Quick summary: Form 12BB is a simple declaration you submit to your employer (not the tax department) to claim tax benefits like HRA, LTA, home loan interest, and deductions under Section 80C and similar sections. Your employer uses it to calculate how much tax (TDS) to deduct from your monthly salary. Get it wrong or skip it, and your employer will deduct more tax than necessary, money you’d have to claim back later while filing your ITR.

This guide explains what Form 12BB covers, who needs to file it, what proof you need, and how to avoid the common mistakes that cost people money every year.

What Is Form 12BB?

Form 12BB is a statement that salaried employees submit to their employer, listing the investments and expenses they’ve made during the financial year that qualify for tax deductions or exemptions. Based on this form (and the evidence attached to it), your employer calculates your estimated annual tax liability and deducts TDS (Tax Deducted at Source) from your salary every month accordingly.

Think of it this way: your employer doesn’t automatically know about your rent payments, your insurance premiums, or your home loan. Form 12BB is how you tell them, formally and with proof, so they can factor these into your tax calculation instead of deducting tax on your full salary.

Why Does Form 12BB Exist?

Before Form 12BB, there was no standard format for declaring these investments to employers, which led to inconsistency. The Income Tax Department fixed this by introducing Rule 26C of the Income Tax Rules, requiring employees to furnish evidence of their claims in a prescribed format, Form 12BB, under Section 192(2D) of the Income Tax Act, which requires employers to obtain proof of deductions before computing TDS on salary.

Is Form 12BB Mandatory?

Form 12BB itself is not mandatory in the sense that you’re never forced to file it. But it is mandatory if you want your employer to factor in any tax deductions or exemptions while calculating your TDS. If you don’t submit it, your employer will deduct tax on your salary without considering any of your investments, rent payments, or other eligible expenses, meaning more tax cut from your monthly paycheck.

You can still claim those deductions later while filing your own Income Tax Return, but that means waiting longer for your money (in the form of a refund) instead of having lower TDS deducted right away.

One thing Form 12BB does not cover: the standard deduction. This deduction is automatically applied for every salaried employee and pensioner, you don’t need to declare it separately in Form 12BB or any other form.

What’s Included in Form 12BB?

Form 12BB is structured around four main categories of claims:

| Section | What It Covers | Supporting Evidence Typically Needed |

| House Rent Allowance (HRA) | Rent paid to your landlord, along with the landlord’s name, address, and PAN | Rent receipts or rent agreement; landlord’s PAN if total annual rent exceeds ₹1,00,000 |

| Leave Travel Allowance/Concession (LTA/LTC) | Travel expenses incurred for leave travel, eligible for exemption | Travel tickets, boarding passes, or other documents supporting the LTC/LTA claim |

| Interest on Home Loan | Interest paid or payable on a housing loan, along with lender details | Loan agreement and interest certificate from the lender |

| Chapter VI-A Deductions | Investments and expenses under sections like 80C (PPF, ELSS, life insurance premiums, etc.), 80D (health insurance), 80CCC, 80CCD, and similar | Investment proofs, premium receipts, or related documents |

A closer look at each section

1. House Rent Allowance (HRA):

If you live in rented accommodation and receive HRA as part of your salary, you can claim exemption under Section 10(13A) by declaring the rent paid, your landlord’s details, and their PAN (mandatory if your total rent for the year crosses ₹1,00,000).

2. Leave Travel Allowance:

If your salary structure includes LTA and you’ve travelled within India during the relevant period, you can claim exemption on the travel cost (subject to conditions under the Income Tax Act).

3. Interest on Borrowed Capital (Home Loan):

If you’re repaying a home loan, the interest portion (not the principal) is eligible for deduction under Section 24(b), up to ₹2,00,000 for a self-occupied property, subject to conditions.

4. Chapter VI-A Deductions:

This is the broadest category, covering popular tax-saving instruments like:

- Section 80C, life insurance premiums, PPF, ELSS mutual funds, children’s tuition fees, principal repayment of home loan, and more (overall limit of ₹1,50,000)

- Section 80CCC and 80CCD, pension scheme and NPS contributions

- Section 80D, health insurance premiums

When Should You Submit Form 12BB?

The process typically happens in two stages over the financial year:

- At the start of the financial year (around April):

Many employers ask for a rough, estimated declaration of your planned investments and expenses for the year. This helps them calculate an approximate monthly TDS so you’re not hit with a large deduction later.

- Towards the end of the financial year (usually December to February):

You submit the actual Form 12BB along with proof of the investments and expenses you’ve genuinely made, not just planned. This is when your employer finalises your TDS calculation for the year.

Employers generally set internal deadlines (often in January or February) so that the last one or two months of payroll can reflect your final, accurate tax liability. Missing this internal deadline usually means your employer proceeds without considering your claims, and any extra TDS deducted would have to be claimed back as a refund when you file your ITR.

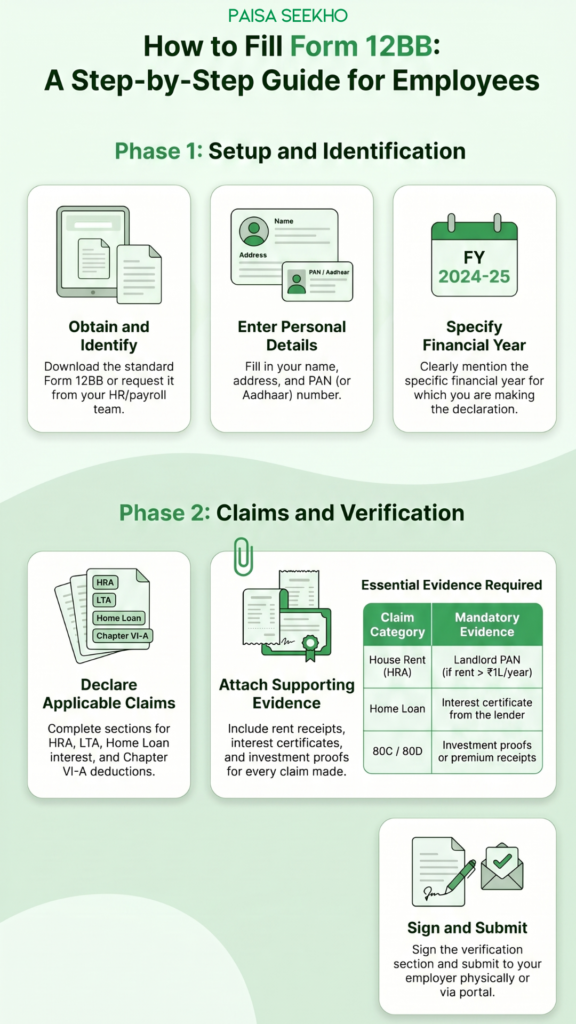

How to Fill Form 12BB: Step-by-Step

- Get the form from your employer’s HR/payroll team, or download the standard format (Form No. 12BB under Rule 26C).

- Fill in your personal details, name, address, and PAN (or Aadhaar) number.

- Mention the financial year for which you’re making the declaration.

- Go section by section and declare only what’s actually applicable to you, HRA, LTA, home loan interest, and Chapter VI-A deductions.

- Attach the supporting evidence for each claim, rent receipts, loan interest certificates, investment proofs, insurance premium receipts, and so on.

- Sign and date the verification section, certifying that the information provided is true and complete.

- Submit it to your employer, either physically or, if your company has a payroll portal, electronically.

You do not need to submit Form 12BB to the Income Tax Department directly, it stays entirely between you and your employer.

What Happens If You Don’t Submit Form 12BB

If you don’t submit any claims through Form 12BB, your employer will calculate TDS based purely on your salary, without factoring in any deductions or exemptions you might be eligible for. This usually results in higher monthly tax deductions than necessary.

The good news: this doesn’t mean you lose those deductions permanently. You can still claim them when you file your own Income Tax Return, and if you’ve overpaid tax through TDS, you’ll get the excess back as a refund. The downside is simply that your money sits with the tax department for longer instead of staying in your monthly salary.

Form 12BB and the Old vs New Tax Regime

This is an important point many salaried employees miss. Form 12BB’s usefulness depends heavily on which tax regime you (or your employer, by default) are computing your TDS under:

- Old tax regime: All four sections of Form 12BB are relevant, HRA, LTA, home loan interest, and Chapter VI-A deductions can all reduce your taxable income.

- New tax regime (the default regime today): Most of these deductions and exemptions are not allowed. HRA, LTA, home loan interest on a self-occupied property, and most Chapter VI-A deductions (except a few like the employer’s NPS contribution under Section 80CCD(2)) cannot be claimed. So Form 12BB has very limited use if you’re under the new regime.

For context: the standard deduction for FY 2025-26 is ₹75,000 under the new tax regime and ₹50,000 under the old tax regime, and this is applied automatically either way, without needing a Form 12BB declaration.

If you want your employer to compute your TDS under the old regime so that your Form 12BB claims actually count, you need to communicate this preference to your employer (and, if you have business or professional income, you may separately need to file Form 10-IEA with the tax department, that’s a different process from Form 12BB).

Important: Form 12BB Is Becoming Form No. 124

Similar to several other income tax forms, Form 12BB is being renumbered under India’s new Income Tax Act, 2025 and the accompanying Income Tax Rules, 2026, which take effect from 1 April 2026. Under the new framework:

- Form 12BB is renamed Form No. 124

- The corresponding section changes from Section 192 (old Act) to Section 392(5)(b) (new Act)

- The corresponding rule changes from Rule 26C to Rule 205

According to the Income Tax Department’s own guidance on Form No. 124, the purpose and structure remain largely similar, it’s still a statement furnished by an employee to the employer to claim deductions, exemptions, and allowances like HRA, LTA, home loan interest, and investment-related deductions, along with supporting evidence. The form now has two clearly defined parts: Part A for employee details, and Part B for the specific tax benefits being claimed, with relevant annexures.

For most salaried employees filing for FY 2025-26 (the year ending 31 March 2026), Form 12BB under the old framework continues to apply. Form No. 124 becomes relevant for income earned from FY 2026-27 onwards, under the new Act.

Common Mistakes to Avoid

- Submitting an estimate without following up with proof. Your initial declaration at the start of the year is just an estimate, you still need to submit actual evidence later for it to count.

- Forgetting the landlord’s PAN. If your annual rent exceeds ₹1,00,000, your landlord’s PAN is mandatory for your HRA claim to be accepted.

- Mixing up principal and interest on home loans. Only the interest portion goes in Form 12BB’s home loan section; principal repayment is claimed separately under Section 80C.

- Declaring deductions not allowed under your chosen regime. If your employer is computing TDS under the new regime, most Form 12BB claims (other than a few exceptions) won’t have any effect.

- Missing your employer’s internal deadline. Each company sets its own cutoff (often January–February) for final proof submission, missing it usually means losing the benefit for that year’s TDS calculation.

Frequently Asked Questions

1. Do I need to submit Form 12BB to the Income Tax Department?

No. Form 12BB is submitted only to your employer. It is not filed with or uploaded to the income tax e-filing portal.

2. Is Form 12BB compulsory for every salaried employee?

It’s only required if you want your employer to consider deductions or exemptions while calculating your TDS. If you don’t claim anything, you don’t need to file it, though you’ll likely have more TDS deducted as a result.

3. What if I forget to submit proof by my employer’s deadline?

Your employer will calculate TDS without those deductions. You can still claim them later while filing your ITR and get any excess tax refunded.

4. Is the landlord’s PAN always required for an HRA claim?

It’s mandatory only if the total rent paid during the year exceeds ₹1,00,000. Below that threshold, it’s not compulsory.

5. Does Form 12BB matter if I’m under the new tax regime?

Its relevance is very limited under the new regime, since most deductions like HRA, LTA, home loan interest, and Chapter VI-A benefits aren’t allowed there. The standard deduction is applied automatically regardless.

6. Can I revise Form 12BB if my investments change during the year?

Yes. If your actual investments or expenses differ from your initial estimate, you can submit a revised or updated Form 12BB with the correct figures and supporting proof.

7. Will Form 12BB still exist in the future?

The form itself will be renamed Form No. 124 under the Income Tax Act, 2025, applicable from FY 2026-27 onwards. For now, salaried employees should continue using Form 12BB as usual.

Key Takeaways

- Form 12BB is a declaration you give to your employer, not the tax department, listing your eligible investments and expenses for tax purposes.

- It covers four broad areas: HRA, LTA, home loan interest, and Chapter VI-A deductions (like 80C and 80D).

- It’s not strictly “mandatory,” but skipping it means more TDS is deducted from your salary, you’d need to claim it back later via your ITR refund.

- Its value depends heavily on your tax regime: it matters a lot under the old regime, and very little under the new (default) regime.

- From FY 2026-27 onwards, Form 12BB will be replaced by Form No. 124 under the new Income Tax Act, 2025, but for now, continue using Form 12BB as usual.

Sources: Income Tax Department, Government of India – Form No. 124 (Earlier Form No. 12BB) FAQs; Income Tax Department – Rule 26C, Income Tax Rules; Income Tax Department – Form No. 12BB; News On Air (Prasar Bharati/Government of India) – Standard Deduction for salaried employees increased to ₹75,000 under new tax regime.

This article is for general information and does not constitute tax advice. For your specific situation, consult a chartered accountant or tax professional.