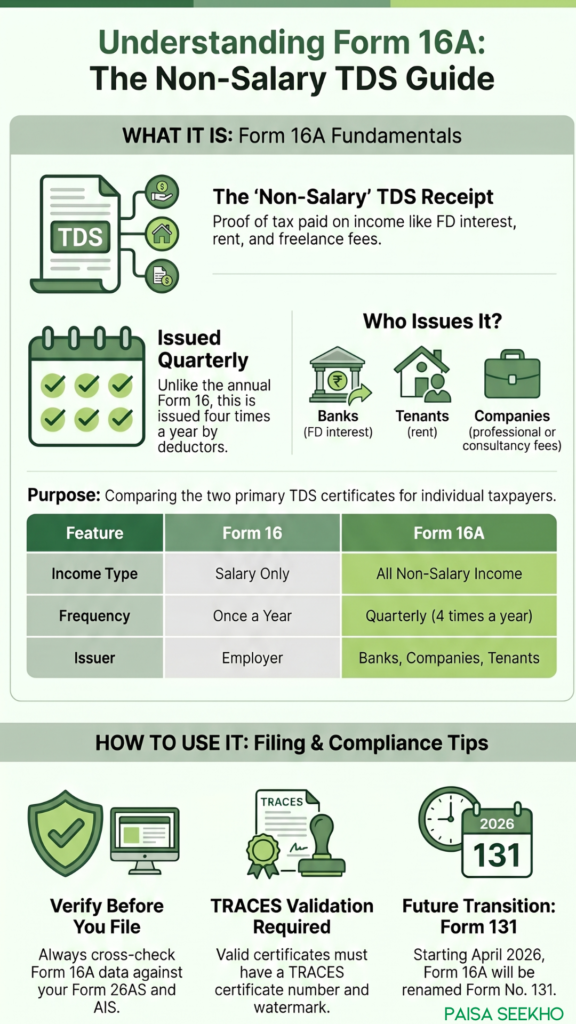

Quick summary: Form 16A is a TDS (Tax Deducted at Source) certificate that covers all income other than salary. When a bank deducts tax on your fixed deposit interest, when a company deducts TDS on rent or professional fees you’ve earned, or when an insurance company deducts tax on a payout — the proof of that deduction comes to you as Form 16A. Unlike Form 16 (which covers salary and is issued once a year), Form 16A is issued quarterly — up to four times a year — and you can receive it from multiple payers. It is critical for anyone who earns income beyond just their salary.

What Is Form 16A?

Form 16A is an official TDS certificate issued under Section 203 of the Income Tax Act, 1961, read with Rule 31(1)(b) of the Income Tax Rules, 1962. It certifies that:

- A specific person or entity (called the deductor) has made a payment to you

- Tax was deducted from that payment at the applicable TDS rate

- That tax has been deposited with the Central Government on your behalf

In plain language: Form 16A is the government-authenticated receipt that proves someone paid tax on your income before handing the rest to you.

Just like Form 16 is a salaried employee’s proof that employer-deducted TDS has been deposited, Form 16A is the equivalent proof for non-salary income — FD interest, rent, freelance fees, contractor payments, insurance commissions, and more.

Who Issues Form 16A?

Form 16A is issued by the deductor — the person, bank, company, or institution that made a payment to you and deducted TDS before doing so. Depending on the type of income, this could be:

- Your bank — for TDS on fixed deposit (FD) or recurring deposit (RD) interest under Section 194A

- Your tenant or their company — for TDS on rent from commercial property under Section 194I

- A company that hired you as a consultant — for TDS on professional or technical service fees under Section 194J

- A company that engaged you as a contractor — for TDS on contractor payments under Section 194C

- An insurance company — for TDS on commission earned (Section 194D) or on policy maturity proceeds (Section 194DA)

- A company paying brokerage or commission — under Section 194H

- EPFO — for TDS on PF withdrawals in some cases

You can receive Form 16A from multiple deductors in the same financial year — one from your bank, one from a company you consulted for, one from a tenant, and so on. Each deductor issues a separate Form 16A for each quarter in which they deducted TDS from your income.

What Income Does Form 16A Cover?

Form 16A is required for TDS deducted under the Section 194 series of the Income Tax Act — which covers all non-salary payments. Here are the most common types of income for which you’re likely to receive a Form 16A:

| Type of Income | Relevant TDS Section | Who Deducts TDS |

| Interest on FDs, RDs (bank, co-op bank, post office) | Section 194A | Bank / post office |

| Interest from other sources (NBFCs, companies) | Section 194A | NBFC / company |

| Rent on land, building, machinery | Section 194I | Tenant (if liable) |

| Professional fees, technical service fees | Section 194J | Company / individual paying you |

| Contractor / sub-contractor payments | Section 194C | Entity that hired you |

| Commission or brokerage | Section 194H | Company paying commission |

| Insurance commission | Section 194D | Insurance company |

| Life insurance policy maturity proceeds | Section 194DA | Insurance company |

| Dividend income | Section 194 | Listed company |

| PF withdrawal (in certain cases) | Section 192A | EPFO |

Note that if your FD interest is below the applicable TDS threshold (₹50,000 for general taxpayers or ₹1,00,000 for senior citizens for FY 2025-26), TDS will not be deducted and no Form 16A will be issued for that bank.

What Does Form 16A Contain?

Form 16A is a standardised document generated exclusively from the TRACES portal (the Income Tax Department’s TDS system at tdscpc.gov.in). It contains:

- Name, address, and TAN of the deductor (the entity paying you)

- Name and PAN of the deductee (you, the income earner)

- Assessment Year for which the certificate applies

- Nature of payment — the type of income (e.g., “Interest other than interest on securities” or “Professional fees”)

- The TDS section under which deduction was made

- Amount paid or credited — the gross amount paid to you before TDS

- Amount of TDS deducted — the tax cut from your payment

- Date of deduction and date of deposit with the government

- Challan Identification Number (CIN) — proof of the specific government payment through which TDS was deposited

- A unique certificate number generated by TRACES

This last point matters: a valid Form 16A must always have a TRACES certificate number. A document prepared manually by the deductor — without this number and without the TRACES watermark — is not a valid TDS certificate and will not support your TDS credit claim during ITR processing.

When Is Form 16A Issued?

Form 16A is a quarterly certificate, not annual. The deductor must issue it within 15 days from the due date for filing the quarterly TDS return (Form 26Q for domestic non-salary payments) for that quarter.

The due dates for Form 16A issuance for FY 2025-26 are:

| Quarter | Period | Form 26Q Due Date | Form 16A Due By |

| Q1 | April – June 2025 | 31 July 2025 | 15 August 2025 |

| Q2 | July – September 2025 | 31 October 2025 | 15 November 2025 |

| Q3 | October – December 2025 | 31 January 2026* | 15 February 2026* |

| Q4 | January – March 2026 | 31 May 2026 | 15 June 2026 |

*The Q3 FY 2025-26 deadline was extended by CBDT Circular No. 02/2026.

If you’re a freelancer who received professional fees from a company, or if you hold FDs in a bank that deducted TDS — you should receive a Form 16A for each quarter in which TDS was deducted. By the end of the financial year, you could have up to four Form 16A certificates from a single deductor, covering each quarter separately.

Why Does Form 16A Matter for Your ITR?

Every rupee of TDS deducted from your income and deposited with the government is a credit against your final tax liability. When you file your ITR, this credit reduces how much tax you owe — or increases your refund.

But you only get this credit if the TDS is:

- Correctly reported by the deductor in their quarterly TDS return, and

- Matched against your PAN in the government’s records

Form 16A is your document to verify both of these things. It tells you exactly how much TDS has been deducted and deposited under your PAN, quarter by quarter, for each source of non-salary income.

Without cross-checking Form 16A, you risk:

- Missing out on TDS credit you’re entitled to

- Paying tax twice on income where TDS was already deducted

- Mismatches with Form 26AS that could trigger notices from the Income Tax Department

How to Use Form 16A While Filing Your ITR

Here is how to practically use Form 16A when it’s ITR filing time:

Step 1 — Collect all Form 16As.

Gather every Form 16A you’ve received during the financial year — from your bank, from any company that paid you freelance or professional fees, from your tenant’s company, from your insurance company, etc. Remember: each deductor issues a separate Form 16A for each quarter.

Step 2 — Cross-check with Form 26AS and AIS.

Log into the Income Tax Department’s e-filing portal (incometax.gov.in) and check your Form 26AS (Consolidated Tax Credit Statement) and your Annual Information Statement (AIS). Every TDS entry shown in your Form 16A certificates should appear in Form 26AS/AIS as well.

Step 3 — Resolve any mismatches before filing.

If a TDS amount shown in Form 16A is missing from or different in Form 26AS, it could mean the deductor reported your PAN incorrectly, or didn’t file the return, or deposited an incorrect amount. In this case, contact the deductor and ask them to file a correction TDS return. Do not file your ITR until this is resolved — claiming a TDS credit that isn’t in Form 26AS will likely be disallowed, and you’ll need to pay the tax again or face a notice.

Step 4 — Enter TDS details in Schedule TDS-2 of your ITR.

In the ITR form you file, TDS on non-salary income goes into Schedule TDS-2 (as opposed to Schedule TDS-1 which is for salary TDS). Enter the TAN of each deductor, the income amount, and the TDS deducted, as shown in the respective Form 16A.

Step 5 — Report the income as well.

Form 16A tells you the TDS was deducted — but you must also report the underlying income in your ITR. For example, FD interest goes into “Income from Other Sources,” rental income goes into “Income from House Property,” and professional fees may go into “Income from Business or Profession” or “Income from Other Sources,” depending on your situation. TDS certificates do not replace income reporting — they only record the tax already paid on that income.

Form 16A vs Form 16: Key Differences

| Form 16 | Form 16A | |

| Type of income covered | Salary only | All income other than salary |

| Issued by | Employer | Banks, companies, insurance firms, tenants, others |

| Issued how often | Once a year | Once per quarter (up to 4 times a year) |

| Legal basis | Section 203, Rule 31(1)(a) | Section 203, Rule 31(1)(b) |

| TDS return it’s based on | Form 24Q (quarterly salary TDS return) | Form 26Q (non-salary TDS to residents) or Form 27Q (to non-residents) |

| Contains salary breakdown? | Yes (in Part B) | No — only shows payment amount and TDS |

| Contains tax regime details? | Yes (in Part B) | No |

| How many per year | 1 per employer | Multiple — one per quarter, per deductor |

| Generated from | TRACES portal | TRACES portal |

Common Mistakes to Avoid

Not collecting Form 16A from your bank.

FD interest is the most commonly missed source. Banks issue Form 16A quarterly if TDS was deducted. Check with every bank where you hold an FD or RD.

Filing ITR before Form 16A figures are reflected in Form 26AS.

The Q4 Form 26Q is due by 31 May 2026. TRACES takes a few days to process it. Filing in early June without waiting for the data to update can result in an incomplete picture of your TDS credits.

Ignoring small Form 16As.

Even a TDS certificate for ₹500 deducted on a small commission payment should be reported. Omitting income — even inadvertently — can lead to a tax notice.

Accepting a manually prepared Form 16A.

A genuine Form 16A always comes from the TRACES portal with a certificate number and digital signature. A document prepared in Word or Excel by the deductor has no legal standing. Insist on the TRACES-generated version.

Assuming Form 26AS will automatically handle everything.

While the IT portal pre-fills some details from your TDS data, always verify the pre-filled figures against your actual Form 16A certificates. Errors in the deductor’s return can cause gaps.

What If You Don’t Receive Form 16A?

If TDS was deducted but you haven’t received Form 16A from a deductor:

- Check Form 26AS first — if the TDS credit is showing there, your return filing isn’t blocked, though getting the certificate is still advisable.

- Contact the deductor (bank, company, tenant, etc.) and request they issue it. It’s their legal obligation.

- If the deductor refuses or cannot be contacted, you can still file your ITR using your Form 26AS data. However, you can also report non-issuance to the Income Tax Department — as per the TRACES FAQ, it is the duty of every person deducting tax to issue a TDS certificate, and failure to do so is a compliance violation.

- If the TDS is not in Form 26AS — the deductor may not have deposited it. This is a more serious issue. Report it to the Income Tax Department, as TDS deducted but not deposited means the government never received the money despite it being cut from your payment.

Important: Form 16A Is Becoming Form 131

Under India’s Income Tax Act, 2025 (effective from 1 April 2026), Form 16A is being renamed Form No. 131. According to the Income Tax Department’s official FAQ on Form No. 131:

- Form No. 131 is the new TDS certificate for non-salary income under Section 395(4)(a) of the Income Tax Act, 2025, which corresponds to the old Section 203

- The applicable rule changes from Rule 31 to Rule 215(1) of the Income Tax Rules, 2026

- The quarterly TDS return it’s based on changes from Form 26Q to Form No. 140/144 under the new framework

- The structure and purpose remain the same: it is still a TRACES-generated certificate issued quarterly by each deductor

- A duplicate Form 131 can be issued if the original is lost, though the deductor must mark it as a duplicate

For FY 2025-26 (income earned up to 31 March 2026), you continue to receive Form 16A as usual. Form 131 applies from Tax Year 2026-27 (income earned from April 2026 onwards), for certificates issued in 2027.

Frequently Asked Questions (FAQs)

1. Is Form 16A the same as Form 16?

No. Form 16 covers only salary income and is issued once a year by your employer. Form 16A covers non-salary income (interest, rent, professional fees, etc.) and is issued quarterly by any entity that deducts TDS from your payments.

2. Can I download Form 16A myself from the TRACES portal?

Not directly. Form 16A is downloaded by the deductor (the bank, company, or other entity) and then provided to you. However, you can log into the TRACES portal as a taxpayer/deductee to verify that your TDS credits are being reflected, or download a statement of TDS credited to your PAN.

3. I have FDs in three different banks. How many Form 16As will I receive?

Each bank that deducted TDS on your FD interest will issue you a separate Form 16A for each quarter in which they deducted TDS. So if all three banks deducted TDS in all four quarters, you could receive up to 12 Form 16A certificates. If a bank’s total interest paid to you stayed below the TDS threshold, no TDS and no Form 16A will be generated.

4. What should I do if there’s a mismatch between Form 16A and Form 26AS?

Contact the deductor immediately. They need to file a correction TDS return to fix the mismatch. Claim only what appears correctly in Form 26AS. Don’t file your ITR with an unresolved mismatch.

5. Do I need to attach Form 16A to my ITR when filing online?

No. Form 16A does not need to be uploaded or attached when filing your ITR online. You use it to fill in the correct figures in your ITR form, particularly in Schedule TDS-2. Keep the physical or digital certificate for your records.

6. My bank deducted TDS on my FD interest but my total income is below the taxable limit. What should I do?

You can claim a refund of the TDS by filing your ITR. If you submit Form 15G (for individuals below 60 years) or Form 15H (for senior citizens) to your bank at the start of the financial year — and are eligible — the bank won’t deduct TDS in the first place.

7. Is Form 16A valid as income proof for loan applications?

It depends on the lender. Form 16A shows non-salary income and the TDS deducted on it. Banks and lenders primarily look at Form 16 (salary) for loan assessment, but Form 16A can support a fuller income picture — especially for freelancers, consultants, or those with significant rental income.

Key Takeaways

- Form 16A is the quarterly TDS certificate for non-salary income — FD interest, rent, professional fees, contractor payments, commission, insurance payouts, and more.

- It is issued under Section 203 of the Income Tax Act, 1961 and generated exclusively from the TRACES portal — a manually typed Form 16A has no legal standing.

- Form 16A is issued within 15 days of the quarterly Form 26Q due date — so up to four certificates per year from each deductor.

- For FY 2025-26, Q4 Form 16As must be issued by 15 June 2026.

- Always cross-check Form 16A against Form 26AS before filing your ITR. Claim only TDS that appears in Form 26AS — a mismatch must be corrected by the deductor first.

- Use Form 16A details in Schedule TDS-2 of your ITR; also separately report the underlying income in the right schedule.

- From Tax Year 2026-27 (income from April 2026), Form 16A will be renamed Form No. 131 under the Income Tax Act, 2025. For FY 2025-26 filings, Form 16A remains unchanged.

Sources: Income Tax Department, Government of India — Form 16 and Form 16A; Income Tax Department — Form No. 131 (Earlier Form No. 16A) FAQ; TRACES — Form 16/16A FAQ.

This article is for general information and does not constitute tax advice. For your specific situation, consult a chartered accountant or tax professional.