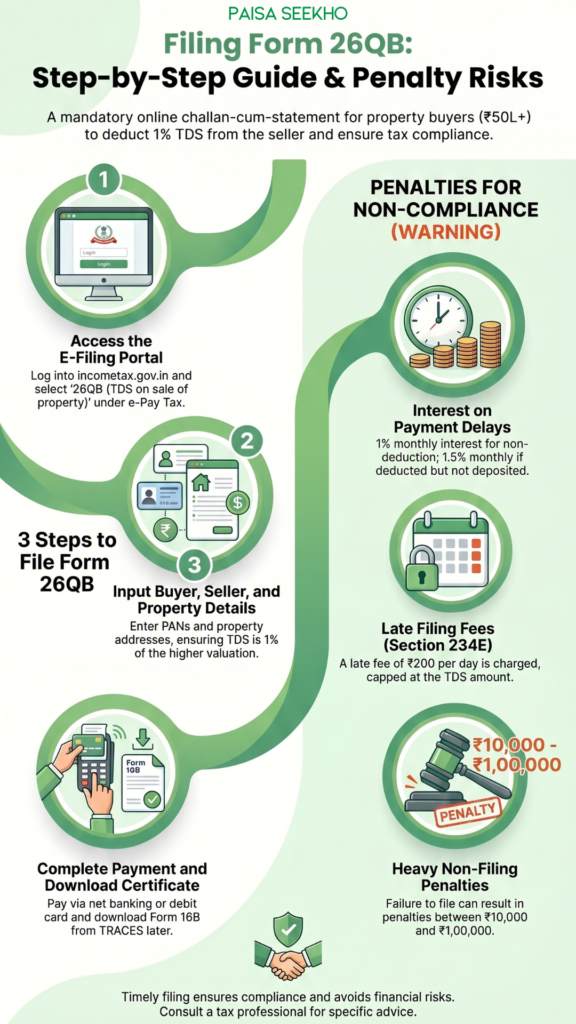

Step 1: Log into the Income Tax e-filing portal at incometax.gov.in using your PAN and password.

Step 2: Go to e-File and click on e-Pay Tax. Under “New Payment,” select 26QB (TDS on sale of property).

Step 3: Fill in the form carefully across three sections:

- Buyer details: Your name, PAN, address, contact details, and residential status.

- Seller details: Seller’s name, PAN, address, and residential status (must be “Resident”).

- Property and payment details: Complete address of the property, nature of property (residential or commercial), total sale consideration, stamp duty value, amount being paid in this installment (if in installments), date of payment/credit, TDS amount (1% of the higher value), and payment date.

Step 4: Choose your payment mode: net banking, debit card, RTGS/NEFT, or pay later (offline challan at an authorised bank).

Step 5: Complete the payment. Once successful, a unique acknowledgement number and a challan are generated. Download and save both immediately. The acknowledgement number is needed to download Form 16B later.

Step 6: After 5 to 7 working days, log into TRACES (tdscpc.gov.in) as a taxpayer and download Form 16B. Enter the assessment year, the seller’s PAN, and the Form 26QB acknowledgement number to generate the certificate.

What If Payment Is Made in Installments?

Installment payments are very common in under-construction projects and builder flats. The rule is:

- TDS must be deducted on each installment at the time of payment.

- A separate Form 26QB must be filed for each installment.

- A separate Form 16B must be issued to the seller for each installment.

This is something many first-time buyers miss. The ₹50 lakh threshold is checked against the total agreed consideration, not the individual installment size. If you are buying a flat worth ₹60 lakh and paying in three installments of ₹20 lakh each, all three installments are subject to TDS because the total price crosses ₹50 lakh. You file three Form 26QBs across the course of the project.

What If There Are Multiple Buyers or Sellers?

This is another area where mistakes happen frequently.

Multiple sellers: A separate Form 26QB must be filed for each buyer-seller combination. If you are buying from two co-owners, you file two Form 26QBs, one for each seller, based on their respective share of the consideration.

Multiple buyers: Similarly, if two buyers are purchasing together, each buyer files a separate Form 26QB for each seller. Two buyers buying from two sellers means four Form 26QB filings in total.

Each buyer is responsible only for their own share of the TDS deduction. If Buyer A is paying 60% and Buyer B is paying 40% of the consideration, each deducts 1% TDS on their proportionate share.

Home Loan Buyers: An Important Note

If you are buying property through a home loan, and the bank disburses money directly to the seller, the TDS obligation still falls entirely on you, the buyer. The bank does not handle Section 194-IA TDS. You must deduct 1% from each disbursement the bank releases to the seller and deposit it via Form 26QB separately before or at the time of each payment.

Penalties for Non-Compliance

Missing Form 26QB compliance is costly. Here is what happens:

| Default | Penalty or Interest |

| TDS not deducted at all | Interest at 1% per month from the date it should have been deducted |

| TDS deducted but not deposited | Interest at 1.5% per month from the date of deduction to the date of deposit |

| Late filing of Form 26QB | Late fee of ₹200 per day under Section 234E, capped at the TDS amount |

| Penalty for non-deduction or non-deposit | Up to 100% of the TDS amount under Section 271C |

| Penalty for non-filing of Form 26QB | ₹10,000 to ₹1,00,000 under Section 271H |

| Not issuing Form 16B on time | ₹100 per day under Section 272A(2)(g) |

If you file within one year of the due date and pay the TDS, interest, and late fee, the Section 271H penalty may be waived. Beyond one year, relief is rarely granted.

What the Seller Needs to Do

If you are the seller, your role is simpler but important:

- Give your PAN to the buyer. Without it, TDS jumps to 20%.

- Check your Form 26AS about a week after the buyer files Form 26QB. The TDS credit should appear in Part F of your Form 26AS.

- Collect Form 16B from the buyer. This is your official TDS certificate.

- Claim the TDS credit in your ITR. When you file your income tax return for the year of the sale, report the capital gains and claim the TDS as a credit in Schedule TDS-2. If the TDS exceeds your tax liability for the year, the excess is refunded. To understand the deductions and exemptions that can reduce your final tax bill, our guide to income tax deductions and sections explains the major options available.

If the TDS is not appearing in your Form 26AS, contact the buyer immediately. Only the buyer can fix it by filing a correction on the TRACES portal.

Corrections to Form 26QB

Corrections can be requested on the TRACES portal, but they are limited in scope and require the seller’s digital consent for most changes. This is why accuracy at the time of filing is critical. Double-check the following before submitting:

- Both PAN numbers (buyer and seller)

- Sale consideration and stamp duty value (enter the right one as the higher value)

- Property address

- Date of payment

A wrong PAN is the most common and most damaging error. It prevents the seller’s TDS credit from appearing in their Form 26AS, which can result in notices and double taxation for the seller.

Form 26QB Is Becoming Form 141

India’s Income Tax Act, 2025, which took effect from 1 April 2026, has renamed and restructured many TDS forms. For property transactions, Form 26QB has been merged into a new consolidated form called Form No. 141. Specifically, property TDS under the new Act is reported through Schedule B of Form 141.

For all payments made on or before 31 March 2026, continue using Form 26QB as described in this article. For payments made from 1 April 2026 onwards (Tax Year 2026-27), use Form 141 Schedule B. The corresponding TDS certificate also changes from Form 16B to Form No. 132. Our article on the April 2026 financial rule changes covers the broader transition to the new Income Tax Act, 2025.

The core obligation remains unchanged: 1% TDS on the higher of sale consideration or stamp duty value, deposited within 30 days of payment, and a certificate issued to the seller within 15 days of the filing deadline.

Form 26QB vs Form 24Q: What Is the Difference?

People sometimes confuse the two forms because both carry “Q” in their name and relate to TDS.

| Form 26QB | Form 24Q | |

| What it covers | TDS on purchase of immovable property | TDS on salary payments by employers |

| Who files it | Property buyer | Employer |

| Legal section | Section 194-IA | Section 192 |

| TAN required? | No, PAN is sufficient | Yes |

| Frequency | Once per payment/installment | Quarterly |

| Certificate issued | Form 16B | Form 16 |

Frequently Asked Questions

1. Do I need a TAN to file Form 26QB?

No. Section 194-IA specifically exempts property buyers from obtaining a TAN. Your PAN is all you need.

2. The property I am buying costs ₹45 lakh. Does Form 26QB apply?

No. The threshold under Section 194-IA is ₹50 lakh. If both the sale consideration and the stamp duty value are below ₹50 lakh, no TDS is required and Form 26QB does not need to be filed.

3. What if the sale price is ₹48 lakh but the stamp duty value is ₹54 lakh?

Form 26QB applies. The law says TDS must be deducted if the consideration or stamp duty value, either one, is ₹50 lakh or more. Since the stamp duty value crosses ₹50 lakh, TDS is triggered on the higher value (₹54 lakh). TDS = 1% of ₹54,00,000 = ₹54,000.

4. I bought an under-construction flat. Do I need to file Form 26QB for each installment?

Yes. A separate Form 26QB must be filed within 30 days of each installment payment. TDS is deducted from each installment proportionately.

5. I already paid the seller the full amount without deducting TDS. What should I do?

File Form 26QB as soon as possible. You will need to pay the TDS amount plus interest under Section 201(1A) at 1% per month for the period of non-deduction. The seller may need to cooperate so you can recover the TDS amount or adjust it from future payments if any remain. Consult a chartered accountant to handle the correction and interest calculation.

6. Can Form 26QB be filed offline?

No. Form 26QB is a fully online process. Offline filing is not available.

7. What if I do not receive Form 16B from the buyer?

If you are the seller, the TDS credit is still reflected in your Form 26AS if the buyer filed Form 26QB correctly. You can file your ITR and claim the credit using Form 26AS even without Form 16B. However, you should still follow up with the buyer as they are legally obligated to issue Form 16B.

Key Takeaways

- Form 26QB is the challan-cum-statement filed by a property buyer under Section 194-IA when purchasing immovable property worth ₹50 lakh or more from a resident seller.

- TDS is 1% of the higher of the sale consideration or the stamp duty value (rule effective from 1 October 2024).

- No TAN is needed. Both buyer and seller must provide their PANs. Without the seller’s PAN, TDS is at 20%.

- Form 26QB must be filed within 30 days from the end of the month in which TDS was deducted.

- After filing, the buyer downloads Form 16B from TRACES and issues it to the seller within 15 days of the Form 26QB due date.

- For installment payments and multiple buyer-seller combinations, a separate Form 26QB is required for each transaction.

- From Tax Year 2026-27 (payments from April 2026 onwards), Form 26QB is replaced by Form No. 141 (Schedule B) under the new Income Tax Act, 2025.

Sources: Income Tax Department, Government of India — TDS on Purchase of Immovable Property; Income Tax Department — Form 16B Download; Finance Act (No. 2), 2024 — Amendment to Section 194-IA effective 1 October 2024.

This article is for general information and does not constitute tax or legal advice. For your specific situation, consult a chartered accountant or tax professional.